Tanay Jaipuria

@tanayj

Followers

58,685

Following

1,771

Media

1,517

Statuses

11,823

partner @wing_vc . opinions, analysis, and banter on technology and business

New York

Joined October 2008

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

어린이날

• 557030 Tweets

こどもの日

• 530979 Tweets

#HAPPYBAEKHYUNDAY

• 122681 Tweets

#해피큥데이

• 92422 Tweets

GW最終日

• 79113 Tweets

#기다리던_민족대명절_큥탄일

• 71049 Tweets

Al Jazeera

• 67998 Tweets

Vlad

• 54968 Tweets

#HappySkyDay

• 53287 Tweets

Bernard Hill

• 51276 Tweets

Cole Palmer

• 42170 Tweets

سعد اللذيذ

• 35527 Tweets

Theoden

• 26776 Tweets

Gallagher

• 25287 Tweets

Madueke

• 23362 Tweets

Sodoma e Gomorra

• 23121 Tweets

Nicolas Jackson

• 21575 Tweets

#LIVTOT

• 20928 Tweets

D-1 to BLOSSOM

• 20407 Tweets

Happy Cinco de Mayo

• 19169 Tweets

West Ham

• 18158 Tweets

Cucurella

• 15656 Tweets

碧海くん

• 13357 Tweets

LOSE MY BREATH MV TEASER 2

• 12180 Tweets

Rohan

• 11798 Tweets

Anfield

• 11528 Tweets

Pinned Tweet

Twitter: Where brands pretend to be people

Instagram: Where people pretend to be brands

83

3K

7K

Duolingo making a dating show was not on my 2023 bingo card

397

4K

36K

How Tesla caught the employee who was leaking confidential information to the press in 2008.

Really clever

335

3K

28K

Just realized that a $1b breakup fee from Musk (were Twitter to get it) would represent more in net income for Twitter than it has made in aggregate in its lifetime as a company

218

1K

26K

Top Twitter Shareholders:

1. Elon Musk: 9.2%

2. Vanguard: 8.8%

3. Morgan Stanley: 8.4%

4. Blackrock: 6.5%

467

3K

26K

People are making $70-80K per year selling restaurant reservations in NYC on the secondary market 😯

275

2K

18K

The redditor who started the $GME saga DeepFuckingValue has turned his $50K position into >$22M

286

2K

16K

Google lost $100B of market cap today as its Chatbot Bard made a factual error during its first-ever demo and its AI event fell flat.

Must be the most costly live demo fail of all time

238

1K

14K

The US might have been a leader in 5G had it been easier for one immigrant to stay in the country

373

1K

11K

Streaming subscribers in India:

• Disney+ Hotstar: ~46M

• Amazon Prime Video: ~19M

• Netflix: ~5.5M

369

890

10K

Among us has 500M monthly active users and only 4 employees!

125M users per person working on the game 🤯

79

753

9K

To clarify, this is an April Fools' joke, but maybe they'll reconsider and actually make this show. I know I would watch it 😂

29

208

8K

The Airbnb IPO listing range is $56 to $60 per share.

So once you account for service fees, cleaning fees and accommodation taxes it'll come out to $90 to $100 per share.

60

492

8K

Tim Cook thinking about contract renewal negotiations on the $15B a year Google pays Apple to be the default search engine on iOS

60

238

7K

Starbucks has $1.2B in total unredeemed value on Starbucks cards which is like a 0% loan from customers

It also recognized ~145M (12%) as card breakages, i.e. the value customers aren't expected to redeem

So essentially Starbucks is borrowing money from customers at -12%/yr 🤯

139

2K

7K

The Netflix 'Skip Intro' button is pressed ~136 million times a day, saving people 195 years in cumulative time everyday

97

540

7K

Damn, Onlyfans is doing $300M of EBITDA on $400M of Revenue.

Finally a tech startup doing real software margins 👀

88

480

6K

Microsoft Teams has more than 280M monthly active users now.

Slack has ~40-50M.

614

323

6K

Incredible scenes of Saudi fans celebrating their team’s goal vs Argentina.

One of them took the door off 🤣

143

538

6K

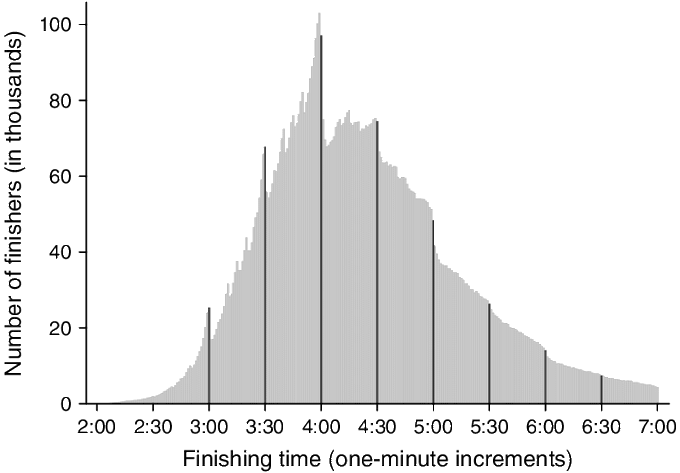

the distribution of marathon finishing times is fascinating

(via )

110

430

5K

Sequoia put in $100M into Zoom in Jan 2017 at $1B valuation.

It's currently trading at a ~$45B market cap, meaning their stake is worth ~$4.3B

That's a 40X in 3 years (>325% IRR). Wild.

62

781

5K

Eric Schmidt when asked in an internal townhall at Google in 2006 whether $1.5B was the right amount to pay for Youtube:

"It absolutely wasn't the right amount. It was either way too high or way too low and I'll tell you in 10 years."

35

331

5K

Calendly got to $70M in ARR on just a $550K seed round. Super impressive!

75

248

4K

Instagram revenue was just disclosed for the first time in court filings.

2018: $11.3B

2019: $17.9B

2020: $22.0B

2021: $32.4B

It makes more in ad revenue than YouTube (and likely at much higher gross margins!)

70

377

4K

Ryan Cohen sold Chewy in 2017 for $3.3B and put all his proceeds into two stocks: Wells Fargo and Apple.

His Apple stake is up 275% (worth $886M) making him the largest individual shareholder.

Late last year he added a $76M stake in Gamestop which is now worth ~$692M (up >800%)

49

350

4K

Crazy that Robinhood is monetizing Reddit better than Reddit

22

168

3K

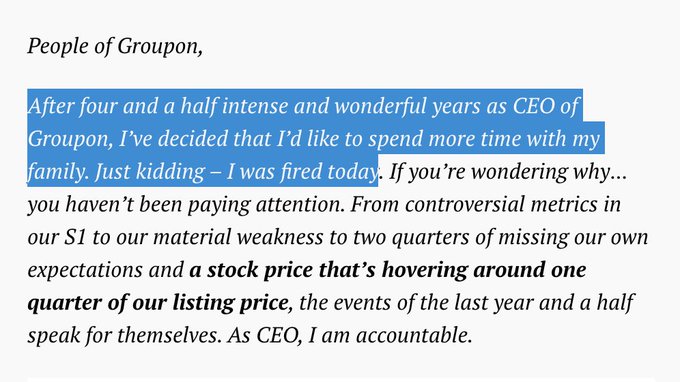

Still one of the best openings to a CEO departure memo (from 2013)

12

286

3K

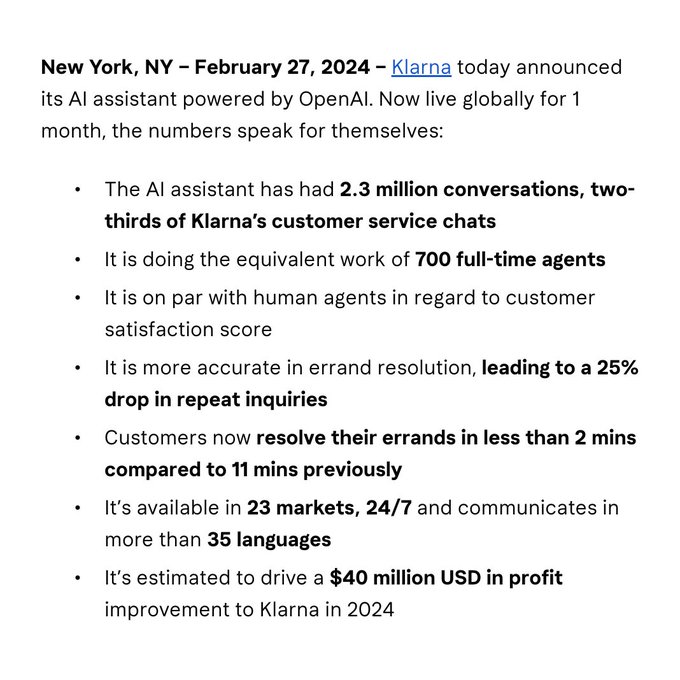

Wow Klarna's AI customer support agent is able to handle 2/3rd of the requests by itself in its first month and is doing the job of an equivalent of 700 agents.

92

477

3K

I'm certain that Airbnb has run A/B tests in which they show users the final prices (including all fees) in search results.

It likely reduced conversions so the growth team had its way and users are left with the misleading prices.

116

104

3K

3 months ago, Zendesk rejected a ~$17B private equity buyout offer because they felt it undervalued the company

Today, it accepted a $10.2B buyout offer by a PE investor group.

Sign of the times

46

215

3K

Cool photo from Freshwork's IPO, which values the company at ~$13B

The first public 'global' Indian SaaS company

16

204

3K

The US Senate has unanimously passed The Sunshine Protection Act, a bill to make daylight saving time permanent across the US.

140

233

3K

AWS still growing 33% at a $79B run rate with 29% margins.

What a business 💯

31

154

3K

Amazon now delivers >65% of its own packages.

For comparison in 2015, it delivered under 3%, and in 2017, under 20%.

43

214

3K

OnlyFans' 2022 financials are bonkers

- $5.6B in GMV (+17% y/y)

- $1.1B in revenue (+17% y/y)

- $525M in pre-tax profit (48% profit margin)

- 3.1M creators on the platform (+47% y/y)

- $338M in dividends paid out to owner

Likely the most successful "creator economy" company

89

309

3K

Take rates for different platforms:

Visa: 0.2%

Shopify: 2.7%

eBay: 10%

Amazon: 15%

Uber Rides: 23%

Lyft: 26%

App Store: 30%

Groupon: 50%

Shutterstock: 72%

52

415

3K

Today I learned Tesla has a $0 advertising budget and has never run a paid TV commercial

76

125

2K

Airbnb should start recommending their hosts add internet speed test screenshots to their listings

52

90

2K

Google paid Apple an estimated ~$10B in 2020 to be the default search engine on iOS 🤑

47

249

2K

Phenomenal video of a 12 year old Lewis Hamilton on his ambitions to become a Formula 1 driver.

He’s incredibly mature and poised for his age

38

450

2K

Meta announced that Reels (across their apps) is now on a $10B revenue run-rate, up 3.3x since last year.

For comparison, TikTok made ~$9.5B last year.

36

143

2K

I was today years old when I learned that Slack is an acronym for Searchable Log of All Communication and Knowledge

32

193

2K

FTX over the last 18 months:

July '21: Raises $900M at $18B

Oct '21: Raises $420.69M at $25B

Jan '22: Raises $400M at $32B

Jul '22: Bails out BlockFi for $250M

Sep '22: Buys Voyager for $1.4B

Nov '22: Acquired by Binance

66

218

2K

Just realized LinkedIn makes more revenue per year than Twitter, Snap and Pinterest combined

76

172

2K

As the saying goes, you either die a startup or live long enough to appoint a desi CEO

25

100

2K

Do you click on ads of companies you don't like so they get charged or are you normal

56

96

2K

Only just found out that Bezos was one of the first shareholders in Google 🤯

He invested $250K for ~1% of the company in 1998 (the year it was founded).

34

339

2K

Just absurd that Google search is a $150B/yr of revenue business still growing at 44% y/y.

The best business ever invented

23

130

2K

The story is fascinating

• founder bought domain for $55K in 2005

• bootstrapped for the first 15 yrs to over $50M/yr in revenue

• big spike with Queen's gambit + COVID (2-5x new users per week compared to normal)

• now a top 250 website globally

22

88

2K

Really hope the English Media don't scapegoat Rashford, Sancho, and Saka.

It takes a lot of courage for 23, 21, and 19 year olds to step up to take a penalty after coming on as substitutes in a Euro Final.

45

221

2K

FTX is a sponsor of the Cricket World Cup.

They removed the logo that used to be on the pitch for the final today 🤣

17

77

2K

Zoom, the company that became a verb during the pandemic, is down 12% since the pandemic started.

In that period:

- Revenue is up ~5x from ~$830M to ~$4.1B

- Operating margins are up from 4% to 28%

70

103

2K

Benchmark owns 11% of Uber which is worth ~$10B.

Just on that one exit, they will return ~26X of their 2011 $425M fund in 8 years which is an IRR of 50%. Wild.

23

249

2K

Tesla lost ~$50B in market cap today (which more than the market cap of the entirety of Twitter) because of a Twitter poll

45

147

2K

this remains one of the best slides ever in an activist investor presentation

23

91

2K

Wow the territory of Anguilla is making ~$3M per month from .ai domains, which is 1/3rd of their total monthly government budget

33

151

2K

Some companies that have market caps less than the total money they have raised:

• Bird ($120M mkt cap vs $1.2B raised)

• Wish ($810M mkt cap vs $2.9B raised)

• WeWork ($2.8B mkt cap vs $16.2B raised)

• Lyft ($5.1B mkt cap vs $7.3B raised)

53

173

2K

Some stats on Honey, which Paypal just acquired for $4B:

• Saved $1B for users this year

• Currently at $100M in revenue growing >100% y/y and profitable

• Works with 30K merchants and has 17M MAU (valuing it at roughly ~$230/user)

• Only raised ~$40M prior to acquisition

27

243

2K

Digital orders as a percent of sales

• McDonalds: ~20%

• Starbucks: ~25%

• Chipotle: ~50%

• Domino's: ~75%

47

168

2K

AWS still growing at 40% y/y at a $71B run rate. What an incredible business.

24

85

2K

The role the film The Social Network played in the rise of startups is underrated

45

119

2K

OH: A DAO is an organisation run on Discord instead of Slack

21

104

2K

Mailchimp went from $0 to $800M in revenue and a $12B valuation at acquisition with no outside funding.

Believe it is the first bootstrapped decacorn exit in tech.

22

178

2K

Meta makes $207 per year per user in the US and Canada, without charging them anything.

That's more than what many subscription products (Netflix, Spotify, etc) make from their paid users

31

114

2K

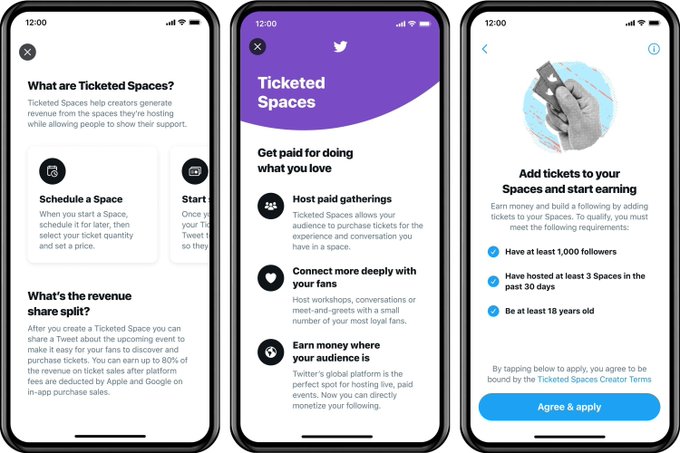

Twitter launching "Ticketed Spaces" soon, with the following revenue split:

• Creator: 56%

• Apple/Google: 30%

• Twitter: 14%

52

314

1K

Interesting how much Stripe and Adyen diverge in terms of profitability and opex.

Net revenue per employee

Adyen: $417K

Stripe: $403K

EBITDA per employee

Adyen: $237K

Stripe: negative

34

107

1K

The Chapwood index is really interesting.

Suggests that the true cost of living in America has been going up ~10-12% per year, rather than ~2% as implied by CPI.

85

283

1K

Since Parag took over Twitter 11 months ago, Twitter's stock is up 22% while the S&P is down 16%.

He'll also reportedly receive a severance of ~$42M.

Job well done I guess🤷♂️

30

90

1K

Netflix makes ~$190/yr from every paying subscriber in North America

Meta makes ~$206/yr from every (free) active user in North Ameria

35

120

1K

Wow, Klarna raising a new round at a $6.5B valuation, 85% lower than their round at $45.6B last June.

For comparison, Affirm is down ~75% in that period.

42

120

1K

American remote workers when they realize they'll have to compete against global talent willing to work for a quarter of the compensation

37

153

1K

This slide in Uber's first pitch deck always gets me.

TAM = $4.2B

Uber's bookings in 2020 = $58B

16

142

1K

For those interested in reading more about the technique, known as the Canary trap, check this out:

14

137

1K

Toast now makes 84% of its revenue from fintech solutions compared to 12% from subscriptions.

Similarly, Shopify makes 73% of its revenue from fintech solutions compared to 27% from subscriptions (+ app marketplace)

42

110

1K

amazing how Jack decided to use his free time (from no longer being ceo of Twitter) to shitpost on Twitter like the rest of us

23

64

1K

Some notes on Adobe's acquisition of Figma

Figma financials:

• $400M in ARR in 2022 growing ~100% y/y

• >150% net dollar retention

• >90% gross margins

• positive operating cash flows

23

104

1K

Duolingo just filed to go public. Some notes:

• $161M in revenue (75% subscriptions, 25% virtual goods and ads) which grew 129% y/y in 2020

• 72% gross margins, 9% fcf margins

• ~40M MAUs of which 4.5% are paid subs

• Make avg of $90/yr per sub or $5/yr per user in aggregate

17

123

1K

The co-founder of Asana, Dustin Moskovitz, has bought over $1B worth of Asana stock on the open market over the last year.

Might be the most high-conviction insider buying by an executive ever.

35

36

1K

When Lyft went public, it was spending $350M/yr on payment processing fees, a full 16% of their revenue.

Similar with Uber which was spending $750M/yr or 10% of their revenue in 2017.

Crazy how expensive payments can sometimes get for marketplaces

55

80

1K

Not every day you see an S-1 for a company planning to go public at an ~$80B valuation without the revenue line item in the financials

67

139

1K

Amazon's ads business is bigger than YouTube and growing faster.

- Youtube: $7.3B (+5% y/y)

- Amazon: $8.8B (+18% y/y)

24

102

1K

RXBar took on no outside money and sold to Kellogg for $600M.

The founder was discussing his plans to raise money when starting out, and his father told him: "You need to shut up and sell 1,000 bars"

14

181

1K

Microsoft's market cap has grown (an average of) ~$805M per day since Satya Nadella became CEO in 2014.

INSANE fact of the day: Apple's market cap has grown $700m PER DAY since Tim Cook became CEO in 2011.

122

355

5K

22

88

1K

Kind of crazy that Twilio which does ~$3.4B in revenue a year growing ~40% y/y with 125% NDR only has an enterprise value of ~$9B.

The market currently values it at less than 3x revenue.

75

46

1K

Amazon's ads business made $31.2B in revenue in 2021 growing at 32%.

It's bigger than YouTube's ads business (~$29B) 😯

24

111

1K

Uber was valued at $68B in private markets in August 2016.

5.5 years later, its market cap is still essentially the same (~$69B)

59

91

1K

Alibaba now under its IPO price over 7.5 years ago.

In that period:

• Revenue is up ~12x from ~$10B to ~$120B

• Operating income is up ~3x from $5B to ~$14B

57

120

1K

Spotify wrapped going viral every year makes me wonder why they don't invest even more in social features.

People clearly want to share and discover music from friends throughout the year

59

47

1K

It's really amazing how Google Docs takes me to the wrong account between the two that I want to use 99% of the time

37

35

1K