Viresh Kanabar

@VKMacro

Followers

3,724

Following

1,380

Media

2,306

Statuses

16,056

Explore trending content on Musk Viewer

Drake

• 3072749 Tweets

Kendrick

• 2757310 Tweets

madonna

• 640474 Tweets

Sant Rampal Ji Maharaj

• 292936 Tweets

Not Like Us

• 202060 Tweets

こどもの日

• 191044 Tweets

어린이날

• 180646 Tweets

#अविनाशी_परमात्मा_कबीर

• 149028 Tweets

Copacabana

• 144044 Tweets

Flamengo

• 113930 Tweets

Anitta

• 92854 Tweets

ケンタッキーダービー

• 71346 Tweets

フォーエバーヤング

• 62890 Tweets

Anthony Edwards

• 58959 Tweets

子供の日

• 55391 Tweets

Maidana

• 53071 Tweets

鯉のぼり

• 52168 Tweets

#UFC301

• 47285 Tweets

Timberwolves

• 40482 Tweets

Minnesota

• 37591 Tweets

Leafs

• 36972 Tweets

Katt Williams

• 29967 Tweets

端午の節句

• 29666 Tweets

Bruins

• 27011 Tweets

Vogue

• 25788 Tweets

カグヤ様

• 25705 Tweets

ゴージャス

• 25457 Tweets

設営完了

• 25303 Tweets

Fortaleza

• 20616 Tweets

Like a Prayer

• 20328 Tweets

Hung Up

• 19576 Tweets

テーオーパスワード

• 17606 Tweets

Isabella

• 16195 Tweets

Naz Reid

• 13980 Tweets

Live to Tell

• 11960 Tweets

Ant Man

• 11765 Tweets

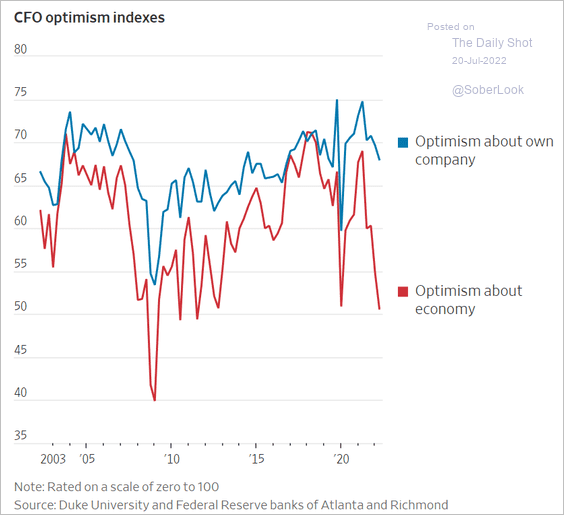

This is a pretty interesting divergence regarding CFO optimism on the economy vs. their own company.

19

72

318

Really hard to overstate just how impactful 30 year mortgages are in terms of reducing transmission

10

8

124

Really simple way of looking at spreads.

Here's ISM Manufacturing vs 2s10s. Trying to understand why the macro guys were putting on steepeners but I don't see it.

5

16

120

@Halsrethink

You might find this article interesting Harald. Something you have spoken about before too.

8

23

78

@y_alibhai

@afneil

‘You have to report on all facts that I deem appropriate, or else you’re bias’

So your problem isn’t that he’s not reporting facts, but that he’s not reporting all of the facts that you’d like to be reported. Just lol.

0

4

53

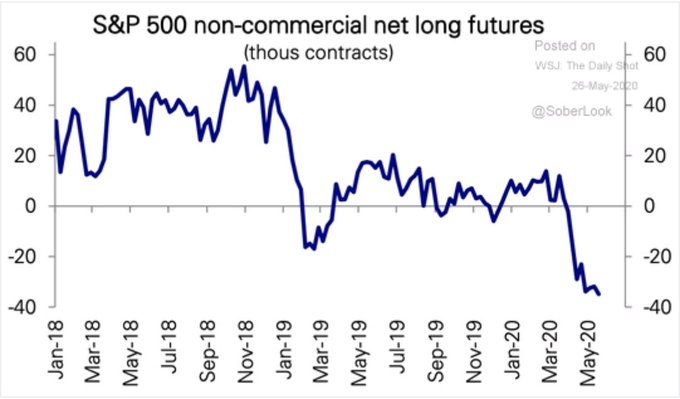

Reminder: none of them thought bitcoin would fall 50% over this period

REMINDER: Bitcoiners have been saying for awhile we would see rates at zero, massive QE, and eventually helicopter money.

Welp, we got all that in the last 3 days 🤷🏽♂️

79

322

2K

4

6

57

Rarely post personal stuff on here, but thought I might this time:

Just proposed and got engaged to my long time girlfriend

10

0

51

@agnostoxxx

1) exports are at or close to a 7year high

2) other areas such as autos, renewables, rail all use steel and have been strong

1

1

53

Worth a read

1

9

48

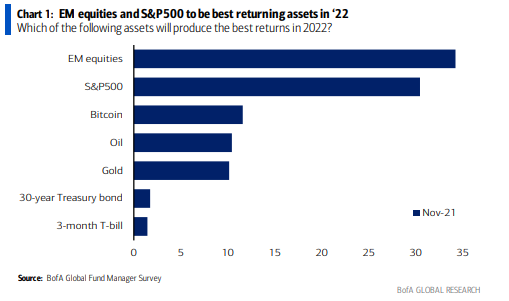

Okay, so consensus appears to be:

- EM equities to outperform US

- Dollar rally is over

- Inflationary pressures continue

- ECB to continue tightening, Fed to pause

Blackrock 2019 outlook:

- We see US entering late cycle phase

- We see fed becoming more data dependent

1

0

13

2

12

46

So you’re telling me the US equity market isn’t concentrated enough?

3

7

43

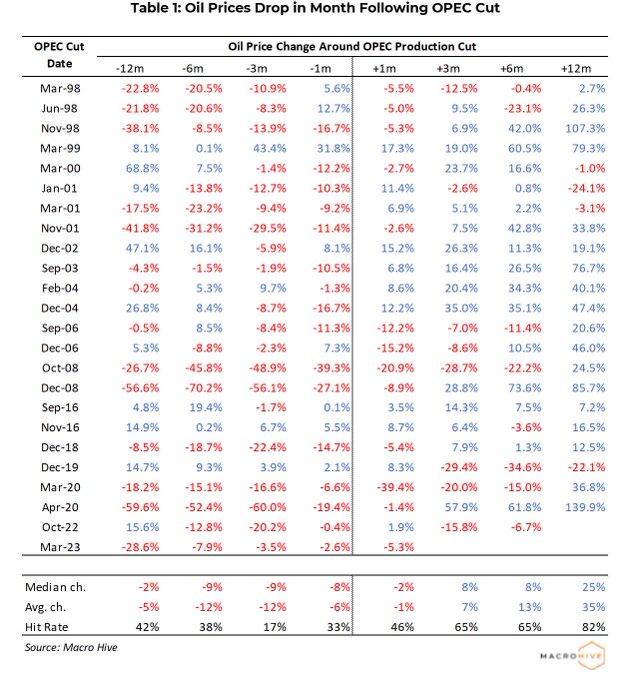

@Big_Orrin

We looked at every opec cut going back to 1998 - prices are very often lower one month later

2

11

42

From Damodaran's paper on risk premiums - the money illusion:

3

3

41

$DXY - Europe risks again underwhelming in its fiscal response to a crisis.

5

7

39

Bit late to this this one with

@agnostoxxx

and

@marketplunger1

. Good convo.

Takeaway is the goal is to make money, not to pontificate about being right

1

2

37

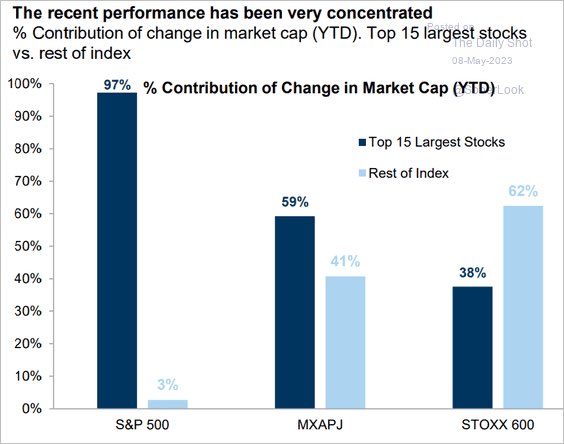

Last chart from me today: From GS showing how the top 15 stocks have contributed to YTD return across regions.

2

5

37

Best interview on macro I've heard recently.

@agurevich23

on Macro Huddle.

Discussions around process, decision making and r/r always trumps blue sky vision macro.

3

4

38

I’ve been going through Dallas and other PMI comments for ages. It didn’t read like this last year FWIW

4

8

38

Given how easy it has been for SBF to buy good coverage and political support, imagine how easy it has been for foreign actors

2

9

37

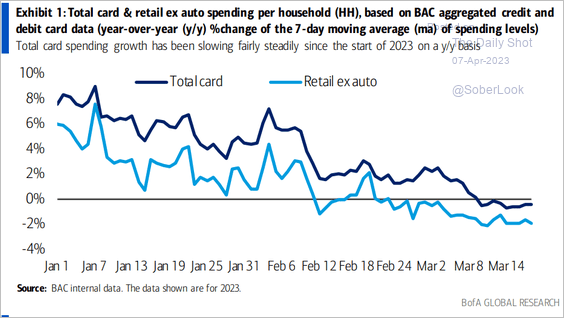

Its not just Citi's credit card data that's now declining over March

1

6

36

I know everyone’s focusing on the virus at the moment, but thought I’d share some personal news.

After 3 long days consisting of 5 events, I got married last month!

Unforgettable experience, but happy to say I hopefully will never have to go through that again though!

3

1

33

Cool Fed research looking into the Private Credit market, including loan characteristics, market size and potential spillovers.

4

7

28

Hearing a lot of talk about speculative positioning being at records for bonds and gold etc. But very few of these actually show positions as a % of OI. Gold does look like its at extremes, but 10 year treasury’s aren’t. Ht:

@movement_cap

2

10

25

Quick shout out to

@Sunchartist

for the excellent charts/ comments he’s been sharing. Must follow imo.

3

2

24

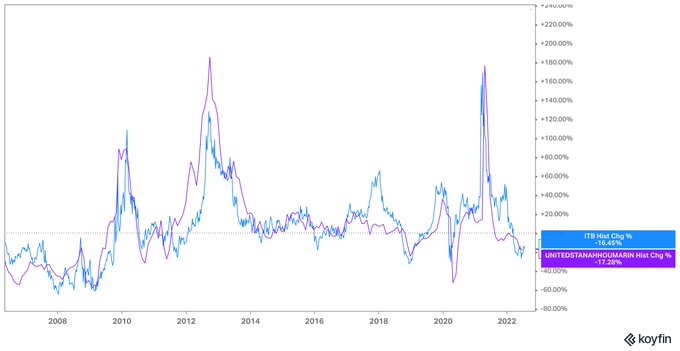

@MacroAlf

@SrivatsPrakash

Here's $ITB YoY vs. NAHB YoY. Naturally, they track each other, so question is if you incrementally believe the housing market continues to deteriorate, $ITB should continue to fall on a YoY basis.

2

1

24

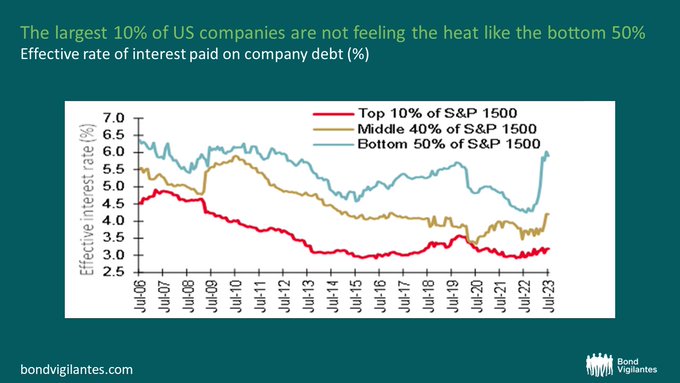

Good chart from M&G showing the effective rate paid by firms of various sizes

1

4

23

Best one so far:

Business has gotten stupid slow, and we estimate having many days of just a few hours’ work due to low volume. This is crazy—as busy as we were last year, and now for this year to have it turn off so quickly, it is hard to understand why.

3

4

21

Eurozone inventories are now at record highs relative to GDP per Simon Ward

2

4

21

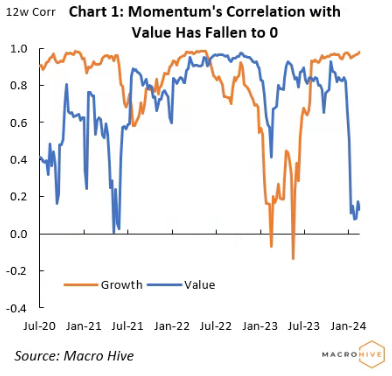

Why do people keep acting like momentum and growth is the same thing?

1

1

19

This has barely budged

2

6

20

@TheStalwart

More fiscal --> higher growth --> higher yields + broader investment opportunities are helping to take excess out of the market. Who knew!

1

7

18

Industrial earnings calls this year are a lot like Semi calls at the start of 2021.

Large backlogs, demand mostly exceeding expectations.

Talk of mega-trends helping longer term demand: sustainability, push to EVs, and IRA all given as examples.

3

5

20

In most other countries ex U.S, any benefit to the consumer from oil energy prices which will slowly filter through this year will be offset by higher mortgages rates.

So question becomes, which impact is larger?

In the US there is no such trade off. Apart for new buyers.

0

2

20

Somethings never change. EM predicted to be the best market next year!

3

6

20

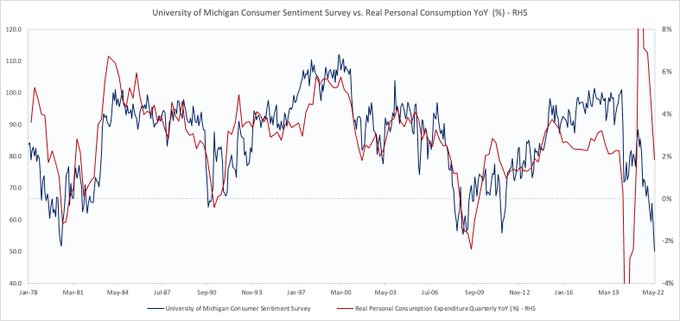

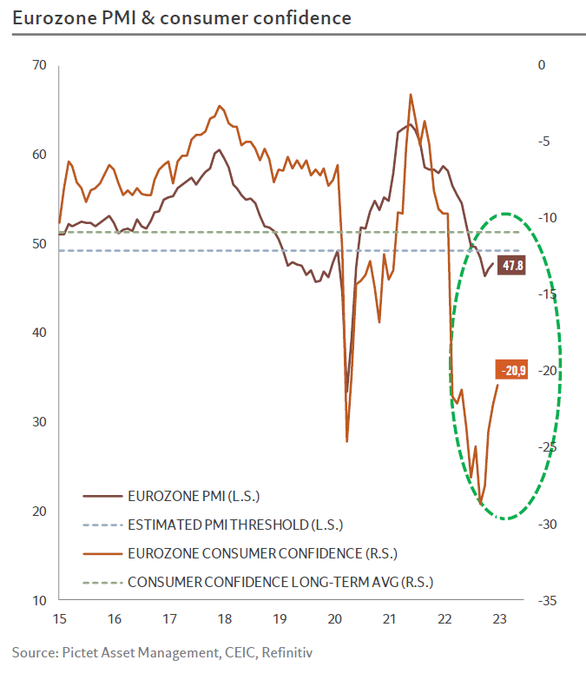

1/ Consumer confidence surveys have cratered globally.

Why does this matter?

Historically, high and rising consumer confidence is consistent is strong real consumption growth.

4

2

20

Why have average annual hours per worker in Japan fallen so sharply?

8

5

20

This cycle has been humbling af.

Markets and economies are fascinating, complex but also so fun.

Enjoy your hols!

It’s been a crazy month after a bipolar year

0

1

19

Momentum's correlation with growth is currently near 1, while its correlation with value has fallen to near 0.

It hasn't been this low since June 2021, while just 10% of value constituents can be found in the momentum index currently

0

1

18

The 3 🔑 factors in macro atm:

1) China slowing as a result of credit and monetary impulse - EZ also now slowing

2) USD decline now stopped

3) US equity market expectations are sky high. Companies no longer rewarded for beating earnings. Rev. and earning comps also high

0

2

17

Chart showing interest coverage ratio for IG constituents.

Why do we expect credit spreads to widen materially this time - even in the face of tighter lending etc.?

5

2

17

Rates are mattering less for a few stocks, but still mattering for the many

2

3

16

Just wanted to re-share this chartbook by

@Jesse_Livermore

which gives a great history of US large and smid caps

0

3

17

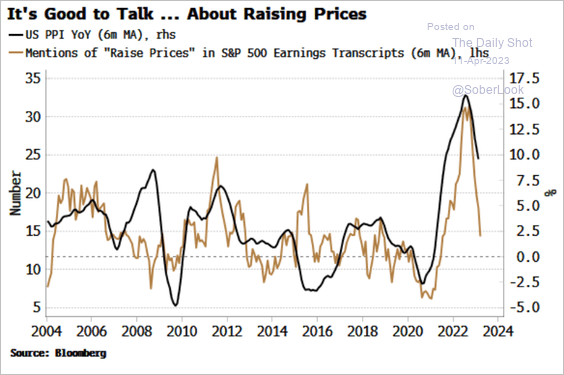

Really good chart from BBG comparing corporate mentions of 'Raise prices' vs. PPI

1

2

17

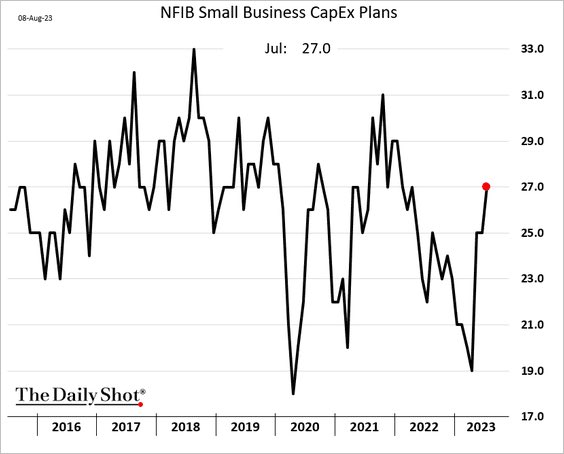

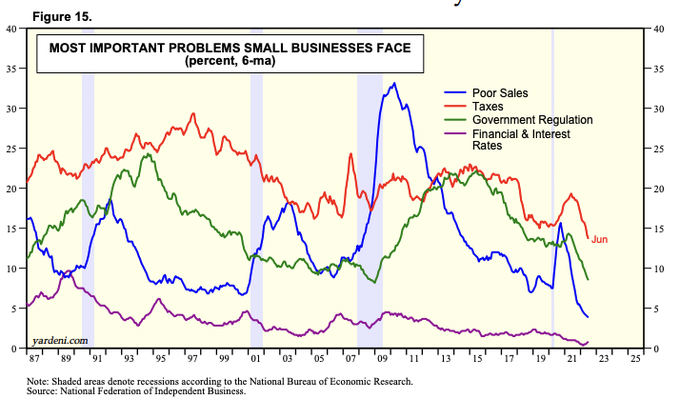

And lastly, the historic reasons for issues that are impacting small businesses don't really matter. The current environment isn't really driven by poor sales, high taxes, high regulation or high rates.

4

2

15

Jensen's comments are always worth reading in full, but this from

@TheTranscript_

is interesting!

1

5

16

This is been a wild year and a great one for both for performance but more importantly to continue my learning. As always thanks is due to all fintwit, esp..

@mark_dow

@lhamtil

@jturek18

@borrowed_ideas

@MacroOps

@jsmian

@marketplunger1

@teasri

@profplum99

@ballmatthew

5

0

15

Macro really takes a backseat to earnings over the next few weeks.

There’s nothing really new that can come from data or Fed speakers at this juncture.

However there’s tonnes of useful bottoms up information coming from corporate transcripts

1

4

15

Worth remembering that Sterling is one of the most cyclical DM currencies around. Usually follows the cycle on a YoY basis without any hassle or idiosyncrasy.

I've been short for a while.

1

3

14

How does this help?

The ECB will need to buy stocks in order to stimulate Europe's economy, says $BLK CEO Larry Fink

44

46

76

2

0

14

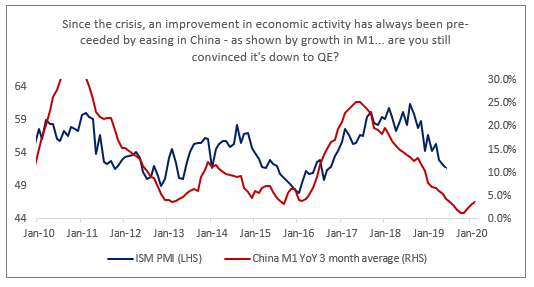

If QE wasn't preceded by stimulus in China, I'd be more inclined to believe it had a sizable impact on growth thus asset class returns...

Maybe this time we'll see what happens when you get QE, but no big easing in China

2

3

14

Japanese machine tool orders still falling. In real terms, the situation is a bit worse.

Usually, Machine tool orders are a good coincident indicator of manufacturing.

1

5

14

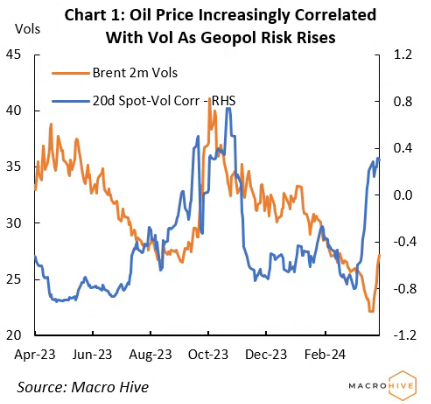

Oil's correlation with vol has risen to the highest since Oct in recent weeks, initially on Ukr drone attacks, and most recently on Iran risks

2

3

14

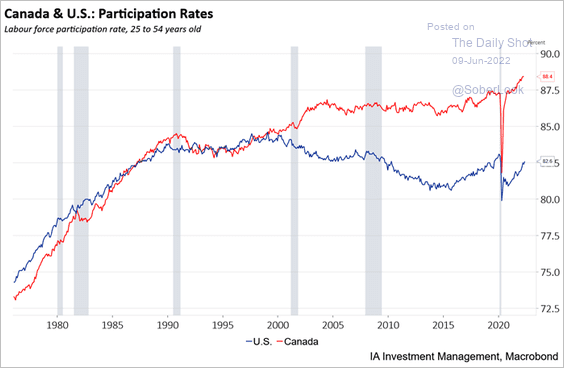

Such a striking chart which compares LFRP for 25 to 54 year olds in the US vs. Canada.

1

3

14

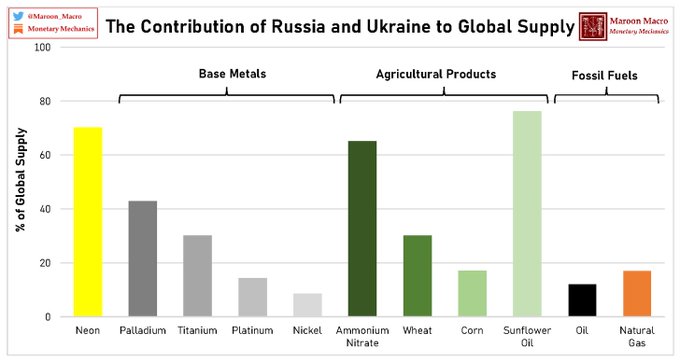

Great chart from

@Maroon_Macro

looking at combined contribution from Ukraine and Russia to supply

Monetary Mechanics Issue

#44

out now!

There have been a lot of requests for me to cover the impact of the Russia-Ukraine conflict on financial markets and the global economy.

This is part 1/2, focusing on global supply chains and commodities markets.

1

10

36

1

4

13

Best returns come when the situation goes from truly awful, to less bad (I think I’ve butchered Soros there)

Eurozone deep recession out of the cards. Even a small one is becoming relatively unlikely.

@skhanniche

#EurozoneRecession

#ECB

#BCE

4

15

32

1

5

12

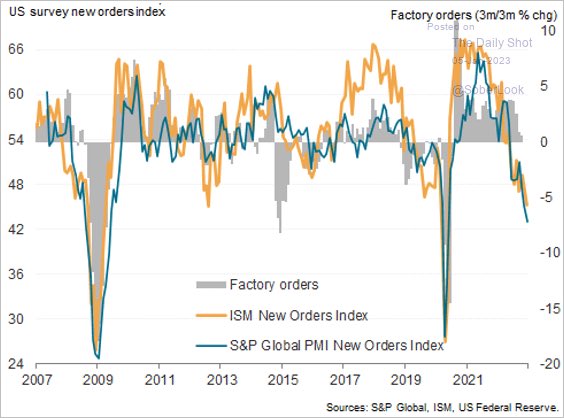

Just a chart showing ISM new orders, prices, and the historic gap.

Almost always resolves with prices falling rapidly shortly after.

Periods when the spread was largest was and for the longest duration was naturally during the 70's. Most recent period of extremes was 08

1

2

13

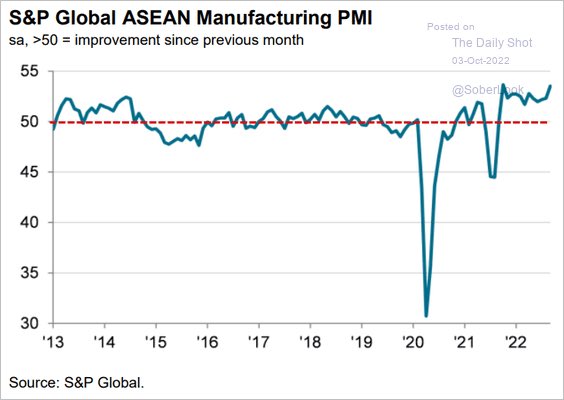

How often do we see this during a global slowdown?

Asean manufacturing PMI ticking much higher

1

5

12

Dear FinTwit,

I’m currently looking for new opportunities, would be keen to connect with those of you in London who require a macro analyst.

Please DM me if you’re interested.

0

5

13

TSMC is having g more luck building in Japan than in the US

1

3

13

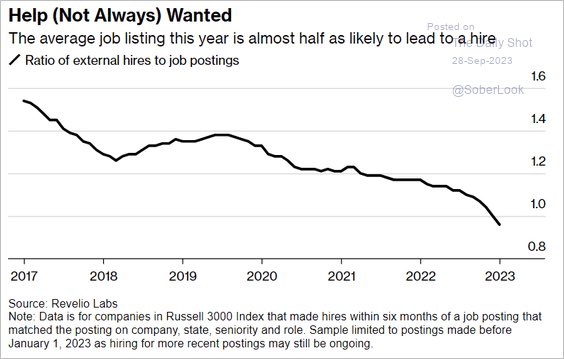

Job postings now stabilising

Online job postings aren't falling like they were earlier this year. In fact, they aren't falling at all.

The Indeed Job Postings Index has moved sideways over the past 3 months.

5

29

96

0

5

13

The Consumer Discretionary Boom has peaked.

Equal weight consumer discretionary is rolling over vs. equal weight staples.

2

1

13

This is interesting, the copper market isn’t exactly experiencing an abundance of supply atm... if global growth does rebound, expect copper to rise meaningfully.

2

1

13

Have enjoyed listening to this interview of

@DennisHong17

. 1 thing I found most surprising was Dennis talking about himself as a skeptic / negative person. I would never have got that impression based on Twitter. Also good chat around providing challenge.

0

0

13

I think we’re starting to see more ingredients of a legit shift in outperformance from US to RoW.

- Not just valuation based but that’s one element

- Big tech on big tech violence

- Continued regulatory pressures (FTC)

- Increased spending abroad (EZ)

- Rate tailwind (EM)

3

1

13

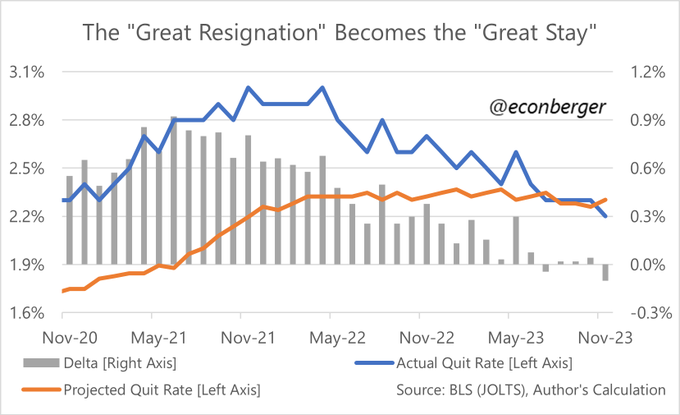

Quits as the more robust measure of future wages (versus Nfib future wage plans) continues to point to further wage disinflation over next 3-6 months.

2/ Quits rate also ticked down in November, to 2.2%. The lowest since September 2020.

Like hires, below where we'd expect given the current unemployment rate.

1

2

25

2

2

11