Bob Elliott

@BobEUnlimited

Followers

137,106

Following

688

Media

4,178

Statuses

21,747

CIO at @UnlimitedFnds | PM of $HFND | Fmr IC @Bridgewater | Described as one of the "sane" voices on #fintwit | Comments are not investment advice

New York, NY

Joined March 2022

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

$BTC

• 479860 Tweets

renjun

• 158993 Tweets

Heat

• 120635 Tweets

Lewis

• 76432 Tweets

#SmackDown

• 72435 Tweets

#DragRace

• 70247 Tweets

Mani

• 58713 Tweets

Bulls

• 52414 Tweets

Saint Dr MSG

• 48251 Tweets

Lando

• 43916 Tweets

#FreeMillie3D

• 33736 Tweets

Ethan Hawke

• 31838 Tweets

Edmundo González Urrutia

• 29170 Tweets

Celtics

• 23416 Tweets

Role Of Police

• 20167 Tweets

Sapphira

• 19827 Tweets

Verstappen

• 16658 Tweets

#2024BAEKHYUNASIATOURinBKK

• 15723 Tweets

Yamamoto

• 11290 Tweets

Juan Soto

• 10015 Tweets

The US banking system is built on the expectation that equity and bond holders accept the bank economic risk and depositors, particularly the small folks, do not.

While that is not legally the structure, its important to keep in mind that's functionally how it works. Thread.

153

518

3K

Hearing from some insiders:

-big banks actively working on buying svb business

-fdic considering insurance / liquidity covering up to 95pct of uninsured depositors to acquirer

-Monday 250k on track

-50pct of uninsured paid out next wk

Cant confirm myself but seemed worth sharing

146

460

3K

Fed/FDIC decisions on SVB determine whether they risk a bank run trillions of dollars in size.

1/3 of US deposits are in small banks and ~50% are uninsured. Haircutting SVB depositors will raise sensible questions about holding deposits at any small bank, risking a broader run.

223

694

3K

Years ago I led research on the GFC and was way out front suggesting trillions in losses, so I know a little something about crummy banks.

Getting panicked calls about the risk of SVB deposit losses, a bank with:

1) 15% tier 1

2) 40% LTV

3) 100% deposit liquidity coverage

94

382

2K

The market action today reflected the fact that there is far too much liquidity still in the system than desirable.

Bear market rallies typically come after periods of declines and are driven by short-covering. Today was driven by leveraging up on expectations of a bottom.

67

206

2K

The FDIC has taken SVB in receivership and will manage its resolution. This has happened hundreds of times over the last decades and there is a well tested game plan as I mentioned earlier. Thread.

80

291

2K

Most investment portfolios are totally unprepared for war.

In times of conflict inflation rises, gold and commodities outperform, while stocks, bonds, and cash underperform. A typical portfolio of 60/40 + cash is the worst portfolio, particularly on a real return basis. Thread.

123

334

2K

Pricing switched from hikes to cuts in 72hrs, signaling small bank stress is enough to derail the macro strength.

JP must be considering lessons of '98 right now when a financial panic drove Fed cuts and extended the tech bubble. Except this time the costs are higher. Thread.

49

270

2K

Typical macro cycle turns are slow to start, but they all end in recession.

The current modest rise in unemployment is about median for a year in since YC inversion compared to post-war cycles. But it’s usually in this time frame where things start to get interesting:

86

399

2K

Elliott fam so happy to bring home our newest member, baby C.

Petunia (our golden retriever) is most excited, though still figuring out what kinda of dog it is. She’ll be having fun with her new friend soon!

Try not to break the expansion while I’m offline for a little bit…

218

10

2K

If bitcoin is going parabolic, maybe money isn't all that tight right now.

298

109

2K

It's hard to know where any economy is going.

But if you want to start predicting where the macro economy will go in the next 3-6m, here are the 13 key indicators to track that will give you a head start. 👇

74

319

2K

I don’t trade crypto and have no inside knowledge. I have traded currency markets for decades, including those that are heavily managed by central banks.

Free markets are stochastic. Manipulated markets show abrupt direction changes and signs of stability at narrow ranges:

130

164

1K

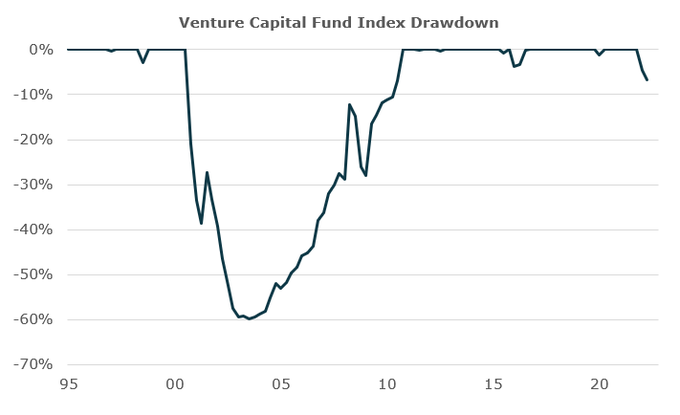

One of the biggest dynamics in '23 will be the recognition that privately held, illiquid assets are worth nothing close to their current marks.

VC, PE, CRE, PC are all marked around highs and do not reflect the re-pricing of the risk free rate, let alone any economic weakness.

51

166

1K

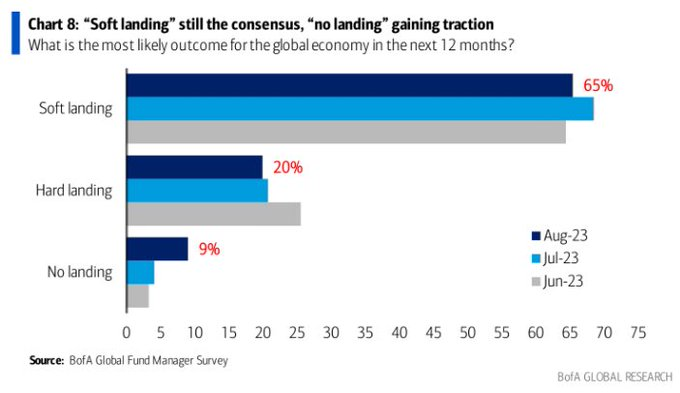

My guess is today will mark the top in the ‘no landing’ scenario narrative.

Market based tightening with much more duration supply coming. Tighter for longer Fed. And cyclical sectors starting to turn back over again.

A recession is coming. Sooner and harder than most expect.

132

241

1K

Regional bank 'crisis' shifting from deposit runs driving equity declines to speculators engineering equity declines to increase the risk of deposit runs.

This new phase divorced from fundamentals risks creating a metastasizing crisis rewarding speculative attacks. Thread.

114

261

1K

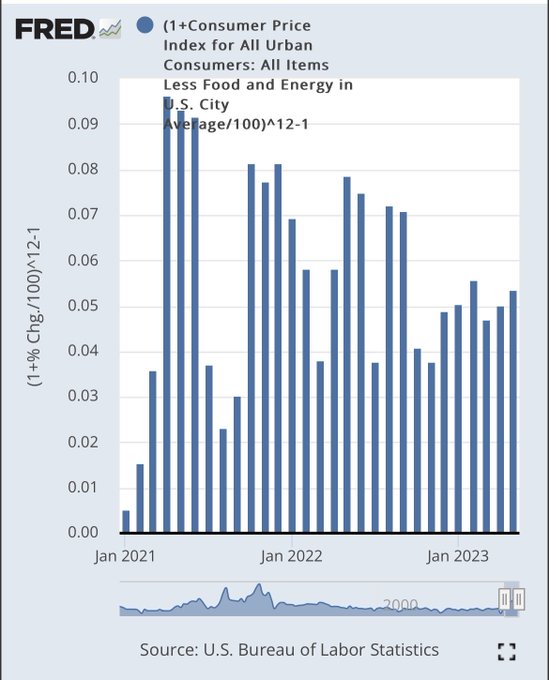

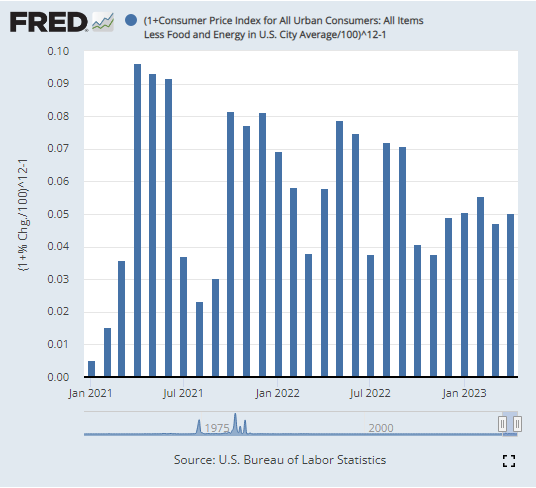

Cut through the noise. Core inflation has been stable at 5% annualized over the last 6 months.

That is far too high given the Fed’s mandate.

109

262

1K

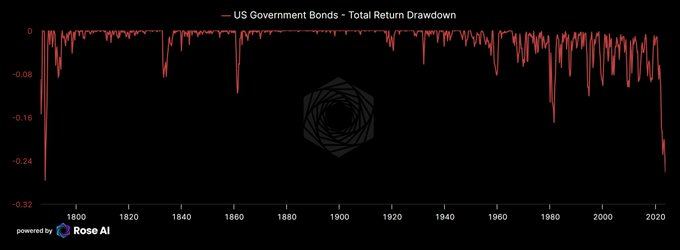

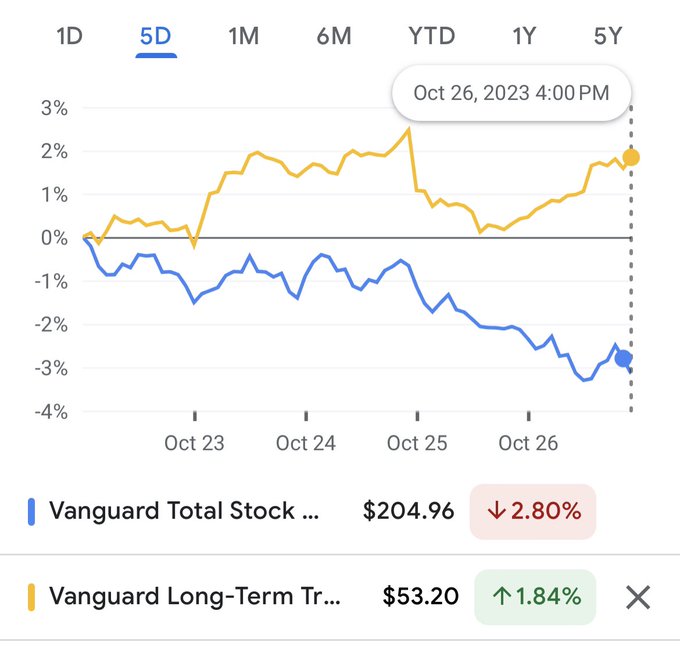

With the most recent leg down, this US bond selloff is on par with the largest ever in history.

As shown next, it's also in line the largest falls for major countries that didn't lose a world war or have hyperinflation. Some perspective from my friend

@abcampbell

on the selloff:

55

304

1K

Many buying bonds to get ahead of the coming recession in '23. But if you look through time, the start of Fed easing is a better timing indicator to buy bonds.

In inflationary cycles that typically occurs well after recession start. In growth-focused cycles it happens before.

65

241

1K

The China/US decoupling is gaining steam. A good reflection of that dynamic is that Chinese share of US imports is on track to fall in half within a year.

The decoupling is rewriting global supply chains. Broad based set of gainers, including MEX, CAN, JPN, Asia.

97

360

1K

While it may be difficult to predict the public markets in '23, it is pretty easy to figure out that Venture Funds are on track to lose $1 trillion in value from peak.

The vast majority of these losses have yet to be recognized. '23 will bring more realistic marks. A thread.

71

226

1K

Don't focus on the nuances of the CPI report. Its much more valuable / less noisy to focus on incomes. That's because in any economy nominal income vs. output determines the structural inflation rate.

Most stats show US incomes are growing pretty consistently at 5-6%. Thread:

74

218

1K

Pretty incredible to see covid-period like deficits being run at a time when unemployment is at secular lows and the economy is growing above potential.

In the short-term this helps delay any recession incoming. Long-term it will make managing an eventual recession difficult.

111

228

1K

The biggest unpriced duration supply risk is that the PBOC will need to intervene to support the CNY.

CNY at 15 year lows means not too much longer before the PBOC mounts a more aggressive defense. Last time they did, it created a huge ripple through global markets. Thread.

52

242

1K

Buying stocks at these elevated prices on expectations of future Fed easing is a fools errand.

The type of conditions that would cause the Fed to ease would also lead earnings to significantly disappoint the current lofty growth expectations.

94

116

1K

Markets are all-in on a soft landing, pricing:

- 25% earnings growth thru '25

- 20% fall in oil prices by '25

- 2.2% inflation forever

- Just 3 fed cuts in 2H24

And to generate any alpha, actual outcomes have to be *even better* than the very optimistic scenario above. Thread.

45

166

1K

Bunch of data points suggest a substantial weakening in consumer spending in August. If the consumer is actually fading, very hard for equities to hold these levels.

Morgan Stanley, Chase, and Citi retail sales trackers all weakened a lot in Aug. Short thread.

57

204

1K

A Fed pause/cut is not supported by the macro data, and also not supported by market signaling.

- Stocks are up during this 'crisis,' and IG spreads have risen a mere 30bps.

- Compare to '98 when the fed cut 75bps in response to a 22% fall in stocks and 100bps IG spread rise.

72

137

1K

BoE move today is being pointed at to imply both a put and a pivot.

That's not a good interpretation. The BoE provided short-term liquidity to a distressed market to ensure solvent entities didn't go broke unnecessarily.

That's a central bank serving as lender of last resort.

54

174

1K

What is the likelihood 2024 will have 12% earnings growth *and* 5 rate cuts?

That is what is currently implied by the short-rate and stock market. Soft landing both 100% priced in and unlikely to be achieved. Thread.

First the short-rate market, priced for 5 cuts in '24:

58

172

1K

It takes a combo of dynamics to bring recession, many of which will likely come together in the next 6m or so.

1) late cycle

2) weakening of cyclical sectors

3) monetary, fiscal and/or market tightening

4) added drag (like weak foreign demand)

That combo emerging now. Thread.

53

198

979

One of the most consequential shifts in global markets over the next decade would be a re-pricing of neutral rate expectations.

For nearly 15 years, most investors and central banks have held that neutral in around 2-2.5%, but increasing evidence it may be higher, even 4-5%.

59

173

976

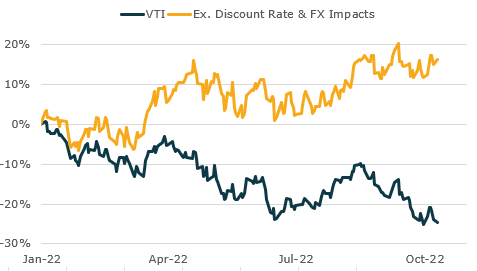

Stocks are down 25% on the year. But once you take into consideration the rise in discount rates and the impact of the dollar on earnings, the stock market implies higher earnings than at the start of the year.

That creates a large earnings re-rating risk to current prices:

37

140

950

One of the most important GFC lessons was that it is better to go big and move swiftly in order to prevent a bank problem from metastasizing.

JP & JY clearly drew on that experience today. While the program is likely more than what's needed, it is also likely to work. Thread.

40

145

961

The no-landing scenario is now consensus.

Growth expectations are now 2.2% for '24 *and* inflation expectations are near 3%. All the while, the Fed is expected to cut 3 times this year and the term-premium still at zero, an increasingly improbable set of pricing.

56

176

961

Today's mkt cap concentration in the top 10% largest US stocks has only occurred one other time in history in 1929...

80

218

926

This is disappointing. It is normal for people to have differences of opinion, but these types of unfounded personal attacks are totally unprofessional and stifle what could have been interesting public discussions of markets, the economy and policy.

164

27

913

The last time that core inflation was at today's levels and the unemployment rate was at multi-decade lows, the 10-year bond yield was running at 8-9%.

76

121

893

The markets are still pricing in a near 100% probability of a soft landing.

Expectations are for rapid earnings growth, no credit issues, inflation at 2%, oil px fall, modest Fed cuts and secularly high real rates. First S&P500 earnings growth, expected to be 12% for '24 & '25:

44

148

893

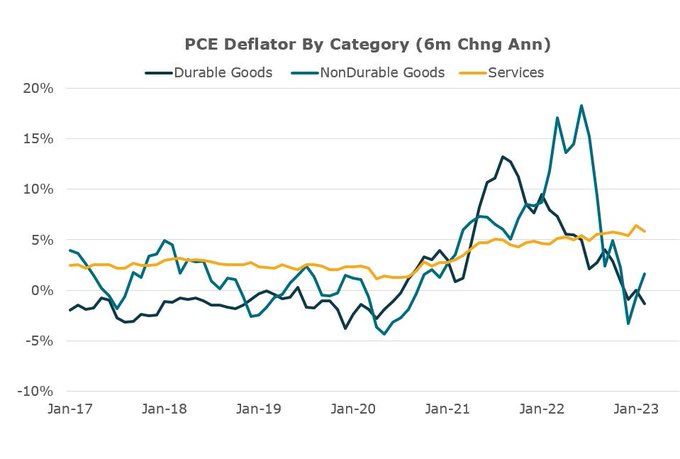

Past cycles show that inflation, once entrenched, is hard to beat. And it has proven darn near impossible to beat without significant economic weakness. There is no "immaculate disinflation".

PCE data in line with recent CPI, PPI, GDP data. Inflation persistence.

47

185

883

Private credit funds are lying to their investors about the valuations of the underlying assets, often claiming marks much higher than in traded public markets. Most investors will be shocked by the losses they eventually take...

72

189

883

Buying stocks and bonds here is a bet that the Fed will proactively ease policy which will juice asset returns.

If growth is holding up and inflation is moderating there is no need to ease because their goals are accomplished with the current policy in place. Thread.

70

97

886

The FDIC's 130bln insurance fund *currently* has enough resources to cover >$1tln of depositors if needed.

That's because the FDIC doesn't pay out depositors entirely. It only pays out the incremental amount needed to make a failed bank's depositors whole. Thread.

40

149

880

How is it possible that nominal GDP grew 6% in 2023 when M2 was flat, bank balance sheets were flat, and borrowing my nonfinancial sectors was pretty stable?

Velocity.

102

161

924

I taught an intro macro and markets course for a decade and thought folks would enjoy it if I shared some readings inspired by that course. An updating thread:

This POW Camp reading covers nearly every topic in macro and markets in just a few pages:

I taught an introductory macro & markets course for a decade and each year started with "The Economic Organization of a P.O.W. Camp." It covers nearly every major macro concept in 11 pages. The start to the school year reminded me to read it again.

35

130

747

68

170

859

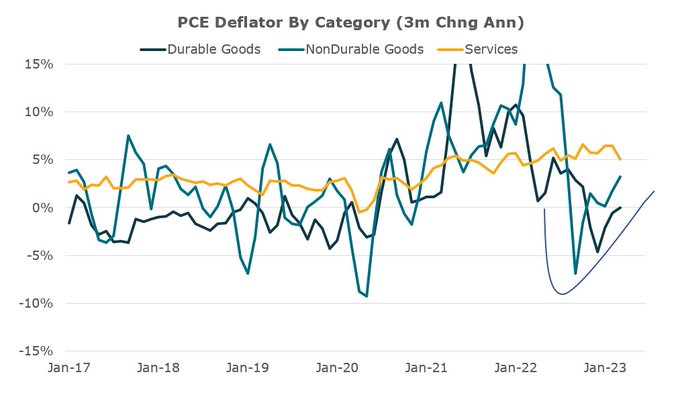

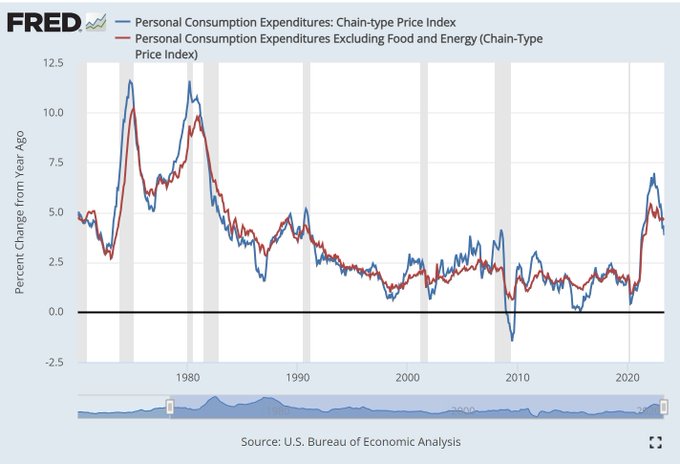

Inflation is too high and too sticky given the Fed's mandate, and in the short-term it looks like things are going in the wrong direction.

Lets start CPI week with a quick review of what's going on with inflation pressures. First, breakdown of the most recent PCE report:

35

144

857

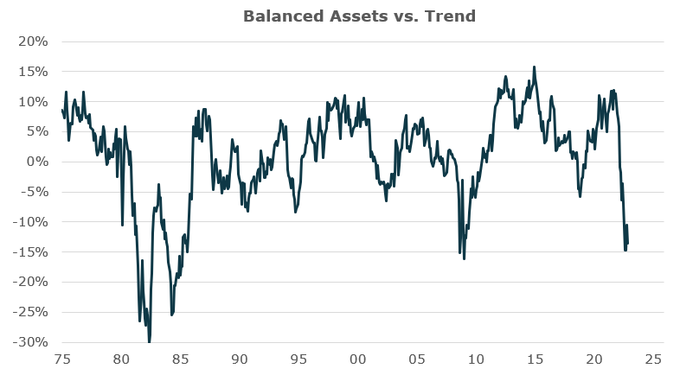

Assets prices are at their weakest levels in 40yrs. Not necessarily a buy at these levels - it took another 10pct down to break inflation 80s.

Looks like the Fed has more work to do, but watch this closely bc at some point in '23 assets will become a great buy.

Thread on '23.

31

157

859

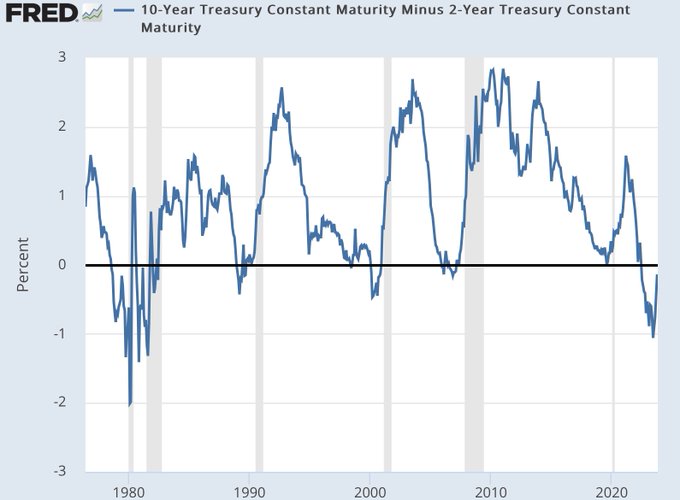

The history of what comes soon after a rapid steepening of the YC following inversion is clear. Recession.

You certainly have to believe ‘this time is different’ if you are long stocks with 25% earnings growth expected over the next 2yrs.

85

161

853

Most of the easy money is gone in the bond market at this point. The asset that is now so clearly overvalued is stocks.

50%+ outperformance of stocks vs long bonds in last 3 years is not sustainable. Closing that gap will be extremely painful to most investors.

57

141

847

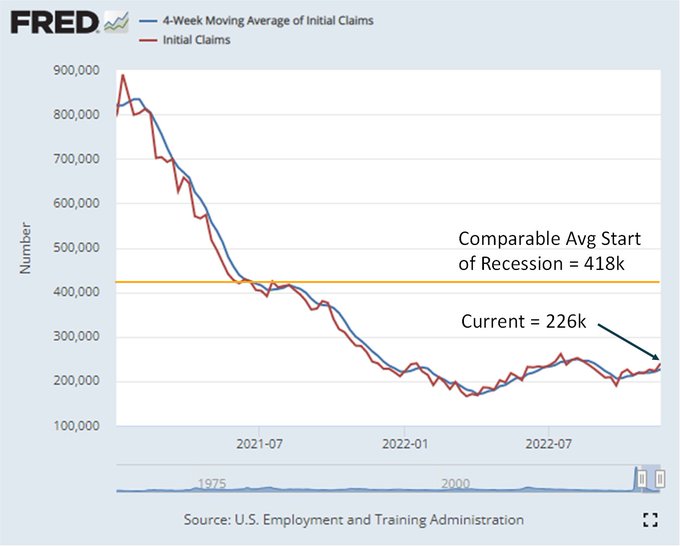

The US economy is quite a ways from recession.

Looking at the labor market, we should expect recession to begin when claims are ~418k given the past couple cycles and today's working age population size. Even a relatively fast deterioration would take nearly a year to get there.

71

159

838

EM stocks are at 50 year lows relative to US stocks.

Over any short time these divergences wont necessarily close, but if you are saving on a multi-decade horizon, it seems pretty clear that a lot more value is in EM vs. US. Note also the story is true with or w/o China stocks.

89

187

816

The most likely macro scenario by the end of '24 looks like little to no Fed cuts, elevated rates on the long-end, and the economy slipping into recession.

134

95

816

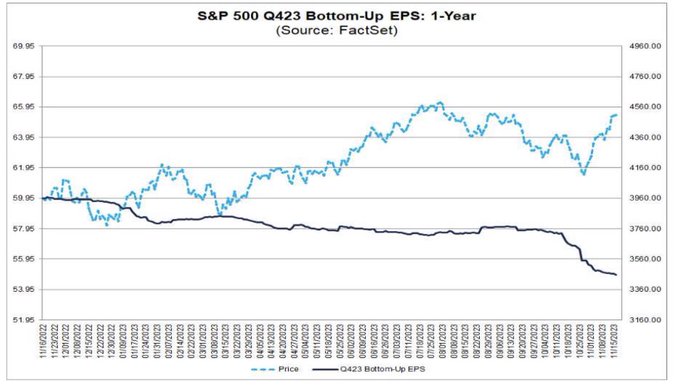

The rally in stocks in recent weeks has taken attention away from what looks like a pretty concerning forward picture from earnings releases.

Q4 earnings expectations have come down considerably in recent weeks, in contrast with equity market strength.

54

161

813

Gold pushing new all time highs despite broad hatred in the US, higher dollar, and tighter dollar US monetary policy expectations suggests the surge in demand is from abroad, particularly China.

Gold price is rising even as US ETF assets keep falling:

56

202

807

Sentiment today does feel very similar to mid-08 when many folks created justifying narratives on why the US (and global) economy could navigate the period without a recession.

51

121

784

China is on the verge of a BoP crisis.

For weeks not the PBOC has held the line at 7.3 for weeks through the fix, intervention, and rate rises, but it is not working. Pressure is mounting for a more substantial FX move, likely on par with the stress seen in '15/16.

44

148

770

Bitcoin reinforcing in recent days that it is not driven by rising geopolitical conflict, macro dynamics, or rising banking stresses. Huge discrete moves on idiosyncratic news.

Lack of clear fundamental economic return properties undermines its inclusion as a portfolio asset.

318

80

759

Inflation is higher than the Fed's mandate and not on a path to get to that mandate soon. The CPI report is one data point and most measures show elevated inflation.

Areas that had been disinflationary are reverting. And the stickiest parts of inflation remain elevated. Thread

49

177

762

Never imagined that my first time on

@CNBC

I would be suggesting cash is the best asset out there, but these are the times we live in.

Many thanks to

@MorganLBrennan

and

@jonfortt

for having me on to get my 'cold shower' take. Check it out!

82

63

755

I taught an introductory macro & markets course for a decade and each year started with "The Economic Organization of a P.O.W. Camp." It covers nearly every major macro concept in 11 pages. The start to the school year reminded me to read it again.

35

130

747

The kind of conditions that would lead to Fed cuts starting in March would be terrible for the equity market.

71

65

747

The best macro folks I've seen actively adjust their views with incremental new information.

In macro there are a lot of unknowns about how things will play out, so surprises are part of the business. Many get durable edge by responding agilely to the changes they see. Thread.

32

76

743

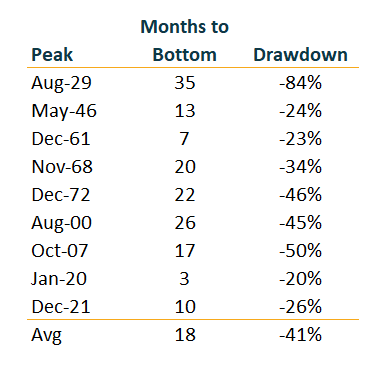

Most investors today have not experienced a normal recession. It's important to remember that they typically take a *long time.*

A few charts about the 2000s cycle. End to end it took 3 years: the full equity market index peaked in Mar '00. That last bottom was Mar '03.

40

149

737

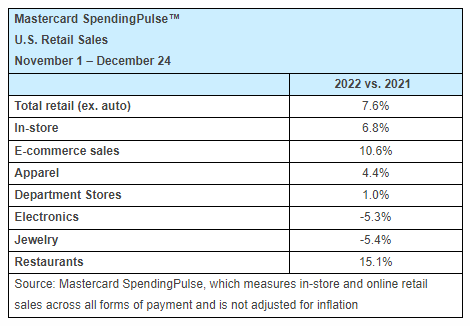

Mastercard spendingpulse ends the holiday season at 7.6% y/y nominal ex-auto. Not much different than initial NRA estimates. Roughly zero real, given PCE nondurables prices were about 8% y/y thru Nov.

Soft but not collapsing goods demand. But look at that restaurant spending!

43

117

732

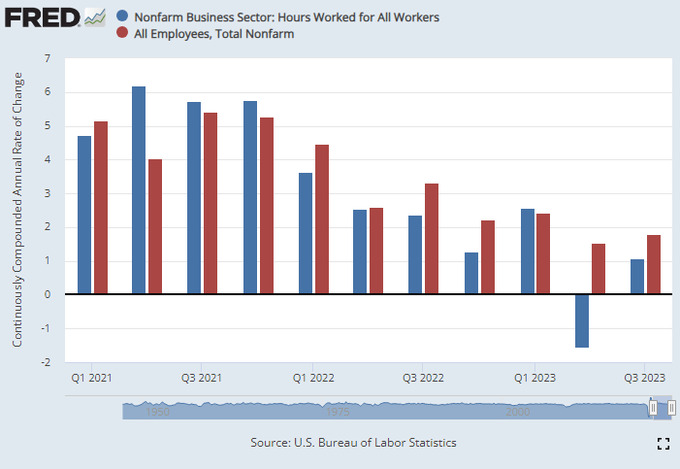

The US is not experiencing a real productivity boom.

Stronger reported productivity relies on a cyclical collapse in hours worked which means either the economy is rapidly weakening or there's a measurement error. Neither is good.

Total hours growing less than jobs for 1yr now:

38

154

727

Thinking this duration 'crisis' is like the GFC is off by an order of magnitude:

- 08 cycle losses were around 1tln against about 1.2tln of bank capital coming in.

- Today's unrealized (vs. capital), unhedged bond losses are on the order of 250bln vs. bank capital of 2.2tln.

66

98

723

A telltale sign of a bad investor is when they make bets based on their views of how political dynamics will transpire. Listen for it.

No skilled investor has edge in predicting politics. The only reasonable investor view today is there is more uncertainty than on Friday.

88

60

718

The Fed’s pause is not a data driven decision, it’s a risk averse preference.

If the Fed decided on the actual data below, further hikes wouldn’t be a close call, even at today’s 5.5% rates:

- 8% gdp growth

- 5% real growth

- 3.8% UE rate

- 5% wage growth

- 4% core inflation

81

83

720

If a pivot is going to come quickly, it will be driven by financial stability concerns.

Spread markets are the best lens into a deterioration of financial conditions. When I scan across them (below), I see basically nothing, even in the crummiest corners.

Lets start with IG:

38

132

713

Stocks down. Bonds down. Gold up. Oil up. Combo is starting to become a trend.

The worst possible combination for the 60/40 investor. Time to start thinking hard about whether you are prepared for more of the same.

85

101

708

Views on the dollars future role as the lead global reserve currency differentiate serious, experienced macro folks from those who are tourists and ‘disconnected luminaries.’

The dollar isn’t going anywhere any time soon and it’s wasteful to spend time worrying about it much.

73

123

701

Cutting through the noise, core CPI has been running at 5% m/m annualized for a half year now and is showing no signs of budging.

The Fed will not cut rates with 5% core inflation.

84

142

697

So far this earnings season has seen the weakest sales beats in the US in a decade, And its been even worse in Europe.

Suggests nominal growth deceleration faster than most bottoms up analysts were expecting. Tough to keep earnings up with margins without labor cuts here.

32

189

686

Soft landings are like a mirage, looking like reality but rarely persisting more than a moment.

Either growth keeps weakening (Apr 08, May 01, Jul 90, Jan 70, May 60) or inflation re-accelerates (Jun 72).

Today's pricing of a near certainty of one goes against past experience.

63

78

676

Stocks will outperform bonds as long as the economy keeps going.

The economy will keep going as long as stocks / home prices don't fall too much.

Prices of stocks and homes wont fall too much as long as bond yields don't rise too high for too long.

76

90

684

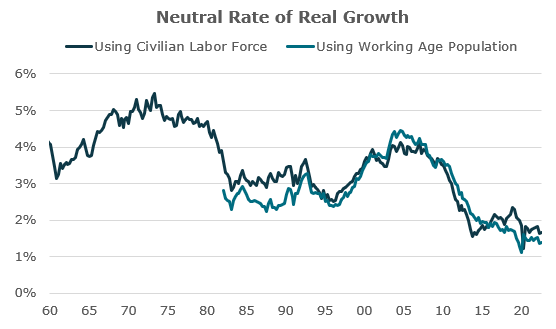

The neutral rate of real growth in the US today is around 1.5%, less than half what it was in previous cycles.

That means that even what feels like relatively modest growth (a 'slowcession') will still keep labor market conditions tight. Thread.

30

128

676

The rise in stocks since Nov 1 has mostly been driven by the rise in long-dated bonds. The rise in long-dated bonds has mostly been driven by pricing in 5-6 Fed cuts in '24 plus some term-premium compression.

But these moves sow the seeds of divergent pressures ahead. Thread.

51

87

668

‘Buy bonds because recession is coming soon’ crowd running into the central bank higherer for longerer buzzsaw.

Tough thing is recession more likely deeper & coming faster than it was a week ago. But bonds aren’t paying off. Shows unique challenge of trading a stagflation cycle.

74

64

660

If you love bonds here with 5 cuts already priced in for '24, then you must really love being short stocks.

80

46

657

@Claudia_Sahm

This is disappointing. It is normal for people to have differences of opinion, but these types of unfounded personal attacks are totally unprofessional. And they stifle what could have been interesting public discussions of markets, the economy and policy.

57

10

655

After a robust 24 hours of thinking of the trade-offs, lets consider what a balanced improvement to the regulatory framework would be. I'll start.

Raise the FDIC limit on non-interest bearing accounts to 5mln and enforce regulations that limits risk taking with those funds.

92

78

651

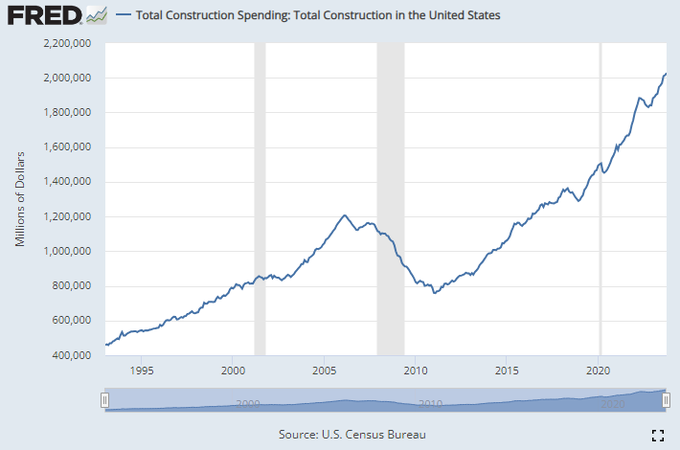

The construction boom in the US is an important driver holding up the expansion.

In typical recession periods construction spending slows, particularly residential, as rates tighten which then creates broader knock on effects. No significant slowdown today:

49

109

643

This week we learned:

- Growth remains above trend.

- Employment still secularly tight.

- Wage growth stable at 6-7%.

- Inflation above target and expectations rising.

- Banking "crisis" fading.

- Fed's main concern is still inflation.

H4L dynamics remain strongly in place.

49

99

628

The problem for the Fed is nominal wages are growing at 5-6pct which is sustainably financing nominal spending at 5-6% for an economy with productivity growth near zero.

Until there is a decline in wage growth relative to productivity growth, inflation will remain a problem.

97

123

633

5yr TIPs with current real yields at 2.6% will be the most compelling risk-return asset vs cash over the next couple years.

These bonds are offering boom level yields at a time when the economic cycle is softening and recent market moves suggest further softening.

32

76

640

The *order* of macro linkages matters more than calendar time to create growth turn and durable inflation decline. Still early:

1. Rates rise

2. Stocks fall

3. Demand slows

4. Earnings decline

5. Job market weakens

6. Wage growth slows

7. Inflation durably falls to target

55

122

629

What happens if stocks fall, bonds don't rally, and commodity prices rise?

The answer is its real ugly for most investors. 60/40 is an all-in bet on disinflationary strong growth. How prepared is your portfolio if we have inflationary weakness?

101

63

621

The decades of peace we have experienced recently is extraordinarily unusual in a longer-term context.

600yr chart of conflicts highlights how extremely low it’s been of late (ticked up to touch less than 1.0 since ‘13). Most investors unprepared for a period of higher conflict.

54

145

621

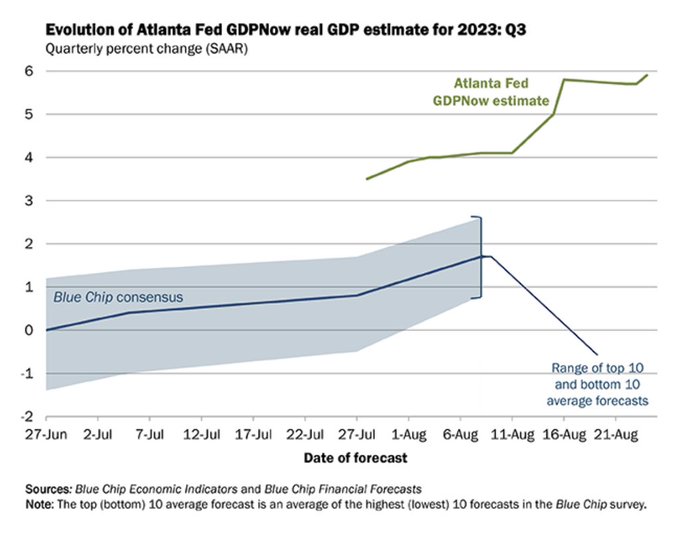

The finance world is *all in* on the soft-landing or no landing outcome.

Promoting GDPNow at 6%. '24 Earnings growth expected to be 12%. And this: 75% think either soft-landing or no-landing. Expectations of a good economic outcome this cycle have become extreme.

46

108

626

Most traders today don't have good perspective about how long can take to find an equity bottom in a downturn.

The covid bottom happened in weeks. Financial crisis bottom in months (since many mark the 'real' start at Aug '08).

It's pretty common for bottoms take years.

35

119

618

The majority of Fed board members project that thru the end of '25:

- Growth remains above potential.

- UE remains at secular lows.

- Core PCE remains above mandate (for the 5th year)

- The Fed cuts 175bps or more.

One of these is not like the others.

83

64

621

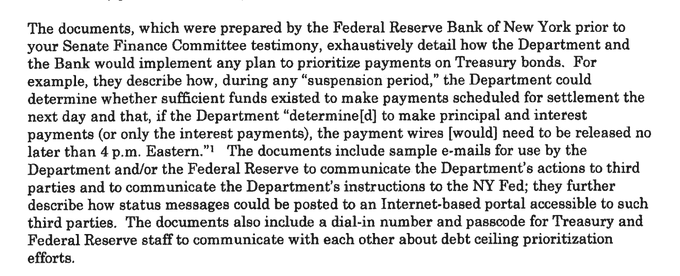

The US will not default once the debt limit is hit.

While its fashionable to breathlessly talk of disaster, it indicates a poor knowledge of the mechanics.

Treasury will prioritize debt payments. The gameplan is in place and has been discussed extensively in congressional docs:

56

131

608

Some folks think recessions get fully 'priced in' for stocks well ahead of the actual decline in activity. In reality equities bottom after a recession begins, often much later.

Dec 2007 Start - Eq bottom Mar 09

Mar 01 - Eq bottom Oct 02, but very close again in Mar 03.

26

95

610

What happens when the 2 biggest global trade chokepoints rapidly halve their combined capacity?

69

154

607

My central hypothesis is this cycle will move more slowly bc the economy is less rate sensitive than most expect.

Folks often are confused when I look at a range of indicators to test this hypothesis, particularly things are coincident/lagging. Thread.

Most investors today have not experienced a normal recession. It's important to remember that they typically take a *long time.*

A few charts about the 2000s cycle. End to end it took 3 years: the full equity market index peaked in Mar '00. That last bottom was Mar '03.

40

149

737

31

91

608

The biggest 2H23 macro question is whether core inflation will durably decline toward recent lower headline prints or not.

The answer lies in understanding wage growth vs productivity growth. Given current dynamics it doesn't look like the Fed can meet its mandate soon. Thread.

62

116

602

The regional bank 'crisis' at this point is not primarily a credit problem. Its a policy problem.

Regionals are facing a bank run because transactional businesses with transactional deposits greater than 250k have no protections to stay.

Bring back TLGP and its resolved.

83

85

606

Bonds are up 5pct vs stocks over the last week.

Starting to price in recession dynamics. Very different market action than we’ve seen for most of the year. Particularly notable on the day the strongest growth in two years was reported.

38

128

598

Today's ECI and PCE report consistent with the picture from yesterday that the Fed has not made much progress slowing nominal growth.

Economic strength today is driven by *wage growth* not credit like past cycles. ECI still running double pre-covid and not much change.

37

111

585