Jared

@jaredhstocks

Followers

12,654

Following

139

Media

541

Statuses

3,009

Explore trending content on Musk Viewer

#LCDLF4

• 254445 Tweets

Renzo

• 149067 Tweets

Costello

• 114398 Tweets

Romeh

• 72945 Tweets

#WWERaw

• 70030 Tweets

SAROCHA REBECCA ON RED CARPET

• 64909 Tweets

Maripily

• 50376 Tweets

Lupillo

• 50217 Tweets

FELIX ENAMORA A BARCELONA

• 35647 Tweets

BLINDAJE FURIOSO

• 32592 Tweets

#ฤดูฝนนี้ไทยทึเมมีน้องสมบัติ

• 31376 Tweets

STRAY KIDS HITS HOT100

• 28518 Tweets

Scarlett Johansson

• 27715 Tweets

MADAME FIGARO X GULF

• 24290 Tweets

定額減税

• 21934 Tweets

Kingdom Hearts

• 20666 Tweets

Fani Willis

• 20358 Tweets

梅雨入り

• 20227 Tweets

Birds Nurturing

• 17701 Tweets

給与明細

• 14249 Tweets

#Canucks

• 13449 Tweets

Gunther

• 13056 Tweets

金額明記

• 12279 Tweets

Amber Rose

• 11949 Tweets

Lyra

• 11807 Tweets

#ゴンチャの新作

• 11136 Tweets

Keys For Healthy Life

• 11002 Tweets

Otis

• 10003 Tweets

Pinned Tweet

1/ Selling “penny puts” in the $SPX complex has become commonplace in today’s markets, it’s essentially now a socially acceptable practice amongst portfolio managers. This is the story of James Cordier from Optionsellers, a fund that blew up and the infamous $150M margin call.

44

195

1K

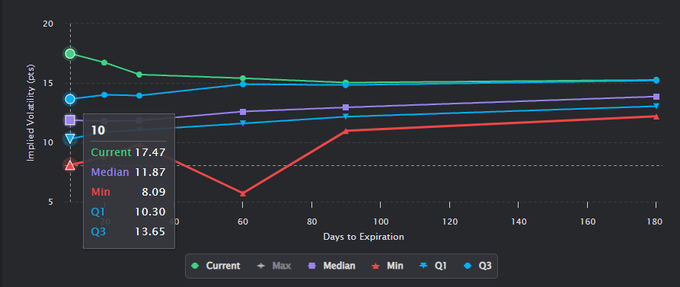

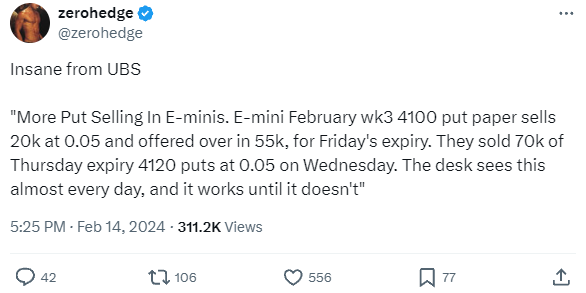

Welcome to the highest skew reading since October 24th with implied vols now above the 3rd quartile in the $SPX complex. This goes to show what I've been pounding the table on for quite some time now, own vol don't sell it.

This $VIX expiration tomorrow AM is an important

31

82

523

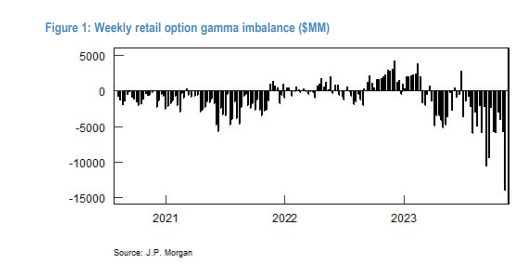

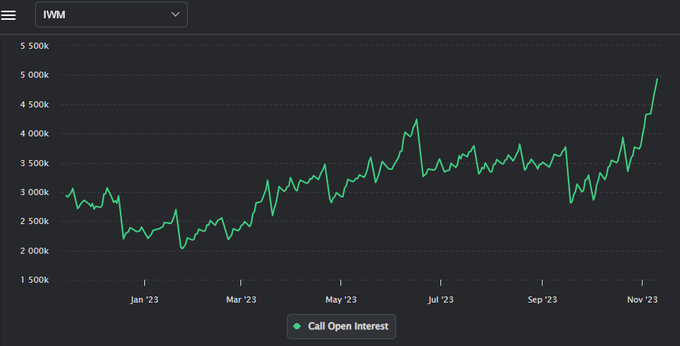

1/ $SPX This past week saw the most extreme retail gamma imbalance (-$14B) in history.

$IWM recorded the highest ever call OI on record.

With OPEX this week, participants will look to monetize delta-positive positions.

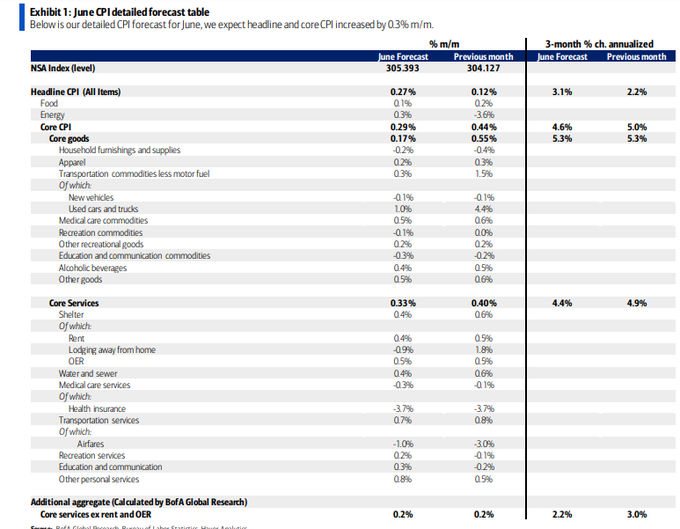

Is Santa at risk of bringing coal with CPI/PPI?

26

85

504

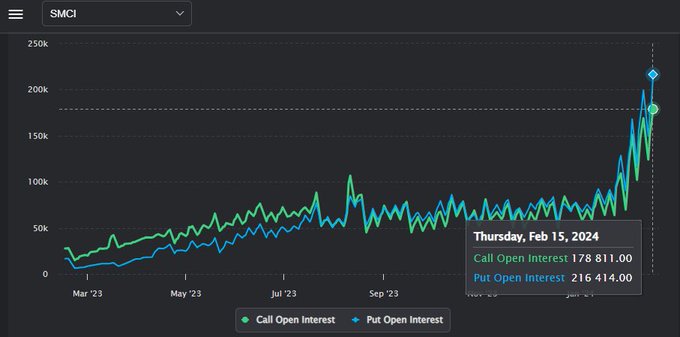

$SMCI Made history today with the most options ever traded. The majority of it being calls. Open interest continues to favor puts with a 1.2 put to call ratio. Is there room higher for the stock?

The vol structure currently found in $SMCI reminds me of the 2021 $GME days.

50

97

506

$AAPL and $QQQ had the highest ever call volume on record last week. The market internals are flashing warning signs.

23

75

493

@Barchart

For those that don’t know, Ruffer returned 16% in the 2008 crash, nailed the 2015 flash crash, nailed the 2018 XIV (Volmaggedon) implosion, and nailed the 2020 COVID crash making $2.2B. They have a very accurate and long track record of these bets.

27

48

430

1/ As someone who trades index vol on a daily basis, every time a large $VIX call order comes in, it draws a lot of attention from less sophisticated investors who believe Volmaggedon 2.0 is here.

TL;DR ignore the noise… For now.

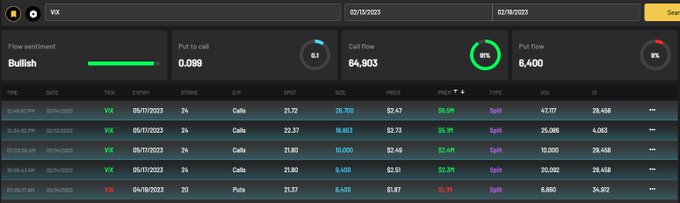

🔸 A trader bought about 250,000 call contracts on the VIX Index with a strike price of 17 that expire on Feb. 14. The trader spent about $16.7 million in premium, with each contract costing between roughly $0.63 and $0.67. The VIX hasn’t traded above the 17 level since early

172

226

1K

13

45

347

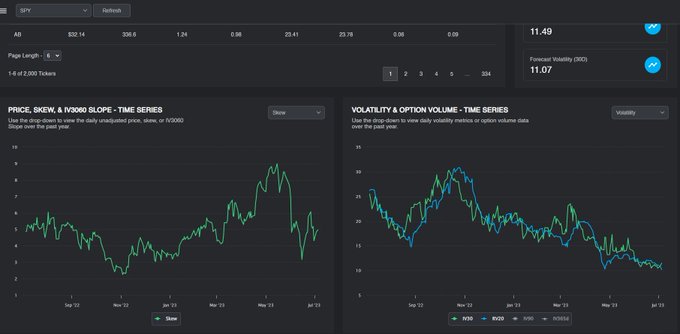

$SPY Welcome to the lowest realized volatility since January 28th, 2022. Is the market discounting current risks? Let's dive in.

1/

26

62

339

$SPX Is it finally time for a deeper pullback?

Essentially since November, I’ve had zero interest in playing any sort of SPX downside. I've discussed the possibility in this quoted tweet but have refrained from an entry, until now. I’ve mainly been sitting long VX to play the

As we approach the $SPX targets mentioned above, I thought I would throw out my comments from this AM. I hope everyone has a fantastic weekend! Cheers🍻

10

1

68

46

45

343

Market participants have a clear consensus that PCE data will arrive "hot" tomorrow. What if it doesn't?

The hotter than expected CPI/PPI is well telegraphed, and it's no secret that PCE is the FED's "preferred" inflation gauge. There has been a recent history of the market

45

45

300

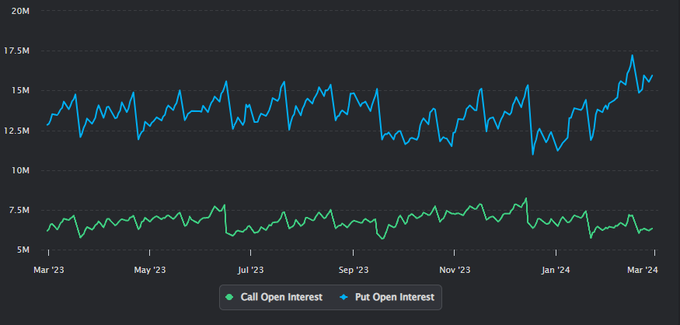

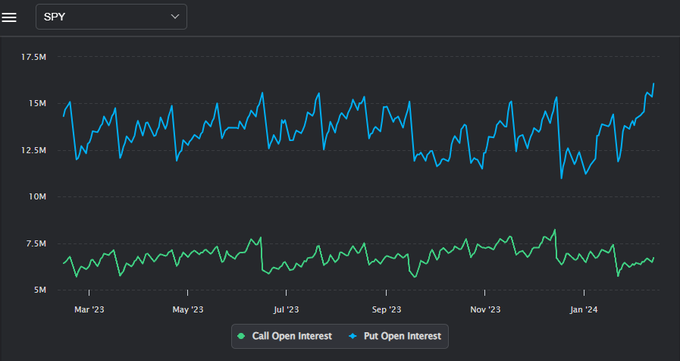

After CPI, $SPY now has one of the highest put open interest in history! 16 million contracts.

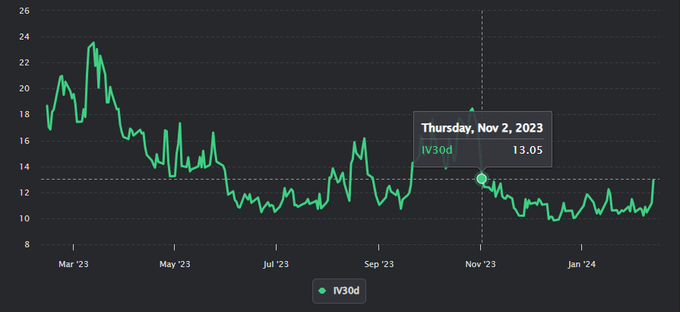

30 Day Implied Volatility is now at a 3 month high, dating back to November 2nd, 2023.

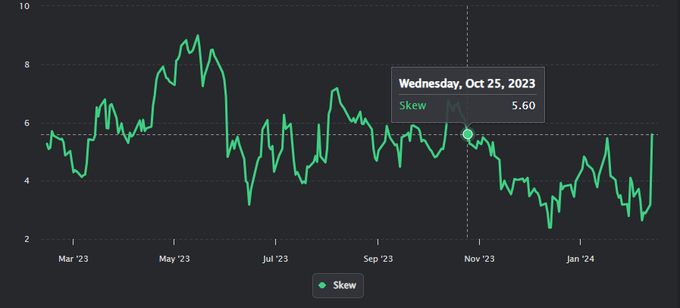

Skew just recorded its highest reading since October 25th, 2023.

33

46

263

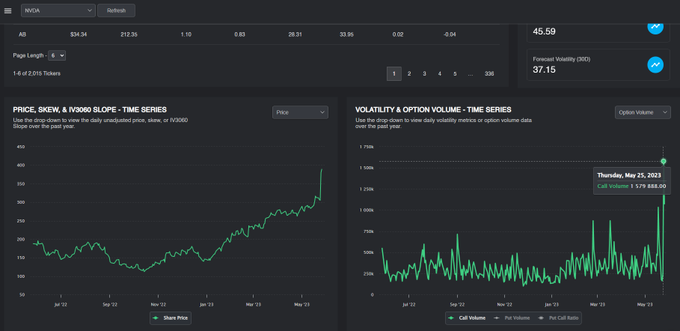

1/ $NVDA The next "meme" stock?

Up 247% from it's October bottom. 1.6 Million calls traded on May 25th, the highest call volume in 2 years.

How does it compare to the peak of GameStop's gamma squeeze?

How can we use the $GME saga to form a trade on $NVDA?

Lets dive in!

27

43

206

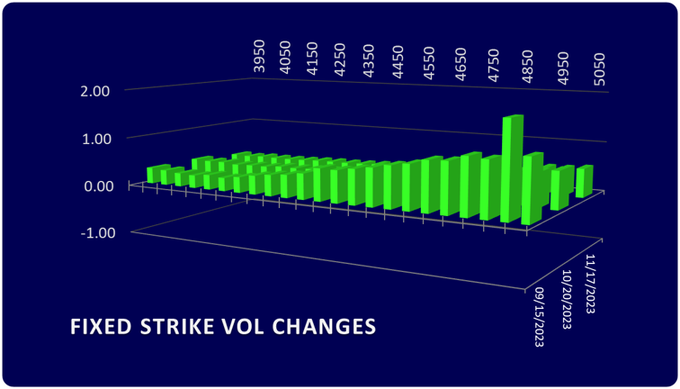

$SPX at the close:

Fixed Strike vol on Puts down 1-1.51%, Calls up 0.50-0.97%.

Despite the narratives, participants aren’t reaching for downside protection on this selloff, evident in $COR90D, calls stay bid.

Skew has yet to see an uptick since 10/17.

6 point vol risk premium.

27

29

182

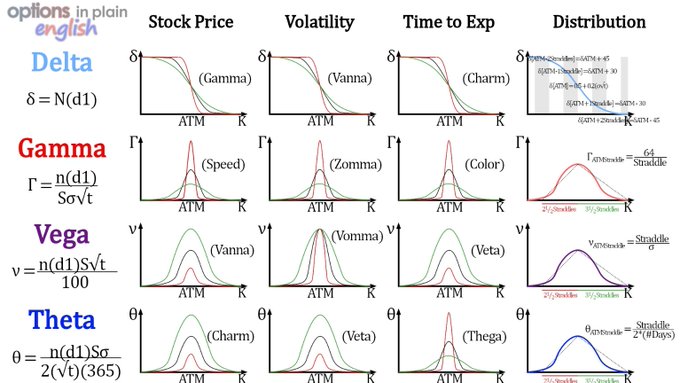

5/ Allow me to introduce you to the option greeks through the lens of a short call holder.

Delta: When you're short a call you hold negative delta which means that for every 1 point change in the spot price higher, the option price would lose that amount.

Gamma: In simple

1

17

172

Happy Monday, I hope everyone has a fantastic week!

For those wondering, yes, I still see this playing out. Holiday shortened week with less liquidity as most firms are either on Spring break or early Easter. This simply means that the path of least resistance is flat to up but

17

14

167

1/ The lackluster reaction from vol markets while $SPX has sold off 250 points in 2 weeks is rather concerning for a bear case.

Skew and fixed strike vol are both either flat or down. 1M RVol sits at 11 with $VIX at 18.

These speak to the monetization of hedges on the way down.

14

20

149

1/ I think this is an extremely important issue/example that needs to be drilled home, and what I believe sparks the next major tail event. While it’s “funny” to us, it shows the lengths as to what current PMs go through to try and generate a fraction of Alpha in today’s markets.

Sell a cab, drive a cab

Brutal start to '24 for this short SPX 0DTE manager

...what advantage could there be to selling spreads like this at 0.10-0.15?

risking 125-1 losses..

when there are much more attractive, premium-intensive structures upon which to build your approach?

11

8

95

9

28

143

$SPX This move should come as no surprise to anyone, every warning sign was given. Vol has been reset, so natural buyers will need to support higher. If you didn't catch the bottom, DON'T FOMO here, at most 50SMA. Wait for the pullback next week (4220-4240) to confirm this move.

$SPX at the close:

Fixed Strike vol on Puts down 1-1.51%, Calls up 0.50-0.97%.

Despite the narratives, participants aren’t reaching for downside protection on this selloff, evident in $COR90D, calls stay bid.

Skew has yet to see an uptick since 10/17.

6 point vol risk premium.

27

29

182

14

18

151

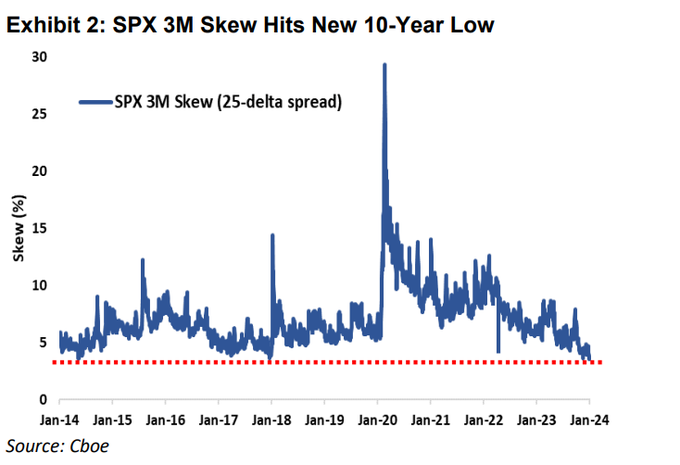

$SPX Skew just hit a new decade-long low, dating back to 2014 when the iPhone 6 was released!! Meanwhile, the 25D vs 50D call wing rose to a 10 year high as well.

The 3M 25 delta skew measures the Implied volatility of 3 month 25D puts vs 25D calls. CBOE points out that this

17

32

148

What a wild ride to $SPX 4750! As we look ahead into 2024... history often rhymes. 1970 (2020) and 1974 (2024) where equities made ATH before crashing to 10Yr lows. Arthur Burns cut/raised 2 times that year with the economy already in a recession by mid-1973. Will history repeat?

11/ To put a ribbon on this thread, either the market retakes the 50d first or I'm bid for March '24 calls between 419.53-420.63. I don't believe we are done with $SPX 4600 (Even 4750) as outlined here:

3

0

30

7

16

146

As we hit the 50d, I monetized my short $SPX position along with some VX as this was my first major target. That doesn’t mean we don’t have immediate room lower, just that skinny pigs get fat and fat pigs get slaughtered. I’ll be looking for a re-entry very soon once the VRP

15

8

144

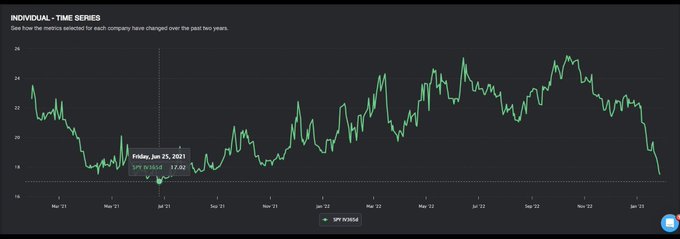

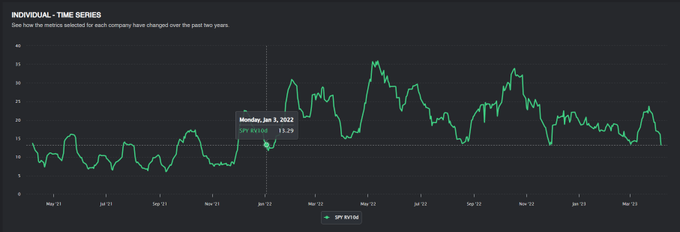

This is an IV365 chart of $SPY options contracts. We are trading at levels not seen since the 2021 bull market.

9

39

142

1/ Weekend Research Thread:

Structured Product Issuance

Dispersion Trading PnL during Election Years

Retail & Institutional Trading Activity (Week of 2/9)

Implied Correlations & $VIX Distributions (why vol has decayed since Jan).

Short $SPX Long $RTY Variance?

2

19

136

9/END

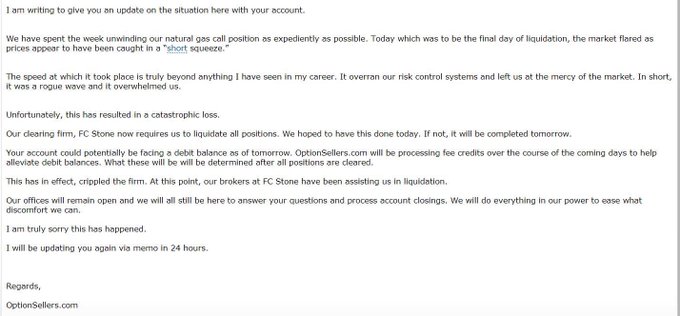

In the aftermath of the Optionseller’s blowup, James famously made this apology video ().

Mr. Cordier now runs a commodity investment advisory site and has a YouTube channel which I’ll leave a link to both in the sources. This would be like if

25

3

135

1/ Apologies for the lack of posts recently. My thoughts have not changed from this thread, which is still on track.

For now, here are a few things I am watching and why I am NOT short.

7

20

131

“The call and put options sold will have no more than 200% notional value of the funds net asset value.”

Okay so let’s leverage up 2x on 1DTE OTM strangles with realized in single digits and 4 years since the last major vol spike. It can’t go tits up right?

Dealers still need

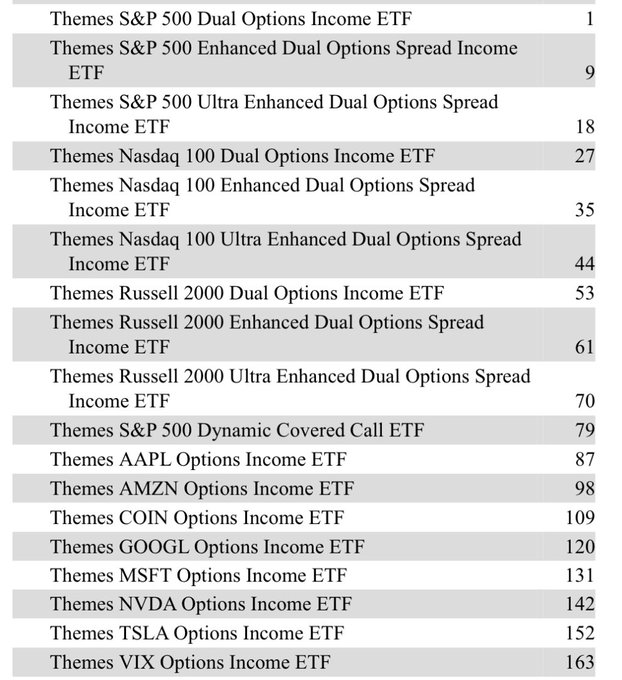

New filing for a slew of duel options spread income ETFs along w a dose of single stock covered call ETFs

50

50

299

15

31

122

8/ So how does the Optionseller story relate to $SPX “penny puts”? Well, as of late, we have seen a dramatic uptick in funds selling DOTM puts for 0.05 a piece like this example below. Why might they do this? Low correlations in a low volatility envrionement. The maximum profit

8

11

121

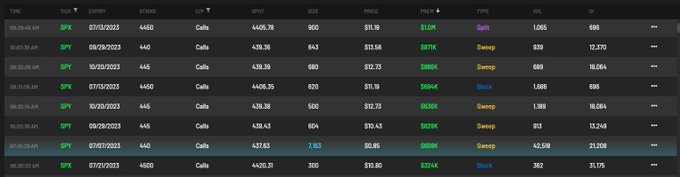

$SPY So far 420.89 has marked it. $9M in $VIX calls (100,000 lot) and a $16M $SPX put nearly 500 points OTM with 6/16 expiry came in today. With the OPEX narrative gaining traction, it doesn't hurt to hedge the weekend news through Tuesday. The outcome here remains the same.

12

12

118

25/ With the upcoming CPI report 7/12, I believe this is the catalyst to break a 4 week consolidation and when the market will mass capitulate into the upside. I am looking for the first $SPY target of 453 and the ultimate target of 464-468 which I’ll pinpoint at a later date.

7

9

116

1/ The Week Ahead: Expect Volatility

Central Bank Meetings- FOMC, ECB, BOJ.

Economic Data- GDP, PCE, Consumer, PMI, Jobs.

Earnings- $MSFT, $GOOGL, $META.

A look into Index Volatility: $SPY, $QQQ, $DIA, $IWM

5

18

108

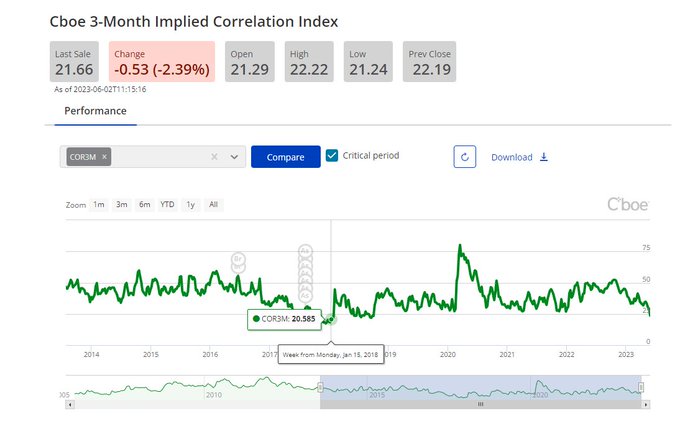

$SPY Vol risk premium gap closed. Skew back to March. Options at min IV and back in steep contango.

$COR3M Correlation at the lowest level since Volmageddon.

$COR90D (Crash risk) back to pre-banking crisis levels.

Tread carefully, full thread this weekend! 🎯

13/ Failure here sounds a major alarm. This means that the market will be supported into June (refer to my last thread for those details) until the debt ceiling passes. Hence, why it's important to ALWAYS hedge! This means 6/5-6/7 is the next target date.

4

1

29

6

11

106

1/ A recent study showed a whopping 41% of users say X can impact investment decisions.

You would think the world is ending with the mass influx of recently negative sentiment & IV at 3 month highs, yet $SPX realized volatility continues lower and is -1.5% from all time highs.

12

12

106

$SPX up, vol up 🛑

$COR90D +1.63%

with the big move up, big chase for upside, this is $SPX dec 4500 call volatility, stocks up + vol up

1

4

26

10

7

109

$SPY bulls remain relentless before the long weekend. Let's check in on the market internals, review last week, and see what's ahead to understand the risks associated behind the curtain.

8

34

104

1/ Roulette, "an unbeatable game unless someone steals money from the table when the croupier isn't looking." -Albert Einstein.

That is until Niko Tosa, a gambler who did the impossible.

How we can use the story of Tosa to beat the Stock Market?

14

25

107

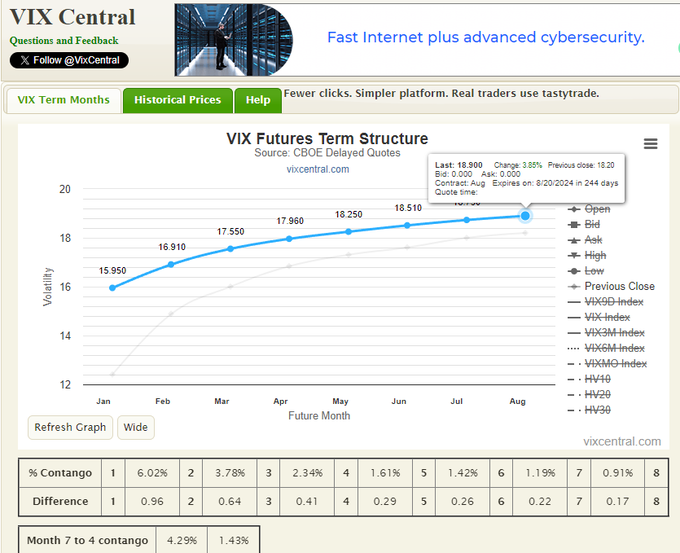

1/ No coincidence on the vol bid post VIX opex. The last 5TD has seen VX complex higher, especially 12/18, providing a warning with FSV. $VIX TS front month +27%, even back month is +3.8%. $TDEX +22%, $COR90D +11%, $VIX1D up a staggering 65%. Be very careful "IF" this continues.

If you’re trying to take a shot here, let AM OPEX settle and follow lunchtime into next week. Let under the hood confirm first before a tactical approach for mean reversion to the +2StdDev and +1.5StdDev (20SMA).

3

1

26

5

15

105

$SPY Exact same scenario. Millions worth of 0DTE call buying before Bostic talked + put selling. 459K 393p traded today. Dealers bought back those shares while further call buying fueled the gamma squeeze. All off of one word from a non-voting member. "Summer pause." 1/9

For those wondering why the market is not accelerating to the downside despite the abysmal econ data. $SPY Put selling+0DTE Call buying=Supportive market flows. Until they close out positions or flip to puts, we are stuck. Do they want to hold risk over the long weekend?

4

9

50

15

17

100

58/ This thread serves as the placeholder until I am ready to release the one that reaffirms my SPX 2500-2750 price target. I have given everything you need for now with clear invalidation points. Trade safe and stay diligent. Cheers!

15

3

100

For the sake of transparency and so nobody thinks I'm just talking my book, I sold out of my $SPX long position today at 5165 for just about a +100% gain. This brings my Q1 performance to one of the best on record. I continue to remain in a VX June position to play the spot/vol

8

3

102

$SPX I’m short (-delta) with slightly long vega exposure from the close. 🚩Read thread below for warning, FSV holding in/VRP gap. The rising 20SMA is the target.🐻 are on the shot clock here until EOM/BOM rebal takes place. Have a fantastic thxgiving-spread kindness! Cheers🍻

1/ $SPX This past week saw the most extreme retail gamma imbalance (-$14B) in history.

$IWM recorded the highest ever call OI on record.

With OPEX this week, participants will look to monetize delta-positive positions.

Is Santa at risk of bringing coal with CPI/PPI?

26

85

504

12

9

102

2/ Before we dive into how selling $SPX penny puts and Optionsellers is connected, it’s important to begin with the story of Cordier’s fund and career.

James began his career at Heinold Commodities in Milwaukee as a broker in 1984. After establishing a good reputation in the

3

4

99

1/ Clear warning was given yesterday as vol markets did not agree with the price action. That move is being realized today. With NFP tomorrow, the only point that matters is the 20SMA. Time may catch up to price once again like on 6/26. If this happens... a massive Vanna squeeze.

@RJRCapital

There is clearly some fear under the hood today that's not agreeing with this price action. 10D/30D OTM puts are both at the same level.

1

3

26

4

17

98

@RJRCapital

@Jedi_ant

@neildecrypt

I’m positioned as short as I’ve ever been in my entire career. I even added more today. IMO this will turn out to be the greatest bull trap in market history.

12

10

94

END/ These will be your tell-tell signs to get in for a possible tail event. Of course there’s more to it, but I’m trying to make it as simple as possible for you guys to understand.

For now… Ignore the noise.

8

3

96

1/ Pay attention to what's going on under the hood.

$VIX Dealers tried to suppress Vol into OPEX this AM.

RV has moved slightly higher; forcing Vol control to sell, but there is still a variance risk premium present.

This selloff has some of the same fingerprints as June.

Yesterday we finally saw a move up in fixed strike vol on SPX as we broke below the 50d MA. Has something changed or will vol supply come back into the end of the week?

3

3

32

9

21

93

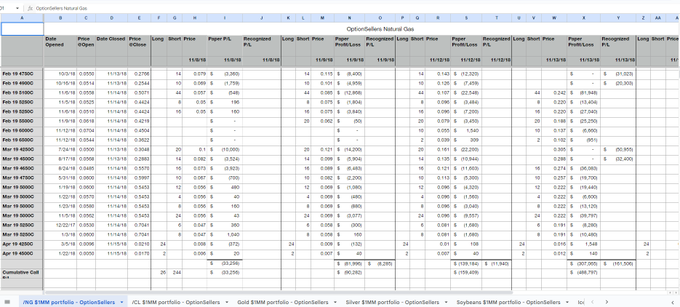

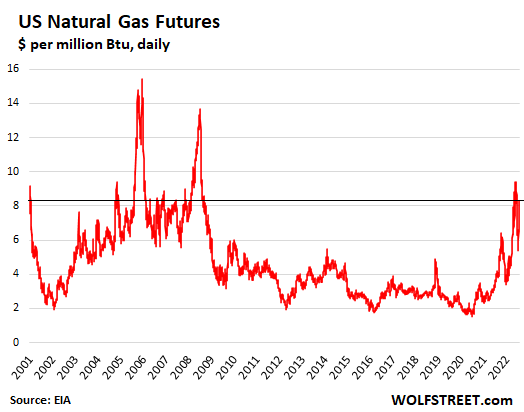

4/ This exact philosophy of high leverage trades is what’s going to cause the ultimate blowup of his fund, but how did it happen?

In the fall of 2018, the BLS reported that Natural Gas storage supply hit a 16 year low. Fast forward to November 14th, 2018 and warnings of a cold

1

6

95

25/END I will update throughout the week as this thread serves as a cautionary tale. Watch fixed strike vol extremely closely here. As always, remember to hedge your positions and follow strict risk management, this week especially. Trade safe & stay diligent. Cheers!

11

3

93

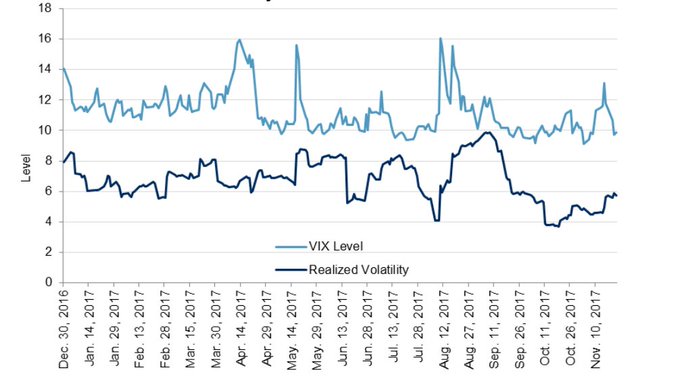

Even with $VIX now at 11, there is still room lower if $SPX continues to make ~0.70% daily moves. 1M RV has crashed to an 8 handle. It's important to remember that a low $VIX doesn't mean cheap. Before Volmaggedon in 2018, 1M RV floated around 4 and stayed under 10 for 14 months!

31/ The only guarantee I can give you in the markets is that all $VIX gaps will fill. The last one to fill is at 12.10, which could serve as the final bottom. Long vol buyers remember, "the market can stay rational longer than you can stay solvent."

4

12

92

5

11

92

31/ The only guarantee I can give you in the markets is that all $VIX gaps will fill. The last one to fill is at 12.10, which could serve as the final bottom. Long vol buyers remember, "the market can stay rational longer than you can stay solvent."

$VIX gaps fill 100% of times.

February 2020 gap filled today.

January 2020 gap at $12.10 left to fill.

Top gap at $45.41 from April 2020 still unfilled.

$VIX $SPX

14

23

115

4

12

92

1/ Weekend Research:

Retail Trading Data

$SPY Volatility

Dispersion Trading Insight/PnL

Institutional Orders/Volume

$DAL Mean Reversion Trade?

Notable Tweets

6

18

92

Did anybody notice the 5146 target and where we bottomed yesterday?

Fixed vols carried very well today and downside reach remains bid. May VX holding 50 cents of roll and $VIX just had its highest weekly close dating back to 10/27/23. This doesn’t scream panic mode but it

15

6

90

3/ Optionsellers as the name implies, specialized in selling options, mainly deep out-of-the-money options. Assuming you already have basic knowledge of what an option is, why would James only sell DOTM (deep out of the money) calls and puts? Four words. Leverage to the tits!

5

3

89

Sell Oct/Buy Dec✅

I’ll say this over and over again. Volatility needs a reason to stay elevated, $SPX does not.

Today: Bonds green, Yields down, DXY red, $VIX 0.50%, correlations lower, fixed strike vol lower.

$SPX Down almost 1%. I buy when folks are scared of weekend risk.

1/ The lackluster reaction from vol markets while $SPX has sold off 250 points in 2 weeks is rather concerning for a bear case.

Skew and fixed strike vol are both either flat or down. 1M RVol sits at 11 with $VIX at 18.

These speak to the monetization of hedges on the way down.

14

20

149

7

14

88

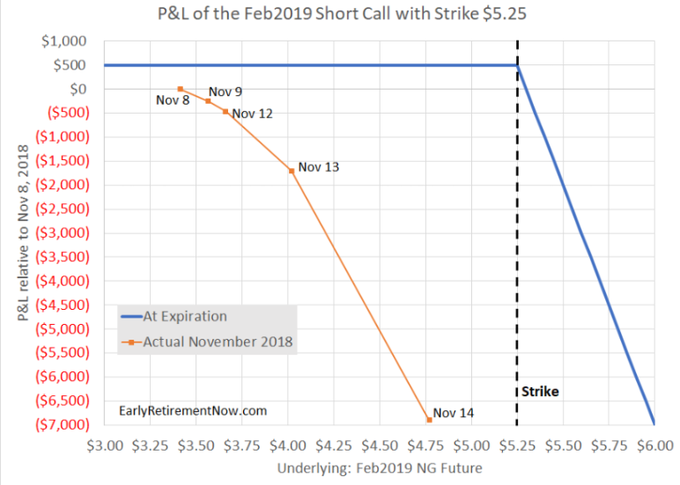

6/ Now that you understand the option greeks at play, let’s look at the short call position the Twitter user was actually in day by day.

The chart below is the option PnL of one Feb 2019 5.25c:

On November 5th, 2018, James sold to open the 5.25c for 0.05 a piece for a net

2

4

88

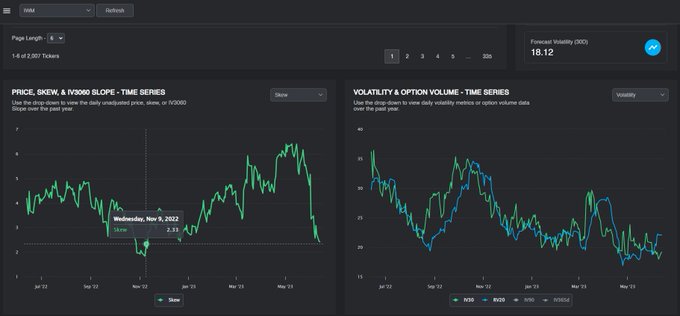

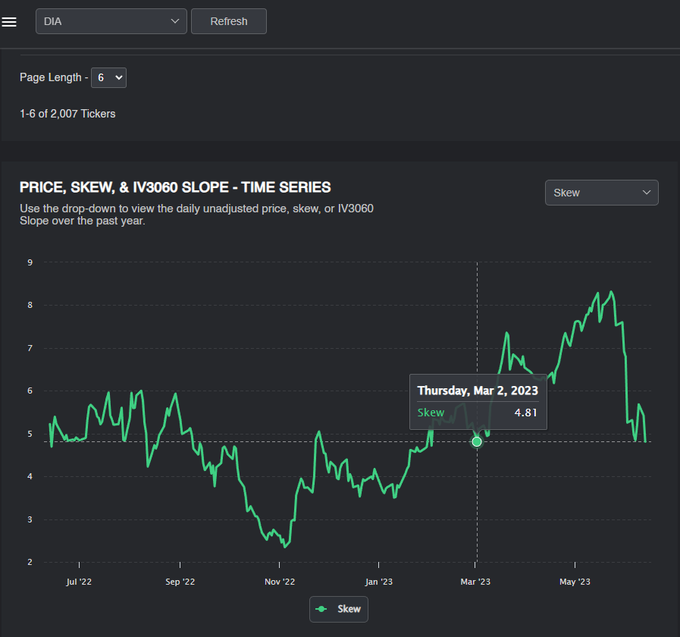

1/ $SPY Skew has now flushed out March banking crisis levels.

$QQQ Skew back to Jan 9th.

$IWM Skew now at Nov 2022 and a massive vol risk premium present.

$DIA Skew also has flushed out to March levels.

The market is pricing perfection for FOMC. Trust data not narratives🎯

19/

2016-2018 Vol Suppression=

2018 Volmeggadon

2018-2020 Vol Suppression AGAIN=

2020 Covid Crash

2020-2023 Vol Suppression AGAIN and AGAIN=

????

It's only a matter of time⏲️

2

3

31

7

12

83

Instead of making a separate post since it's the weekend, I thought I would throw some Saturday research into this thread. Nothing revolutionary but rather interesting data from sell-side desks. I hope everyone has a great Easter weekend! 🍻

These 4 charts are from the technical

3

10

86

1/ $SPY I have been adamant on waiting for a backtest before longing this market, which was reinforced in the screenshot below (give it a read). I believe we get a Vanna bid but there is ZERO reason to believe so until mid 443s confirms support.

Small update before the weekend:

$SPY Big day tomorrow with NFP. After JOLTS #, bad news is still good news. Skew has been reset back to July 31st. Realized vol>implied/forward vol. Option premium is now in the 12%ile. <10DTE puts are bid. A healthy backtest to the 50d soon ($446) would solidify this bull move.

7

5

58

6

12

79

1/ $SPY The market is down -1.5% and Skew is moving lower with fixed strike vol up a measly 1%. IV30 is at 19% but RVol is still at 11. We now have the 2nd largest Vol risk premium of the year. The market is hedged and is monetizing as we move lower.

1/ The lackluster reaction from vol markets while $SPX has sold off 250 points in 2 weeks is rather concerning for a bear case.

Skew and fixed strike vol are both either flat or down. 1M RVol sits at 11 with $VIX at 18.

These speak to the monetization of hedges on the way down.

14

20

149

4

7

80

1/ Humbly speaking: Called the top at $SPY 459.

FOMC plan in the quoted thread was exactly on point.

Gave a clear warning regarding BOJ.

Called the vol unwind squeeze (index higher) for this week.

Now what?

1/ The Week Ahead: Expect Volatility

Central Bank Meetings- FOMC, ECB, BOJ.

Economic Data- GDP, PCE, Consumer, PMI, Jobs.

Earnings- $MSFT, $GOOGL, $META.

A look into Index Volatility: $SPY, $QQQ, $DIA, $IWM

5

18

108

11

5

80

1/ It's approaching do or die time for equity bears. Given the Vol crush today, you gotta take your shot next week.

10

10

79

If you made it this far and leave this thread with anything, this picture sums it all up.

31/

Narrator: the S&P 500 bull walking the “3950” line entirely unaware what lies beneath

$SPY $SPX

3

12

68

3

1

75

9/ “Okay Jared, what if some systematically shocking news happens, how are we supposed to know something larger is brewing?”

Look for shorter dated tenors explode in convexity. 1 Wk/M VIX calls moving from 0.02 to 0.30 or SPX 1 delta puts moving 500% etc. I talked about it here:

1/ No coincidence on the vol bid post VIX opex. The last 5TD has seen VX complex higher, especially 12/18, providing a warning with FSV. $VIX TS front month +27%, even back month is +3.8%. $TDEX +22%, $COR90D +11%, $VIX1D up a staggering 65%. Be very careful "IF" this continues.

5

15

105

3

5

75

1/ With $SPY skew at new 1YR highs today and the $VIX up 15%, volatility is finally back into the markets. But with a 24% IV for an ATM straddle, are the current risks being underpriced, or will the bulls finally reach 4200?

Here is how to prepare for FOMC/ $AAPL and beyond.

6

16

75

4/ Powell essentially leaked Core PCE today. 4.3% vs 4.2% expected. Looks like the disinflation narrative is coming to an end. Be smart and hedge your trades, next week is crucial! Sitting out is also a position.

Have a great weekend! I will have a more detailed thread soon🍻

6

2

76

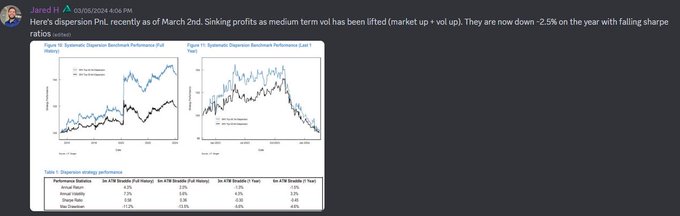

With the new Fed Dot Plot, structured products are significantly less appealing. Why settle for the once great 10% when $SPX is +23% on the year? Liquidation thereof causes the infamous market up+ vol up. Combined with the dispersion trade, this is why vol was suppressed.

@Mystral2042

@MrStudPuffin

TA points towards 4700+ after digestion. I have a near 95% probability we see SPY 464-468 before it’s truly done. Macro wise, BOJ is the black swan IMO + when the fed cuts, yield stacking products and the dispersion trade will be over. Only issue is that we looking at Q1-Q2 ‘24.

4

1

11

3

12

75

7/ In the equity derivative world, puts are more expensive than calls because of what’s known as skew. The risk is always that stocks will crash but the most likely move is higher, so option prices reflect this. You might have heard the saying “Up like an escalator, down like an

3

6

75

8/ Lastly, I will have the long overdue thread explaining my thoughts for July and beyond hopefully by this weekend. I have put nearly 3 weeks and a ton of effort into making it the best I possibly can so stay tuned. Trade safe, stay diligent, and remember to hedge!

4

0

74

1/ It's June Opex. Time for a small update on the markets & my own account.

1/ $SPY Skew has now flushed out March banking crisis levels.

$QQQ Skew back to Jan 9th.

$IWM Skew now at Nov 2022 and a massive vol risk premium present.

$DIA Skew also has flushed out to March levels.

The market is pricing perfection for FOMC. Trust data not narratives🎯

7

12

83

8

7

71

Shot term floating vol and fixed strike vol is moving higher today across the $SPX structure causing option premium to move into the 98th %ile and widening the Var risk premium. Put open interest continues to move higher and calls lower. Inverted C/P ratio is 0.39 which is one of

10

5

71

@BotFintwit

IMO we get a quick spike to 20SMA (finally), and that's your final dip long into new highs. 4850-4900. With QOPEX expiring I believe we finally see vol become unpinned. The next leg higher would be market up + vol up in a big way!

6

5

70

Sources:

.

9

3

71

As we approach the $SPX targets mentioned above, I thought I would throw out my comments from this AM. I hope everyone has a fantastic weekend! Cheers🍻

10

1

68

The final squeeze I have been waiting for... Be ready🙂

1/ Bulls, you've got to ask yourself one question... Do I feel lucky?

It's do or die time.

5

8

54

9

5

64

First major SPX target of the 50d is nearly complete, where I'd be looking to monetize. Skew is performing extremely well today along with fixed strike vol. Var risk premium has widened to nearly 8pts, the highest since March '23 (SVB Blowup). The 3rd chart below shows the

9

6

66

1/ $SPY Tomorrow's candle close is going to be the most important one in over a year. Hopefully you guys read this thread in full! Traders are bullish on $AMZN and here is what that means.

1/ Now that we are here, let's try to analyze what could possibly be coming next. Thread into $SPY, $MSFT/ $GOOGL earnings, $VIX.

3

10

47

12

14

61

52/ I know this is a long thread and some might say it’s useless, but you have to zoom out and weigh all the evidence from a critical point of view. If you made it this far, thank you! Making informed investment decisions based on hard data is the key to success. Right or wrong.

1

0

63

While $SPX has been grinding higher, the $COR90D index which quantifies expectations for a left-tail event (Crash), is back to March banking crisis levels. Also noteworthy, is one of the largest $VIX calls I have seen in recent times. $16M in June 26c, nearly 100k contracts.🚨

7/ $SPY +2StdDev sits at 419.64, it will open the door for $SPX 4200 if $NFLX earnings go well. Otherwise, we start our sell to 20SMA (405.25). Bulls will need a close above 4200 for further upside. Failure to show strength tomorrow will sound the alarm🚨

Trade safe!

0

0

15

4

17

63

1/ $SPY Another $2.6B at 418.72 bringing the running total to nearly $10B within 2 days and $2 apart.

"Hedge through Tuesday." Now you can see why I said this. The majority related to post-opex but the debt deal has to be factored in.

Here is what I see moving forward:

$SPY So far 420.89 has marked it. $9M in $VIX calls (100,000 lot) and a $16M $SPX put nearly 500 points OTM with 6/16 expiry came in today. With the OPEX narrative gaining traction, it doesn't hurt to hedge the weekend news through Tuesday. The outcome here remains the same.

12

12

118

8

12

63

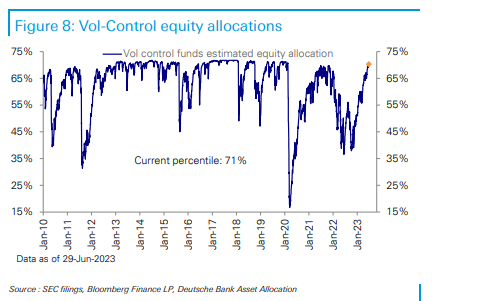

14/ Vol control funds raised their equity exposure further to 70.3% (71st percentile). The highest since February 2020 and close to the historical maximum.

1

4

62

END/ If you made it this far, thank you! Hopefully you were able to get something out of this thread. If you didn’t and are completely lost, feel free to ask whatever and I'll do my best to explain. If you already knew everything in this thread and it was a complete waste of

5

2

60

@SamanthaLaDuc

They also nailed Silicon Valley Bank blowup just to name a more recent systematic event.

5

2

59

$SPY Big day tomorrow with NFP. After JOLTS #, bad news is still good news. Skew has been reset back to July 31st. Realized vol>implied/forward vol. Option premium is now in the 12%ile. <10DTE puts are bid. A healthy backtest to the 50d soon ($446) would solidify this bull move.

7

5

58

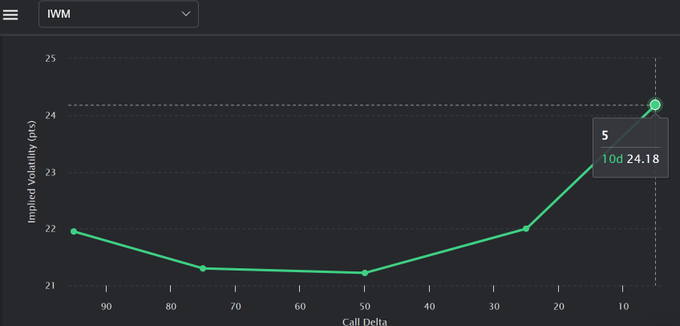

Market is pricing in 5 cuts for 2024. Meanwhile, $SPY call OI has reached 1YR highs and $IWM has a completely abnormal 10d call skew structure. Total index skews, $QQQ $IWM $SPY $DIA, have all collapsed to lows. $SPX is 2StdDev above 20d. Talk about asymmetrical risk to reward...

Today is FOMC day, right?

Today's 4,650 at-the-money straddle is currently just:

$25.5 or 54bps.

That's pricing for perfection, lets see if Powell delivers!

22

25

159

5

5

56

@JustinRyu10

@HardenChandler

I'm short from 5195, no July entry yet but trading the expected pullback for now.

@Curious6789

@JustinRyu10

@HardenChandler

When the 20SMA is likely tested by mid week then watch for what the reaction is, not price, but under the hood metrics like momentum/FSV. I don’t see a scenario where I wouldn’t take July vol by 5/13 after hours - 5/14 an hourish after the open. Larger participants are well aware

4

0

21

4

1

58

5120-5130 I plan on exiting longs, and yes I know we can overshoot to 5145 but the objective is complete at that point and the Var risk premium has normalized. Will cover front month VIX at any point in 14s and start my roll into July from June.

8

1

57

There’s supposed to be images here but for some reason they won’t load in the post.

1

3

56

1/ Bulls, you've got to ask yourself one question... Do I feel lucky?

It's do or die time.

18/ June puts and VIX calls. Remember when the "Santa rally" never came? We squeezed after it was expected from Dec OPEX into the 1st week of Feb. Same story here but inverse. No downside 5/5-5/8, 5/15-5/18 then I'm afraid we could squeeze into the first week of June.

3

5

25

5

8

54

1/ Some interesting vol dynamics after today's CPI. Let's take a look at $SPY, $QQQ, $VIX, and $IWM.

$SPY The VRP (Volatility Risk Premium) gap was closed, RV has just been crushed. RV10 now dates back to Nov 2021. Options still trading near min levels.

Congratulations, $SPY 20DTE contracts are trading at the historical min levels.

RV10 now goes back to Jan 3rd, 2022.

With NFP, Kashkari, CPI, PPI, Jobless Claims, Bank Earnings, and Retail Sales next week, you have to ask yourself... How long will this stay around for?

5

5

23

1

19

52

2/ Before we get into new information, it’s important to understand what happened as it lays the foundation behind this thread. I have covered April and May extensively so I am focusing on June/July here.

Buckle up, this is a long one. You'll understand why at the end.

1

4

54

2/ To clear up some misconceptions about this trade, there is zero immediate impact unless vol actually starts to get going here. This can be a large portfolio hedge as $VVIX and the $VIX sit near all time lows while the cost to hedge is nearly the “cheapest” on record.

2

0

54

For those wondering why the market is not accelerating to the downside despite the abysmal econ data. $SPY Put selling+0DTE Call buying=Supportive market flows. Until they close out positions or flip to puts, we are stuck. Do they want to hold risk over the long weekend?

4

9

50

END/ If you leave with anything:

Sell a damn cab

Drive a damn cab

Cheers🍻

3

1

53

@jam_croissant

Thought I would give my $0.02 for whatever it's worth. The most expected decline in what feels like forever is "supposed" to start tomorrow. Vol markets are reflexive. I'm seeing no reach for downside in higher delta strikes and calls remain well bid as of this AM.

5

4

50

13/ VolC funds don’t care about macro, sentiment, or any other indicators. They trade solely on the premise of realized volatility. If RV goes down, they buy equities. If RV goes up, they sell equities. They’re a lesser known culprit supporting markets everyday to the tune of $B.

1

5

52

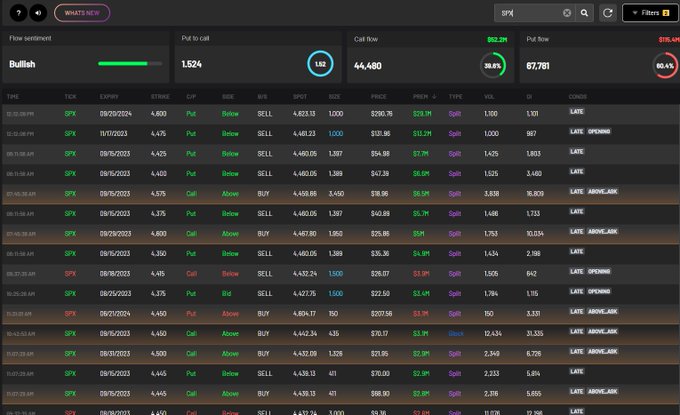

Let's see how institutions are positioned this week.

@CheddarFlow

$SPY, $SPX, $VIX, $QQQ

Filter: $1M+

3

7

48

@Jedi_ant

I don’t expect you to read this all but I make the case for a tad bit higher, a convincingly enough pullback to get 4100-4200 puts closed, and then one more leg up. IMO after that is when the “true” move comes into an unhedged market.

5

5

50

23/ Lastly, we still have record short interest in the market. There isn’t much commentary needed for this one.

2

1

49

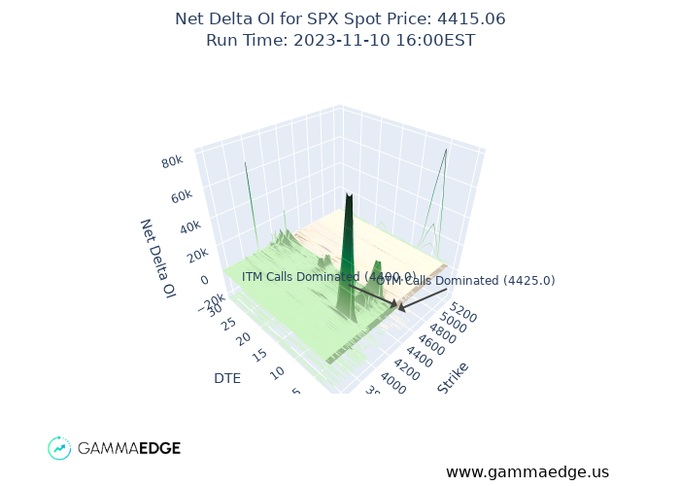

11/ This weeks econ data comes as dealers are stuffed with gamma at the 4,400/4,450 strikes. This could hinder if not reverse the upside progress seen. In case you might be new, when participants sell (monetize) calls, MM are selling the deltas (stock/futures) back to the market.

2

2

51

5/ $SPX We are seeing some clear put selling and call buying into this selloff. Aug OPEX is Friday 8/18, there are some nice structures to try and play a 4450-4475 pin which sits just over the 50d. This would pair well with the supportive ITM put Charm.

10

2

49