John Mihaljevic

@JMihaljevic

Followers

11,093

Following

2,858

Media

94

Statuses

4,071

Chairman @manualofideas , The Zurich Project, and Ideaweek St. Moritz. Co-Host @twiii_podcast . Author, The Manual of Ideas. Value investor with a growth mindset.

Joined August 2011

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

#RafahOnFire

• 712988 Tweets

#مجزره_رفح

• 140321 Tweets

NASCAR

• 79530 Tweets

Eugenio

• 68788 Tweets

#AEWDoN

• 64037 Tweets

都知事選

• 60842 Tweets

İsrail

• 58994 Tweets

Rangers

• 51062 Tweets

Pato

• 39378 Tweets

Cruz Azul

• 30487 Tweets

Lively

• 25638 Tweets

Larson

• 25433 Tweets

ドラクエの日

• 23740 Tweets

Bahia

• 20206 Tweets

蓮舫さん

• 17212 Tweets

雨の月曜日

• 14851 Tweets

人身事故

• 10974 Tweets

While investors trip all over themselves to get into $NVDA, Sam Altman makes a fascinating point:

"Energy is the hardest part."

Now think about how the market values AI darlings versus energy companies.

Am I the only one who smells opportunity?

Sam Altman: compute is going to be the currency of the future, maybe the most precious commodity in the world

142

339

2K

72

98

636

How do you model a DCF when management tells you this:

"We may earn a profit when revenues are high, and we may lose money when revenues are low, but our goal is to roughly operate the company at break even..."

$COIN

63

28

506

Position sizing: When you're right, it's too small. When you're wrong, it's too big.

15

47

491

One of the biggest things I've learned as an investor is that if you are buying within a 10-20% range of your desired entry price, what matters much more than your actual entry price is your allocation to the idea. A great idea without a great allocation is a waste of insight.

20

44

412

🧵 highlighting ten investment ideas from Best Ideas 2023, the online summit hosted by

@manualofideas

I shared these investment theses a couple of days ago at

@GSpier

's fantastic

@VALUExZH

Klosters conference. Thank you, Guy, for bringing together such a great group of people!

5

55

331

Whoa! This gem of a video just came out. Featuring

@mjmauboussin

,

@HowardMarksBook

, and other great investors/authors.

6

79

322

If you invest in good companies at reasonable valuations, and if bitcoin becomes the currency of the future, those companies will produce a lot of bitcoins for you. You are long the bitcoin bull case automatically by owning equities. Absolutely no need to buy bitcoin outright.

31

37

305

So many brain cells wasted on trying to predict what the market will do next. Why not just buy undervalued businesses and wait, especially if you invest for your own account?

50

23

291

Value investing has underperformed because much of it was "shortcut investing" -- relying heavily on metrics like P/B, P/E. I am seeing a lot of "shortcut investing" on the growth end these days -- much reliance on a narrow set of KPIs, too little focus on sustainable advantage.

11

21

240

Grateful to

@AswathDamodaran

for sharing his wisdom in this remarkable conversation with

@veiled_value

about the book, The Dark Side of Valuation.

Excerpts follow in this thread.

Members, access the full interview below.

4

67

240

When someone says, "I didn't grasp the investment case at $10 but now at $30 I finally do," what they're often saying is, "I couldn't handle the fomo any longer."

9

15

235

Netflix vs. Youtube.

That's the real battle in the media landscape.

Highly-produced vs. user-generated content.

Both have a place, but my hunch is that user-generated will keep gaining share (not the silly cat videos, but the super-niche stuff you can find only on Youtube).

33

20

220

Now that I've gone down the crypto rabbit hole, I honestly don't see how crypto improves things. Building less efficient architecture in order to achieve decentralization makes no sense. We need to work on making the world better, not on building systems for a dystopian future.

23

17

209

Many libertarians love crypto, but crypto reminds me of communism.

Why?

Communism was conceived as a "better way" to organize the rules of human financial interaction.

Yet, crucially, it failed to take into account human nature, as does crypto.

15

16

197

Just as fintwit capitulates on $BABA, a glimmer that the old man could still turn out to have been right. Time will tell.

14

3

192

The Nasdaq bloodbath is nothing compared to the coming crypto bloodbath.

8

5

196

The same people who now happily pay 14x revenue for Microsoft will not be willing to pay 14x earnings for Microsoft in the future.

And they will have clever-sounding reasons for both.

6

11

184

As an investor, an economics degree clearly wasn't the right choice. Pretty much anything else would have been better. Philosophy, history, psychology, anthropology, religion. Anything but economics.

30

14

186

Nearly everyone dissed $META below $100 per share.

150% later...

...suddenly people like it.

That's *not* the way to invest.

Gotta be able to go against your own sentiment if you want to make money in a pari-mutuel betting system.

31

21

185

Carvana is a good example of sophisticated investors not seeing the forest for the trees. If you had just looked at the "forest" -- a supposedly disruptive leader that can't turn a profit even on an adjusted EBITDA basis -- you would have questioned the quality of the business.

32

9

176

Socialism is nothing more than people's inherent laziness unleashed. With no incentive to create, most people choose to do the bare minimum. In the end, the socialists don't take money from the rich, because there is nothing left to take. Everyone is poor, except those in power.

13

23

167

If you own $GOOG and want to get a feel for the threat ChatGPT poses to Google search, you may like to install this Chrome extension. It generates a ChatGPT response alongside every Google search query.

4

10

171

In investing, you can do really well when a company goes from horrible to bad.

14

4

163

Small investors are ceding their only real advantages too easily:

1) ability to invest in small caps --> prefer well-covered big caps

2) ability to think independently --> prefer following the herd

3) ability to invest for long term --> prefer high-turnover trading

7

20

155

This conversation with

@AltaFoxCapital

was one of my favorite interviews in a long time. Connor talks candidly about the firm he is building and a couple of fascinating case studies in standing up for the rights of owners. Lots of lessons to take away.

3

12

158

If growth companies with great products are getting hit this hard (e.g., Netflix), just imagine what could happen to cryptocurrencies, which have zero utility in real life.

9

11

157

Jack Ma records 50-second video, adds $50+ billion to $BABA market cap. At a billion a second, he should have kept talking. 😃

6

14

148

Crude oil futures for December 2023 are now above $75 per barrel.

$RIG stated on a past earnings call that an oil price in the mid-$50s would bode well for its business.

When will investors realize that offshore drilling may finally be entering a major new upcycle?

21

13

146

Huge fan of

@AswathDamodaran

. Maybe it has something to do with learning valuation from him all the way back in 1998 during Merrill Lynch's investment banking analyst orientation. So great to see him continuing to share data, analysis, and insight. Thank you, Professor Damodaran!

4

8

138

"We are seeing very substantial inflation. We are raising prices, people are raising prices to us. [And it's being accepted.]" --Warren Buffett

4

24

138

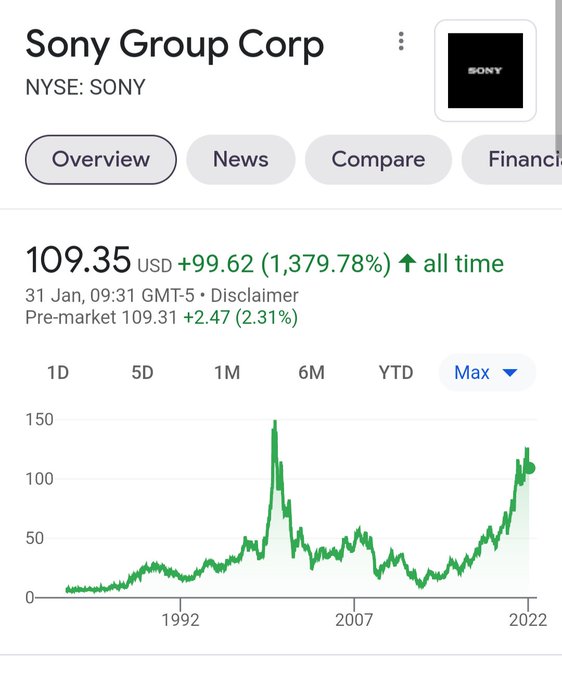

When Sony shares peaked around $150, how many people would have predicted that more than two decades later $SNE would still trade below that level?*

How many investors today are open-minded enough to consider such a possibility for $AAPL?

‐--

* not adjusted for corporate events

39

15

137

Relief rally

Correction

Crash

Meltdown

Meltup

Sideways market

All mini-narratives that give investors the false illusion there is a method to the market's short-term madness.

No one knows.

Focus on the long term.

4

15

134

I always chuckle when someone in their teens or twenties says "you only live once" or "life is too short" to justify doing something stupid.

Actually, life is really loooooong if you have to live permanently with the consequences of having done something stupid.

4

11

129

Talk is cheap. The guy who actually democratized investing is Jack Bogle.

3

14

124

Investing might be the only field in which if your product is amazing, you don't need customers.

4

18

124

On a mistakes-adjusted basis, my track record is amazing.

8

8

123

I see a lot of portfolios these days that look like wishlists one would put together if one knew nothing about the market quotations of the underlying businesses.

5

7

113

Some books deserve to be reread dozens of times over a lifetime.

They are not just books, but philosophies, playbooks, blueprints.

A great book is the north star that will help you resist peer pressure and keep you from succumbing to the mediocrity of conventional wisdom.

12

13

117

An eye-opening conversation on the semiconductor industry with

@jbathgate

.

Jon and his colleagues nailed the industry dynamics before the enormous value creation at companies like $TSM and $NVDA became apparent.

Indebted to

@RishiGosalia

for the intro.

5

20

115

Anchoring is a well-known cognitive bias in investing. Less well appreciated is that we tend to anchor not only to price but also to sentiment. An ability to imagine a change in sentiment is a superpower.

2

9

114

$FRC = the ultimate contrarian investment right now. If I get paid buying it here at $31 per share, it will be directly as a result of allowing the seller to sleep better at night. Feels like I'm in the service business on this one.

23

6

113

It's funny how whoever ends up on the losing side of a particularly nasty bet -- dial in $GME shorts -- claims the market is broken. The market is what it is. It might be time to give more credence to the role of human nature. That, my friends, has not changed much lately.

4

9

111

Anyone else think that travel, leisure, and entertainment could boom when this is over? Some pent-up demand in our household already. And people's attitudes might evolve toward, "We're going to enjoy ourselves a little more because you never know what might happen in the future."

19

8

107

Making money in financial markets has been too easy for too many since April 2020.

2022 could get interesting.

Time to (re-)read George Soros, Ed Chancellor, Barton Biggs, Jim Grant, Peter Bernstein, et al.

And, of course, Buffett's letters.

7

9

109

Crypto is a decentralized ponzi fueled by the god complex of b-list tech elites.

16

6

105

Contrarian investing is much harder in practice than it seems in theory.

Example:

"The most compelling bargains are in countries going through crisis. Invest when everyone else is running away."

Easy to agree with this statement.

Now for the hard part:

"Turkey."

Told ya. 🤷♂️

19

8

103

Did not think we'd see $TWTR below $40. Down more than 50% from the high (down more in EV terms). Meanwhile, the company continues to execute on monetization (as far as I can tell). The price seems to be narrating the story here, so we'll just have to let the results to come in.

21

8

105

Worried about Charlie's blood sugar. He keeps digging into the See's box in front of him. 😂

13

2

103

When internet stocks were flying high, nobody wanted to listen to investors who brought up valuation to warn of overheating. For me, it was tough to watch exceptional value investors get overlooked by allocators simply because the former were not fishing in the "compounder" pool.

8

7

98

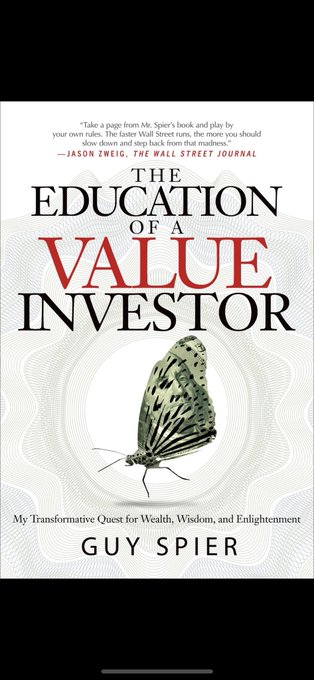

You won't find a book packed with more wisdom per page than this one. If you want to learn about investing or living an exceptional life, The Education of a Value Investor is a must read.

So far one of the best books on investing, money and life.

At par with

@WilliamGreen72

RWH and

@morganhousel

POM

Thanks

@GSpier

🙏🏼

8

21

125

4

10

99

I'm clueless on this topic, but I'll opine on it anyway. Just in case. 🤔

22

3

99

A real-time example of why The Carlyle Group is one of the most successful PE firms:

In 2010, Carlyle invested $550 million for 82.5% of money-losing Bank of Butterfield.

(This thread is for education purposes only. Not investment advice. Always do your own work.)

1/

4

7

97

How much higher was $ARKK when Cathie Wood told retail investors on CNBC that she expected a 40% IRR going forward?

16

2

93

If you were bearish on $CVNA, $NFLX, $SPOT or any other high-flyer, and you want to stay bearish, more power to you.

If you were bullish at the highs and are bearish now,

GET THE HELL OUTTA HERE !!!

13

1

94

Jim Simons' five guiding principles:

1) Don't run with the pack.

2) Partner with wonderful people.

3) Be guided by beauty.

4) Don't give up.

5) Hope for good luck.

1

14

90

Jim Chanos said back in the day he was short Blockbuster because anything "bits and bytes" would get disrupted. Folks, banking and insurance (for the most part) are "bits and bytes." The

@stripe

Treasury announcement is another milestone on the relentless path of disruption.

10

9

94

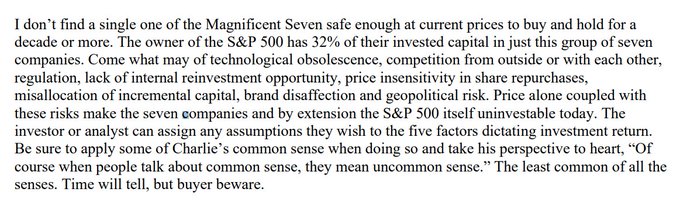

Always a must read!

@ChrisBloomstran

's annual letter -- loved this paragraph on the Mag 7.

Happy sharing the Semper 2023 Annual Letter. Writing it every year gets me outside the box. Love the process and always thrilled to be done! We released the PDF last night. Somehow page 41 was out of order. Perhaps Adobe's hint that 40 pages is enough...

29

50

371

10

12

95

Investing is a field in which no one really knows, so reflecting regularly on the extent of one's ignorance is a source of edge.

6

12

92

Anyone have thoughts on stock-based compensation at $SNOW?

Their non-GAAP adjusted FCF margin of 25% looks impressive, until you realize it would actually be *negative* if they stopped treating stock-based compensation as if it did not exist.

30

13

92

If you own $RACE instead of $PAH3.DE, take your eyes off the rear-view mirror.

19

5

94

Lo and behold the macro picture improved, and Tatneft went on a multi-year run from $1 to $120 per share.

I sold out at $2.

(The patience thing would become a recurring theme. Working on it!)

3/

5

1

92

ChatGPT and AI are going to obsolete a slew of companies previously considered well-positioned competitively. The real surprise will be the speed of obsolescence. Investors will have to redefine what it means to be "wide moat". Real assets may fit the bill better than tech firms.

13

11

90

The best ideas are usually the ones most people find unappealing, even if the investment thesis is articulated well. This is why you may have found it frustrating to share your best ideas, even if -- or maybe *especially* if -- those ideas went on to be big winners.

10

6

89

Live by the sword, die by the sword.

If you make your fortune with leverage, it would be superhuman to lay off leverage.

It's just not how the brain works.

He did not think, "$10 billion is enough."

He thought, "I can make $100 billion."

4

1

81

All the technology in the world does not change human nature one iota.

1

6

80

Looking for reading materials to understand the semiconductor industry and the players a bit better. If anyone can point me to any good resources, that would be much appreciated.

13

6

81

Some investors are now finding out that the valuation section in a writeup is not a throwaway.

2

10

79

The great thing about (long-term) investing is that you don't need the approval of others, and you don't need to play politics.

2

4

82

Investors still underestimate how many business models will get disrupted, if not obsoleted, by AI. Any business that sells some version of 1s and 0s is going to be fodder for AI.

15

6

81

Priceless

@BeckyQuick

eyeroll.

Becky, it's the crypto cesspool. That's how they roll. The opposite of what you're used to with Buffett.

3

8

81

Totally unpredictable and shocking.

A new study shows that 95% of NFTs' values have dropped to $0

"More than 23M people’s investments are now worthless"

(via

@dappGambl

)

1K

3K

42K

8

6

80

When everyone says buy the dip, it's not time to buy the dip.

6

6

79

The real answer might be that we have inflation *and* deflation. Deflation in all things bits, inflation in all things atoms. Bottom line: Unless you live in the world of bits, you better figure out how you'll pay for the things you desire in the physical world. Or, desire less.

5

8

80

Of course Adyen $ADEYE is not worth 38% less today than it was yesterday.

The problem is it was overvalued yesterday, and it might still be overvalued.

Those are (some of) the perils of paying up for growth.

2

7

81

Amazing that you can listen to so many podcasts by hypersuccessful people who don't need the money yet are sharing their wisdom with the world.

Also amazing: that those hypersuccessful people are so eager to make an extra buck that they attach their wisdom to minutes-long ads.

5

1

78

A Tobin's Q way of thinking for SaaS businesses?

"Twilio's enterprise value approximates the net present value of the cost of all the engineer-hours it would take to rebuild the relevant subset of their features in-house for every single user." --

@ByrneHobart

(h/t

@LibertyRPF

)

6

6

78

Plenty of overlap, but value investors at their core are financial analysts (think Bain Capital) while growth investors are first and foremost business analysts (think Bain & Company). Both approaches can work well. Know where you are most comfortable and lean into that skillset.

5

7

77

The older I get, the more I love these kinds of stories.

Also inspiring: Julian Robertson didn’t start Tiger Management until he was 48.

4

3

92

5

6

74

Grateful for their wisdom and ideas over the past year:

@ElliotTurn

@pcordway

@ChrisBloomstran

@PenderDave

@ShaiDardashti

@BillBrewsterTBB

@danielgladis

@Logos_LP

@LCTempleton

@GSpier

@GreenhavenRoad

@BobRobotti

@ClarkSquareCap

@david_katunaric

@Tyler_G_Howell

@EzraCrangle

7

11

77

Please enjoy my conversation with

@_inpractise

.

Will Barnes and Will Oliver are building an immensely valuable service for investors to learn about high-quality companies, with a focus on European and US midcaps.

Thank you,

@RishiGosalia

, for the intro.

2

10

74

Looking at Farfetch $FTCH. Levered, losing money, with finance costs of ~$35mn in Q2. Dicey proposition, but you think, okay, mgmt sees positive free cash flow in 2023. Then you realize they define FCF as basically an adjusted EBIT number, i.e., *before* interest expense. Ouch.

13

3

74

I love Constellation Software as much as the next guy, but at some point the rear view mirror no longer reflects what lies ahead. At CAD 3,750 per share, the risk-reward does not look favorable to me. (Add to this my thesis on AI putting long-term pressure on software companies!)

12

3

75

This market feels crazy, even foreign, to me as a value investor. But if you love investing, you love this market, too. When Mr Market acts this manic, it's a great time to look for opportunities, long and short. You just need to size things right and have the right time horizon.

7

8

73

$RIG: "...expect demand for the increasingly scarce high-capability drilling rigs Transocean owns and operates to remain strong for the foreseeable future, resulting in higher utilization and dayrates."

Time to pay attention.

1

5

75

I meet a lot of creators who invest in tech stocks and don't really understand why I focus on value, such as buying companies at a low multiple of sales.

1/

5

13

74

Some humans are fraudsters, most others are simply greedy. The latter suspend disbelief in pursuit of riches, playing into the fraudsters' hands.

In crypto, fraud and greed combine to create a massive decentralized ponzi scheme.

Witness Bitfinex, Tether

9

5

68

The emperor quite literally has no clothes.

11

4

72

Remember when Coinbase was going to be the next Goldman Sachs? 🤔

Lesson:

Don't try to be the next Goldman Sachs, and *especially* don't try to be the next Warren Buffett. 😂

9

3

72

Got some responses to the effect of "you don't understand China", which is true, but it reminded me of an investment I made in 1998.

I had bought a Russian oil company, Tatneft, at $1 per share, a $100 million market cap while ranked in the top ten worldwide in reserves.

1/

11

2

72

Taste of freedom after two years: mask requirement removed almost entirely in Switzerland. Feels good!

3

1

70