Matt H 🇺🇦

@mdharrisnyc

Followers

3,249

Following

535

Media

298

Statuses

4,360

Fintech guy to exec coach for 10+ VC backed cos. Investor 10+ fintech cos ( @trueaccord + @usesmileID + @trykarat etc) + founded @bloomcredit and @claimsetter

New York, USA

Joined November 2013

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Madrid

• 1659365 Tweets

Champions

• 711131 Tweets

Bayern

• 660763 Tweets

Joselu

• 348556 Tweets

مدريد

• 224155 Tweets

Neuer

• 172326 Tweets

Vini

• 154238 Tweets

Tuchel

• 141522 Tweets

Harry Kane

• 82551 Tweets

Luka

• 81657 Tweets

FURIA ES GRAN HERMANO

• 79017 Tweets

De Ligt

• 73404 Tweets

Uruguai

• 72604 Tweets

Steve Albini

• 65650 Tweets

Kimmich

• 55304 Tweets

Joker

• 51592 Tweets

共同親権

• 50007 Tweets

#虎に翼

• 41848 Tweets

Shai

• 38382 Tweets

Jokic

• 38124 Tweets

نوير

• 37042 Tweets

Venus

• 27594 Tweets

Shaq

• 22999 Tweets

#SalvemOCavaloDeCanoas

• 22248 Tweets

DPVAT

• 21914 Tweets

アイスクリームの日

• 20083 Tweets

Soto

• 19404 Tweets

twenty one pilots

• 17828 Tweets

Talleres

• 12579 Tweets

もちづきさん

• 10225 Tweets

Pinned Tweet

Getting to spend so much time working with

@tedr

in his final days was one of the great honors of my lifetime. Grateful for every moment.

2

2

35

Biggest Fintech lesson I’ve learned in the last 5 years.

Incumbent financial institutions are slow, not stupid. If your main advantage is acquiring consumers banks don’t want, there’s probably a good reason they didn’t want them.

Your biz model should account for that reason.

46

364

2K

Feel like joining a startup is like being told you’re going to a new place where the streets are paved with gold.

Except when you get there you find out the streets aren’t paved and in fact you’re the one paving them

51

131

1K

An alarmingly large percentage of fintech pitches I get are given to me by CEOs with very little to no financial services background who aren't totally aware they are blatantly violating a financial regulation with their product.

Always speak to lawyers before you speak to VCs

39

35

303

BNPL is going to eat the credit card market in ~10 years.

It’s a product that is easier to underwrite, that gives more people access to credit (and building credit responsibly) without the lender taking too much risk.

The trick will be verticalization of BNPL businesses

28

33

267

I don’t know who needs to see this but…

Percentage chance of getting into a fatal car accident (%.009)

Percentage chance of any vaccinated person being hospitalized from the delta variant (%.004)

Take this information and act accordingly.

10

23

243

Using “alternative data” to underwrite loans in the US has not yet worked at scale (defined as vintage yields of greater than 5% YoY for >3 years). If you believe this is “the future” or a major component of underwriting, you don’t understand how loans are actually underwritten.

28

20

191

Really excited to announce our Series A for

@bloomcredit

! We have plans to use the new funding to make new hires and build more of the infrastructure to enable inclusive consumer credit products

17

14

179

CEOs are up to 12x more likely to exhibit psychopathic traits (or just straight be psychopaths) vs general population.

Founders are also 3x more likely to abuse substances, 10x more likely bipolar and 2x more likely to wind up in the psych ward.

This job tears people apart.

35

16

158

Only on this bird site can you see people mansplain BNPL to the former chief risk officer of Klarna.

What a magical place :)

5

4

127

Friendly reminder to VCs investing in lending businesses

Growth ≠ business quality

The product is giving away money. You can discount the debt price and generate growth w/ a “data advantage.” But you’ve effectively created fab for lending.

Look for better indicators ;)

10

11

121

Had someone inform me today that a major card network is seeing a ~15% reduction in total usage because they are losing customers to BNPL.

It’s already happening. BNPL is eating credit.

BNPL is going to eat the credit card market in ~10 years.

It’s a product that is easier to underwrite, that gives more people access to credit (and building credit responsibly) without the lender taking too much risk.

The trick will be verticalization of BNPL businesses

28

33

267

21

14

117

Been considering if you could raise VC to buy a sports team.

If you buy a league 2 club in England and get them promoted 3x by investing in fitness technology/ analytics you’d likely see the investment go up 5-10x.

Feels like a VC investment to me. No?

48

7

113

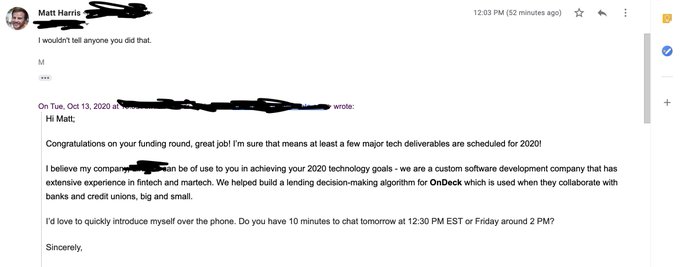

Idk if anyone knows this but the reason startup founders announce funding rounds is because we love all the emails from dev shops.

It’s actually the reason we built this biz. The joy of emails that start with “matt, I see you work in tech!”

I find the reminders healthy ya know

13

3

101

This is generally the shape of fintech infrastructure providers.

They take a fair deal of time to get going (because they are dealing with all the incumbents you don't want to)then once everything is in place they tend to take off.

Cc

@fintechtoday_

@julieverhage

@iankar_

6

5

97

Every Fintech founder should have a network of debt capital providers the way they do VCs.

15

5

92

Your Q1 OKRs are probably not helping your team win... but that doesn't have to be the case.

Here's a 3 things to think about as you start doing some Q1 planning... a thread 🧵 (sorry... I know I know)

6

15

79

There’s one company in Fintech I know that has about 3-4x the traction as it’s competitors, for nearly identical products, and yet 1/10th of the funding.

VCs… when you hear this disaggregated from the company names what’s your guess as to why?

40

3

72

Debit interchange exists as a means of helping banks cover fraud loses, not as an actual revenue generator.

If your only source of revenue is debit interchange then you are essentially saying your secret sauce for success is to be better at managing fraud risk

5

2

77

I wonder what that Dan price guy thinks about payments businesses?

Never heard him talk about that

7

1

72

Incredible how

@CommonBond

announced it was closing it’s doors this week and no one seemed to notice.

CommonBond was considered once was tapped to be a unicorn on every Fintech article.

Huge warning to neobanks - large customer base with bad economics are not valuable

14

7

73

This upcoming weekend will be my last in Colorado.

Moving back to the NYC area! Excited to hang with everyone out there again. Shoot me a note if you want to catch up in the next few weeks.

Colorado was a great experience. Will try to see everyone to say bye before I go <3

12

0

68

If you are freaking out about the delta variant, you need to listen to this.

TL;DR… are you vaccinated? Then don’t panic 🙀

Podcast I did on the delta variant and metrics on “Is it Normal Yet?” Thanks.

6

17

63

1

8

63

Even after ~a decades worth of *publicly available* data on the subject I get asked about this about once a week.

If there were alt data points with such incredible signal we’d have found them already.

The best alt data you’ll ever get is that which is native to your bizmodel

if I were a lending startup I would simply use alternative sources of data to achieve lower risk with borrowers who can’t qualify under conventional standards

37

6

214

11

3

66

If you are a VC that is investing in lending businesses... please be cognizant of how a company presents it's numbers to you.

Loan performance data should be presented on a vintage basis. If they give you aggregate, the data is likely fudged and you should run.

6

5

63

If you're trying to raise money for anything that's remotely lending related... I'm wayyyyy more interested to hear your GTM plans than I am your underwriting scheme

Underwriting gets easier when CTA is lower because it means you can more effectively compete for high LTV loans.

5

5

62

Gotta just celebrate and say I’m the happiest I’ve been in years.

Life is good 😊

7

0

59

Between being named Matt Harris and having a company called “Bloom Credit” I clearly chose the most competitive possible quadrant in the matrix

2

0

58

I have an opinion about $SQ buying Afterpay, but I’ll need to give it to you in installments.

3

0

54

My favorite emails have become those from headhunters trying to recruit me to be CEO of another company.

Isn't this like asking me to abandon my own child to parent another person's child? Which I'm sure anyone whose ever been a parent would be very excited for?

Very silly.

6

0

58

I’m just wondering when we’re gonna start judging credit companies on the quality of the loans they make… ya know?

7

3

52

Excited to announce a new chapter in

@bloomcredit

History! I'm stepping into a new role as Executive Chairman where I'll work with our new CEO (

@widhalm

) on bringing about a vision of making credit more accessible.

I'll still be FT. Pumped for bloom =)

3

4

52

I name dropped

@pitdesi

this week and it helped me land a super sweet apartment in Denver (where I am moving tomorrow 😎).

Are we at peak Fintech yet?

11

0

53

I've begun to think of the lack of public recognition of

@trueaccord

as one of the company's greatest assets.

Consensus fintech is not performing well. End of story. Everyone got marked up. No one became liquid from those markups.

The best fintech companies will not be sexy

6

1

52

Hey guys you may not know this but I don’t think alt data underwriting works

17

1

50

I don't tweet about Fintech anymore... it's because nothing new is actually happening.

Most pitches I get are recycled versions of companies I knew about 10 years ago.

Most new product launches are the same as 5 years ago.

I have no new opinions. We've done nothing new.

31

3

51

I’m curious what lessons VCs learned from Ondeck and LendingClub?

(I.e fundamentally not great businesses, but with presumably good venture returns)

Do these outcomes dictate our current market at all for Fintech?

16

2

48

If you are a fintech company that's thinking about improving the financial health of consumers, and you aren't looking into furnishment... now is probably the time to start =)

I guarantee that your competitors are if you are not.

3

8

48

@linasbeliunas

I think those things are important, but usually not core to a biz model.

I think the issue we're having as an industry is we've over funded a series of companies all built on the same poor business models.

Compliance likely isn't going to save these businesses.

5

2

45

I’d like to announce that bloom credit is rebranding to lambda school

1

0

44

The two ways lenders really are able to compete are acquisition and cost of capital.

It’s easy to fall in love with the idea that a better underwriter can find a deeper truth.

But the truth is you can only express financial wellness so many ways in data

8

4

47

Today is in fact my 29th birthday.

I was 22 when I founded bloom. It’s super crazy how time has flown.

Grateful to everyone that’s helped along the way. And even those of you who are total trolls ❤️🙏

happy birthday to my least favorite matt harris

@mdharrisnyc

on the bright side, now he’s finally old enough to be a good founder

1

1

14

11

0

48

Who do I know that could intro me to

@jack

?

I really feel that the acquisition of

@afterpay_au

could be huge for

@CashApp

customers to improve their credit standing and create a sustainable system of financial inclusion.

Would love to help if I can :)

1

8

46

Great post on how lending works =). Was happy to contribute to this in a very small way.

Credit is tons of disciplines wrapped into one outlet. As Frank and I discussed privately, it's hard to cover everything.

If you want to learn the nuts and bolts. This is it 👇

1/27: We’ve seen a few $10B+ lending companies emerge from the fintech ecosystem in the past few years. We’ve also seen a few fintech lenders meltdown in the public markets.

Are lending companies VC backable? Thoughts plus a framework to answer this question👇

20

108

626

0

6

44

🙃Quick moment to celebrate 🙃

Between the coaching work I do and investing I'm working with over 25 companies right now. Can't say it's not challenging, but def amazing.

I get asked by VCs if I'm going to found another company. The answer is probably not =)

I love what I do

4

1

45

If you aren’t paying attention to

@trueaccord

becoming a massive business you should be.

And if you’re still in the camp that you can’t build a technology driven and customer friendly collections based venture backable biz then idk what to tell you.

It’s clearly happening

9.9 million.

This is the number that matters to us most at TrueAccord.

Why?

It’s the number of customers who worked with us in 2021 to:

💸 Resolve debt on their own terms

💸 Improve their financial fitness

💸 Take charge of their future

1

19

33

4

9

44

If you really think about it… everyone in Fintech is either “Matt Harris” or “Not Matt Harris”

4

1

43

Line around the block for the Ukrainian restaurant in the east village.

Glory to Ukraine 🇺🇦

2

2

38

Almost everyone has intent to repay loans. Not everyone necessarily has ability to do so.

Underwriting is a means of predicting financial shock. Not necessarily calibrating to highest potential of financial performance.

Reframe your thinking this way and it makes more sense

2

2

42

Whose your favorite person in fintech who hasn’t taken the founder leap yet?

20

0

41

Who are the best founders turned investors?

Have founders asking me for this recently and I don't have a definitive list. Would love to connect with VCs who really get the founding journey.

A few that come to mind are

@pitdesi

/

@iamjakestream

/

@maiab

Any others?

22

4

40

Yet another bloom Fintech company 🙃

Welcome to YC W22, team

@BloomAppSD

!

Bloom offers students and young professionals in East Africa US Dollar banking. By saving money in USD, they won't be subject to the volatility of their home currencies.

9

20

83

5

2

38

Really excited to announce that

@bloomcredit

has raised our Series A! We'll be using the $$ to make new hires and continue to build out our API to connect with credit bureau infrastructure to enable consumer products that support financial health.

2

3

40

Going to be in NYC next week! Excited to catch up with everyone that's there.

Let me know if you wanna grab coffee / drinks to catch up or talk fintech stuff.

13

1

38

Lending innovation in the US is almost *never* a result of technological innovation.

Building positive selection usually requires operational innovation. Very few lenders have any real competitive advantage in data science.

Hard to get different outputs from similar inputs.

5

3

40

There is almost always a regulatory or compliance explanation for why the credit system functions the way it does.

4

1

37

Feel like being an entrepreneur is similar to being a musician in that each company or project is an album. It's an expression of that period of someone's life. Rather than a catch all for who they are forever.

My second album isn't going to be anything like my first.

5

2

38

Despite healthy cynicism, I think Credit is venture backable.

But, I think the model that usually applies to software (build moats via IP) doesn't apply to lending.

You should really think of them more in the framework of an Ecommerce investment vs a software company.

3

1

39

Just got to nyc and having huge “what have I been missing out on?” Energy.

New York, I missed you.

4

0

36

I’m looking for a way to help more companies figure out their credit strategies.

Credit is really complicated and nuanced stuff. And we have the most exposure

@bloomcredit

to what works and what doesn’t.

What is the best way for us to guide other fintechs to desired outcomes?

9

4

36

Bloom Credit is growing super fast right now.

Not in the PR - the business 4x’d sales in Q1 on the back of tons of latent demand to launch credit products and we’ve just made some pretty epic hires too.

I’m admittedly biased but…Keep your eyes on us 😉

3

5

35

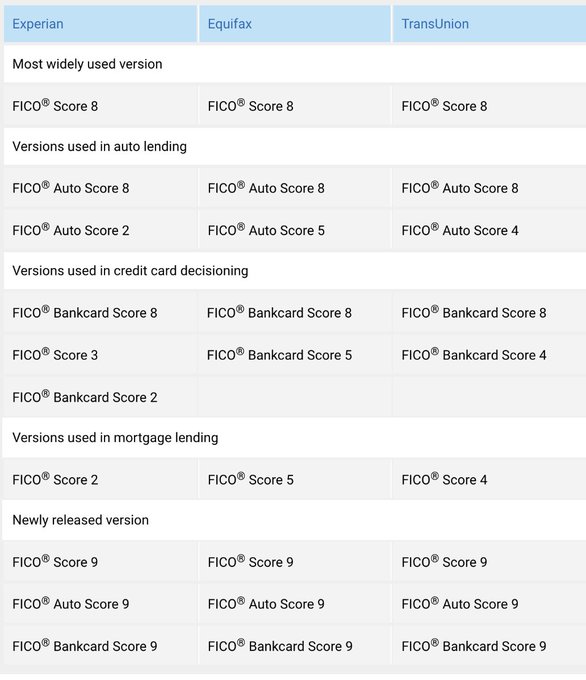

Reporting utility data to improve credit scores is NOT a thing

Most scores prior to FICO 9 do not take utility into account. F9 is likely a decade away from mass adoption. Reporting that data is screaming into the void.

Want to improve scores? Turn utility payments into BNPL

5

2

36

Bloom is hiring for a Director of Product! We have tons of demand and are looking for someone to help us build products to help our customers.

Please apply, or recommend me the best product person ever =)

0

10

34

I often have college students reach out to me asking to connect. I used to be this kid, so I almost always engage.

I'm pretty disappointed at the number who just ask me (without developing a relationship) for an internship.

Don't be transactional. You'll miss the real value.

3

2

28

We're doing a lot of hiring

@bloomcredit

! Lots more positions are going up, but wanted to get this out there.

Let me know if you, or anyone you know is interested in joining us to make access to credit data and services more accessible!

0

5

34

We're hiring for a VP of Revenue

@bloomcredit

! We have a ton of inbound demand, and are looking for a sales leader to create systems and build a team to enable us to scale and grow.

If you or anyone you know is interested... please get in touch!

1

4

34

Very quietly...

@VCMike

has had multiple portfolio companies ($OPEN, BarkBox, Color, Whoop) become unicorns this year

Given how much attention VCs generally get, the fact he remains so under the radar (by design btw) is pretty impressive.

Seed founders should speak with Mike :)

1

3

33

I always think it’s funny people want to always have the conversation about how predictive fico is …

You’re missing the point. Fico is never going anywhere because of the compliance use cases it offers.

Say it with me now: “We. Are. Never. Replacing. Fico.”

6

1

32

I'd like to announce that as part of our Series A... we are rebranding to Paisley Credit.

We are expecting that with the name change, we will likely see a preemptive Series B at a 5x valuation sometime in the next 3 days.

2

1

32

Today is the 4 year anniversary of

@tedr

passing away. Ted helped start

@bloomcredit

, so I think of him often.

He taught me many lessons in a short time. None more important than to reframe your purpose in terms of what you can do for others.

Miss him lots. Enjoy every day

1

0

32

People think CEOs becomes burnt out or depressed because their company hit a road block.

More often, the company hits a roadblock because the CEO got burnt out or depressed.

If you're a VC ... encourage your founders to take care of themselves. It'll help your returns

3

2

32

I feel like it’d be a fun exercise to do a list of “critically acclaimed” Fintech companies.

@onbondstreet

,

@pinchrent

,

@final

,

@BankSimple

come to mind.

Companies where they got bought before their time but we all respect the founders and the paths they paved etc

5

1

31

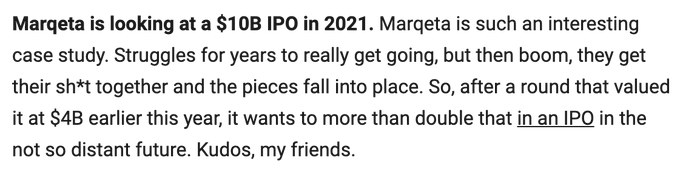

I think there's an inverse relationship between the size / ease of a raise vs how successful that company will be when it comes to fintech infrastructure.

Look at early rounds in Marqeta, Socure, MX... Not competitive Series As or brand funds.

Privacy is more recent example

7

1

32

VCs... never tell a founder to bootstrap. They wouldn't be talking to you if that was an option.

It highlights your clear lack of empathy with founders and also your lack of understanding of the financial distress ~95% of founders go through.

Just don't ever do it.

2

0

30

API businesses seem to be among the best venture capital businesses once they hit the public markets.

Especially in an increasingly digital world.

Twilio's market cap is $37.3 bln

It was $10.6 bln last time I saw any of my colleagues

5

28

554

4

3

31

Things that are quite likely when you found a company:

- Anxiety / stress

- Fractured relationships

- Financial Instability.

Things that are quite unlikely when you found a company:

- An exit where you become extraordinarily wealthy.

Act accordingly.

2

0

31

@pitdesi

For those that don't know.... Sheel was also first institutional money in the biz. Grateful for all the support over the years <3.

Even if we're not cool enough to make his twitter bio 😋

1

0

31

Want to know why credit is so difficult to understand?

Just the FICO score has multiple use cases.

You need it for:

- underwriting

- compliance (AAN reasoning)

- securitizations

- Marketing (direct mail)

And so on…

That’s 4 (largely unrelated) departments of a business.

2

1

31

95% of pitch deck feedback is irrelevant

Most of it is aesthetic feedback around how information is presented.

The best way to know if your pitch deck is good would be to ask someone to pitch you your company back to you.

If they can easily do this, your pitch is working 🦄

3

1

30

Credit looks at 2 things. Ability and willingness to repay.

We focus a lot as an industry on ability (this is what a FICO/ plaid calculates).

Next gen credit models will attempt to understand a consumer’s willingness and build that understanding into their business model.

6

1

29

Who would want to do some Fintech devcon karaoke tomorrow night?

@tommyrva

,

@venturedan

,

@sairarahman

,

@cokiehasiotis

,

@dionlisle

,

@shamir_k

,

@jakebruemmer

,

@lcdavis1225

?

Tag others but would love to book the karakoke bar near the conference if others are interested!

14

2

30

Multiple people have been trying to start businesses that look like

@bloomcredit

pre pivot.

Really love this model and sincerely hope people can make it work.

But also just a funny reminder everything in fintech repeats itself every 5 years.

1

1

29

One week away from

@infinicept

's ignite conference!

Super pumped to be hosting the embedded fintech panels.

Featuring...

@laurencrossett

from

@PinwheelAPI

@bolingj

from

@lithic

@shamir_k

from

@SilaMoney

@lcdavis1225

from Atomic

Ginny Chappel from

@moov

See you there!

0

7

23

The rumors are true. I did in fact turn 30 today. Which I'm sure is surprising for many of you given I've been in the fintech world since I was 19. But here we are.

Also thanks a ton

@cokiehasiotis

for giving me the best birthday yet. Truly the best partner I could ask for <3

2

0

27

Or… and this is a crazy idea but hear me out…

We keep asking all the BNPLs to report their payments so consumers can track them?

Can confirm they are all thinking of this… let’s keep asking for it :)

Product idea for a bank:

A BNPL budgeting app for consumers to pull together all of their BNPL loans and get a unified view into their future cash flow.

To build this, the bank would likely have to screen scrape the BNPL providers, which would be the ultimate irony…

17

7

110

2

2

29

For y’all who were wondering why I no longer live in nyc this sums it up.

It’s hard for us to separate ourselves from our natural roots. Concrete jungles are not what our nervous systems naturally seek.

Simply put - I feel better in nature :). You might too.

Leaving NYC was so good for my mental health—left May 2020 and since then barely took anything for my anxiety, I’ve now been back for 1 month and have had more anxiety in 1 month than in 1 year being away.

13

1

179

3

0

27

For anyone that generally believes this… give me a call and see if I can’t change your mind in 10 mins 😇

Anything you likely see has “shady”behaviors almost always has a really solid and logical reasoning to it.

Credit bureaus are a cartel and operate an extensive criminal enterprise.

27

19

328

5

0

27

Hey friends!

I’ll be

@money2020

this year - who is around and wants to catch up.

Pumped to see y’all in person 🙏😎

9

2

28

I miss early to mid 2010s tech vibes in nyc. Genuine optimism from people trying to build things because they were passionate and cared about the stitching instead of building for external validation.

How do we bring back that energy?

12

0

26