Diego Milano

@diegobmilano

Followers

1,562

Following

358

Media

46

Statuses

1,121

Quercus Fund Investment Manager

Ourique, Portugal

Joined July 2014

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Mother's Day

• 1277376 Tweets

Mauro

• 145377 Tweets

#DebateChilango

• 91528 Tweets

Emma

• 70398 Tweets

Nuggets

• 67045 Tweets

Wolves

• 46920 Tweets

Taboada

• 45129 Tweets

Iztapalapa

• 37952 Tweets

Clara Brugada

• 37366 Tweets

つばさの党

• 36815 Tweets

Juliana

• 34860 Tweets

Denver

• 34217 Tweets

Jokic

• 32531 Tweets

Sebastián

• 31118 Tweets

BIRTH Campaign

• 26428 Tweets

Minnesota

• 25997 Tweets

Jamal Murray

• 25814 Tweets

Cruz Azul

• 25202 Tweets

Pumas

• 23815 Tweets

Bruins

• 22801 Tweets

Benito Juárez

• 22474 Tweets

Fabra

• 20622 Tweets

家宅捜索

• 19235 Tweets

Rayados

• 17450 Tweets

Gobert

• 15995 Tweets

Tigres

• 15862 Tweets

LOSE MY BREATH REMIXES OUT NOW

• 13195 Tweets

Jordi

• 12588 Tweets

#Canucks

• 11441 Tweets

#ほっともっと16周年

• 10508 Tweets

Gambino

• 10316 Tweets

Pinned Tweet

Quercus Fund website () is finally available!

There you can find all our Letters to Shareholders, and much more.

Check it now, and subscribe

1

1

13

@JTLonsdale

The book “Concrete Planet: the strange and fascinating story of the world’s most common man-made material”, by Robert Courland, shows some interesting perspectives over Roman concrete characteristics.

1

8

98

Our 2024 First Letter to Shareholders has just been released!

3

10

69

“You build your network, tools, screens, relationships like a spider builds a web. You keep building it out. Then one day something hits the web. You feel the tremor and you go look at what you caught. This is how the great ideas find you.”

New Article

Great investors develop Active Patience. Active Patience means knowing what you are looking for and doing nothing until you find it.

16

75

308

2

7

30

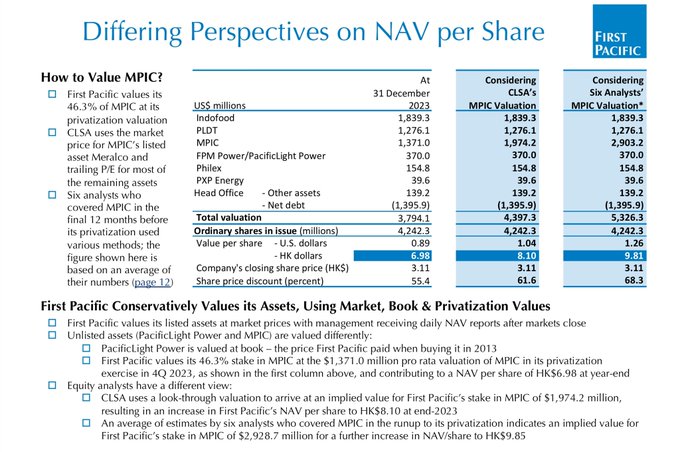

The most interesting chat on $142.HK FirstPacific results

It does not address the discount on discount of Indofood / ICBP or the undervaluation of PLP (at BV), but it is a start

(Trailing P/E for the non-listed MPIC assets is extremely conservative, for both MPTC and Maynilad)

3

2

29

@SchopenhauerCap

Have a look at (Peugeot Invest).

With shares today at 105.6, you get 114 EUR/share in their stake in STLA, plus another 110/share in other net assets.

2

0

29

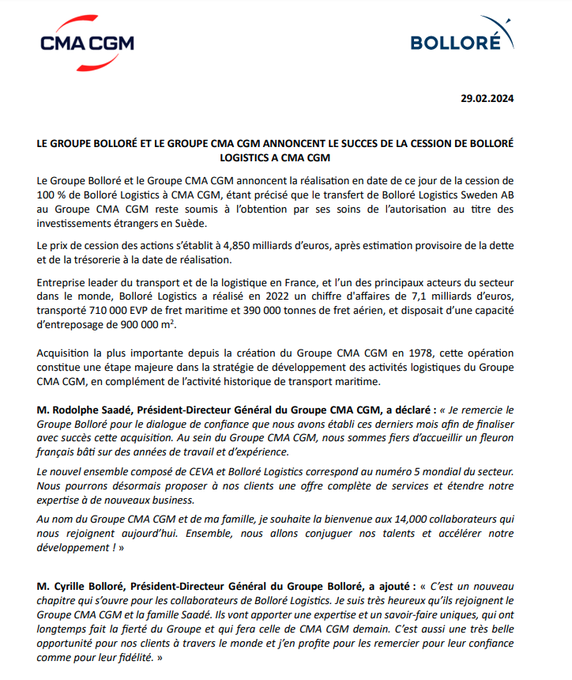

EUR 5.7bn bid for Bolloré Africa. Official.

@LuchesiPhilippe

@ohcapideas

@EricKoop3

@off_the_run

@french_special

@FoxCastlehold

@chriswmayer

@GWInvestors

@DapperDanMan0

3

1

23

I have a dream.

To be able to say that $882.HK is trading at a P/E ex-cash of 1.0x

It only has to go up about 150% before that. Probably more after 2023 results.

4

2

24

$HSBK less than 2.7x P/E on 2024 guidance

I feel fine with >30% 2024 ROE

4

3

23

@sinstockpapi

$882.HK, Tianjin Dev, is worth >5x its market cap right now, by its stake in Otis China +net cash.

If it doubles in 5-10y, it’s a 10-bagger (1H21 is not out yet, but Otis results implies China profit is +25% YoY).

And there are still a few other valuable subs, some listed.

6

0

22

$3382.HK Tianjin PortDev with a positive profit alert for 2023… +110% to 120% YoY.

$882.HK TianjinDev owns 21% of it.

Its segment profit of the port operations should be HKD 150-160mm

1

0

21

3Q23 results were published for Indofood, MPIC and PLDT.

It’s highly likely that $142.HK FirstPacific 2023E core income will be higher than USD 600mm, +20% YoY. And counting.

Its mkt cap? USD 1,500mm.

4

2

18

$142.HK FirstPacific

Indofood results: IDR 9.8bn in core profit, up 8% YoY - roughly $300mm to FPC, which owns 50% of Indofood

Due mostly to Indofood CBP results (80% owned by Indofood), with core profit up 27% YoY to IDR 9.3bn.

2

1

18

$142.HK

+22% YoY 1Q24 net profit for MPIC, 46% owned by FirstPacific.

Not bad

0

1

17

$142.HK FirstPacific:

Meralco core net income up 37% YoY in 2023.

That’s 20% above MPIC TOTAL net income in 22 ⚡️(we still have toll roads, water, light rail, hospitals… and yes, net debt)

MPIC has a 47.5% stake in Meralco (FPC owns 46% of MPIC).

1

0

17

Tianjin Port Holdings net earnings +9% YoY in 1Q24

That is on top of a 33% growth in 2023

$882.HK TianjinDev owns 21% of $3382.HK TianjinPortDev, which owns 56.8% of Tianjin Port Holdings

2

2

17

As expected: 70% to 80% increase in 2023 net profit to owners for $882.HK TianjinDev.

(Just a reminder that only 1/3 of the one-off gains of Lisheng Pharma flows to the owners of TianjinDev, so I guess less than 15% of the profit is non-recurring)

4

0

15

My guess is $2198.HK (Sanjiang Chemicals) trades at a P/E of less than 1x, on forward earnings

Even better if we get to mid-cycle in 2024/25

(It had negative gross margins in 2022, but should have a completely different profile now that the new plant is operational)

I am long.

1

0

14

Easter bunny brings us a 37% increase in dividend from $882.HK TianjinDev

Also, with the normalization of A/R, net cash ex-Lisheng Pharma up to HKD 3.90 per share. 230% of the mkt cap lol.

Profit in line with the already published results from subs.

3

0

15

Less than 1y ago, $3378.HK Xiamen Port was delisted for 2.5x the price it was trading.

Less than 6m ago, $SNG.PL Sonagi paid in dividends 2.2x its whole mkt cap where it has been trading for years.

Nothing happens for a long time in small caps. Until they suddenly do.

2

0

15

Ok, now I have something to do. TianjinDev Annual Report is out.

0

0

13

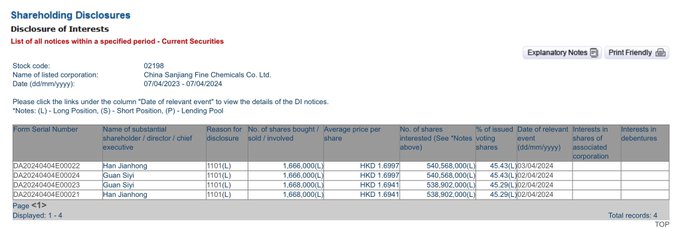

The controlling family of $2198.HK Sanjiang Fine came back to the market buying shares, at 1.70 HKD/share.

Last time they were buying was in 2022, around 1.50, and 2021, around 2.40 HKD/share.

2

0

13

@morganhousel

Coincidentally, I started reading it yesterday. First chapter already blew my mind with stats like “75% of all births during the next 50 years will happen in Africa”.

0

0

12

@IrrationalMrkts

$882.HK Tianjin Dev, $220mm mkt cap

- Trades at less than 3x P/E

- Net cash more than 2x its mkt cap

- Stake in Otis China worth at least 2.5x its mkt cap

- Stake in 2 listed cos 1.4x its mkt cap, at market prices

And a bunch of other assets

2

0

12

@FocusedCompound

$882.HK, TianjinDev. Net cash is twice the size of mkt cap. A conglomerate structure hides a very high quality business (Otis China), easily worth 3x mkt cap. Also, stakes in listed companies worth >100% of mkt cap.

2

1

12

Am I seeing things or, considering the just released MPIC 1H23 results, First Pacific ($0142.HK) is trading close to 2.5x P/E, on 2023 core income?

4

1

12

$142.HK First Pacific

This is quite relevant: Meralco (47% owned by FPC) will participate in a JV for a new combined cycle plant and LNG import/regas terminal, total investment of USD 3.3bn ($1.2bn in equity by Meralco)

Meralco is underlevered, 0.1x.

3

0

11

Can someone tell me why $ODET is up 10% this morning, on a huge volume and no new news? Not that I am complaining, quite the contrary…

@ohcapideas

@EricKoop3

@french_special

@FoxCastlehold

@LuchesiPhilippe

@GWInvestors

@chriswmayer

2

0

11

@jay_21_

$0882.HK, TianjinDev, by miles

2.5x mkt cap in cash + 1.5x mkt cap in two listed companies + 3x mkt cap for its stake in Otis China.

And other assets too.

Less than 3x recurring P/E.

What can close (part of) the gap? Do something with the cash (M&A, dvds…)

3

2

11

@FocusedCompound

Ok, here I go.

$882.HK. 2x the mkt cap in net cash.

A stake in Otis China (elevator is a great biz), that at a mere 15x would be worth more than 3x mkt cap.

Stakes in listed TianjinPort and Lisheng worth another 1.5x mkt cap.

And 2x mkt cap in other assets. Keep that as a change

1

0

11

@DapperDanMan0

@ohcapideas

@FoxCastlehold

@FrenchCMunger

@chriswmayer

@GWInvestors

@foso_defensivo

@valueDACH

@vitaliyk

@LuchesiPhilippe

@evantindell

@EricKoop3

@smallandvalue

@off_the_run

Excluding draconian moves (possible), imo the best way for VB to increase the value for himself is to buy more $ODET and $BOL shares at his 100% owned holding (Bollore Participation SE), before any simplification. Now, in order to do that, the divs must indeed flow again to $BOL.

1

0

11

@alluvialcapital

TianjinDev, $882.HK.

2.5x its mkt cap in net cash +

1.5x mkt cap in two listed companies +

3x its mkt cap for its stake in Otis China

Oh, they also have other assets but we can stop counting xd

At less than 3x P/E, on recurring earnings.

Seems like a mirage…

1

1

11

@ClarkSquareCap

@Larryjamieson_

Hmm I’ll try to be brief:

$882.HK <2x net cash AND <3x P/E AND >70% discount

$142.HK <3x P/E AND >70% discount

$HSBK < 3x P/E (is bank cyclical?🧐)

$743.HK <2x net cash (Cement🤢in China🤮)

4

1

10

Ahahaha “we already have the buyback authorisation by the shareholder’s meeting”

0

1

10

Wondering if the 20% move in PLDT’s ADR today will be reflected in $142.HK FirstPacific (which owns 25.6% of PLDT) shares… 🤔

2

0

9

$142.HK First Pacific

MPIC (46% owned by FPC) 2023 results are out.

We still lack operating details, but net income in line with unofficial guidance: 19.9bn PHP (vs 14.2bn core profit in 2022).

0

0

10

What are underlying returns of $142.HK First Pacific?

If we exclude from the balance sheet only the goodwill related to Pinehill acquisition, and keep everything else, 2023E ROE on a recurring profit basis is expected to be 25% - 30%.

(1/2)

1

0

10

And EUR 200mm more than at the time when they entered into the deal

0

1

10

If no one says it, I will.

I think Bolloré should buy HK bargain stocks with its giant pile of cash 🙃

4

0

10

Vivendi’s Canal+ has a 30% stake in Viu

2

1

8

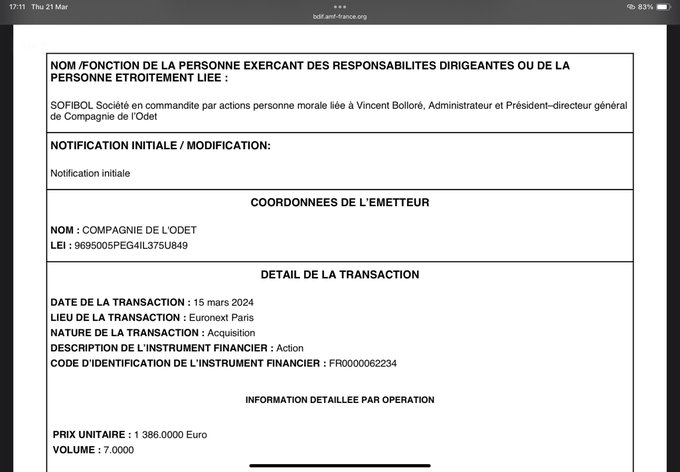

In the first day it was Sofibol… interesting 👏👏👏

$ODET.PA

1

0

10

“Hey $BOL.PA, it’s $ODET.PA here. Why don’t you take 538mm of your own shares in exchange for the 2.34mm shares of Odet you own?

At current prices there would be no cash involved”

@FoxCastlehold

@LuchesiPhilippe

@abroninvestor

would that be possible / allowed?

@YannickBollore

5

0

10

Halyk Bank results are out $HSBK

Includes 25bn KZT one-off expenses

1

0

9

Xiamen Port ($3378.HK) is being bought out by its controlling shareholder @ 12.5x 2021 P/E, or 0.9x P/BV, 140% above a month ago.

If Tianjin does the same, that’s 170% upside for Tianjin PortDev ($3382.HK).

Or 135% of TianjinDev ($882.HK) mkt cap. Just one subsidiary.

0

0

8

At current prices, $PEUG.PA stake in $STLA is worth more than EUR 150/share

0

1

9

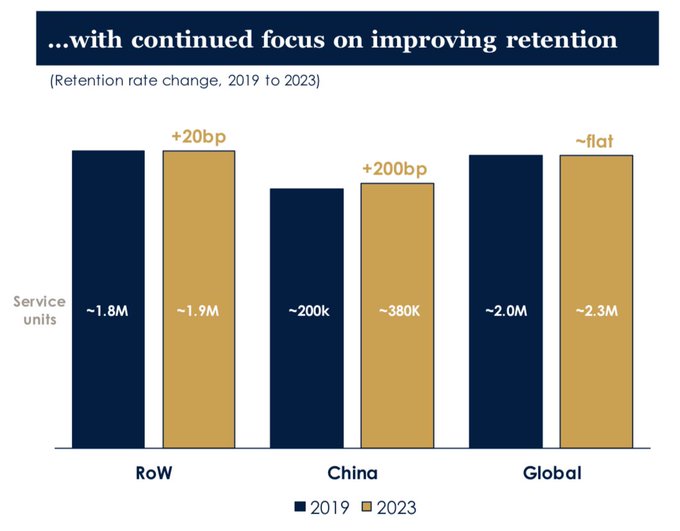

Today is $OTIS Investor Day.

Outlook of 10% EPS CAGR medium-term (up to 2028). Almost all from growth in Services.

If China represented 60% of the growth in service units in 19-23, how much of the 24-28 growth is expected from China?

Just wondering… ($882.HK)

0

0

9

$142.HK

2

0

7

$142.HK

From Meralco results, we can also infer how much FPM Power/PLP will contribute to group net profit:

In 2023, $110 to 120mm (vs $82mm in 2022)

FPM Power is accounted for only $370mm in FPC’s last reported NAV.

Discounts over discounts…

1

0

8

$BOL.PA $ODET.PA

How much does a gigafactory cost? Asking for a friend

1

0

8

$142.HK First Pacific

1

0

8

Mozambique, Ethiopia, DRC, Rwanda, Uganda, and now Zimbabwe.

At this pace, in a couple of years $2233.HK West China Cement may become the largest cement producer in sub-Saharan Africa ex-Nigeria (Dangote is currently

#1

, and by far the largest in Nigeria)

2

0

8

@OtterMarket

Sonagi in Portugal. 80mm in RE, 70mm in cash after selling a non-core investment. 40mm mkt cap.

1

0

8

@SebKrog

2026?

First Pacific $142.HK

Halyk Bank $HSBK

Sanjiang Chemicals $2198.HK

West China Cement $2233.HK

Tianjin Dev $882.HK

1

0

8

@ToffCap

And trades at another 60% discount to NAV, of which 50% is STLA

In other words, you get a bunch of other stuff in addition to STLA for free

3

1

8

@EricKoop3

@OlmesJo

@GWInvestors

@off_the_run

@ohcapideas

@DapperDanMan0

@french_special

@smallandvalue

@FoxCastlehold

@FrenchCMunger

@chriswmayer

@foso_defensivo

@valuedach

@vitaliyk

@LuchesiPhilippe

@evantindell

200k more on the 10th... okay, it has become everyday routine

1

0

8

@french_special

@off_the_run

@ohcapideas

@smallandvalue

@EricKoop3

@FoxCastlehold

@DapperDanMan0

@chriswmayer

@GWInvestors

@foso_defensivo

@valuedach

@vitaliyk

@LuchesiPhilippe

@evantindell

Seems most likely, yes. But I’d not rule out $BOL.PA distributing the $VIV.PA stake, repeating the “tax deductible only over 5%” playbook, opening space for more buybacks on the cheap before any takeover premium, since its effective stake would go down from 30% to 19% (30% * 64%)

1

0

8

I wish HKEX does that to improve market sentiment and…

… no, wait

The Tokyo Stock Exchange will require all of the approximately 1,600 companies listed on the prime market to disclose material information in English from March 2025.

Good news for foreign investors.

0

11

121

1

0

8

@CCM_Ryan

Anything? I’ll try again:

$882.HK, TianjinDev

SOE in China

HKD 1.7bn mkt cap

- 2.2bn in two listed cos

- 3.0bn+ in net cash

- 16.5% stake in Otis China, where they get 300mm+ in profits, 40%+ROE. Otis would jump at the opp. to buy it at, say, 5.0bn

- xxx in other assets

5

0

8

@ohcapideas

@foso_defensivo

Using your numbers, $ODET discount gets close to 85%! $BOL.PA is extremely undervalued, but I think Odet is a better alternative for anyone managing less than $50mm in AuM.

1

0

7

@RodAlzmann

Are net-nets asymmetric enough?

Hidden gems within companies that hold more net cash than their mkt cap:

- Otis China for free with $882.HK TianjinDev (<3x P/E)

- Universal Music Group for free with $ODET.PA

1

0

7

@Steven_Kiel

How can you have more asymmetry than with a company with net cash 2x its market cap, listed stakes worth >100% and a stake in Otis China worth 4x its mkt cap?

The downside is what, to trade at 1/4 of cash?

EV/earnings = 1 (!) => 150% upside

$882.HK Tianjin Development Holdings

1

0

7

@sinstockpapi

I think worst case is the city forces it to buy shitty assets at outrageous prices, so all cash is lost (though SASAC usually arbiters it well enough).

But I don’t see how the value of Otis China can vanish, apart from an unthinkable nationalization. They are parters since ‘84.

2

0

7

Whenever you find you are being too aggressive with your market orders, think of the controlling family of $2198.HK Sanjiang Chemicals who bought more than 40% of total traded shares during the whole month of April…

…AFTER the stock was up 70% in March

0

0

7

$3382.HK Tianjin PortDev

$882.HK TianjinDev

+7.2% YoY growth in TEUs for Tianjin Port in 1Q24.

Not bad.

0

0

6

$3382.HK $882.HK

It seems that TianjinPort showed 5.5% increase in TEUs in 2023 (up from 2.2% in 1H22).

Not bad

2

0

6

Interview with $HSBK Halyk’s CEO.

Nothing really new…

1

0

6

Mkt value of $142.HK FirstPacific right now is less than its stake in listed Meralco.

With net debt about the size of PLDT stake, that gives us Indofood…. For free.

Together with all its other assets

2

0

6

@daniel_toloko

I thought the only stock that could consistently trade at hugely negative EV (ie net cash >> mkt cap) was Surgutneftegaz.

Then I found another one, $882.HK TianjinDev. After a few months calling attention to it to all my 87 followers (😜)… nothing changed :p

1

0

5

@Alex__Pitti

Sonagi, in Portugal (SNG). EUR 41mm mkt cap, has a 10.8% indirect stake in Semapa (listed), which at market prices equates to EUR 100mm (at sub 6x P/E). Plus a bunch of real estate assets worth more than its mkt cap.

Good luck trying to buy any shares though.

0

0

5

$142.HK

Indofood core profit +10% YoY in 1Q24.

Seems like they are raising cash? For… something? Waiting for ICBP results for more details

1

0

5

I don’t have any position, but the recovery of production of iron ore pellets by Ferrexpo ($FXPO.LN) in 1Q24 in Ukraine was really impressive

1

0

5

$142.HK $ICBP $INDF

“Between 2018 and 2022, Nigeria (…) saw a 53% jump in demand, from 1.82bn servings to 2.79bn (…). While countries such as Kenya (…) grew by 160% (…) and 110% in Egypt.”

Also, the bad (salt, sodium, addiction)

0

0

5

@FoxCastlehold

Imperial Mediterranean is within the controlling loops,controlled by Bolloré SE, right? Even better 🤗

1

0

5

@david_katunaric

When your small caps’ next earnings releases are months away because they only update the investors 2x a year 😝

0

0

5

Thank you for the opportunity,

@capitalemployed

Hope you all enjoy the reading!

FRESH OFF THE PRESS 🔥

Read our interview with

@diegobmilano

from Quercus Fund.

Diego is a deep value investor and shares his thesis for investing in two Hong Kong listed stocks that are selling wildly below their NAV. 👇

0

2

4

0

2

5

Two important (long-term) highlights for Otis China in 1Q24 conf call:

“China (…) becoming more of a mature market and reflecting that, especially in Service”

“Service now being 25% of our revenue in China and growing”

25% of rev means what, 40% in op profit maybe? Not bad

1

0

5

Tears….

0

0

5

If you want to post something in Fintwit that no one will even read, this is the time.

You have until tomorrow night.

0

0

4

$0882.HK just released its 1H23 results

Net profit 36% YoY

2.3X P/E on annualized 1H23 🤔

2

1

5

$ODET.PA $BOL.PA

Does that change the expected date of closing of the deal?

1

1

5

When Shanghai and Shenzhen stock markets open on Monday

Doggo's First Day Back At Work After Having A Week Off

401

3K

40K

0

0

5

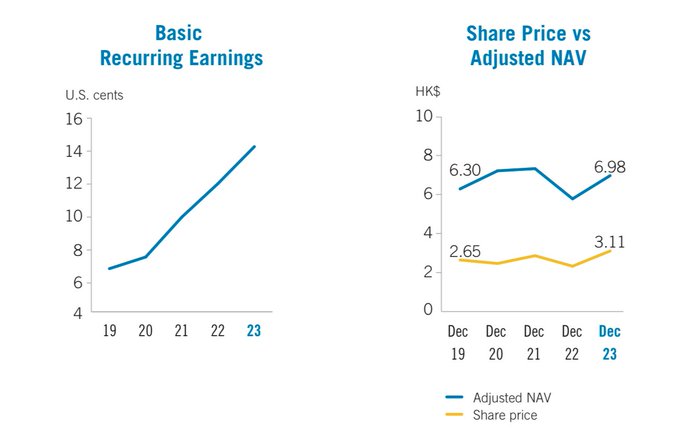

The charts I like the most at the $142.HK FirstPacific annual report

Why people keep focusing on the left one?

Don’t bother answering, it’s rhetorical

1

0

5

@evfcfaddict

@NICKRADICAL4

@DavidDiranko

@JoashReid1

@Jave_t23

@acidinvestments

@mind_the_bear

@JonathanPaxx

@Tintincapital

@RhinoInsight

Truly happy and honored to be on this list! 🤗🚀

1

0

4

$HSBK in KASE trades at almost 6% premium to its GDR in London.

I suppose in this particular case it’s not that easy to arbitrage…?

1

0

5

This kind of disclosure would be an interesting practice for any conglomerate / holding company, but especially those listed in HK.

0

0

5

@off_the_run

@ohcapideas

@EricKoop3

@DapperDanMan0

@french_special

@smallandvalue

@FoxCastlehold

@FrenchCMunger

@chriswmayer

@GWInvestors

@foso_defensivo

@valuedach

@vitaliyk

@LuchesiPhilippe

@evantindell

230k+ shares again on the 8th. I suppose we will see such buying activity for a lot more days...

Besides, seems that ODET is leveraging in order to do that (I would guess giving BOL shares as collateral).

2

0

5

@TheLongHappy

@Bonhoeffer_KDS

@dodgingalpha

@roojoo3

@ReturnsJourney

For FPC? I’d guess a total distribution of at least usd 150mm going forward (9% yield).

Probably growing HSD every year.

That considers 35% payout for Indofood, 60% for PLDT, 0 for MPIC and close to 100% for PLP.

Indofood payout should grow when it delevers

2

0

5

@Larryjamieson_

Only net-nets with at least 200% of the mkt cap in net cash, less than 3x P/E non-cyclical, and conglomerates at 70% discount to NAV.

Low liquidity is a plus, hair is a must.

2

0

5

@FriendlyCapMgmt

@SchopenhauerCap

I think the same way as

@walter_schloss

does: you get STLA at a discount plus a lot of assets for free.

So yes, I think it is far more attractive.

0

0

5