Ritik Goyal

@rpgoyal_

Followers

1,689

Following

341

Media

116

Statuses

1,158

Explore trending content on Musk Viewer

#LCDLF4

• 231987 Tweets

Cauca

• 140455 Tweets

Costello

• 107797 Tweets

Romeh

• 73607 Tweets

#WWERaw

• 51664 Tweets

Lupillo

• 49138 Tweets

Maripily

• 40287 Tweets

SAROCHA REBECCA ON RED CARPET

• 35632 Tweets

#ラヴィット

• 30050 Tweets

FELIX ENAMORA A BARCELONA

• 29735 Tweets

STRAY KIDS HITS HOT100

• 26881 Tweets

BLINDAJE FURIOSO

• 25290 Tweets

Scarlett Johansson

• 23954 Tweets

定額減税

• 20160 Tweets

ビットコイン

• 14013 Tweets

WELCOME TREASURE TO THAILAND

• 13994 Tweets

給与明細

• 11458 Tweets

Fani Willis

• 11347 Tweets

金額明記

• 10795 Tweets

Lyra

• 10790 Tweets

Pinned Tweet

The Fed Does Not Exist

4

8

69

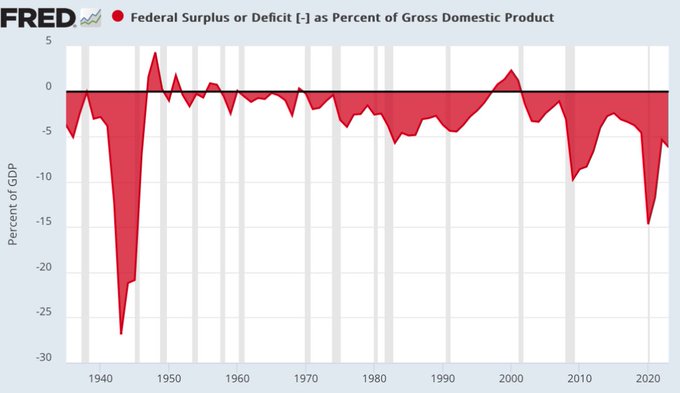

Unintentional endorsement of running a budget deficit

When people say that the economy is super strong, please understand…

We are running a HISTORIC deficit.

6.2% of GDP. Never seen before outside of WW2, the GFC or Covid.

If we weren’t running this deficit and balanced the budget, or even got close, GDP would collapse.

104

434

2K

6

40

190

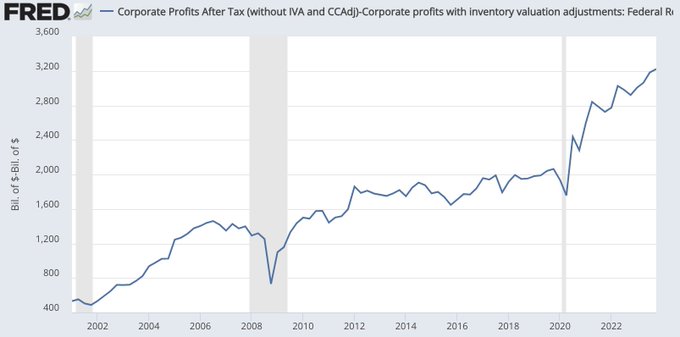

Since Q4 2022, corporate profits have risen every quarter.

At some point this will be understood as a case of rate hikes supporting the private sector, not the private sector overcoming rate hikes.

12

7

74

2020-24 was a validation of MMT's claims:

- The government had no issues spending trillions of dollars in a month

- That spending was able to get inflation up to target (unlike the 2010s)

- That spending helped Real GDP print higher than the IMF's 5yr forecast from 2019 for the

People who believe in the infinite money tree fascinate me.

If I had such a heterodox and counterintuitive view of the world and just witnessed a major case study counter to my view, I might be a bit less condescending to those with a more mainstream view.

24

7

78

9

14

60

Deficits never need to be "plugged". The spending itself "plugs" the deficit.

2

18

49

Bob is just making stuff up.

Inflation falls when money creation falls. Money creation falls when gov spending or bank lending falls. The Fed has little ability to constrain these flows (and often unintentionally accelerates them). And the bond market is an indicator, not a

If the Fed won't do what is necessary to bring inflation back to target, the bond market will just do it on its own.

94

87

697

4

3

43

Previewing a tool I built for visualizing balance sheet operations. Should have utility in working through questions like this.

@JackFarley96

@maggielake

@BickerinBrattle

need to ask how the fiscal spend is being funded? Latest data reveal growing monetisation... I think we can agree that fiscal policy is directing flows towards real economy. No surprise there

2

2

11

5

2

39

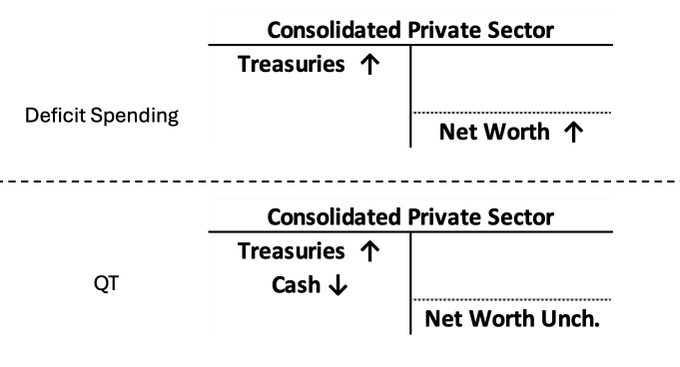

Here is the problem with "QT destroys money, deficit spending adds money, so they're offsetting".

One person’s debt is another’s asset. In deficit spending, new assets are created for the private sector. In QT, old assets (cash) are replaced with new assets (Treasuries).

It’s

@rpgoyal_

Deficit spending -new money- offsets the reduction in the quantity of money that the Fed does through QT.

Money is not an asset or a liability. All fiat money is debt.

2

0

1

7

5

37

Bloomberg asking this question is an existential threat for the Fed.

Without a supportive media apparatus, there is no Fed

What if Fed policy didn’t matter that much to markets? It seems like that’s where we are at the moment. Instead, traders are focused on fiscal stimulus still pumping into the economy and the potential deficit issues that will likely emerge down the line.

39

69

295

2

6

31

Inflation was always transitory UNTIL the Fed started hiking. There's never been a self-reinforcing/spiraling inflation in history that wasn't also accompanied by rising rates.

Rates are just a price. Raise that price, and you raise the income of every seller

If the Fed had left the fed funds rate at 0, the COVID thing would have been largely transitory. But it didn't and now CPI growth will gravitate towards the current fed funds rate that's supporting deficit spending/agg demand/employment/costs/forward prices/etc.

20

71

192

3

5

31

Had a great time discussing monetary and balance sheet operations with Nik Bhatia (

@timevalueofbtc

) at The Bitcoin Layer. Check it out!

🚨NEW VIDEO🚨

How The US Treasury Creates Money

Monetary researcher Ritik Goyal (

@rpgoyal_

) gives a masterclass on monetary mechanics, including how the Treasury creates money when it spends instead of borrows.

3

21

45

5

5

27

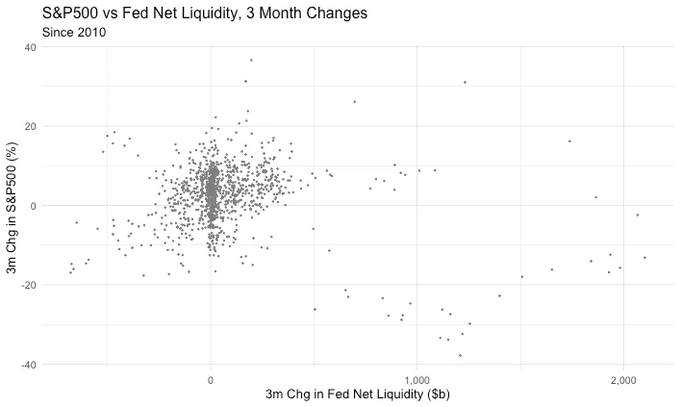

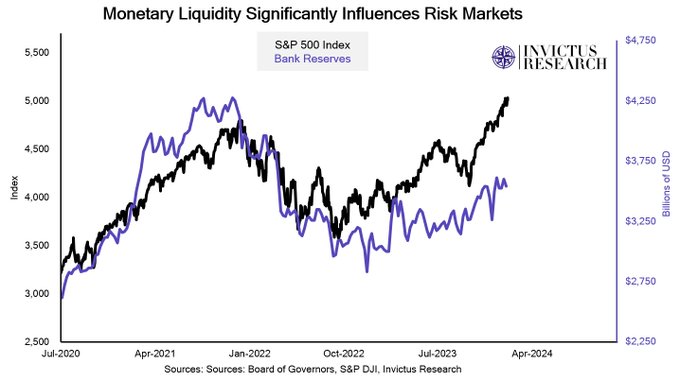

Not just spurious, there is no correlation between stocks and bank reserves. Liquidity isn't a useful concept

@BickerinBrattle

Correlation between bank reserves and stock prices has been *very high* for several years now...

What do we think? Spurious correlation? Or a reflection of important policy/liquidity dynamics?

5

0

9

7

2

25

High bond yields don't cause recessions, it's recessions that cause bond yields to stop being high.

The biggest challenge for asset holders right now is bond yields are high and rising enough to create a drag on asset prices but not yet high enough to create the economic slowdown required for the Fed to ease.

29

56

410

4

0

24

Thanks

@StephanieKelton

Highly recommend this (high-level) conversation on where

@rpgoyal_

thinks markets and the economy are headed and why.

3

34

100

0

0

23

Ah yes QE, the “free” money that you only get if you give up an asset of equivalent worth first

Bloomberg US Financial Conditions trending quickly toward the July 2021 summer of free money (ZIRP, QE, Stimmie, etc.) high.

16

24

125

6

2

23

2020-21: Massive QE, ZIRP, and massive fiscal, stocks/crypto break to new ATHs

2023-24: QT, 5IRP, and massive fiscal, stocks/crypto break to new ATHs (or close)

Process of elimination

8

0

22

A very Howell-ian treatment of liquidity. Which is to say, wrong imo.

Thread.

On Liquidity Dynamics🧵

1. Liquidity is the flow of cash-like assets that potentiate spending in the real and financial economy. Liquidity potentiates returns across assets, while the nominal growth environment determines the distribution of returns within assets.

9

25

104

2

1

23

There’s no evidence that this is true. Rates reflect conditions, they don’t cause conditions.

Much higher long-end rates are pretty much the only thing that has a chance to slow down the income driven economic momentum in the US.

50

19

259

5

0

21

R2K being -16% from its 2021 high is the bull case, not the bear case.

Most US companies are still deeply undervalued relative to current corp profitability and nominal growth. The mid-2000s style boom in cyclical risk (banks, commods, industrials) is still ahead of us.

1

4

21

Fiscal deficits without QE is just as powerful as with, perhaps even more. QE isn’t creating new purchasing power like fjscal is.

Equites and crypto at ATHs amidst anti-QE…

Fiscal Deficits + QE is one of the most powerful monetary combinations in the world.

You are going to see it more often over the next decade.

Here is how it impacts markets and the economy:

1/

31

181

970

7

0

21

So many unrelated concepts being conflated here. Have to think of money as dual-sided asset and liability.

Deficit spending does not "offset" anything the Fed does. QT only converts money from one form to another; deficit spending creates new money. Categorically different.

Persistent inflation is not a coincidence.

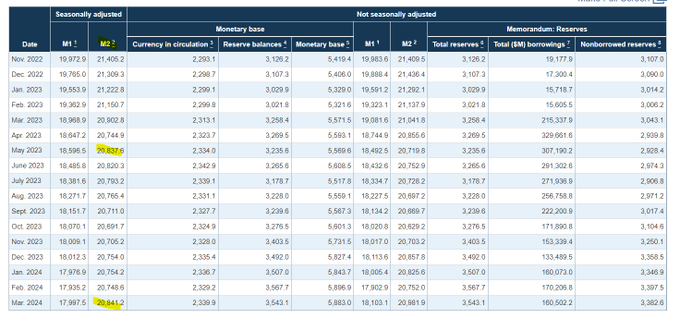

The money supply (M2) has bounced above March 2023 levels, while deficit spending offsets any Fed balance sheet reduction.

Table via Federal Reserve

13

35

115

3

1

19

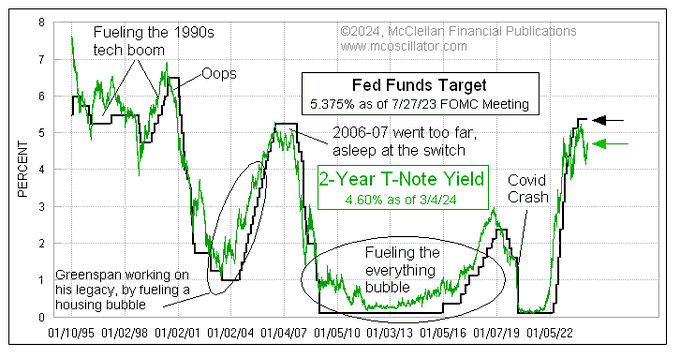

ZIRP fueling an “everything bubble” is one of the biggest myths in macro

One can follow the Taylor Rule, which is mathematically complex with several inputs. Or one can just listen to the 2-year T-Note yield, which knows better than the Fed's 400 PhDs do about what the FOMC is going to do.

28

132

595

7

3

20

To steal from

@wbmosler

, the CB policy error discussion is like worrying that the kid in the back seat is going to crash the car

Michael Howell: Central Banks Are About To Make A Major Error

13

101

385

1

1

19

Except rate cuts are anti-labor

@BobEUnlimited

You can easily get cuts without any political motivation. Fed officials have already spent time explaining they view the world through real rates, so cuts can come from slowing inflation. It's also easy to see that new Fed leadership tends to be more pro labor.

8

5

42

1

4

19

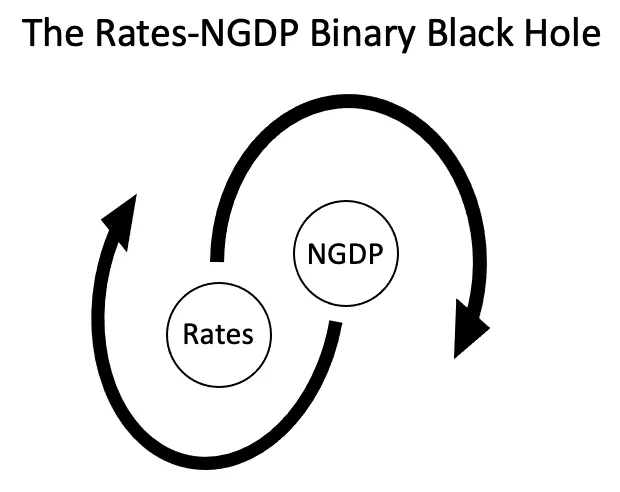

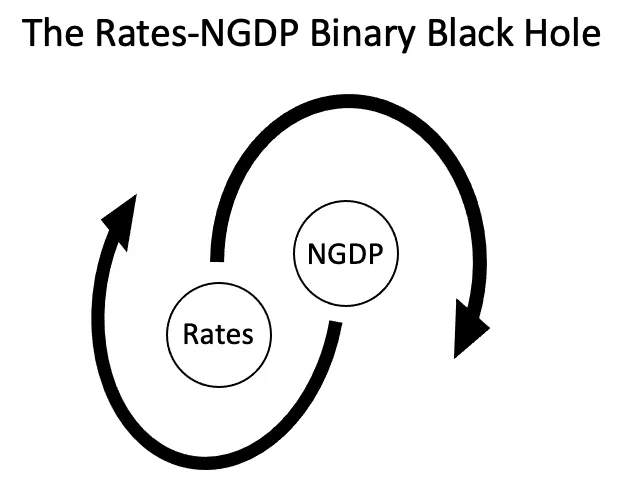

Inflation and rates are one and the same. Set rates somewhere, and that's where inflation will eventually go. Pulling on each other like a pair of black holes.

@Econ_Parker

What do you think his counterfactual is? If they had left rates at 0 (like Japan) where do their models say GDP/unemployment/inflation would be today? ;)

2

5

29

0

2

17

For a guy with a phd in economics you’d think he’d understand calling things cults and conspiracies is Step 1 in evading the scientific method. MMT isn’t even prescriptive it’s descriptive

Oh another nice byproduct of the pandemic inflation episode: MMT as a radical cultish (at one point potentially virulent) political ideology has been pretty thoroughly debunked and rejected. 😊

32

2

96

9

2

17

@TaviCosta

What is this ethical framework that makes you avoid Chinese companies but be okay with any other country's equity market?

4

0

18

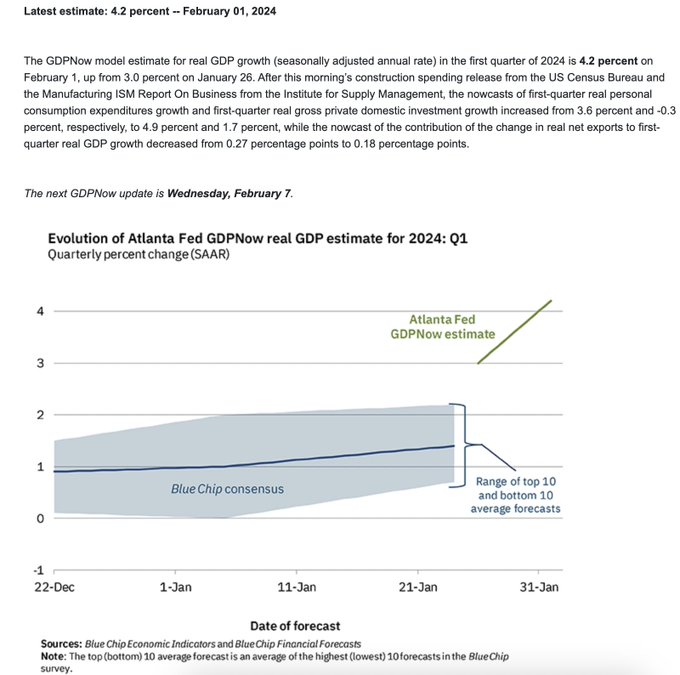

After 550bps of “tightening”…

The Atlanta Fed's 🇺🇸 Q1 GDPNow forecast is now at +4.2% up from +3%

11

42

190

1

4

17

This is like asking how NGDP growth can keep expanding when the supply of physical paper cash is falling.

Everyone knows it's not literal paper money that matters, it's total purchasing power, and converting paper money to a bank deposit doesn't change that.

But Bob has to fall

How can nominal growth keep expanding when major DW central banks keep contracting the money supply?

The answer is simple - rising velocity facilitated by strong nominal income growth.

21

30

181

5

3

18

The notion that the "ultra-easy monpol" of the 2010s (ZIRP, QE) is now finally spilling over into higher inflation is peak Fed-apologism.

Much more likely is that the Fed was mostly irrelevant then, is mostly irrelevant now, and what's changed is that the private sector holds

This is why I say the old theory that 12-18 month lag on monetary policy effects is no more.

15 years of Zirp and Balance Sheet Expansion. They locked it up though by paying out interest on excess reserves, and now on just reserves.

The effects of the earliest QE measures are

1

0

7

5

2

16

The weird thing about "we're repeating the 1970s stagflation" is that the 1970s actually had some of the best real GDP growth of any decade in recent history.

0

4

16

MMT is a lot like monetarism, except “base money” is the supply of government debt, not the supply of bank reserves.

7

1

16

Everybody realized rate hikes are inflationary

Anyone want to take a stab at explaining why Fed Funds Futures show an increase in probability for a March cut today after a hot CPI print?

124

14

316

0

1

14

@JackFarley96

Bond yields can also be quoted on a discount basis, which uses the bonds face value as denominator to calculate interest rates, whereas the investment basis used the current bond price.

FRED also has discount basis quotes for some of the Treasury yields

1

0

14

@ajlidbeck

@FoxNews

@newsmax

Lol newsmax literally had to provide a 3 minute disclaimer video that all the claims they made were false in order to avoid getting sued. You're running out of places to get your propaganda :(

1

0

12

Quarterly Refunding Astrology

2

0

14

That’s why the 2010s had no inflation despite the massive expansion in liquidity. Every attempt at measuring any sort of “total assets” shows the same picture: steady growth and then a dramatic, permanent, plateau.

3

0

15

Great discussion of business cycle dynamics by the folks at

@AppliedMMT

It's the combination of fiscal and bank money growth that dictates the cycle, and the Fed's rate policy only matters insofar as it affects those things

0

2

14

Big Fiscal + Rate Cuts is how you keep inflation transitory while spending. As long as the fiscal itself isn’t continuous, the funds just shift the price level higher.

Big Fiscal + High Rates is how you entrench inflation; it means the money that’s spent is paying its own money.

The problem with letting the transitorist victory-lappers off the hook is that they are already calling for renewed Big Fiscal and sharp Fed cuts (when output is not significantly below potential) and seem to want to entrench significantly higher long-term inflation

11

2

43

1

1

14

Thanks for having me on!

Talking Fed, interest rates, the economy, and why everything isn’t as it seems

🎙 NEW EPISODE with special guest

@rpgoyal_

is live!

🦉 The value of the MMT framework

🏦 Ritik's "The Fed Does Not Exist"

💸Monetary policy & inflation

📈Our outlook going forward

🎧Listen here:

3

6

31

0

0

12

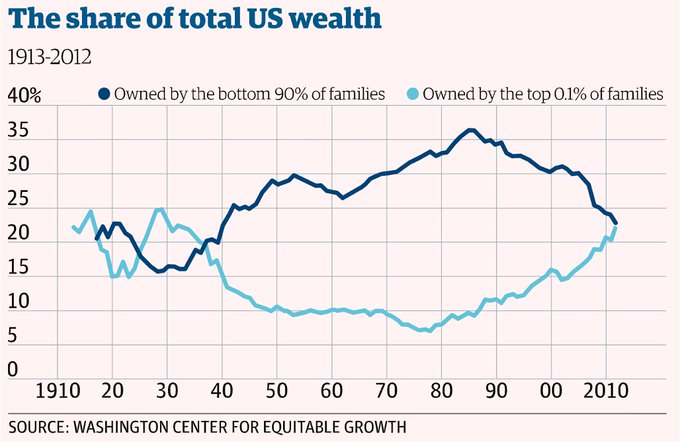

In other words, the demand for safe US assets exploded (via China), and at the same time, the supply of those safe assets fell. The only solution was for private safe assets to make up that shortfall.

The lesson is to never let true safe assets ever become too scarce.

Disagree.

The fiscal surpluses of 1998-2001 + the entry of China into the WTO in 2001 that exploded the US trade deficit.

Both factors forced US domestic households into debt to maintain consumption.

Caused an inevitable debt crisis.

13

2

63

1

1

17

@stevehouf

@wabuffo

In aggregate, the dollars that the Tsy spent into the private sector bought the new Treasuries

2

0

11

Yellen has no control over the size of the deficit.

Need to be able to distinguish between Powell Liquidity, Yellen Liquidity, and Biden Liquidity to accurately describe the economy.

*YELLEN: CONCERNED ABOUT 'WHERE WE'RE GOING' WITH US DEFICIT

You're the one driving! Pull the damn car over.

16

21

174

2

1

12

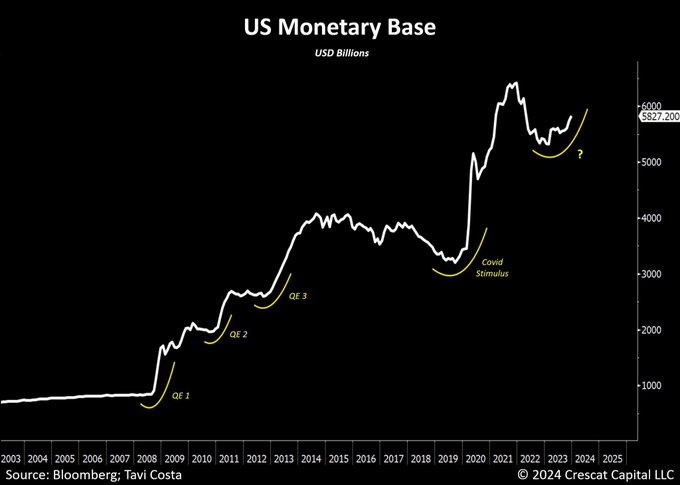

Wrong monetary base. QE’s increase in supply of reserves can’t stop a recession because a recession is a private sector BS contraction and QE isn’t a private sector BS expansion

If the monetary base is increasing despite one of the most restrictive monetary policies in history, what should one expect in a recession?

We probably all know the answer for that.

It’s imperative to own hard assets in my view.

44

154

750

1

2

12

@timpierotti1

Disagree. High interest rates are associated with high velocity and high private credit creation. Empirically that's the case, and logically, existing money must change hands faster when rates are high in order to satisfy larger obligations (velocity) and the incentive and

1

1

11

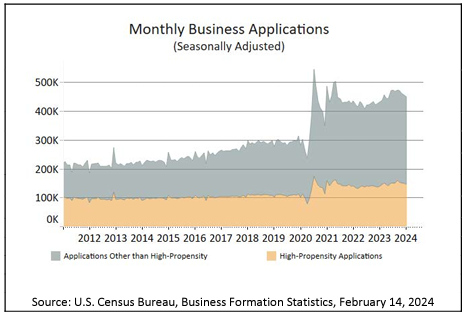

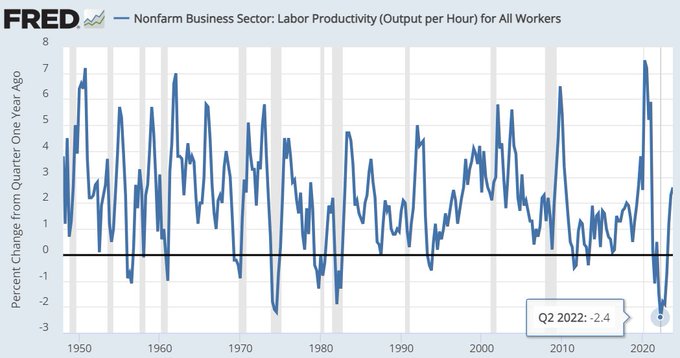

Government spending crowds in private activity.

Truly remarkable, especially that it's continuing.

h/t

@SamRo

, who connects it with higher productivity.

14

43

163

2

0

11

Duke is an awfully coached basketball team. 75% of their points come from offensive boards/transition or big mistakes by the other team which is why every game still feels like a toss-up. Almost no offensive design, screens, pnr, whatsoever.

1

1

8

Great pod. “The economy has 3 months to prove to the fed it deserves higher rates.”

It’s like having to prove you’re not high-risk to be able to buy insurance, even though it’s those who are high risk who need it.

Completely backwards, but it’s the world we live in

🎙 NEW EPISODE is live! Our 2023 wrap-up covers:

✅ What we got right

❌ What we got wrong

🏦 Where does the Fed go from here?

🔮 Predictions for 2024

🎧Listen here:

1

2

7

2

1

11

Higher for shorter is much more deflationary than higher for longer. With higher for longer, you give the system time to adapt to the new rate paradigm and iron out any balance sheet frictions. Once everyone is earning more on their assets and paying more on their liabilities,

1

3

10

Risks to our 2024 outlook piece coming soon.

Spoiler: the biggest risk is the Fed tries to “preemptively” cut to get a soft landing, which sows the seeds of a hard landing.

Can’t have a recession without rate cuts…

1

0

10

Re: all the talk of "easing financial conditions". The real concern with yields falling enough is not a reignition of inflation, it's recession. I.e. why every time the Fed "pivoted" we got a recession.

Discussed this with

@AppliedMMT

around 30-45:00

3

3

10

Had a great discussion with Daniel on the interplay of business cycles and monetary/fiscal policy!

1

0

9

Fiscal spending is only a redistribution through inflation. Making money less scarce makes assets less scarce which hurts those with assets. But no one directly gets their money taken when the government spends.

Fiscal spending redistributes income from those who spend less to those who spend more. The effect may be particularly strong when spending is financed by debt than taxes. This suggests continued strong growth in nominal GDP and is supportive of credit.

39

71

347

3

0

9

After 550bps of rate hikes, the levered and rate sensitive homebuilders are at an all time high.

3

0

8

Rising prices pulls consumption forward to avoid future higher prices.

Rising rates pulls borrowing forward to avoid future higher rates?

1

0

9

Bagehot would've hated QE. As FOMC member Fisher said in 2011:

Most of these variations that have been suggested are very un-Bagehot-like. And what I mean by that is, twisting entails purchasing assets that investors are fleeing toward, not assets that they are fleeing from.

should not confuse a Bagehot emergency response from the central bank - lend freely against sound collateral - with QE. They are not the same and QE is in reality a move to raise reserves, to fund an increase of reserves, the Bagehot action doesnt change reserves.

0

0

0

0

0

9

Nothing ruins your confidence like trying to sign an online document with your mouse

0

0

7

Focusing on cash-like assets as drivers of nominal growth or asset returns is a fallacy of composition. It’s not the supply of cash-like assets, but the total supply of all assets, that determines outcomes. Net worth drives decisions, not how much of that net worth is held in

2

0

9

Markets would be so much more efficient if they prioritized the amount of assets in existence, not whether assets exist in the form of a reserve or a Treasury security.

Until then the Fed's placebo tactics will continue to play a big role.

The Fed acknowledges the "lack of further progress toward the Committee's 2 percent inflation objective" and also slows the pace of treasury QT by more than half.

Easing policy at the same time inflation is a greater concern is at best inconsistent and at worst imprudent.

72

69

492

1

1

8

Rate cuts create a shortage of safe assets. A shortage of safe assets causes risk-taking to be less insured. Less insured risk-taking makes that risk-taking occur in a safer manner. Safer risk-taking is equivalent to less risk-taking. Less risk-taking means less growth.

1

0

8

@dampedspring

@JeffSnider_AIP

Jeff is making a structural argument about the system's ability to produce cyclicality, which he thinks has been kneecapped since 2008, with swap spreads and other prices indicative of that. In such a state there are no "sudden catastrophes" because to get such an event there has

0

1

8

It's the stimulative effects of rate hikes in action*. One person's loss is someone else's gain.

Doomers gonna doom

This isn't a meme stock, some third world country's currency, or the balance sheet of a failed regional bank - it's the losses at the Fed, and it just exceeded $130 billion:

486

2K

6K

1

2

8

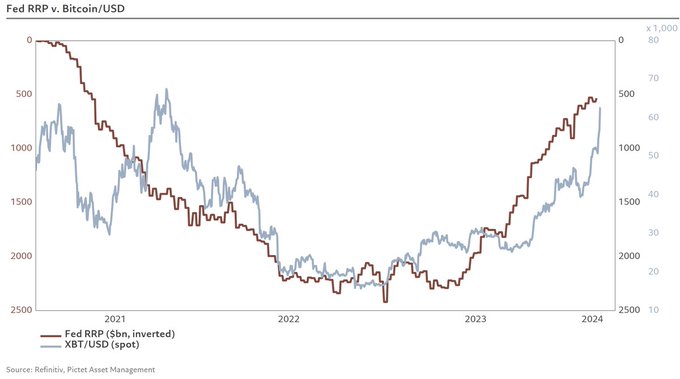

He did not just associate the RRP drawdown with the price of bitcoin

3

0

8

Since 2022, we’ve been living in the first case study of the Fed raising rates following a contraction instead of cutting them.

The recession you are still waiting for happened in 1H22.

4

7

20

2

1

7

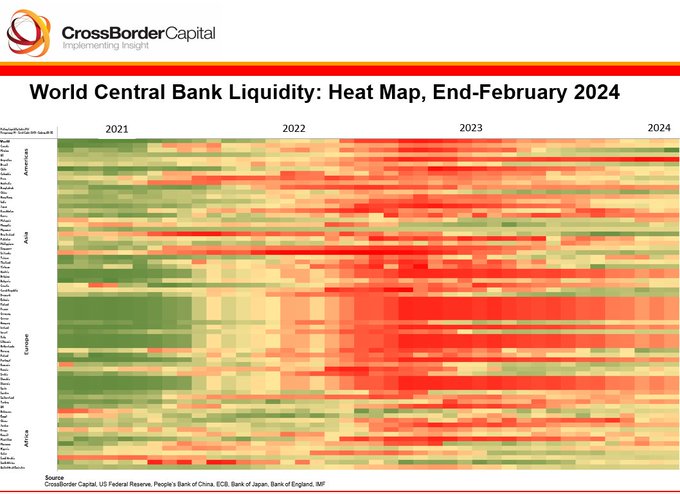

Like any impressionist painting, meant to convey a feeling or emotion rather than the pursuit of realism

Impressionist 'Sunrise'?? Central Bank heatmap with red hues showing maximum tightness of

#liquidity

From our latest GLI data release

15

46

265

1

1

8

ICYMI: I compare our framework at The Monetary Frontier to

@JeffSnider_EDU

's. We agree on what markets are pricing in, but not whether they're right.

0

2

7

A Fed pivot has never once translated to a sustained equity bull market, because a Fed pivot has never once translated to stronger earnings.

Economies usually survive hiking cycles; it's pauses and pivots they don't survive.

Writing a piece on this soon @ The Monetary Frontier

Outlook for 2024: I expect a broadening bull market as the Fed pivots (at least initially) and the bond market finds a new range, while earnings advance and the economy survives the great hiking cycle of 2022-23.

Two caveats:

1. The Fed might pivot prematurely, forcing it to

37

113

514

0

1

8

Each day that we don't get a recession, the "economy holding up despite rate hikes" case becomes worse compared to "because of rate hikes".

0

0

8

Phenomenal interview on the costs of low rates and the importance of the bank loan as the primary engine for economic growth

2

0

8

After 550 bps of hikes, long-duration assets Bitcoin and Ethereum are unchanged vs their Jan 2022 levels.

Rate hikes are income.

0

3

8

Just have to bring back Fisher, and things become a bit clearer.

High rates = high nominal growth

Low rates = low nominal growth

At turning points, both change direction together.

Remember, higher inflation means higher rates for longer which means higher economic risk for longer which means higher risk of lower rates.

See, investing is easy.

8

4

96

1

0

8

In fact, more of “liquid assets” has been a reliable indicator that the supply of “total assets” is falling, not rising. Liquidity tends to rise in deflation, because liquidity is a placebo tactic designed by CBs to obfuscate the real problem, a shortage of total assets.

2

1

9

@dlacalle_IA

All deficit spending is new money. Full stop. The government prints money, and it prints Treasuries.

1

0

7

Inflation was always transitory; a one-shot injection of fiscal cannot produce spiraling prices.

Then the Fed started hiking…

Disinflation has been rapid throughout the past year as supply chain bottlenecks have largely faded.

Demand inflation has started to come down on the back of a falling output gap (demand following relative to domestic output).

With current trend we could see core PCE below 3%

0

2

12

1

0

5

The narrow focus on liquidity is like weighing a car’s engine to try to understand the car’s weight. Sure, a heavier engine means the car could be heavier, but it doesn’t have to be. More of “liquid assets” doesn’t mean there are necessarily more assets in total.

1

0

8

Will have a piece on this on the monetary frontier soon. It’s my life mission to dispel of the Fed-brain and tech-bro-brain and ignorance towards the data that leads folks to think ZIRP is anything but disastrous for innovation

There was no “grit, originality, and innovation” during the ZIRP era? That’s news to me. I think we’ve seen numerous amazing innovative start-ups over the past decade, each of which took tremendous grit, originality and innovation. I’ve never heard of start-ups being easy,

12

2

27

0

0

7

The RRP rundown moves reserves around while QE creates reserves

But the RRP rundown isn’t QE, right… right

@Stimpyz1

? Ha. You literally have them confirming it here. The

@federalreserve

is reckless and wants to literally destroy the poor via inflation to pay for a fake economy where govt spending is EVEYTHING.

9

14

54

2

3

7

@gctradingES

@BickerinBrattle

The flow of new bank and fiscal money into the economy. That's it. "Liquidity" just describes the nature of money, not the amount of money.

2

0

7

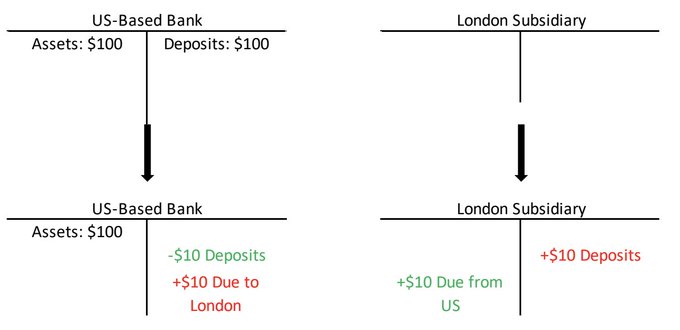

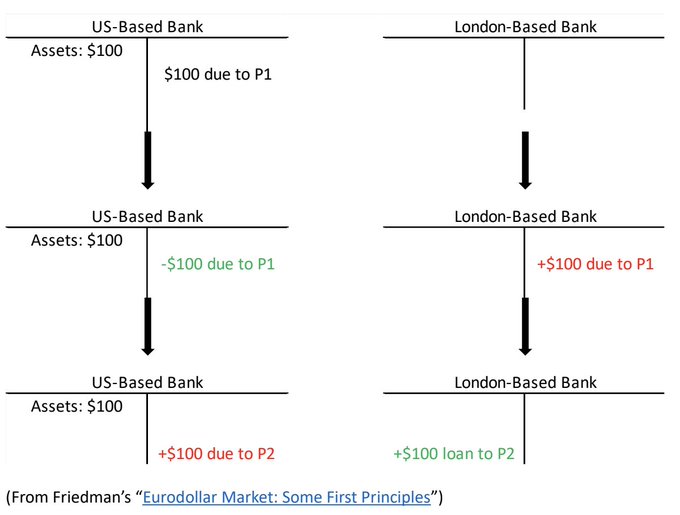

The Fed and money are in a perpetual game of cat and mouse. Tom and Jerry style

@dbaeza13

@crossbordercap

Yep and crafty bank accounting to get around the watchful eye of regulation.

In the first pic, a US bank circumvents reserve requirements by sending deposits to its London subsidiary and then borrowing them back, shifting its liability from deposits (part of M2) to "borrowings"

2

1

4

0

1

7

Today is an example of policy-market reflexivity. Market thinks one thing, policy confirms it and makes the market think more of that thing.

If that feedback loop gains traction, next thing you know we'll be back in a low rate, low NGDP environment.

0

2

7

Neither M2 nor velocity are particularly relevant to understanding the US economy.

M2 was only ever a proxy to measure private credit growth, a shortcut way to summarise the risk appetite of the private economy which a lack of is what ultimately defines recessionary periods.

It isn't a very good measure, so they made up a term "velocity" to make up for it's

0

2

15

0

2

7

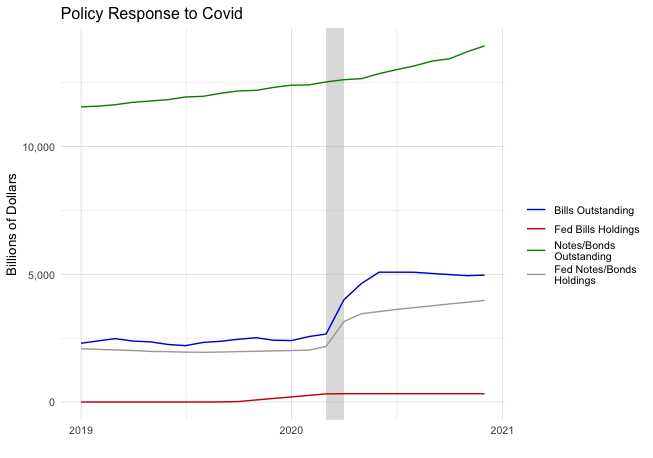

The Fed didn't come close to monetizing the debt. The debt was issued at the short end, the Fed bought the long end. If the Fed bought the short end, the Covid panic would've been 10x worse - the system needs bills, not reserves. (Why is why the Fed stopped buying bills in 2020)

@LynAldenContact

We're so glad you noticed that.

Here is Robert Kaplan (former President of the Dallas Fed) saying that the Fed "monetized the debt" in March 2020 to fund the U.S. government's vast fiscal support:

(1/2)

@JackFarley96

's follow-up question in part 2/2

5

13

55

0

0

7

QE works when the Fed buys assets the market is running away from. When the Fed buys assets the market is running towards, you get the opposite effect -> QE of Treasuries becomes a tightening

@dbaeza13

@BartsQuandry

@dampedspring

@countdraghula

@DiMartinoBooth

QE worked because the Fed bought MBS. It was the only stimulus injection Wall Street couldn't absorb whole. Because you couldn't fail to the Fed, VERY low coupons got created that needed to be loaned up, so homeowners got rich FAST. Then rest is noise.

1

1

2

2

0

7

@DzambhalaHODL

@BickerinBrattle

He’s doing a level to level comparison, which is basically useless. Have to look at the change in one thing versus the change in the other.

2

0

7

"It would have been better to get the recession, then use deficit spending to boost growth"...

That's exactly what's happened since 2022.

@EconguyRosie

~25% of jobs created last year were government.

Deficit spending is delaying the inevitable, meanwhile the lower class has been crushed by inflation.

it would have been better to get the recession, then use deficit spending to boost economic growth. Instead, they used

3

11

46

2

0

7

Whether an asset has 0 duration or some duration is insignificant vs. the fact that the net worth exists. If the Treasury decided to hand every American a 30-year Treasury bond certificate worth $1000, liquidity would be unchanged, but net worth would be radically different. And

2

0

8

The government spending funds the government spending.

Remember the government has already spent money... We are discussing how it is funded

3

4

48

1

0

7

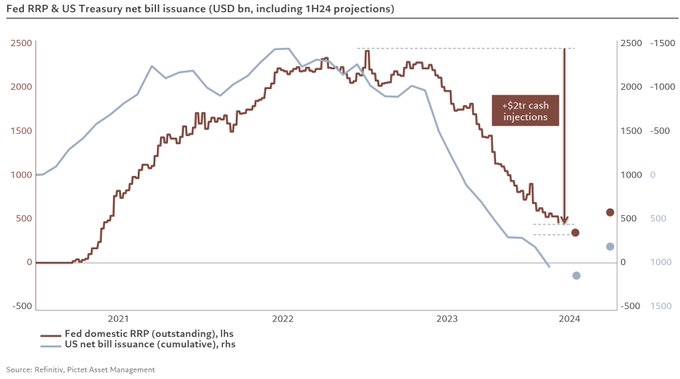

Would hardly call RRP depletion “Fed counter-injections” and would really hardly attribute equity returns to either

RRP depletion more a function of availability of T-bills, and equity returns more a function of creation of new A-L pairs, not composition of existing pairs

Fed counter-injections (via RRP depletion) to keep equities afloat for the remainder of 1Q24 before reversing in 2Q24.

12

29

129

4

0

7

A couple months ago,

@BickerinBrattle

and I put out some materials comparing our framework to the liquidity-based approach.

Tldr: what matters is how many new asset-liability pairs are being produced every day, not how many of those pairs are cash assets.

Links below

What is the impact of "Central Bank Liquidity" on markets?

Today I'm interviewing

@crossbordercap

&

@BickerinBrattle

, who have very different views on the subject

Let me know if there's anything in particular you think I should ask them... 👇

42

6

115

1

0

7