David Rosenberg

@EconguyRosie

Followers

261,961

Following

337

Media

603

Statuses

3,367

Founder and President of Rosenberg Research & Associates Inc. Retweets, Likes and Follows are not endorsements.

Toronto, Ontario

Joined December 2017

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Trump

• 3124809 Tweets

America

• 1025287 Tweets

Justice

• 944230 Tweets

Felon

• 633215 Tweets

New York

• 555212 Tweets

Democrats

• 489149 Tweets

Joe Biden

• 382398 Tweets

MAGA

• 361017 Tweets

Republicans

• 237748 Tweets

Luka

• 135452 Tweets

White House

• 129264 Tweets

Clinton

• 119809 Tweets

Florida

• 112827 Tweets

Dems

• 95432 Tweets

Alvin Bragg

• 92328 Tweets

Stormy Daniels

• 82465 Tweets

Neymar

• 65410 Tweets

Norita

• 64852 Tweets

renjun

• 64601 Tweets

#StateOfPlay

• 41479 Tweets

Minnesota

• 40718 Tweets

ワールド

• 37684 Tweets

Timberwolves

• 36535 Tweets

Silent Hill 2

• 33383 Tweets

#911onABC

• 29432 Tweets

Luana Piovani

• 28044 Tweets

Lively

• 25508 Tweets

Astro Bot

• 24324 Tweets

#BridgertonOcchiamin

• 22534 Tweets

ワイルズ

• 19178 Tweets

San Lorenzo

• 18661 Tweets

#النصر_الهلال

• 15388 Tweets

Borja

• 14808 Tweets

Saint MSG

• 14286 Tweets

アイルー

• 13034 Tweets

Solari

• 10892 Tweets

XCRY JAPON X KICK

• 10793 Tweets

Fonseca

• 10720 Tweets

Pinned Tweet

The replay for my fireside chat with Jeff Gundlach is now live. We covered how to invest around the near-term recession and disinflation call, and the implications of redressing an unsustainable debt burden in the public/private sectors.

Watch here:

21

35

196

Maybe Trump is a genius, after all. What if he finally gets the steep Fed rate cuts he has been demanding? After that, he ends the trade wars, tariffs go to zero, and the stock market surges to new highs -- just in time for the 2020 election!

357

813

3K

Sorry, folks. No soft landing. On track for 3 straight quarters of declines in real retail sales alongside 2 successive negative production numbers. Only happens in recessions.

150

582

3K

Iron ore is down 60%, lumber is down 50%, steel prices are down 25%, soybeans are down 25%, corn is down 20%, oil is down 20%, base metals are down 12% and Powell decides today is the day to join the consensus inflation bandwagon. Great timing!

183

590

3K

Americans pay $2T of taxes yearly. Equal to 9 weeks of Fed balance sheet expansion. So as Dr. Powell medicates the patient with unprecedented machinations, why not print the money and pay the IRS our taxes? Surely taxpayers deserve as much support as HY bond fund managers, right?

121

668

3K

Some nifty math. When you strip out of the CPI all the items that are linked to energy (air fares, moving/freight, rental cars, delivery services, new and used vehicles), the core was +0.36% and the YoY steadied near 4%. The truth beneath the veneer.

#RosenbergResearch

607

502

3K

We've had 8% inflation before. Been a while, but we've had it. What we've never had before was the Fed hiking rates into an official bear market. Brand spanking new. More downside coming.

#RosenbergResearch

116

352

3K

So one Bitcoin buys you 500 barrels of oil, a Honda Civic or half a year's wage. But there's no bubble. Sure thing.

768

267

2K

You have to love the stock market. The Dow soars nearly 1,000 points on Mon/Tues on hopes of Blue Wave stimulus. Next thing you know, there is no Blue Wave and the Dow soars about 1,000 points on Wed/Thurs on no tax hikes. I am calling it the “Tails I win, Heads I Win” market.

145

279

2K

Soaring Treasury yields, an inflation scare, a Fed scared by the bond vigilantes and a weak/increasingly unstable stock market. Takes me back to when I started in the biz in 1987. I'm thinking we could be tiptoeing here into a market crash. Boost your cash reserves and do it now.

150

283

2K

If I told you last October that the unemployment rate was going to surge from 3.6% to 14.7% and on its way to 30%, would you have thought at the time that the S&P 500 would be at the same level today as it was back then? The Fed has broken the GDP-SPX link once and for all!

119

370

2K

The big news today was the 9 months’ supply of unsold new housing inventories in April, nearly doubling in the past year and classifying as a 2 SD event. Inventory excess is now at a level that in the past was consistent with a recession followed by a huge home price correction.

92

368

2K

It’s the mother of all “money illusion” rallies. In 3 months, the Fed juiced up M2 by a cool $2.5T, and the S&P 500 mkt cap surged dollar for dollar. Who needs earnings? Who needs productivity? Who even needs buybacks anymore? MMT arrived early and with a Republican in office!!

90

450

2K

I saw a chilling stat today that 20% of Canadian mortgages were taken on when rates were at the 1.5% floor. With mortgage rates at 5%+, and 40% of this debt rolling over, the hit to consumer spending promises to be spectacular.

#RosenbergResearch

158

335

2K

So let's get this straight. The alleged greatest environmentalist on Earth, otherwise known as Elon Musk, is promoting a "currency" that is among the most environmentally damaging to the earth. Another one to add to Ripley’s.

400

193

2K

You don't need the yield curve to know a recession is imminent. The homebuilders, home furnishings, auto parts and specialty retailing stocks collectively are in a deep bear market and that is a near-perfect signal right there.

#RosenbergResearch

82

283

2K

Restaurant sales have declined in four of the past five months and at a pace we haven't seen in 25 years. That means worse than the depths of the 2001 and 2007-09 recessions. Remember -- they are a leading indicator.

128

647

2K

The crisis is with regulators who are idle while Comerica bonds blow out. The contagion is here. Everyone’s been focusing on an equity market driven by six stocks. This is a liquidity crisis of epic proportions. It’s incredible that policymakers are still sitting on their hands.

97

298

2K

Where’s the recession? Where’s the recession? I’ll tell you where it is. It’s in the UPS earnings release. As in, contraction in shipping volumes. It is now really tough to buy into that Q4 government-massaged GDP data.

163

249

2K

It is a bull market in (i) part-time jobs, (ii) self-employment and (iii) multiple job holders. Outside of these areas, employment actually contracted more than -500k in March and by -2 million in the past year. What an economy!!

102

448

2K

In the past 50 years, every 18% slump in the stock market over a four-month-or-longer period foreshadowed a recession. And recessions, on average, see the market slide 30%. So, no – we're not “there” yet.

#RosenbergResearch

72

275

2K

As the bulls go wild on today's bounce, a reminder: we had 11 sessions in the 2008/09 bear market when the Dow surged 4%; and 7 of these same whippy moves in the 2001/02 malaise. These happen more in bear markets than in bull markets by a huge margin.

65

377

2K

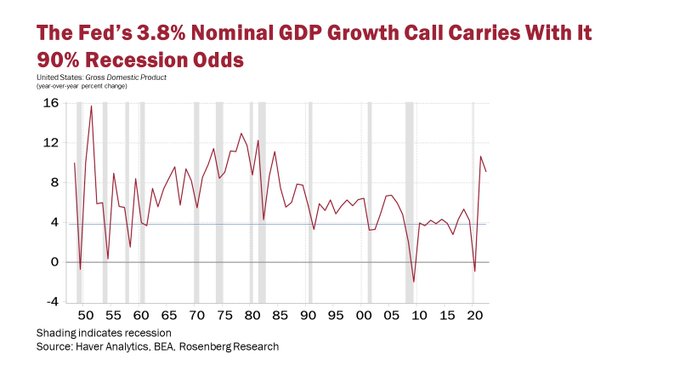

Powell didn’t want to talk about a hard landing on the podium, but the Fed’s 3.8% nominal GDP growth projection for 2024 gave us the answer in any event… this has a 90% recession probability attached to it. Shhhhhh….

95

349

2K

For the first time on record, the Fed is embarking on its first tightening campaign with the Dow, SPX, Nasdaq and Russell 2000 all trading below their 200-day trendlines. And the rates cycle hasn't even started yet. Good luck to long-only equity investors.

#RosenbergResearch

123

234

2K

Hard to believe we have hit the bottom with Cathie Wood still being interviewed on CNBC. When Jeremy Grantham gets the same airtime, you’ll know the lows are in.

#RosenbergResearch

90

144

2K

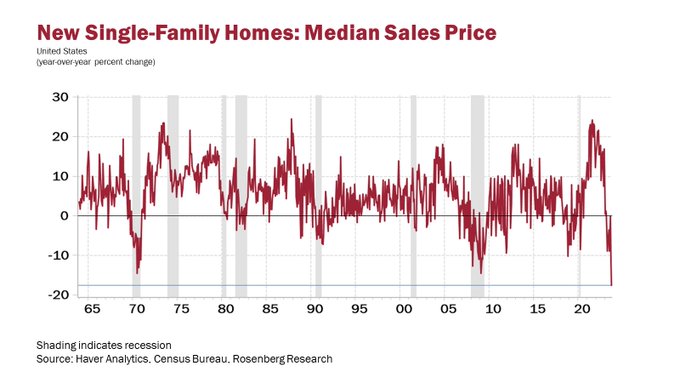

Let me know how the ‘sticky’ inflation narrative is working out, when median new home prices in October sunk a record -18% YoY, taking out the worst point (-15%) we saw in the Great Recession.

243

345

2K

Same institution that brought us “no tech bubble” in 2000, “subprime contained” in 2007, “green shoots” in 2009, “funds rate through neutral” in 2018, “transitory” in 2021, is now peddling “higher for longer” in 2023. Fade the Fed.

71

243

2K

Fed's forecast of real rates goes from -1.1% today to -1.9% in 2023. If that isn't an advertisement to buy gold, I don't know what is.

54

336

1K

Best week for the stock market since 2008. Worst month for the stock market since 1938. Confused? Don't be. Both years were horrible recessions.

29

356

1K

Memo to Powell: say as little as possible tomorrow. Do not commit to anything, including a March rate hike. Keep your options open in this period of intense market volatility and economic uncertainty. You can always revisit your hawkish intentions another time, but not tomorrow.

191

154

1K

The market is, God forbid, down 4% from the peak, and we have this raging debate over whether to buy the dip. I remember the days when a dip was 10% to 20%. Today's manic investor can't even seem to handle a mild hiccup without hyperventilating.

68

213

1K

Canada’s budget gets a big fat F. The tax bite expands. Spending out of control – an added $42bn in the next 5 yrs brings the cumulative burst since 2021 to $345bn! FY24 deficit’s to balloon to $40bn from last Fall’s estimate of $30.6bn and debt/GDP ratio up to 43.5% from 42.4%.

93

353

1K

Bob Kraft on CNBC: “Today’s colleges teach students what to think instead of how to think.” Truer words rarely spoken.

65

244

1K

Let me get this straight. Every talking head is saying the economy is in fine shape. And every talking head is saying we need a massive stimulus. Which is it?

116

238

1K

If households are stuffed with so much "excess savings" and with such strong balance sheets, why have they blown their brains out on credit card debt (at a 15% interest rate) these past four months -- a record $66 billion or +20% annualized!

#RosenbergResearch

#Economy

109

245

1K

Watch the Fed abandon forward guidance and rate commitments and embrace data-dependency. This cycle of hikes ends at 2 pm tomorrow. Buy bonds.

#RosenbergResearch

206

199

1K

We've reached a sorry state where a $1T fiscal stimulus bill is viewed as austerity. Obama's 2009 stimulus was $831B, by comparison. Bush's tax cuts of 2001/2003 were $150B annually. It's not really a sorry state as much as a welfare state. Not a judgment here, just a reality.

85

284

1K

The lagged impact of this U.S. dollar breakout is going to end up crushing inflation in the second half of the year. It has a 62% inverse correlation to the headline inflation rate with a six-month lead time. Nobody expects this, but history suggests otherwise.

121

215

1K

The stock market should have rallied today but didn’t. A bailout that everyone is ashamed to call a bailout couldn’t even trigger a short-covering rally. Smacks of a crisis of confidence.

109

168

1K

We don’t need to debate recession. It’s arrived for 80% of the economy via real disposable income – -0.2% in Feb for the 7th straight decline. Only other time this happened? Try Dec’ 73-Jun ’74 amid the recession that few saw coming. Denial isn’t an effective strategy.

46

291

1K

As the stock market rips in this Santa rally, nobody seems to have noticed that since the end of September, Q4 EPS estimates have been trimmed more than -5% and 2024 by -1%. Then again, who needs fundamentals when you have seasonals, momentum and a dovish Fed as tailwinds?

151

216

1K

This definitely has an early 2000 feel to it -- inflation, tech bubble, tight labor market, flat yield curve, value trumping growth in a down market. Biggest difference? The Fed was completing its tightening campaign back then; this one hasn't even started yet!

80

189

1K

If Putin really wanted to invade, he would have done it already. He knows better than blow up the Russian economy. Diplomacy will win out and he's going to end up getting what he wants. Best not to make investment decisions around this file.

#RosenbergResearch

151

175

1K

The Bank of Canada panicked today with its 100 beeper (!) and the yield curve has inverted. The housing bubble can be assured now of bursting and likely in spectacular fashion. The Canadian dollar popped on the rate hike, but the coming recession makes it a hard “sell.”

84

302

1K

As for the 401(k) comment in the debate — S&P 500 total return index under DJT is +14% per year. For Obama's last 4 years it was +14% annualized; all 8 years, also +14%. Clinton was +17%. Reagan was +13%. When it comes to markets, presidents don't matter. Markets just go up.

91

273

1K

Everyone seems to think the capitulation is in. Yet, can that really be the case when Goldman Sachs, the poster child for the consensus, "trims" its year-end S&P 500 target to 4,700?? No. You need a panic to set in before dipping your toes back in. Stay calm. Stay liquid.

77

122

1K

I keep hearing that this is the most widely advertised recession ever recorded. So tell me then why it is that the consensus is still at +7% for next year's EPS growth forecast?

168

125

1K

Why doesn’t Jay Powell save us all the time and just say “we don’t want the stock market to go up” and call it a day?

#RosenbergResearch

139

102

1K

After this recent round of speculative lunacy, I am starting to wonder if 50 bps tomorrow shouldn't be back on the table.

150

98

1K

If the stock market angst is all about Putin then why would autos (-30% from the highs) & homebuilders (-24%) be in bear markets? Or retailing stocks off 19%? What do they have to do with geopolitics? They clearly reflect the rates market resetting for a Fed-induced econ turndown

91

181

1K

My team just informed me that Tesla actually lost close to $1 Bln on a GAAP basis but the headlines all said posted their first annual profit (thanks to all the non-GAAP adjustments). That's all it takes for the algos and retail crowd to jam the stock higher.

74

320

1K

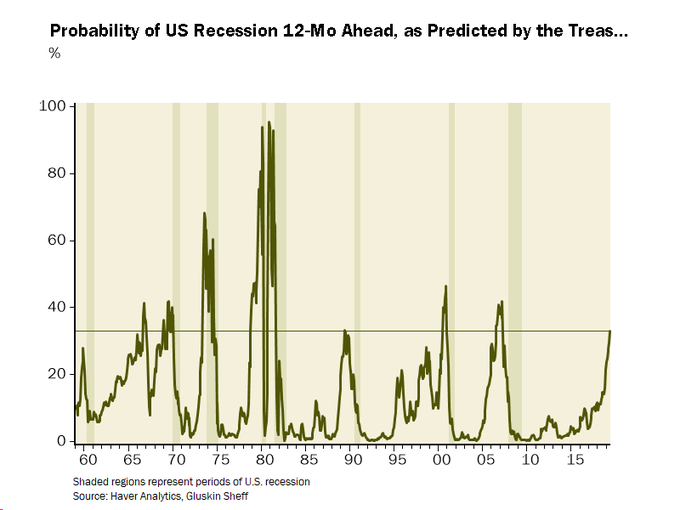

For those who "can't see the recession", it's illustrated for you in this chart. The NY Fed model now pegs recession risk at 32.9%, a 12-year high. History shows there's no turning back at this level.

88

673

1K

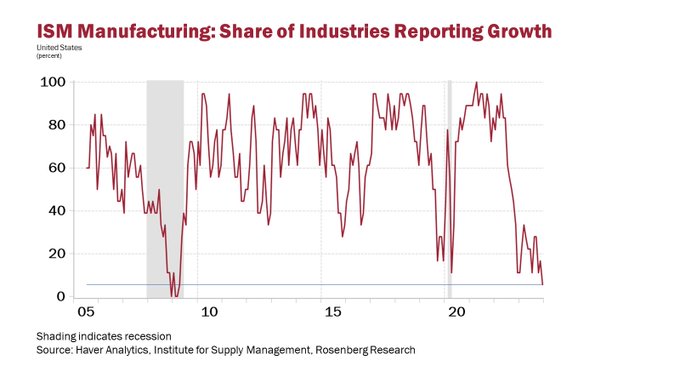

Everyone believes the economy is recession-proof. Yet, the ISM today shows that the grand total of 5.6% of purchasing managers are experiencing any growth. Last time we were here? Try April 2009!

105

317

1K

The 2s/10s yield curve has now inverted to over -80 bps. Last time here? Try April 1981. And the double-dip recession was three months away. Different this time? Bloomberg recession model now at 100% for 2023, so I somehow doubt it.

#RosenbergResearch

63

266

1K

We keep hearing on bubble vision how the S&P 500 lined up with some of the best Augusts of all time. Want to know the other Augusts that were so strong? Try 1928, 1929, 1932, 1933… and 2000. Market tops or economic depressions. Take your pick.

33

295

1K

Hey, if you don't like the yield curve as a recession gauge, how about the -5.9% YoY trend in the Cass Freight Index, the -9.7% plunge in Port of Long Beach cargo traffic and the 3.9% slide in US railway carloadings?

91

423

1K

How I’m spending my 62nd birthday! Nobody wants to party with a bear!!

149

39

1K

Only once in the 10 bear markets in the Russell 2000 did the Fed dare to tighten into the drawdown and that was late 2018. Oops. What's interesting is that the next move is either a pause or a policy easing -- in all 10! Could the rates cycle be over before it even begins??

106

201

1K

Liquidity conditions are about to tighten. Our work shows that global M2 has the most significant impact on U.S. equities and is on the verge of contracting.

91

278

1K

Open Table says 25% of US restaurants won't survive. That's 3 million jobs lost permanently; closer to 10 million when you include all sectors affected. Factor that into your "normalized" P/E multiple.

88

374

1K

The U.S. economy is in such terrific shape that 7 of the 12 FRB district banks reported economies either in contraction or in stagnation in today’s Beige Book. The other 5 are barely expanding. Calling B.S. on the retail sales report.

95

281

1K

It's rather pathetic that we have portfolio managers out there whining that the Fed didn't do enough on Wednesday to bolster their long positions. As if a balance sheet at 20% of GDP and zero rates forever isn't enough for these whiners. Let alone multiples at two-decade highs.

41

175

1K

Essentially 100% of the S&P 500 rally and 166% of the spike in the Dow happened after the Fed announcement at 2 pm. Powell should hang a sign: "Short Sellers Straight to the Unemployment Line With the Other 30 Million"

61

198

1K

Time to stop trading off the payroll data. The downward revisions in 2023 totalled an epic 443k. More than 40% of payroll growth in 2023 didn’t even come from the survey but from the fairy-tale ‘Birth-Death’ model.

82

322

1K

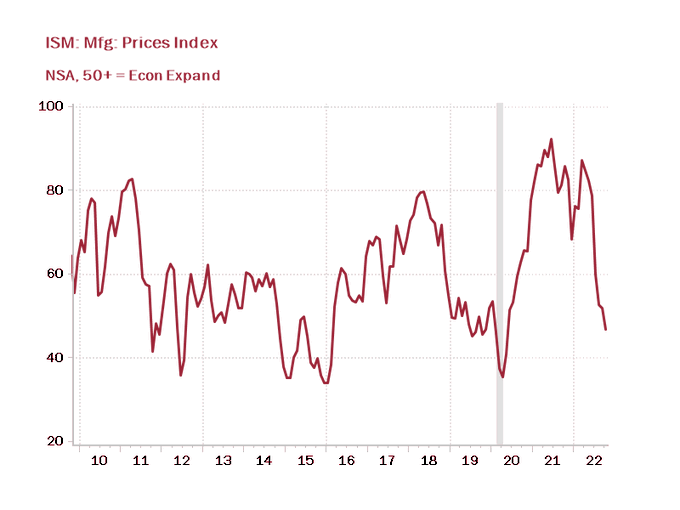

Powell doesn't see inflation coming down because he's focused on the most lagging and flawed inflation indicator of them all--the CPI and all it's imputed guesswork from the BLS. Sir, please have a look at the ISM prices paid, which has plunged to the lowest level since May 2020.

239

220

1K

What are the odds we get a Fed announcement at 8.30 a.m. tomorrow?

133

74

1K

Was just on BNN where I was admonished for not advocating the spending splurge in the Canadian federal budget. Imagine adding as much debt to finance social spending programs in a six-year span (~C$700 bln) as in the prior 152 years combined.

102

297

1K

It now takes >8 yrs of wages to buy a used home (!), 20% above the 50-yr norm. If this excess gets resolved via the numerator, we'll have a housing bubble burst that could rival 2008. This is the Black Swan. If rates do back up, they'll come crashing right back down again.

90

198

1K

The Fed hired Blackrock on March 24th, when it was only "willing" to buy IG bonds. Roughly two weeks later, the Fed is now "willing" to buy HY, Fallen Angels, CLO's, CMBS and leveraged loans that are highly risky in nature.

65

332

1K

In the span of four weeks, six negative daily Dow reversals of 1%+. This happened 99% of the time in the past in 1987 (crash); 1990 (recession), 1997-98 (Asian crisis); 2000-03 (tech wreck/recession), 2008-09 (GFC), 2018 (Powell!). All either ~20% corrections or 30%+ bear markets

66

266

1K

We could be building towards an Oct/87 crash, led by an aggressive Fed & surging bond yields. Difference is that commodities then were in a bull market, the dollar was stable & real GDP growth was +5% YoY. So this financial tightening could be worse & there is no economic support

81

249

1K

Guess what? The demand boom is over. Charts don’t lie – once supply comes back on stream, the demand downturn will cause inflation to morph into deflation. Definitely out of consensus and not priced into anything. Treasuries will rally and cyclical-value equity trade will fade.

121

280

1K

I keep hearing about "pent-up demand." But how does this apply to services? Are people who used to get haircuts monthly going to make up the spending loss by visiting the barber 2x monthly post-pandemic? Makes no sense but people just talk without understanding basic economics.

151

136

1K

The fact that all it took was for Powell to say that 75 basis points is off the table to elicit a 932-point surge in the Dow only attests to how oversold the stock market was going into the meeting. The best days of all time in equities happened in bear markets, not bull markets.

109

108

1K

So the Fed is pursuing a new inflationary strategy even though inflation is a tax on wages & real purchasing power for households. Oh, but it leads to negative real interest rates, a boon to equity investors & stimulates borrowing in an economy already up to its eyeballs in debt.

56

269

1K

I was so close to turning more bullish (less bearish?) until I see this metric was released by the New York Fed on consumer expectations. Since when do bear markets end on record optimism?

90

306

1K

Best way to cure inflation? Recession. Yield curve getting close to inverting and making the call – 2s/10s less than 50 basis points away and 5s/10s within 10 basis points. Never mind bonds – things are getting very interesting for the stock market. Will the bulls fight the Fed?

95

175

1K

As I watch the asset bubbles get bigger and bigger, I can't help but think of Alan Greenspan's parting words before he left the Fed: "History has not dealt kindly with the aftermath of protracted periods of low risk premiums."

45

211

1K

Where's the recession? Where's the recession? Give me a break.

97

244

1K

The Fed must have been on the phone all weekend with its business contacts and got all the info it needed. To move like this three days before the meeting tells me to expect an avalanche of horrible data in the next few weeks.

46

293

1K

Did anyone ever think they'd see, on the same day, ADP showing a 2.8 million job plunge and a mere 22% of ISM service providers posting any growth at all, a 400 point surge in the Dow?

174

164

1K

I saw a promoter on bubblevision saying we're definitely in a new bull market. Industrial conglomerates: -23%. Autos: -31%. Advertising: -34%. Consumer finance: -37%. Regional banks: -37%. Energy: -36%. Casinos/gaming: -43%. Hotels: -52%. Airlines: -55%. Sure thing.

87

263

1K

The bull and bear go out for a coffee (maintain distance). The bull proudly says: "Best three days for the S&P 500 since 1933". The bear responds: "Exactly!".

16

215

1K

The “everything rally.” Bonds. Credit. Copper. Oil. Bitcoin. Equities. Maybe the Fed has to go 50 at the next meeting.

#RosenbergResearch

123

94

1K

Just as rents & goods prices start to deflate, Powell decides his favorite inflation measure excludes products & shelter. He is now targeting less than 30% of the CPI. Why? Because he needs ammo to tighten further into the longest/steepest yield curve inversion since 1981!

86

175

1K

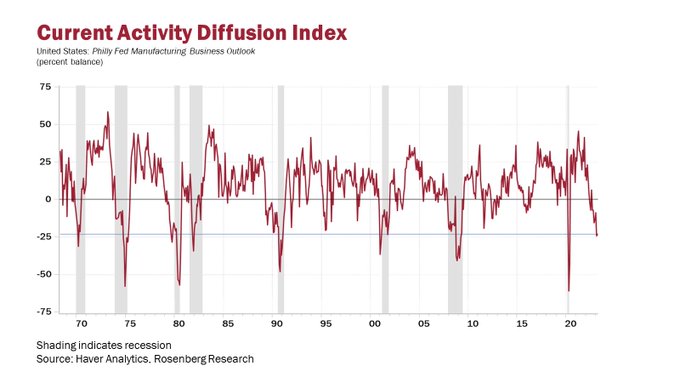

Take a good hard look at this chart and tell me we are heading into a ‘soft’ or ‘no’ landing. More like a ‘crash’ landing. Philly Fed at a level that is 8 for 8 on the recession call and with no head fakes.

71

276

1K

We now have had three months of a 3-mo/10-yr yield curve inversion. The track record this has had in predicting recessions: 100%.

62

467

1K

"I can't see a recession!". "Where's the recession!". I can't tell you how much I hear this every single day. It's like saying "I can't smell the carbon monoxide." By the time you "see the recession", your head's sliced off. Such a ridiculous statement.

71

245

1K

Who knew that all the global markets needed all along was for the BoE to tackle a 10% inflation rate by monetizing a debt-financed tax cut!

#RosenbergResearch

62

112

1K

The Fed has laid down the gauntlet with the dot-plots and the FOMC minutes. The combined rate effect with the balance sheet runoff will be an epic 350 bps this year, dwarfing the 200 bps in 2018 that unleashed all that market havoc. Not to mention 150 bps in 1987. Buckle up!

71

196

1K

Let's get this straight. President Trump calls this the best economy of all time and yet at the same time it needs 100 basis points of rate cuts and a 10% tax cut??

99

206

1K

Unbeknownst to the bond market, payrolls actually plunged -550k in January when the shrinking workweek is factored in.

85

215

1K

Bob Farrell’s Market Rule

#8

: Bear markets have three stages – sharp down, reflexive rebound, and a drawn-out fundamental downtrend. We just moved into the third stage.

65

174

1K

Back-to-back GDP contractions may not be the official definition of recession, but the reality is that whenever it's happened in the past, the economy was in recession. Go figure!

#RosenbergResearch

50

158

1K

First time in my 35 years in the business that I have ever heard so much bullish narrative over a jobs report that saw a 0.9% contraction in the workweek, a 3.1% slide in factory overtime, a 0.6% slide in labor income and 122k plunge in full-time employment.

55

155

1K

Comparisons to 2000 tech bubble are misplaced and not because of interest rates. This time, the bubble is in tech (Apple), comm services (Netflix) and consumer discretionary (Amazon); not in one sector. The bubble actually is in passive indexed investing… Won’t end well at all.

49

229

1K

I keep hearing what great shape the U.S. banks are in today. Here's the problem: it's their customers who are in bad shape. Which then actually means the banks are in bad shape too!

39

164

1K

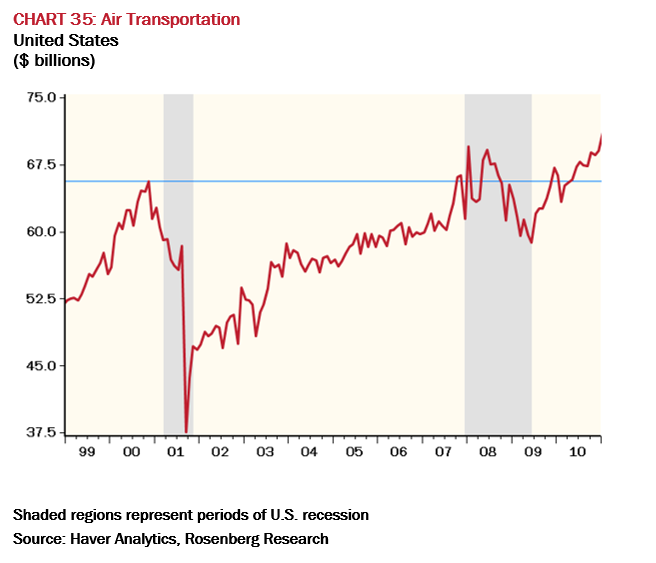

It took seven years after 9/11 for airline travel spending to reclaim the pre-shock peak. Any guess how long it will take this time around?

136

335

1K

Neel Kashkari tells CNBC that policy may not be tight enough because autos and housing are turning up. Meanwhile, the August data showed housing starts -11.3%, NAHB housing index -10%, new home sales -8.7% and auto sales -4.6%. What is he talking about??

167

150

1K

Bill Ackman, once a vocal proponent for higher rates and shorting Treasuries, just covered his profitable bearish bet and stated that “the economy is slowing faster than the data suggests”. Hence this Treasury turnaround.

59

150

1K