joseph francis

@joefrancis505

Followers

5,093

Following

1,813

Media

601

Statuses

5,994

Economic historian, writing on slavery and American capitalism for @Harvard_Press and on Argentina for @politybooks . Honorary Research Fellow @unibirmingham .

A hill in Wales

Joined November 2008

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

貴方のサークル

• 240141 Tweets

#WinkwhiteXอิงล็อต

• 238430 Tweets

ガイナックス

• 108305 Tweets

#MyLoveMixUpTHep1

• 65520 Tweets

松岡茉優

• 51083 Tweets

ノーヒットノーラン

• 48994 Tweets

大ちゃん

• 45904 Tweets

#carp

• 33528 Tweets

ギターと孤独

• 31124 Tweets

雇用統計

• 28245 Tweets

Sinner

• 28133 Tweets

ドラコー

• 26048 Tweets

ジェイド

• 24960 Tweets

有岡くん

• 24615 Tweets

大瀬良投手

• 22954 Tweets

ポーランド

• 21530 Tweets

Cubarsí

• 19305 Tweets

モイネロ

• 16475 Tweets

Alcaraz

• 15197 Tweets

ホタルちゃん

• 12572 Tweets

アルジェンティ

• 11470 Tweets

Pinned Tweet

Correction: every day is the day for getting into debates about Argentine economic history.

1

1

29

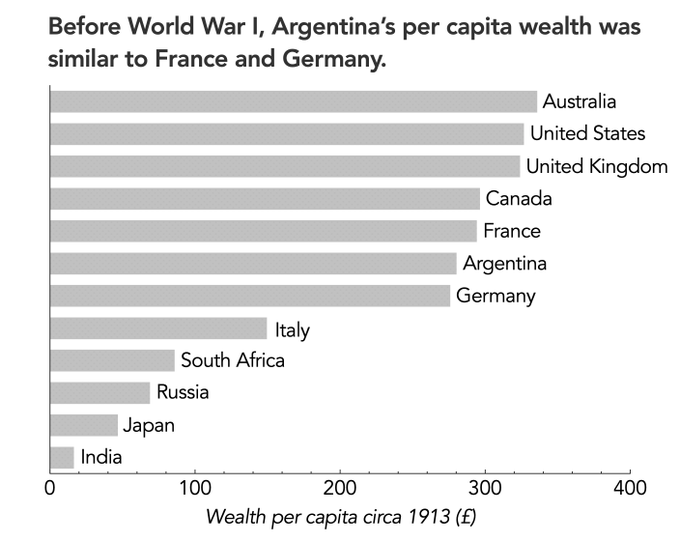

In my PhD dissertation, I thought I had refuted the “golden age myth” that Argentina was once “one of the richest countries in the world”.

In retrospect, however, I actually showed that it wasn’t one of the most developed countries. 1/

33

360

2K

My pessimistic forecast is, then, that we will see a decade of persistent financial crises while we sort out the underlying productive base.

Because no-one listens to economic historians, we will then forget why the crises happened, and the cycle will start again.

8/

8

14

375

Argentines love to beat themselves up for not being Australians. “Why isn’t Argentina like Australia?” is a common question.

My new GDP estimates help provide an answer. 1/

34

100

372

Thereafter, the country’s lack of development was revealed, especially with regard to its political institutions and education levels.

That, in any case, would be my take on the “Argentine paradox” if someone wanted to give me some money to write a book on it. 7/

12

14

342

Today I signed a contract with

@politybooks

for “The Poor Rich Nation: Why Argentina Fell Behind” 🥳. To celebrate, here’s a thread that summarizes the book’s argument as I currently see it. 1/

18

67

340

I made more or less 6,000 pages of documents from the US Embassy in Buenos Aires from the 1960s to the early ’70s available online: .

They mainly relate to economic issues and should be of interest to historians working on the period. 1/

13

115

338

Jerome Powell's speech at the Brookings Institute on November 30th seems to have only been announced yesterday. Notably, it is just two days before the Fed's pre-FOMC comms blackout begins.

1/

13

71

324

That’s why I would now refer to it as a “poor rich nation”. It was wealthy, but had development indicators more typical of a poorer nation. 4/

2

15

295

And if that hypothesis were correct, my interpretation would be that it had experienced a massive asset-price bubble in the nineteenth century that burst once the terms of trade for grain exporters deteriorated during World War I. 6/

4

16

287

My mistake was to confuse development with wealth.

Subsequently, I looked at Argentina’s level of wealth circa 1913, and I discovered to my surprise that it was one of the richest countries in terms of wealth per capita. 3/

3

27

269

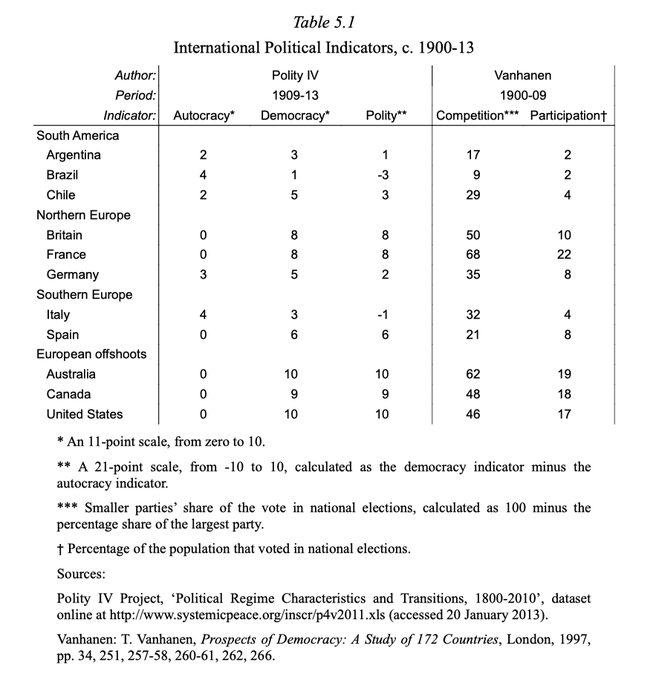

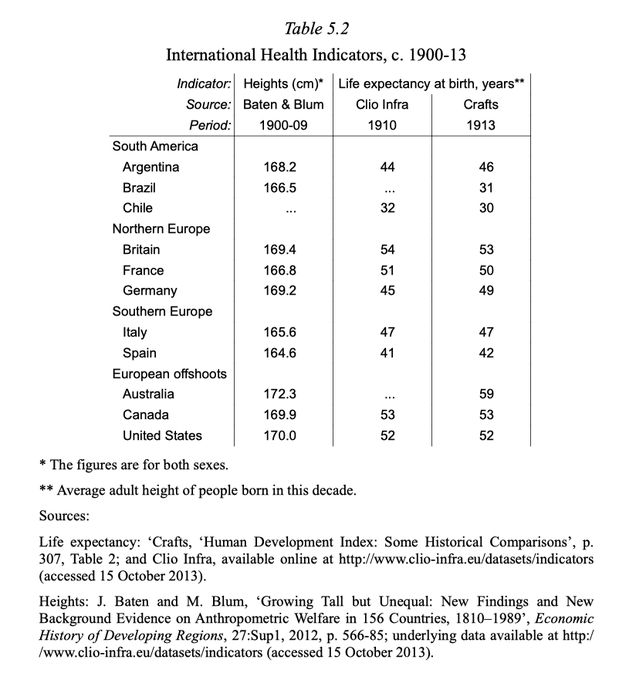

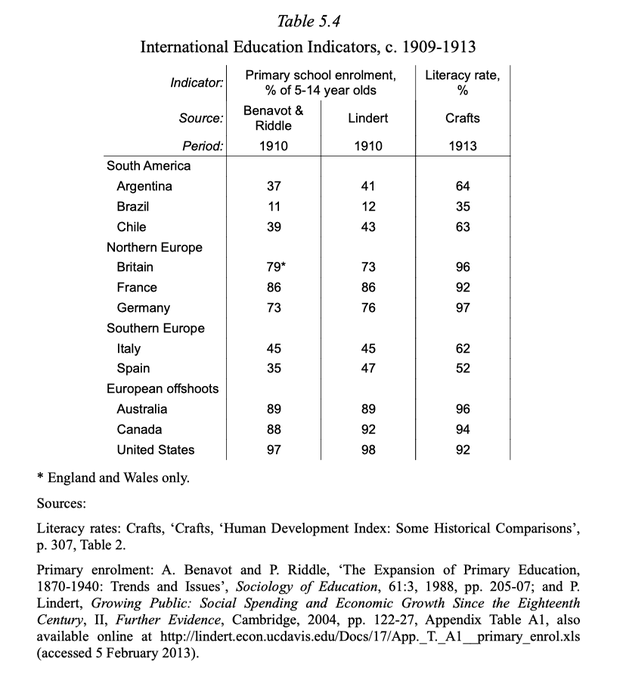

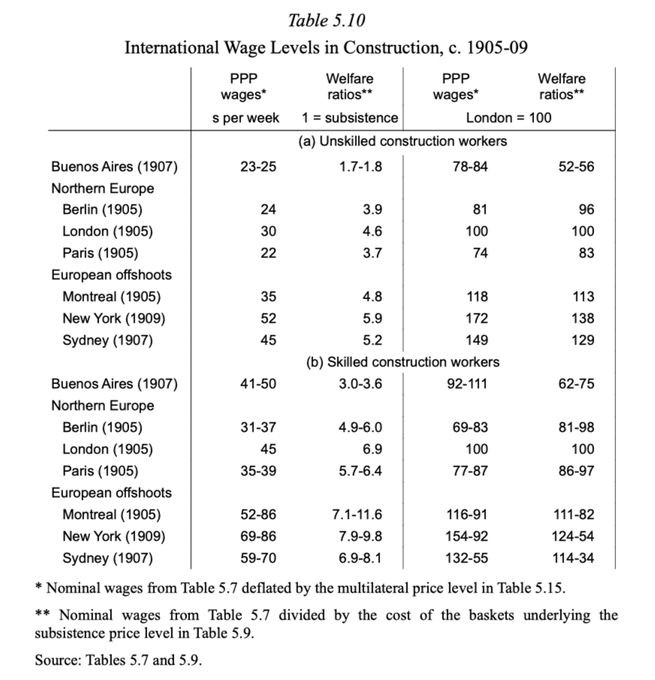

In Chapter 5, I showed that according to various variables – political institutions, health, education, purchasing power of wages – Argentina lagged behind the most developed countries circa 1913.

It wasn’t, therefore, one of the most developed countries in the world. 2/

2

31

244

The current bear market is driven by illiquidity as central banks withdraw their largesse.

Earnings will also fall as US corporations begin to suffer the effects of a strong dollar, high interest rates, and reduced discretionary spending – Engel's Law is a bitch.

2/

4

6

219

As such, the recovery is unlikely to be V-shaped for a lot of sectors. ARK will not recover.

Overall, there are likely to be 10-15 years of relatively poor stock returns, possibly with another major bear market, much as 2007-9 followed 2000-2.

4/

3

10

211

Historians are way ahead of economists in their appreciation of complexity and indeterminacy.

There. I’ve said it. Now crucify me.

17

23

212

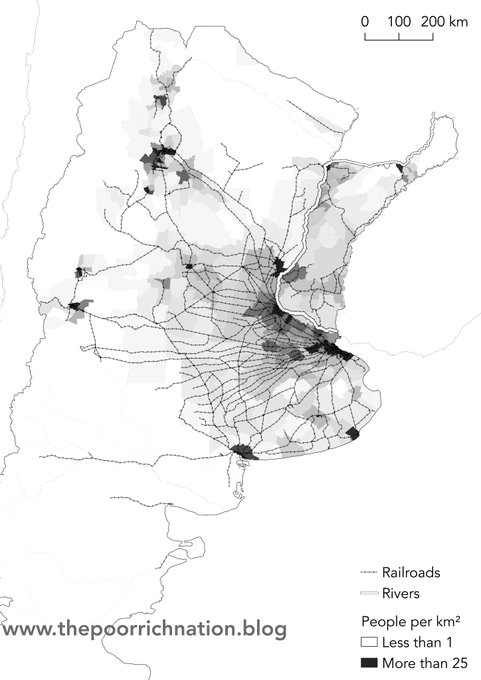

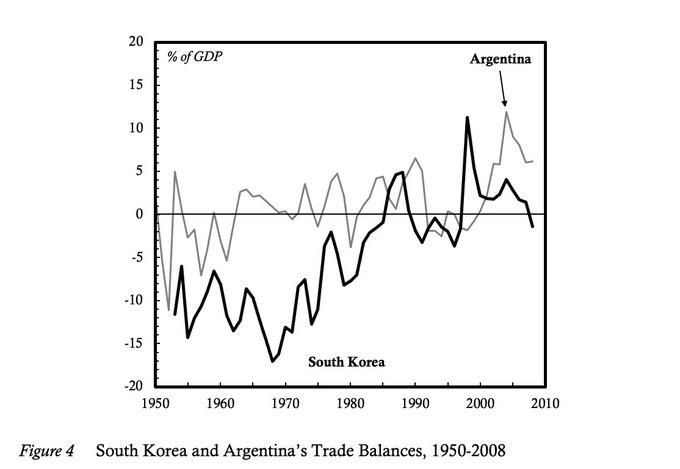

Argentina in 1869 vs Argentina in 1914

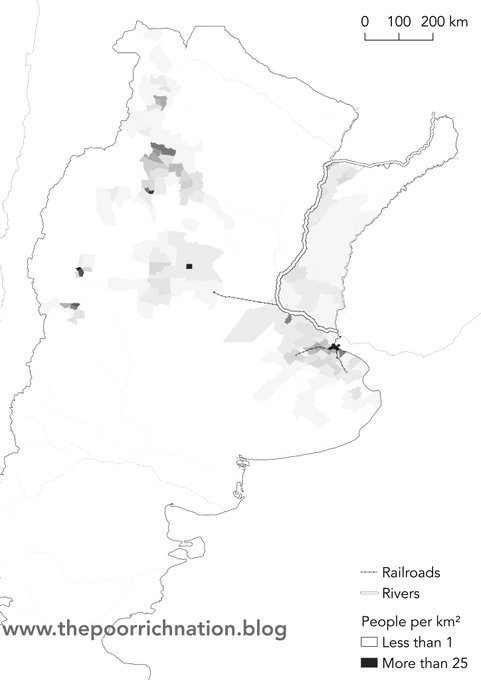

In 1869, Argentina was still two countries: half the population was in the Interior, away from the Paraná River, which gave the half of the population in the Littoral access to the world market. 1/

3

48

209

Commodities and commodity-producers, on the other hand, will do well, although with their usual wild short-term fluctuations.

Nonetheless, scarcity will eventually turn into glut, and the commodity boom will end.

5/

6

5

200

This month's Treasury General Account bounce came a bit earlier than I expected.

The federal government normally pays its bills at the start of each month, releasing funds from the TGA, which in turn provides liquidity to financial markets.

1/

15

50

200

joe francis

Something(s) will break, perhaps sovereign debt, corporate bonds, and/or Europe. Central banks will then be forced to turn QE back on.

Given the threat of structural inflation, however, they will not be able to do so in the same indiscriminate manner as before.

3/

5

4

192

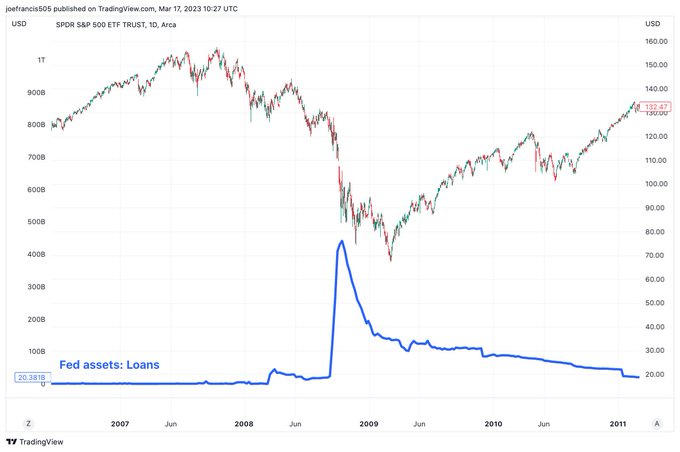

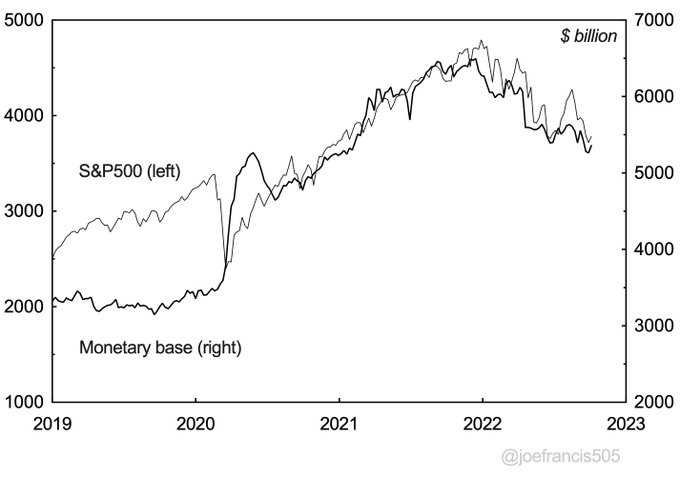

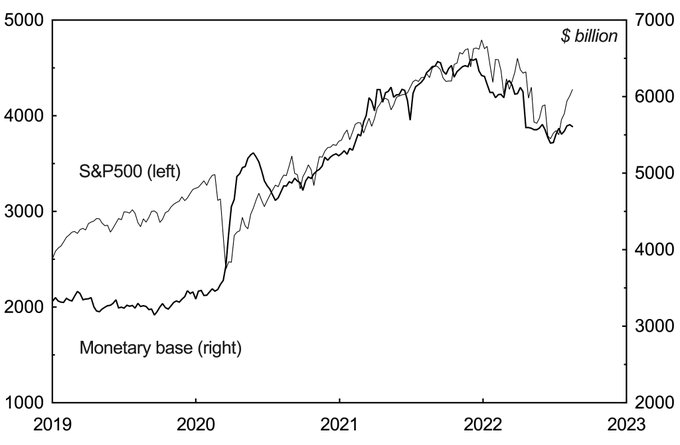

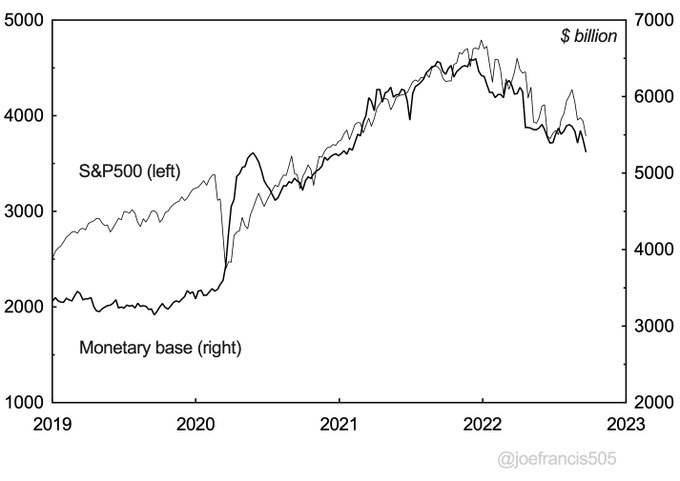

There's much excitement because the Fed's balance sheet has gone up due to the BTFP. However, the Fed hasn't bought securities. Rather, it has made loans (of last resort, etc). Here's what happened to stocks when it did the same during 2007-09.

14

61

196

If I had research funding, I would now attempt to estimate Argentina’s GDP circa 1913. My hypothesis would be that it had a high wealth-income ratio. 5/

5

9

179

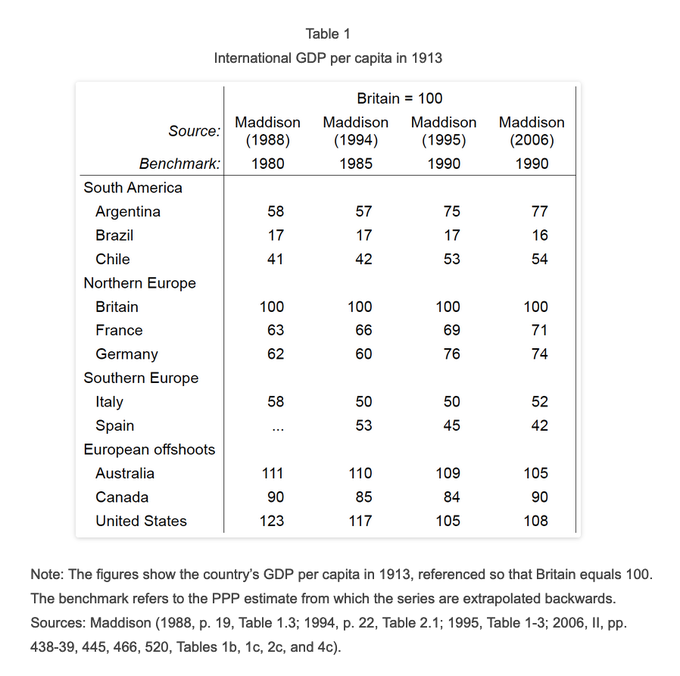

To anyone using the Maddison Project’s numbers for Argentina’s GDP per capita: please don’t.

They’re based on extrapolations backwards from recent estimates of PPP GDP per capita using very dodgy quantity indices. Maddison himself produced wildly different estimates for 1913. 1/

5

49

183

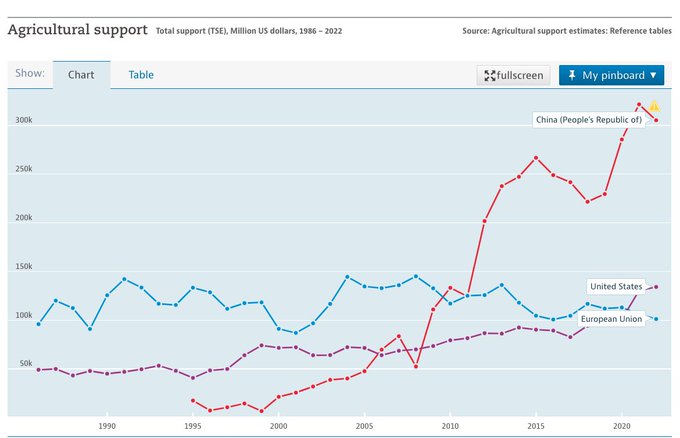

The growth of China’s agricultural subsidies is incredible: now at $300bn per year, according to the OECD.

14

63

171

How did the institutionalist paradigm come to dominate the study of economic history? In short, it was because the institutionalists won the American Civil War of 1860-1865. 1/🧵

6

39

168

Like all things, these cycles have a history. Typically, they last about 25 years. I have speculated about why in a previous thread:

7/

34 years ago, Laibach released their version of 'Across the Universe'.

'Nothing's gonna change my world' goes the chorus.

Yet, a few years later, the country they lived in, Yugoslavia, fell apart.

Europe feels like it is at a similar moment today.

1

11

40

1

2

162

This isn’t a good metric for judging when the Industrial Revolution began because it doesn’t say anything about mechanization.

Instead, the Cambridge research suggests we need to think more about British industrialization BEFORE the Industrial Revolution.

9

34

163

Stocks will then start to recover, as it will be possible to have more expansive fiscal and monetary policies without fuelling such high levels of inflation.

Liquidity will return to the market, and a new era will be declared.

6/

2

2

159

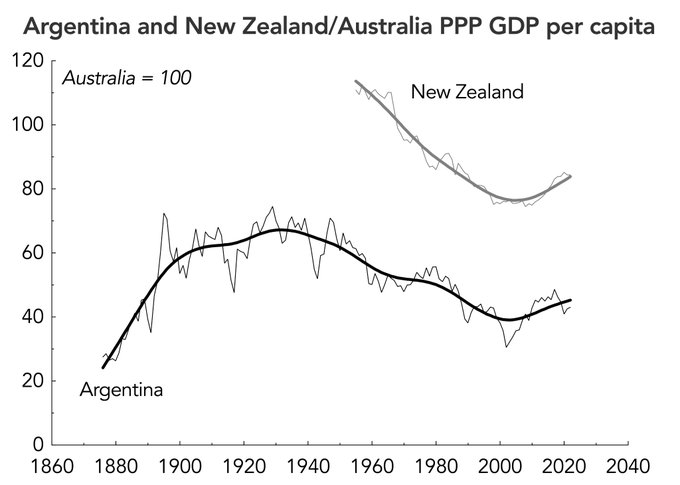

Adding New Zealand to the Argentina/Australia comparison complicates the picture. Why aren’t there more articles in the Economist about how New Zealand’s terrible institutions have led to long-term relative decline?

21

21

164

There has been a correlation between liquidity and stocks since 2020. Initially, it was quite loose, but it has become tighter.

There was also previously a 2 or 3 week lag from liquidity to stocks, but that has now gone to a few days.

The question is why.

1/

5

31

159

I’ve started a blog for my new book project on Argentina.

The aim is to post as I research and write, in a kind of public journal. 1/

9

34

142

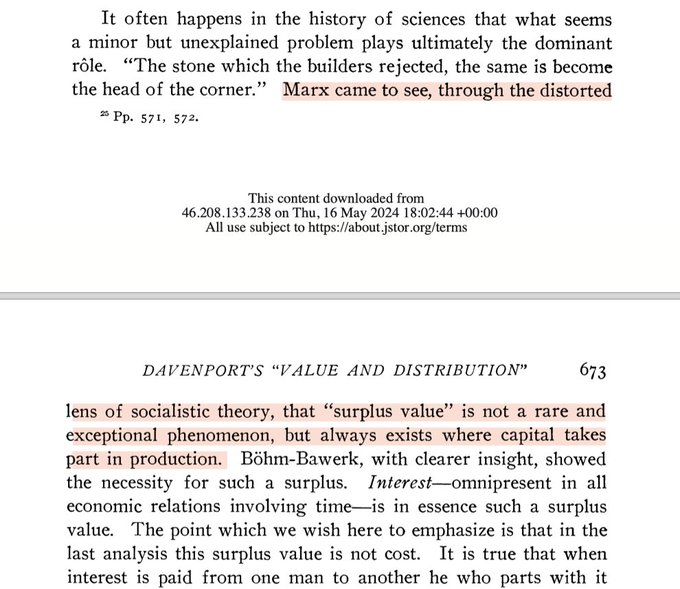

Journal of Political Economy, December 1908.

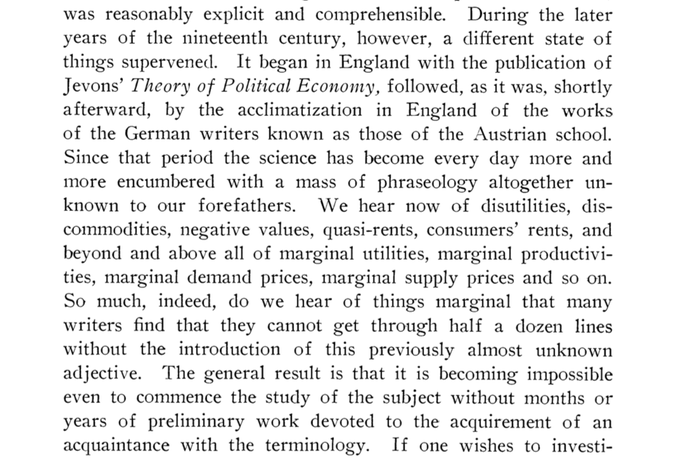

Irving Fisher describes how Karl Marx’s theory of “surplus value” laid the cornerstone for what would later be called the “marginal revolution”.

8

18

121

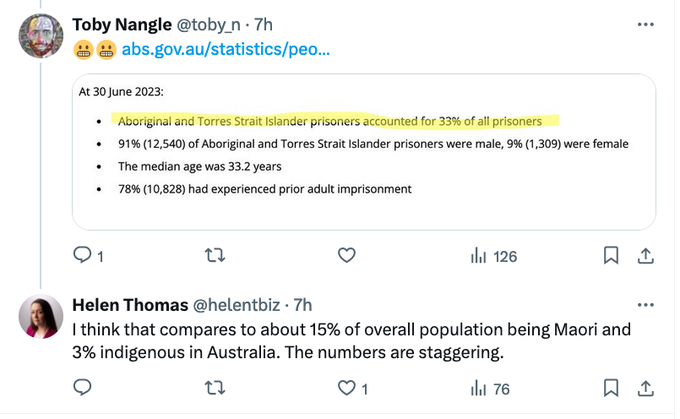

Financial Times: Anglo countries are great at assimilating immigrants; just look at their prisons.

Reality: Australia and New Zealand are outliers because their prisons are full of their surviving indigenous populations.

14

14

117

There’s no consensus among economic historians that tariffs weren’t a significant driver of US industrialization.

A few examples of those who argue that they were during the antebellum period. 1/

Economic historians reject tariffs as a significant driver of the industrial revolution because the evidence strongly suggests this is not the case. Not because they have an unwavering devotion to theory.

5

6

66

7

23

116

First time I got to print the little beastie. Happy New Year to y’all!

6

11

114

Most want development to be a result of things they like. Liberals want it to be a result of the state and democracy. Neoliberals as a result of property rights and free markets. And so on. Few are willing to see it as being due to unpleasant things like exploitation and slavery.

13

15

94

@PauloMacro

@kittysquiddy

Tier1 Alpha highlighted this morning that there is virtually no hedging for left-tail risk going into tomorrow. The last time it was like this was before the crash in 2008.

2

10

83

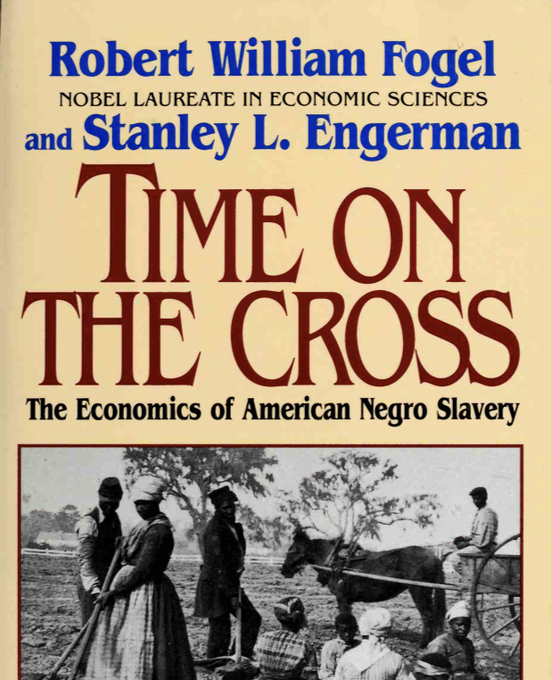

The problem with Fogel’s Without Consent or Contract is that his central claim about slave plantations being more efficient than free farms is wrong.

Slave plantations only had higher productivity if you assume that the enslaved and free farmers worked similar hours. 1/

2

18

80

I'm an economic historian of Argentina, but suddenly I find that everything makes sense here in the UK.

8

8

79

@NewLeftEViews

Althusser’s description of how he “learned” philosophical texts is a classic.

5

14

79

Focusing on the agency of oppressed groups can lead us to misunderstand and/or underestimate the structures that oppress them.

Let me make a broader meta-point:

Since the 1970s, feminist anthropologists, archaeologists & historians have tried to show that women had agency, mattered & did stuff.

This has sometimes blinkered our understanding of actually existing inequalities & differences.

8

85

414

4

10

76

It is, however, worth noting that both countries fared poorly when compared to the United States. This was because of the types of country that they were.

They demonstrate how land abundance ceased to be such an advantage in the 20th century. 10/

4

5

73

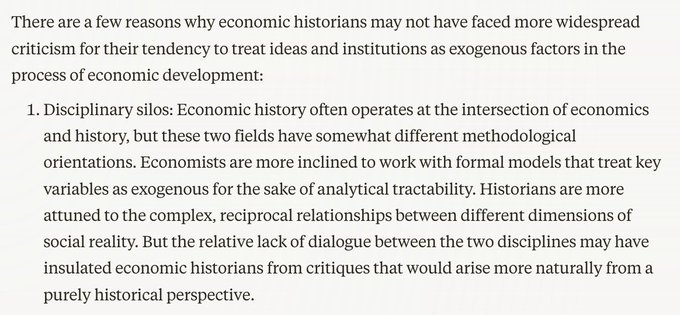

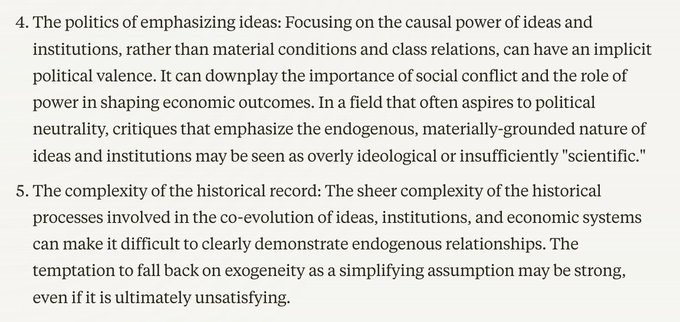

“Why haven’t economic historians been subject to more critiques about their emphasis on the exogenous nature of ideas and institutions?” Claude 3 is quite good.

3

11

72

@drmtgr

Yes, you’re correct. Buenos Aires was like Paris; the rest of the country was more like Latin America.

2

4

69

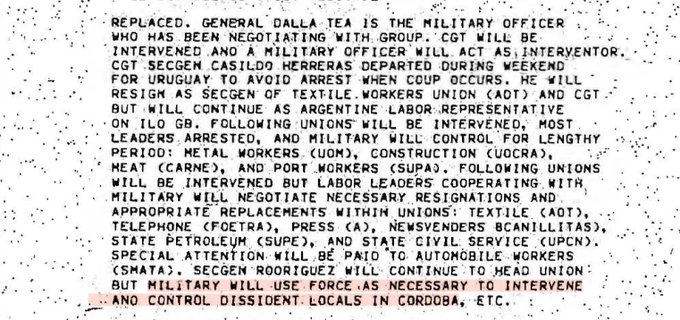

This is probably my favourite US Embassy cable. It’s from March 22, 1976, and describes a meeting in which Peronist union leaders conspired with the military to purge the labour movement. 1/

3

17

71

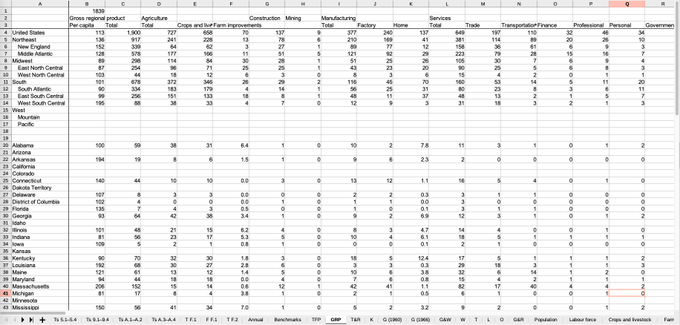

US GDP by sector and state in every census year from 1839 to 1899 is the biggest empirical project I’ve done, even if the results are entirely incidental to my book’s argument.

Just finalizing the mega-spreadsheet...

3

9

68

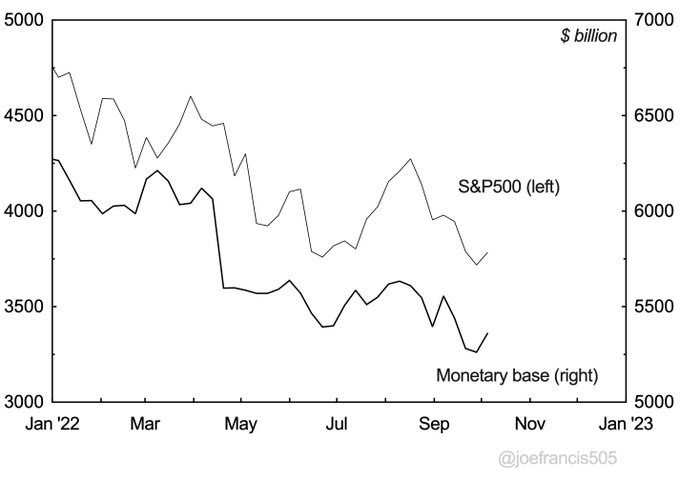

Indeed, if its current trajectory continues, the S&P500 could hit 4100 just as his speech begins, which is a level that some big speculators are looking at to go short. It would also have hit a trendline that is widely seen as an obvious peak of the current rally.

8/

3

8

65

In short, the problem with Time on the Cross was that Fogel and Engerman determined that slavery was more efficient than free labor and then decided that they had to reconcile that with the traditional liberal belief that freedom was good. 1/

4

13

67

This is what QE looked like after 2008. It was only when the Fed started buying securities (not just providing emergency loans) that stocks went up.

4

10

67

1. This article illustrates how the New History of Capitalism has failed to demonstrate slavery's contribution to the growth of the United States. It presents evidence that actually reinforces the critique made by economic historians.

6

17

66

The mercantilists weren’t as crazy/stupid as commonly believed.

It's commonly thought that mercantilists valued a positive trade balance either bc they naively equated gold w/wealth or bc they held a zero-sum view of trade. But the value of specie inflow was that it could support domestic banking, therefore investment and development.

4

2

31

11

6

65

@Jackbmeyer

Every major religion except the biggest, which is also the main religion of the richest countries, where they eat lots of pork.

1

0

65

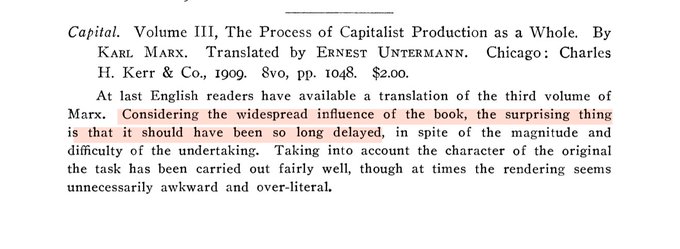

From the Journal of Political Economy, October 1909. It seemed to think that Marx had “widespread influence” back then...

8

4

62

The relationship between liquidity and the stock market is becoming a reflexive feedback loop, creating conditions for another major recession. A thread. 1/

5

18

62

This is an example of a document from the US Embassy: it describes a meeting from 1965 in which Alejandro Shaw, a banker, tries to persuade the US Ambassador to support a military coup, with José Alfredo Martínez de Hoz made Finance Minister. 4/

1

13

62

Never mind the Middle East, things are blowing up in Economic History RIGHT NOW. 🤣

4

4

63

Here’s a brief explanation of why this table explains the importance of the Marshall Plan to Western Europe after WWII. 1/

Here's an "oooh!" moment...

h/t

@adam_tooze

for this one.

The Marshall Plan should have meant lots of imports into Europe buying the US goods to rebuild.

Problem is it doesn't who up in the net export figures. So, what did they do with the cash?

15

31

154

3

9

63

I have become convinced that the cycles are driven by what psychologists call 'generational amnesia'.

With each generation, we forget much of what the previous generation learned the hard way.

We must also learn it the hard way.

1

7

60

Journal of Political Economy, July 1909.

The marginal revolution sucks.

2

12

62

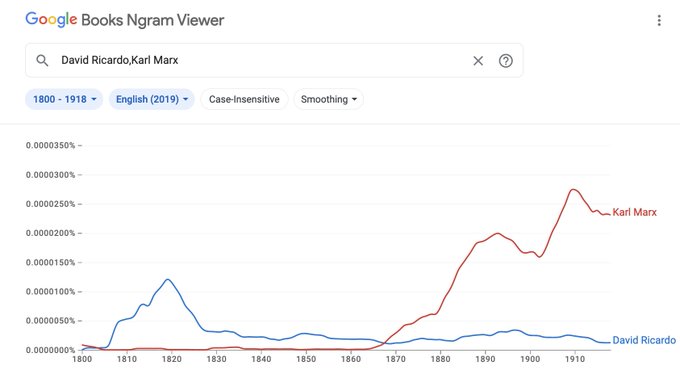

The Ngram data don’t support this assertion.

They suggest that Marx was an important political economist before the Russian Revolution. Then Lenin turned him into the Messiah.

That interpretation probably won’t please either side, but it is more accurate.

Marx was a nobody until a Russian bloodthirsty Psychopath used state power to promote his work for all the useful twitter marxists a century later

Magness, P. W., & Makovi, M. (2023). The Mainstreaming of Marx: Measuring the effect of the Russian Revolution on Karl Marx’s…

6

8

65

8

7

63

@sonjaavlijas

Argentina and Japan are the only interesting countries in development economics.

6

4

61

This was the “American Miracle” from 1790 to 1900. It’s underrated, in my opinion.

9

11

61

One of the limitations of using ChatGPT as a research assistant: it makes up references, then makes up stuff about its made up references.

9

9

58

“Historians, who understand about contingency and about multiple and multidirectional causality, often do a better job than economists of identifying important mechanisms that are plausible, interesting, and worth thinking about…”

1

14

58

Instead, Argentina only fell further behind Australia more recently, during the debt crises of the 1980s and early 2000s.

(There’s a good reason why the University of Buenos Aires houses a Museum of the Argentine External Debt.) 5/

1

4

56

I'm just thinking aloud by writing this thread, and I'm likely to be wrong about all of it, so feedback is very welcome.

14/

5

0

56

Looking forward to reading this: left-wing liberalism has a history. I hope it (a) addresses how the left became so instinctively protectionist, and (b) includes a discussion of Juan B. Justo, the Argentine socialist leader who was a keen advocate for free trade.

So delighted to share the publication of

@Pax_Economica

: Left-Wing Visions of a Free Trade World with

@PrincetonUPress

!

20

127

515

4

7

55

As predicted, last night's Fed balance sheet stats show liquidity falling off a cliff, which explains why stocks have also been dropping.

1/

3

9

55

@INArteCarloDoss

What if Powell only talked to him that one time and he's been bluffing since?

2

0

55

The comparison with Australia suggests, therefore, that the origins of the external debt provides the key to understanding how domestic factors contributed to Argentina’s decline. 6/

2

3

55

The Argentina-Australia comparison thus shows that domestic factors do matter. For Argentina, the military government of 1976–1983 was a disaster that Australia managed to avoid due to its more stable politics. 9/

1

5

53

To what extent did institutions matter to Argentina’s failure in the 20th century?

The roots of institutional weakness are found in the 19th century, when Argentina’s democratization was delayed due to the differential impact of globalization on the Interior and the Littoral. 1/

¿Por qué Argentina no fue Australia? 🇦🇷🇦🇺

Porque:

1) Enviudó mal de Inglaterra (Halperín)

2) Perón dirigió de arriba en tres años una industrialización que Menzies & Co. acompañaron de costado por décadas (Gerchunoff)

3) Mala suerte con minerales (casi todos)

4) Mala suerte…

66

29

218

4

4

53

@simon_ree

It looks like there was systemic fear that something was going to happen in 2019, but then the pandemic put it on hold. Now it's going to happen.

3

1

51

@INArteCarloDoss

It's when bank reserves fall to $2 trillion. That's the minimum they think the system needs to function. That puts the S&P500 on course for about 2500, based on its current correlation with the monetary base, which is in line with your target, I think.

2

2

52

And they did. But then they went back up again.

Unless Powell has had a significant change of heart, you've got to assume that he has decided to give this talk in order to take direct control of the narrative before the next FOMC, in order to reinforce that message.

4/

1

0

48

This is Version 1 of my new Argentina/Australia PPP GDP per capita estimate.

It suggests that from the late 1890s through the 1970s, Argentina’s GDP per capita was around 50% of Australia’s.

There was no relative decline. 4/

2

4

49

I can’t believe Putin locks up philosophy professors like this.

Among those arrested today were Noelle McAfee, Chair of the Philosophy Department at Emory University.

21

71

170

1

3

47

Perhaps I just got lucky or perhaps I'm on to something.

It's also likely that liquidity and stocks will decouple at some point. If earnings go downhill (or improve!) rapidly, for instance, liquidity might not matter so much any more.

13/

8

1

46

Powell must also be aware that this time his speech could have a much greater impact because the stock market is, from a technical perspective, a lot more overbought than when he spoke after the previous FOMC.

7/

1

0

44

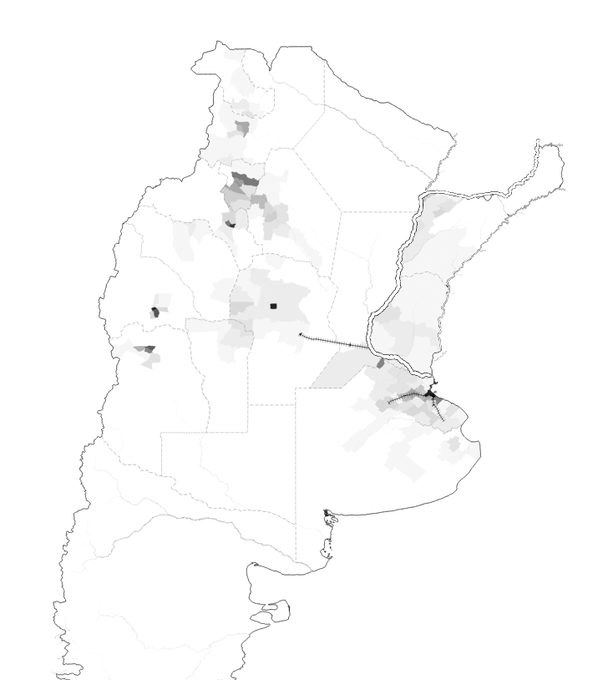

Population density shows how Argentina was divided in two in 1869. A railroad was, however, being built to link Córdoba to the Paraná River.

Railroads would both give the Interior’s oligarchies a stake in globalisation, and allow federal troops to intervene to support them.

4

9

45

James Bullard might have paved the way last week with the warning that rates might have to go to 7 percent before inflation is tamed.

5/

3

1

43

Argentina’s nominal GDP per capita relative to the United States tells a simple story: the country never recovered from the Great Depression.

4

12

42

34 years ago, Laibach released their version of 'Across the Universe'.

'Nothing's gonna change my world' goes the chorus.

Yet, a few years later, the country they lived in, Yugoslavia, fell apart.

Europe feels like it is at a similar moment today.

1

11

40

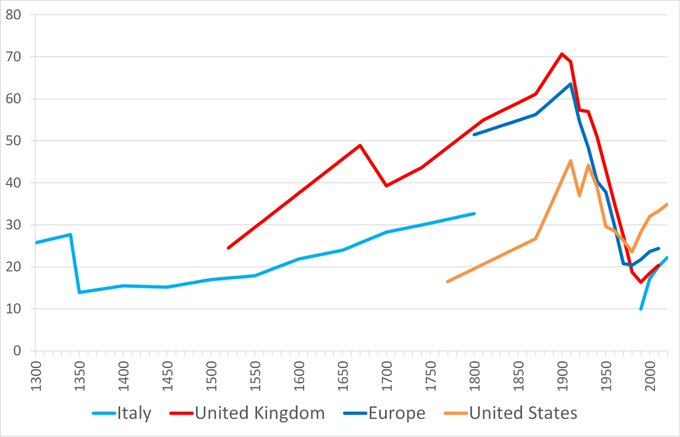

This is extraordinary if correct: in a few decades, the mid-20th century undid centuries of increasing wealth inequality.

1/4 The wealth share of the "one-percenters" in a range of Western countries, 1300-today (based on my book As Gods Among Men,

@PrincetonUPress

). Note the long-run tendency for wealth to become more concentrated in the hands of the few, except after the Black Death and in 1914-70

1

44

87

4

7

41

Even Mary Daly chipped in with the warning that "Pausing is off the table right now. It’s not even part of the discussion".

6/

1

5

41

The next year, Argentina had its own constitutional crisis. The military government ended up killing around 30,000 people while borrowing heavily abroad. Argentina was then left vulnerable to rising interest rates and falling commodity prices in the 1980s. 8/

1

1

41

I’ve wanted this one in hardback for ages. Found it today.

1

2

41

It’s obvious and to be expected that Marx only became a household name thanks to the Russian Revolution.

But it’s also accurate to say that he was at least a moderately well-known economist pre-1917. 1/

I refer to this one as argumentum-ad-"this one time at band camp..."

It entails cherrypicking another name whose Ngram pattern falls below Marx and then declaring that Marx must therefore be important because of your single non-random counterexample.

The problem with this…

2

3

34

3

5

39

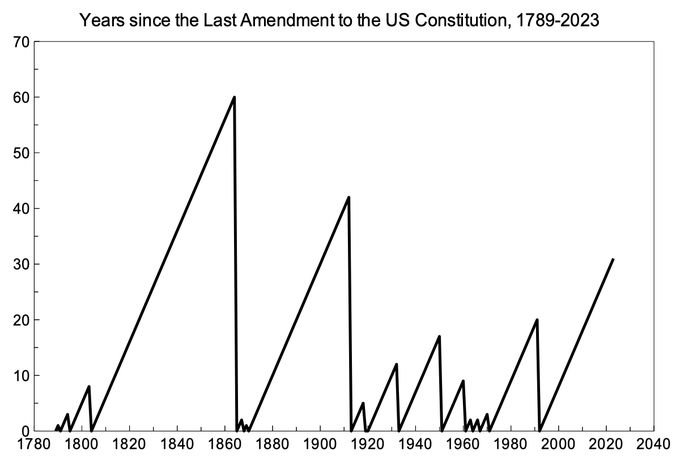

A graph that illustrates how much the United States played with its constitution in the 20th century and how little it has done recently. The country is approaching 19th-century levels of ossification.

4

1

39

Last time, Mary Daly was the last Fed speaker before the comms blackout. She helped spark the current stock market rally with her comments that it was time "to start talking about stepping down" on interest rate hikes.

2/

1

3

38

Michael Howell of

@crossbordercap

has long emphasised the importance of liquidity to financial markets. He wrote the book on it, so I would defer to that for the basic relationship.

2/

1

7

39

'Such is the game that the aeon plays with itself', as Nietzche put it in Philosophy in the Tragic Age of the Greeks.

As a result of our forgetting, this winter will also be tragic, in Europe and elsewhere.

1

2

36

Journal of Political Economy, February 1911.

Marx was described as a “great philosopher”. Shouldn’t this be retracted?

3

1

38

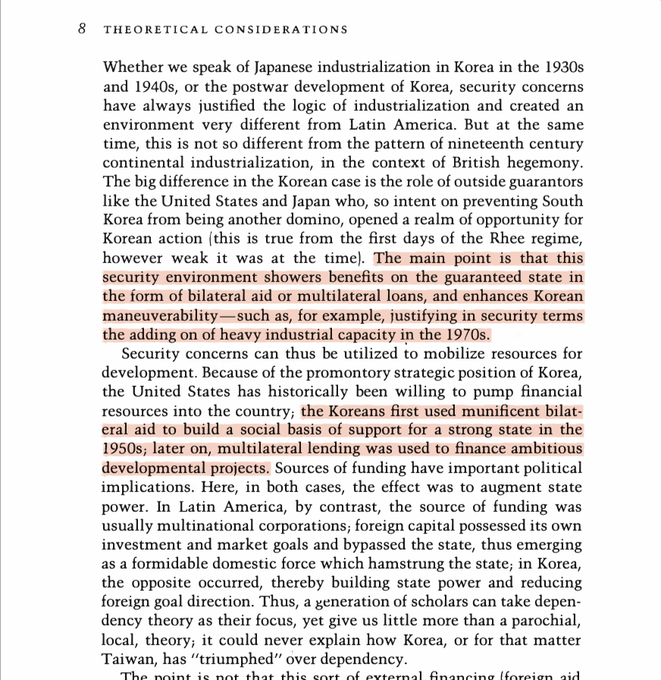

The fuller explanation comes from Meredith Jung-En Woo's Race to the Swift – an under-read account of South Korea's great transformation.

5

4

37

Generational amnesia has, I believe, afflicted humanity from the beginning, as we have traditionally refused to learn from history.

Each generation thinks that this time will be different. But it probably won't be, except for in the details.

1

6

36

We have to rediscover that societies need investment in their productive capacities to maintain their standards of living.

We must understand again that people spend less on aspirational goods and services when they have to focus their budgets on eating and keeping warm.

1

1

35