Bank Policy Institute

@bankpolicy

Followers

10,966

Following

1,431

Media

430

Statuses

3,366

The Bank Policy Institute (BPI) is a nonpartisan research and advocacy group representing the nation’s leading banks.

Washington, DC

Joined December 2009

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Rafah

• 1219849 Tweets

GW最終日

• 517721 Tweets

NUNEW 3RDMV IS OUT

• 447304 Tweets

井上尚弥

• 272395 Tweets

Inoue

• 160309 Tweets

シェリン

• 118934 Tweets

陸奥一蓮

• 96028 Tweets

ボクシング

• 69355 Tweets

大千秋楽

• 57117 Tweets

#キュウゴー

• 50598 Tweets

サプライズ

• 48447 Tweets

BINGLING SACRIFICES FOR LOVE

• 39812 Tweets

モンスター

• 38180 Tweets

Bruno Mars

• 34617 Tweets

ジェシー

• 27818 Tweets

GW終了

• 26655 Tweets

井上選手

• 25746 Tweets

逆転3ラン

• 24439 Tweets

筒香のホームラン

• 21369 Tweets

#GWを写真4枚で振り返る

• 17338 Tweets

20 YEARS OF MINJI

• 15570 Tweets

Białoruś

• 15207 Tweets

MIOTO NO VENUS PODCAST

• 15002 Tweets

筒香選手

• 13218 Tweets

Bernard Pivot

• 12899 Tweets

AESPA SUPERBEING TEASER 1

• 12732 Tweets

Pinned Tweet

The Consumer Financial Protection Bureau finalized a regulation today that will increase costs for responsible consumers who pay their credit card bill on time.

There are five major problems with the rule. 📺⬇️

#FactsOnFees

1

3

7

A "bank" funded by uninsured deposits, reliant on assets that can be subject to rapid and substantial capital losses in times of stress. What could go wrong?

@krakenfx

24

72

348

In 2009, President Obama signed the bipartisan CARD Act into law. Many in Washington celebrated this major accomplishment.

Accusations that banks charge "illegal" fees, or are not committed to providing robust disclosures, are irresponsible and just wrong. Get the

#FactsonFees

.

87

42

289

Day one of FinTech Ideas Festival is wrapping up with Dan Schulman, Brad Garlinghouse, and Deirdre Bosa talking payments.

#FIF2019

12

37

110

We analyzed the reported cases of allegedly fraudulent

#PPP

transactions based on DoJ news releases & criminal complaint affidavits cross-referenced w/ SBA loan-level data.

In a majority of cases, the allegedly fraudulent loan was obtained from a FinTech.

7

54

96

The ON RRP facility, once described as a temporary tool, sits at a massive $2.2 trillion – bigger than the GDP of South Korea.

That's a big problem. But, perhaps there's a straightforward solution. We explain:

13

32

94

The Tsar Bell, the largest bell in the world, weighs approx. 216-tons. That's ~3x heavier than Space Shuttle Endeavor.

Yet the Tsar Bell pales in comparison to the largest bell in the history of the financial world, which will pose extraordinary challenges to the incoming FSOC.

14

23

92

What is a SAR?

How many of these SARs are really illegal activity versus false positives?

Why would a bank identify a suspicious transaction for law enforcement and continue to bank that client?

We answer your questions:

#FinCENFiles

14

35

69

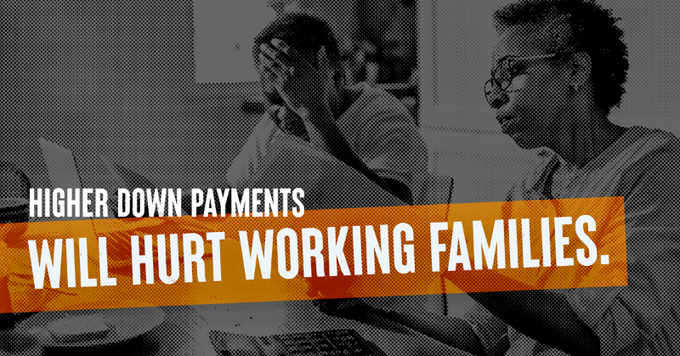

The federal government's new capital rules would make loans more expensive and less accessible, hurting everyday Americans when our economy is still recovering from a pandemic and grappling with rising interest rates.

Take action to

#StopBaselEndgame

:

6

15

56

BPI commented today on the Department of Justice’s request for public input on bank merger analysis.

Please see a copy of our comments and a full statement here:

1/6

13

9

52

RELEASE: Basel Proposal Violates the Law

The banking agencies’ Basel proposal violates both the substantive and procedural requirements of the law that governs all federal agency rulemaking. The only solution is for the agencies to re-propose the rule.

6

11

47

The third (and final) installment of our Basel Finalization series explores potential modifications to enhance the sensitivity to risk & reduce the procyclical impact of capital requirements, so as to prevent worsening of economic downturns.

Read it here—

4

3

41

The Fundamental Review of the Trading Book, the part of the Basel proposal aimed at market risk, would raise market risk capital requirements significantly.

Our latest note examines how an overly severe FRTB could increase risks, and offers a fix:

4

8

41

Happening Now: Fed Vice Chair Lael Brainard joins

#tchbpi2022

to discuss inflation.

Read the Vice Chair’s prepared remarks here:

8

13

40

The new proposal undermines Congress and effectively repeals rules that tailored regulations to a bank’s size.

Learn more about these implications at

4

8

42

Avanti Financial, a cryptocurrency firm, recently got Wyoming’s approval to take deposits like a bank, but its boasts of being “100 percent backed by reserves” belie its real risks to customer deposits.

5

8

38

Notice anything missing from this month’s accountant report from Circle? A breakdown of the types of assets backing

@circlepay

’s “stable” coin (USDC) is conveniently excluded.

So much for greater transparency…

4

7

40

The

@CFPB

has repeatedly denounced legitimate bank fees, like credit card late fees, as “illegal” and as “junk fees.”

This rhetoric mischaracterizes late fees as inherently bad, ignores existing consumer protections and confuses rhetoric with reality. Get the

#FactsonFees

. ⬇️

38

7

33

1/5 Today, the

@bankofengland

is again serving as “market maker of last resort,” supplanting private sector intermediation and trading bonds with taxpayer money. The BofE is acting in crisis but the Fed has taken the same action in normal times (2019) as well as crisis (2020).

2

8

34

What Kevin Costner Can Teach Us About Bank Profits and Regulation -- check out our latest blog

3

10

26

What went wrong at Silicon Valley Bank?

An early explanation and the potential implications:

3

4

25

The

@CFPB

has proposed to cap the safe harbor for credit card late fees at $8, which will have unintended harmful consequences for banks’ ability to serve customers across the credit risk spectrum.

Read our latest here:

37

6

25

Allowing tech companies to enjoy the privileges of being a bank, without requiring them to meet the duties and obligations of being a bank, threatens the safety and strength of America’s banking system.

Learn more at .

#KeepBankingSafe

2

6

26

3/5 Most notably, the leverage ratio requires banks to hold the same capital against a Treasury security as a subprime credit card loan; the Fed has vowed reform but failed to act. Such reform is necessary but not sufficient; it could be adopted immediately.

1

3

26

About that deregulatory wave...

2

2

25

Chairman McHenry is right. Major policy decisions should be driven by economic analysis. Not politics.

@PatrickMcHenry

@FinancialCmte

3

3

23

Denver US Attorney Dwight Schrute announced that his office, through analysis of SAR data, has discovered that marijuana is being sold in Colorado. Schrute credited the BSA/AML monitoring regime, and said he hoped the banks would “keep those SARs coming.”

1

5

23

RELEASE: BPI Releases Report Profiling Innovative Bank Practices to Close Racial Equity Gaps, Bolster Diversity

To learn more, visit

9

5

21

.

@ICIJorg

and

@BuzzFeedNews

recently released

#FinCENFiles

based on thousands of illegally leaked SARs. The report lacks a full understanding of the AML framework and has led to considerable confusion about the AML regime in the US.

We correct the record—

10

12

18

5/5 Pottery Barn rules say “you broke it, you bought it,” but in this case, a failure by regulators to repair broken regulations could mean taxpayers buying securities on a regular basis. Ironically, because the purpose of capital rules is to avoid exactly that.

1

1

18

“We want to provide innovation that is legendary to our customers.” - TD Bank Group President and CEO Bharat Masrani at our 2019 FinTech Ideas Festival joined by Ryan McInerney from Visa, Noah Breslow from OnDeck and Deirdre Bosa from CNBC.

@TDBank_US

@FinTechIdeas

#FIF2019

1

13

19

After promising a holistic review for many months and using it as a justification for the Basel Endgame proposal, Fed V.C. for Supervision Barr states that such a document does not exist. It is a concept...not a document.

7

5

19

Why is that?

It’s because trading one token for another token or for a nonbank stablecoin is unconnected to the real economy. So, concerns about financial stability risks of crypto appear to have been overstated. 3/7

For the layman, what’s happening in crypto is simple: the companies owe each other a bunch of fake money. It’s awesome when the number goes up. Not so much when it goes down.

25

97

1K

2

5

17

RELEASE - Joint BPI, ABA Comment Letter: Basel Proposal’s Costs to U.S. Economy Outweigh Any Benefits

1/6

3

4

18

Payments fraud received significant attention at the recent congressional hearings with the 7 largest retail banks. The focus was on Zelle because the witnesses were bank CEOs but, for any real discussion of online fraud, the focus belongs elsewhere. 1/

4

4

17

Did you know: the operational risk charge in the Basel proposal drives 90% of the increase in capital requirements.

The proposal dramatically overstates banks’ op. risk & layers a broad, unnecessary tax on every bank activity.

#StopBaselEndgame

2

3

18

4/5 More broadly, holding of riskless or low risk assets is penalized by other rules — e.g.,the GSIB surcharge and the Fed’s stress tests. They require reform, but as part of its implementation of the Basel rules, the Fed is considering making those rules even more punitive.

1

1

17

.

@federalreserve

Vice Chair for Supervision Michael Barr said the Basel capital proposal would have a minimal impact on the cost of lending: only 3 basis points, or 0.03 percent. However, the banking agencies’ analysis inexplicably leaves out $1 trillion...🧵

3

4

16

We’ve just witnessed the implosion of the world’s second largest crypto exchange, owned by the most prominent figure in crypto. 1/7

3

6

16

Over 2 million bank employees work every day to help create jobs, grow small businesses and drive economic growth. Learn more about the economic contributions BPI members provide to power your every day:

5

6

15

Given that 35,000 comments were received, and assuming an 8-hour federal workday, this means that the OCC reviewed ~398 comments per hour before finalizing its rule. For an analysis of similar probabilities, see:

@bankpolicy

@baerheel

@IntraFi

The question is whether the OCC rushed the rule. Given that the rule was finalized 10 days after the comment deadline closed, it will be easy to argue it did so.

Opens the OCC up to lawsuit on violation of the Administrative Procedure Act.

2

1

2

1

7

16

.

@federalreserve

Vice Chair for Supervision Michael Barr downplayed concerns in a speech this week about the Basel capital proposal’s effects on lending.

But, the cost analysis relied on has a trillion-dollar omission:

2

1

16

The European proposal maximizes the use of bank models, maximizes the use of external credit ratings, maximizes the pool of unrated corporates that will qualify for a 65% risk weight and provides favorable capital treatment for small business lending.

What is the US going to do?

11

4

11

Diamonds, yachts and private jets. Kleptocrats have learned that "the best way to hide and move stolen wealth is to set up a raft of anonymous shell companies..." It's time for that practice to end.

#EndAnonymousShellCompanies

0

10

14

Part two of our three-part series on Basel Finalization examines the most likely structure and scope of U.S. implementation.

The choices made by U.S. regulators could result in significant differences in overall bank capital requirements.

Learn more:

0

2

12

We'll be on the Hill this afternoon with the

@FACTCoalition

hosting a panel discussion on why legislation is needed to end anonymous shell companies. The panel features experts from

@AEI

@fdd

@GLFOP

@Global_Witness

@StreetGrace

and

@TI_Defence

. Register—

0

4

15

Treating payment tech companies like full-fledged banks can endanger customer deposits.

The business model of Payward Inc’s Kraken Financial, part of a US-based cryptocurrency exchange that WY bank authorities just approved for a special-purpose bank charter, shows just that.

56

6

13

Reserve balances could be expected to reach $5.85 trillion in mid-2022, more than twice the level they reached after QE1, 2, and 3.

High reserve balances have 2 important consequences:

0

5

14

A diverse group of stakeholders, including law enforcement, national security experts, human rights groups, and financial services organizations, support an end to anonymous shell companies. Find out why:

0

7

14

A bipartisan group of more than 100 national security and foreign policy experts, including former Russian Ambassador Michael McFaul and former Acting Secretary of the Treasury Adam Szubin, are urging Congress to end anonymous shell companies. .

0

11

13

Capitol Account recently hosted an event sponsored by BPI to examine the Basel Endgame proposal. In his remarks, Eugene Scalia highlighted the deficiencies of the proposal and the need for a more rigorous analysis.

Watch the full event: .

#StopBaselEndgame

0

3

13

2/5 Since 2019, the Fed and others have recognized that a growth in fixed-income issuance, including Treasuries, has been accompanied by a shrinking of private sector capital devoted to making markets in those securities, driven largely by overly stringent regulation.

1

2

14

The “move fast and break things” mentality of Silicon Valley should not be given a free pass when it comes to the safety of the U.S. banking system and the financial health of Americans.

Learn more at .

#KeepBankingSafe

4

1

12

🎉👏🎊

Featured in POLITICO Playbook PM today: WEEKEND WEDDING -- Alex Schriver, EVP at Targeted Victory and a Bradley Byrne alum, and Tracey D’Antuono, VP at the Bank Policy Institute, got married over the weekend at a small ceremony with family and friends in Charleston, S.C.

0

1

13

Today, legal legend Carl Howard of

@Citi

attended his final BPI (and Clearing House) Bank Regulatory meeting. He retires with the universal respect and admiration of his peers, who will dearly miss his wit and wisdom.

1

2

13

The Fed recently issued proposed guidelines intended to govern how Reserve Banks would review and assess account applications by institutions with novel charters.

Serious policy questions remain unaddressed, which we examine in our latest publication:

1

6

11

Analysis of Silicon Valley Bank’s demise is rife with “what if” speculation. Some have questioned whether SVB would’ve met the liquidity coverage ratio, a req. from which it was exempt under the S. 2155 tailoring law. The answer is “yes,” by a wide margin.

5

4

11

RELEASE: Banks, Credit Unions and Consumer Groups Call for Passage of Bipartisan Solution to Close ILC Loophole

Read:

@FSCDems

@FinancialCmte

@RepMaxineWaters

@PatrickMcHenry

@uspirg

@NCLC4consumers

0

3

12

The HFSC Financial Institutions and Monetary Policy Subcommittee hosted a hearing on Jan. 31 on the Basel III Endgame proposal, which highlighted the proposal's many deficiencies.

Here are the 7 key takeaways. 📺👇

#StopBaselEndgame

2

1

12

RELEASE—Largest banks have served smallest businesses through

#PaycheckProtectionProgram

:

▶️ $115k avg loan size

▶️ 64% of loans < $50k

▶️ 51% of all loans went to businesses with < 5 employees

▶️ 75% to < 10 employees

▶️ 98% to < 100 employees

5

5

9

With 97% of public comments opposing or seriously concerned about the Basel Endgame proposal, it’s time for a new playbook.

Say “no” to Basel Endgame’s costly new capital regulations. Learn more at .

#StopBaselEndgame

3

3

12

RELEASE:

@CFPB

Finalizes Rule to Increase Costs for Responsible Consumers that Pay Bills on Time

5

2

12

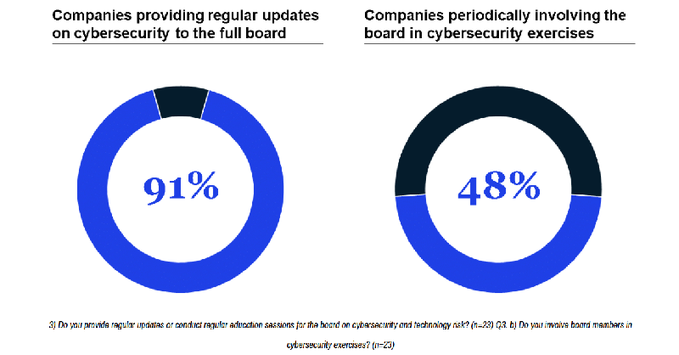

Did you know:

- 95% of board committees discuss cybersecurity and technology risks 4x or more per year

- 91% of companies provide regular cybersecurity updates to the full board

A new survey finds that

#cybersecurity

is a growing priority in financial services boardrooms.

0

3

10

Loans are 3.3% higher than 1 year ago despite reduced loan demand in a recession.

Cash is up 83% b/c banks must hold the Fed’s vastly expanded reserve balances.

Treasuries have grown 41%.

W/ Fed buying $80b/month of Treasuries, good thing banks are there to help as well. 1/3

The biggest U.S. banks reduced the portion of their collective balance sheets they’re dedicating to loans to a new low, extending a trend that’s seen the largest lenders put less and less of their firepower behind everyday borrowers (via

@nasiripour

)

7

28

44

2

5

11

ICYMI:

@GoldmanSachs

surveyed participants of its “10,000 Small Businesses” program, finding that 84% of respondents are concerned that the Basel Endgame Proposal will negatively affect their ability to access capital.

Learn more:

@GS10KSmallBiz

0

3

10

A bank treasurer was told when he took the job borrowing from the discount window would lead to 2 calls:

1. To the CEO from the NY Fed asking why the bank borrowed;

2. To him from HR instructing him to clear out his desk.

What's the source of this stigma?

1

3

10

The Clearing House Association and the Financial Services Roundtable have merged to become the Bank Policy Institute (BPI). Check out our new website to learn more:

1

11

11

A year ago today, BPI announced the merger between the Clearing House Association and the Financial Services Roundtable. It's been an exceptional year for our organization, and we're proud to share some of our many accomplishments over the last year:

The Clearing House Association and the Financial Services Roundtable have merged to become the Bank Policy Institute (BPI). Check out our new website to learn more:

1

11

11

2

1

11

The basic business model of banking is inherently unstable – banks take deposits and use them to make loans. Deposit insurance and liquidity regulations ensure that such a business model remains safe and banks don’t suffer runs on their deposits. 1/4

3

1

11

RELEASE w/

@ABABankers

@ConsumerBankers

@fsforum

and

@TCHtweets

:

Congress should exempt stimulus payments from court-ordered garnishments -

0

6

10

The Basel Endgame proposal would impose excessive capital requirements on consumer loans, making credit more expensive and less available for the most vulnerable American customers.

See our latest on what Basel means for retail lending:

#StopBaselEndgame

2

2

10

The OCC's "Fair Access" proposal lacks logic and legal basis, ignores basic facts about how banking works in the U.S. and undermines safety and soundness.

We published an issue summary that explains why:

0

4

11

At BPI, we shake hands with the regulators at the end of every meeting.

Wow. Most Duke players left the court without shaking hands with UNC players. Sad!

2K

3K

41K

1

1

11

Welcome newest member to the BPI family —Willow Reilly!

0

1

11

The lesson: don’t bail out a failing industry by giving it access to Fed accounts and providing it a new business model, thereby linking it to the regulated financial system and heightening the risk that the next cryptoverse crisis actually could harm financial stability. 6/7

2

2

10

BPI and a coalition of associations representing banks & credit unions submitted a letter to the Senate Committee on Armed Services Chairman

@JimInhofe

and Ranking Member

@SenJackReed

calling for swift passage of legislation to

#EndAnonymousShellCompanies

.

0

7

10

Regulators should

#StopBaselEndgame

and re-propose. The proposal is

⚠️ Bad for consumers.

⚠️ Bad for small businesses.

⚠️ Bad for the economy.

Learn more at .

@federalreserve

@FDICgov

@USOCC

@FSCDems

@FinancialCmte

4

1

9

Ajay Banga from MasterCard and Tim Sloan from Wells Fargo are live on stage with CNBC’s Andrew Ross Sorkin at the FinTech Ideas Festival

#FIF2019

0

3

9

We recently hosted the 2019 FinTech Ideas Festival in San Francisco in partnership with

@CNBC

, the event's exclusive broadcast partner. Check out some of the highlights from the conference, including photos and video of the main stage:

0

3

8

Use of the Fed’s Overnight Reserve Repurchase Agreement Facility just reached a record high of $485 billion. BPI’s blog on the facility from a month ago predicted its rapid growth and provides a primer:

0

3

9

Fed V.C. Barr dramatically understates the impact of the Basel Endgame proposal in his opening remarks that the proposal will only apply to less than 40 banks. Those banks make over 2/3 of all loans in the U.S. and provide over $1.76 trillion in loans to households... 1/2

2

1

9

Congrats to our Moroccan colleague, and condolences to our Spanish colleague. (You can guess who is who.)

0

2

9

BPI CEO Greg Baer issued the following statement in response to a vote by the House of Representatives and Senate to override the President’s veto of the NDAA for FY 2021, which includes language to reform the AML framework and

#EndAnonymousShellCompanies

.

0

9

9

BPI research analyst Jose Maria Tapia took home the gold in the lightweight division this weekend at the Professional Brazilian Jiu Jitsu Federation Virginia Winter Open. Congratulations, Jose!

0

0

9

BPI joined

@ABABankers

,

@ConsumerBankers

,

@fsforum

,

@SIFMA

,

@IIBnews

,

@BAFT_Global

,

@IIF

, Mid-Size Bank Coalition of America to submit a letter to the House Financial Services Committee in support of efforts to modernize the AML / CFT regulatory system:

0

0

9

SVB's failure has prompted calls for banks to reserve even more space on their balance sheets for high-quality liquid assets, leaving less room for lending.

This change could reduce the economic costs of liquidity reqs. while preserving their benefits.

1

0

9

.

@BrookingsInst

hosts "Fixing America’s payment system: The role of banks and fintech" ft.

@BrianBrooksOCC

keynote and panel moderated by

@Aarondklein

incl.

- BPI CEO Greg Baer

-

@ChrisBrummerDr

- Michael Calhoun,

@CRLONLINE

-Margaret Liu,

@CSBSNews

0

5

9

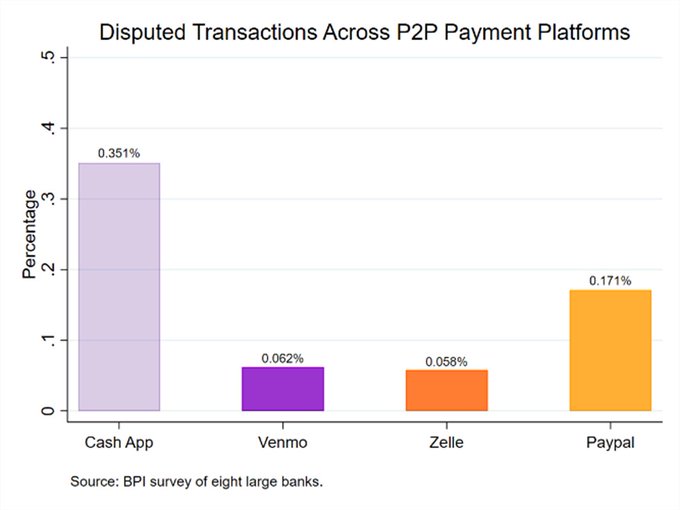

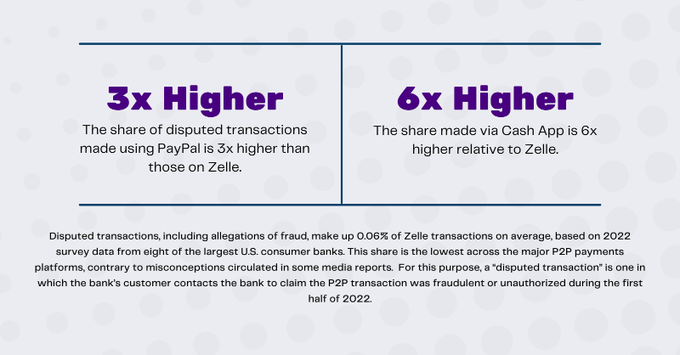

Zelle is the safest way for consumers to move their money. The share of disputed transactions made using PayPal is 3x higher than those on Zelle. The share made via Cash App is 6x higher relative to Zelle.

Learn more:

1

5

9

Bill Nelson, our chief economist, will be on

@SquawkCNBC

tomorrow at 7:30 am to talk about the Fed’s path in 2019 with

@steveliesman

1

3

9

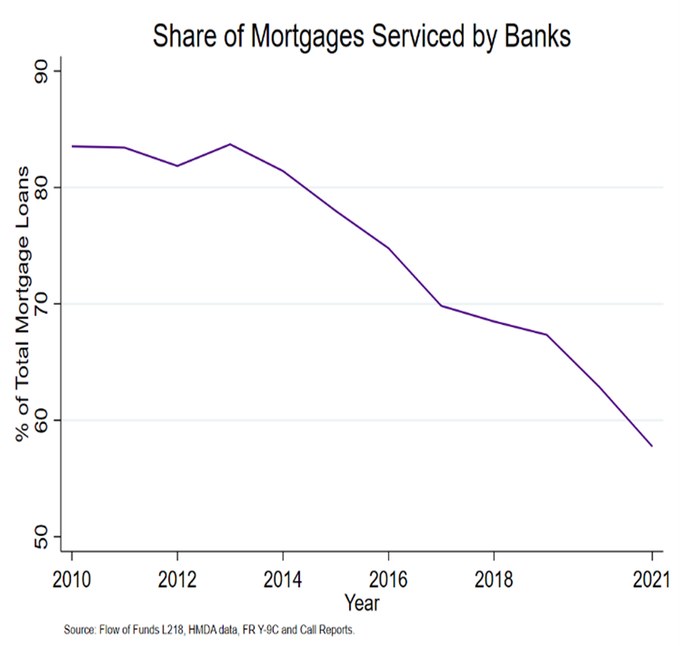

Mortgage lending has increasingly been driven out of the regulated banking sector, partly because of capital regulations. 1/

1

1

9

Anonymous shell companies pose a serious challenge to law enforcement and threaten national security. If you support closing the legal loopholes that enable anonymous shell companies, call congress today and ask them to make HR2513, The Corporate Transparency Act, a priority.

0

10

9

We're excited to be in San Francisco this week to host the 2019 FinTech Ideas Festival with our exclusive broadcast partner,

@CNBC

! Join the conversation using

#FIF2019

and watch coverage from the event by

@dee_bosa

,

@levynews

,

@CNBCJosh

and

@andrewrsorkin

Less than 24 hours to go and production is well underway to turn this incredible space into a place for innovation.

#FIF2019

0

0

4

0

6

8

RELEASE: The data shows that Zelle is the safest way for consumers to move their money.

Learn more here:

0

2

9

Big Tech wants to know: how much money is in your bank account?

Learn more at .

#KeepBankingSafe

1

3

6

🚨 RELEASE: Legislation to Reform Anti-Money Laundering Framework and End Anonymous Shell Companies Nears Finish Line

House of Representatives Votes to Include Anti-Money Laundering Amendment in 2021 National Defense Authorization Act

Read >>

0

1

8

Wonder if we’ll look back in a few years and realize this was a bigger deal than Libra? Or will Facebook have a Utah ILC by then?

0

3

6

BPI Chief Economist Bill Nelson joined

@GeorgeSelgin

and

@DavidBeckworth

this evening at

@AEI

to discuss Selgin's new book "Floored!: How a Misguided Fed Experiment Deepened and Prolonged the Great Recession." Click here to read Bill's remarks

0

2

8

BPI and a coalition of trades including

@ABABankers

,

@ConsumerBankers

@CUNA

,

@ICBA

,

@NAFCU

and

@TCHtweets

urge the OCC to undertake an open and transparent process before considering a new narrow-purpose payments charter:

0

2

8

Joint Statement: Banking and Credit Union Groups Issue Statement on the Availability of Economic Impact Payments to Consumers:

1

0

8

BPI recently released a set of policy recommendations to strengthen the resilience of the banking system while allowing banks to continue funding economic growth.

Learn more about the immediate and longer-term changes that regulators should take:

1

2

7