Cumberland

@CumberlandSays

Followers

29,161

Following

89

Media

155

Statuses

656

A global leader offering 24/7 access to deep crypto liquidity. Not investment advice.

Chicago, London & Singapore

Joined September 2017

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Kendrick

• 647325 Tweets

Drake

• 549975 Tweets

Rio Grande do Sul

• 266814 Tweets

Madonna

• 186475 Tweets

Ole Miss

• 105733 Tweets

Nicki

• 99088 Tweets

Sony

• 86192 Tweets

Porto Alegre

• 67484 Tweets

Star Wars

• 67286 Tweets

Hope Hicks

• 45926 Tweets

ウズベキスタン

• 44098 Tweets

#David69

• 36467 Tweets

Leclerc

• 31960 Tweets

#الاتحاد_ابها

• 30486 Tweets

Helldivers 2

• 23474 Tweets

Mark Hamill

• 21785 Tweets

Luton

• 21054 Tweets

日本優勝

• 19128 Tweets

Keyshia

• 17973 Tweets

みどりの日

• 15007 Tweets

Verstappen

• 14898 Tweets

David Raya

• 14802 Tweets

McLaren

• 11589 Tweets

Lando

• 10928 Tweets

Getafe

• 10041 Tweets

It’s remarkable that that the collapse of an ecosystem worth >$50B created no contagion whatsoever. When Lehman (a similarly-sized institution) went bankrupt, the entire global c-fi system was brought to its knees and had to be bailed out with $trillions of taxpayer money. 🧵👇

119

384

2K

After a period of relative calm, we are now seeing the largest flows of the year through our OTC desk. This is a bit unexpected, and likely a signal that we are nearing either a local bottom, or _the_ bottom.

🧵👇

40

320

2K

The end of 2% inflation and what it means for crypto:

🧵👇

60

265

1K

Last week was Cumberland’s most active week ever. Beneath the chaos and explosive volumes, the FTX bankruptcy has triggered some important market structure changes 🧵👇

37

160

653

“Don’t fight the Fed” is a trading truism whose validity appears to be manifesting itself across many markets in the wake of yesterday’s 75bp hike. After a dead cat bounce, everything from

#Bitcoin

to Brent is steadily grinding lower.

🧵👇

13

110

629

After a very busy month, price action is consolidating. Given the nature of crypto and the tectonic shifts occurring beneath it, we do not expect this paradigm to last 🧵👇

56

132

558

Over the past week, ETH quietly rallied 55%. Prices have retraced this morning, but the broader up-trend is intact and it’s worth understanding why 🧵👇

51

74

432

Post FTX, crypto markets have settled into a new range – wrapped around $16,500 BTC and $1,200 ETH. While we could easily trade sideways through a quiet holiday period, there are a number of catalysts in either direction 🧵👇

59

73

412

Yesterday we tweeted about the concept of a top stablecoin depegging as a possible catalyst for a move lower. In retrospect it is easy to see why the Tweet may have been misinterpreted. Therefore we have removed it.

64

32

413

Rangebound price action belies a volatile picture below the surface: a growing number of centralized cryptoasset companies are halting withdrawals, reducing headcount, and hiring restructuring firms.

🧵👇

37

95

390

Desk Update: Historically, our OTC trading is relatively balanced between buyers and sellers. Over the last week, our OTC buy/sell ratio (by notional value) has increased approximately 60% towards counterparties buying.

15

133

384

A budding uptrend is taking shape in crypto. This comes against the backdrop of a weakening dollar, a more constructive macroeconomic environment, consequential midterms, and a growing drumbeat of progress in digital asset adoption. Let’s break down each factor individually: 🧵👇

16

82

388

The flow we are seeing on the OTC desk is reflecting the new reality. It has been extremely focused in BTC and ETH, and we’re seeing very little profit-taking, despite the fact that BTC is up 70% on the year; our flow ratio right now shows roughly twice as many buyers as sellers.

9

75

369

The people who wanted to sell sold long ago, and now we are witnessing the people who have to sell. Unless the FOMC delivers a spectacular hawkish surprise (100bps?), it feels like we’re finding a degree of equilibrium here.

6

30

353

You love to consume crypto content, but you're looking for a podcast hosted by traders, not journalists.

Check out 1000x, hosted by

@AviFelman

&

@jvb_xyz

Spotify:

Apple:

YouTube:

16

52

329

The Merge is complete, it was uneventful, and that fact is absolutely monumental. 🧵👇

15

31

328

For further clarification, we have no knowledge to indicate that the top two stablecoins are not fully backed and sufficiently liquid to meet redemptions.

22

16

308

Lots of volatility overnight as speculation about

@FTX_Official

continues. With the caveat that we are not investors in FTX and do not have any non-public insight, the following features seem evident: 🧵👇

9

46

299

While it’s impossible to say which, in the spirit of humility, let’s assume it’s a local bottom; objectively, it’s hard to envision a scenario where crypto starts ripping while broader risk assets continue their bear market trajectory here.

3

4

283

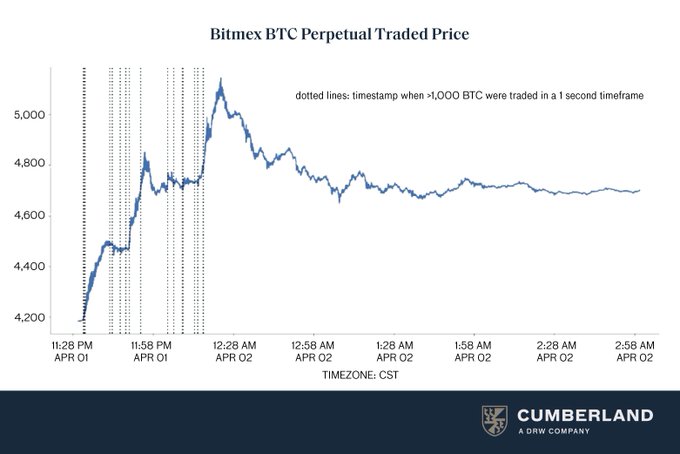

Desk Update: The post-trade analysis of Monday evening’s price action revealed a series of large bids (>1,000 BTC per order) within a 1 hour span, which appear to be actual buyers vs. forced liquidations.

12

86

270

Some would argue that crypto has been a poor inflation hedge during this particular bear market. While true (so far), it’s important to remember that crypto is a debasement hedge, not an inflation hedge.

9

44

279

CFTC vs. Binance is now an important driver of price action. The outcome is likely going to fall into one of these three scenarios: (1) Clearer guardrails, but no material penalty (i.e. they win the case scenario); (2) Clearer guardrails, but a manageable penalty; (3) Clearer…

17

67

255

FTX, Alameda, and a wide array of insolvent lenders would not have filed for Chapter 11 protection if they hadn’t already sold the entirety of their liquid assets in a last-ditch effort to extend runway.

10

31

251

1/ Yes, there was selling across the board last week as participants took risk off the table, but it’s important to highlight that nothing actually broke – no exchanges went bankrupt, no protocols disappeared (ex-LUNA), and no critical crypto infrastructure was damaged.

15

13

245

While it’s disheartening to watch a large digital asset empire crumble into a modern incarnation of Lehman/Enron/Madoff/Theranos, no relevant chain stopped processing blocks last week. These industry-defining events are usually the predecessors of market recovery. -

@jvb_xyz

8

32

242

Yesterday’s crypto price collapse was part of a broader risk-off move that impacted many macro markets. BTC & ETH outperformed on the selloff, which is to be expected. 🧵👇

45

16

220

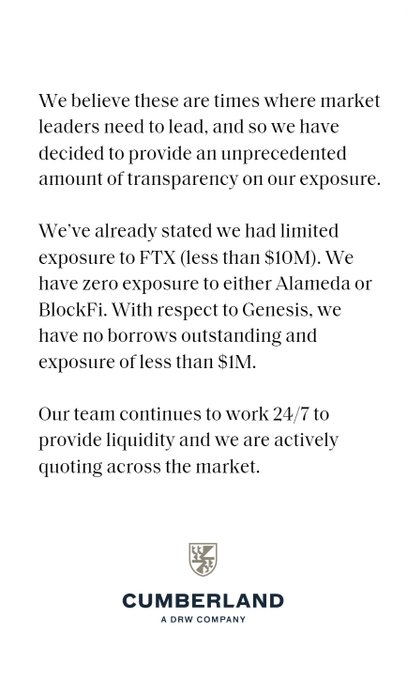

This thread is a thought exercise with the goal of exploring the types of entities that may be impacted by recent price action. We are not expressing any explicit insight or concern with regard to any specific entity.

22

6

229

Thus, unless we’re dealt a deflationary tech miracle (cold fusion?), a higher inflation target or a bankruptcy cycle are the only ways out of this situation. If our CBs choose the former, a crypto summer is around the corner. If they choose the latter, look out below. -

@jvb_xyz

14

14

216

Our heightened flows here are relevant because in the early stages of a bear market, when participants are hurting but still solvent, bullish, and viable, there tends to be a deer-in-the-headlights phenomenon where volumes wane and capital drifts quietly to the sidelines.

1

7

220

Ever since the major lenders started tightening up over the past few sessions, we started seeing forced selling in block size across the entire spectrum of counterparties – something which appears to be occurring on-chain as well (

@parsec_finance

is great for visualizing this).

2

8

217

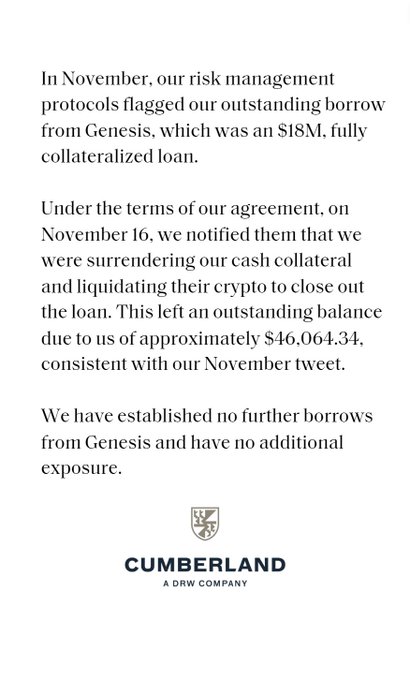

Genesis’ bankruptcy filing today reflects misleading and incorrect information, and as part of our commitment to transparency, we are providing more details.

11

14

215

We recognize the market right now is in search of answers and transparency as we work together to weather the storm created by FTX.

34

27

206

2/ This reveals a robustness that critics have questioned in the recent past. That said, many crypto-native participants take this robustness for granted. While UST was not systemically important, other stablecoins are.

2

7

210

We do not foresee a prolonged paradigm of indifference and price stability. Instead, we foresee a spat of volatility while the market rewires itself and web3 business models recalibrate. This will be followed by an eventual up-trend. -

@jvb_xyz

8

14

209

1/ The crypto selloff that took place in June was largely led by forced liquidation of collateral at centralized lenders.

10

29

199

This is precisely what we witnessed on-desk during some of the recent selloffs (even the sharp ones): there was some voluntary, orderly risk-reduction and the occasional spat of dip-buying bravery, but nothing like the explosive activity we’ve seen this time.

1

4

177

In other words, bitcoin won’t protect a portfolio from a few hot CPI prints. But sustained, tolerated inflation is just another form of fiat currency debasement – a backdrop against which crypto performs spectacularly.

9

11

174

ETH/NASDAQ correlation is nearly back to the highs of the year – a feature which has overshadowed the idiosyncratic dynamics of the Merge (for now) 🧵👇

18

36

177

It’s difficult to predict the scale of the liquidations which have yet to occur, but this type of activity tends to correspond with prices bottoming out. No one has enough dry powder to fight the Fed, but the faster they hike, the shorter hike cycle and the sooner the reversal.

3

12

169

Normally, when prominent economists start calling for a resource war, markets are close to bottoming out. The same sort of dire predictions materialized during the most apocalyptic moments of 2008, just before a historic decade-long rally.

.

@TheEconomist

latest cover.

Almost impossible to overstate the risks/consequences of the world’s food insecurity

Another great “unequalizer” whose implications, depending on the country, may include not just livelihoods but also lives, political stability, social cohesion, etc

47

290

699

12

45

167

In TradFi, this is when the Fed injects liquidity that lenders have failed to provide. In crypto, there is no digital Fed to buy vast quantities of distressed coin, no digital OPEC to cut production and support prices, and no digital congress to ratify crypto stimulus packages.

6

14

160

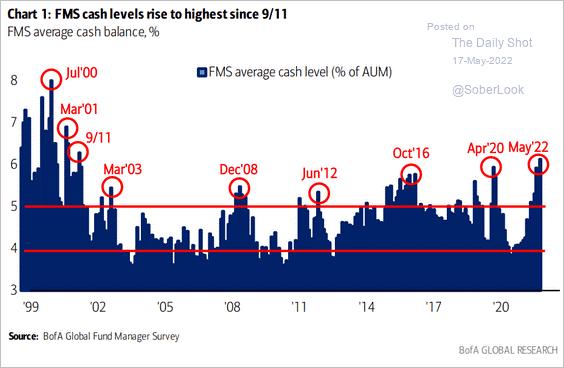

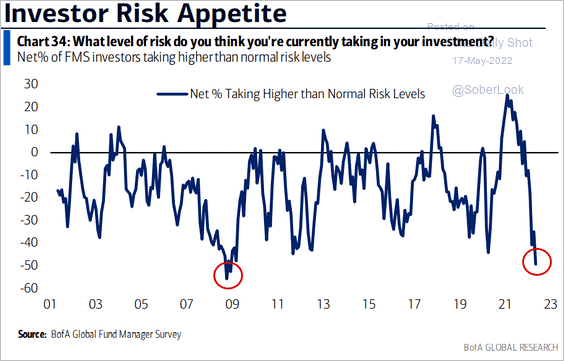

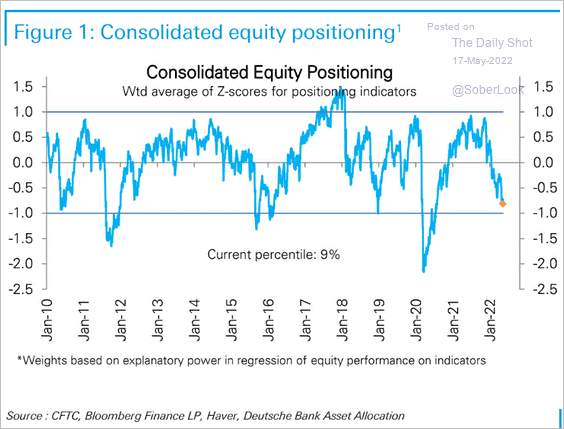

4/ Directionally, we’re getting to the point where bulls are few & far between. This isn’t just true for crypto, it’s a feature of many markets – per the charts below, fund managers are more bearish & hoarding more cash than they have done at any point since the early 2000s.

2

14

162

This past weekend,

@TheEconomist

published an article called “The end of 2%” – a reminder that the inflation target set by central banks around the world is arbitrary and anything but guaranteed to last.

2

18

147

During these regimes, capital tends to flow into assets that appreciate. Until crypto, these assets were either “hard” (i.e. real) or financial, but now they can be digital too. And unlike all other assets, the digital variety is universally accessible by design. This is historic

6

13

149

The assets of these companies will, at some point, need to be liquidated in order to partially offset their outstanding liabilities. Uncertainty around the size and timing of these asset sales is hanging over the market like a cloud.

7

16

147

That said, the Alameda CEO didn’t do her company any favors by calling out a level ($22 FTT) and then watching the market jackknife through it.

7

15

137

Bear markets tend to reach a state of maximum violence at the point when credit disappears, and that is precisely what we are seeing in the digital asset sector right now.

2

7

133

Looking forward to 2023, the sources of market recovery will be related to adoption. Against the backdrop of a weaponized dollar, China and Russia are quietly deregulating bitcoin and augmenting its geopolitical relevance.

7

14

132

Against this backdrop, on-exchange liquidity in both linear and nonlinear derivatives has thinned to a degree that is nearly unprecedented since March 2020. As a direct consequence, we are seeing the largest flows of the year through our OTC platform:

1

9

130

ETH just broke out above its recent range, and the fact that this is occurring against the backdrop of a generally bearish regulatory climate is worth exploring.

Doge-themed redesign of

@Twitter

notwithstanding, ETH gas spiked to 68 gwei yesterday – the highest we’ve seen since…

6

20

116

Instead, digital assets will reside in countless silos around the world and the functions of custody, lending, settlement, clearing, and [most importantly] liquidity will be offered by an array of intermediary nodes and providers in an interconnected but non-interdependent web.

5

14

123

Cumberland is thrilled to work with T. Rowe Price, WisdomTree, and Wellington Management on Avalanche’s Evergreen Subnet, “Spruce”. At Cumberland, we are proud to be among the earliest institutions to participate in digital assets and DeFi, and we are continuously thinking about…

5

26

117

Lenders, both centralized and decentralized, have either exited the space or have tightened capital access to the point where market participants no longer have the liquidity they need to enter and exit positions in orderly fashion.

2

3

120

The reason why is rooted in two tradeoffs:

1. Loss of faith – hiking inflation targets is a slippery slope. It’s also just another form of QE.

2. Rising inequality – assets and opportunities that insulate against the ravages of inflation are unavailable to most people.

3

4

117

In other words, you don’t go bust if you have tradeable coins left to sell. Perhaps what we saw over the past few months was the wholesale liquidation of those coins.

6

5

116

Throughout this period of challenged liquidity, Cumberland is available 24/7 to make tight, institutional-grade markets in a wide array of cryptoassets. -

@jvb_xyz

4

1

111

5/ Unlike then, however, cash is now a terrible place to hide as high-single-digit inflation rages across the developed world. At some point, custodians of capital will have to stop into risky assets to avoid the bleed.

1

6

114

The much awaited FOMC rate decision lands today at 2pm ET. Expectations for a 50bp hike have been widely telegraphed, and anything else would be a shocking deviation.

🧵👇

3

18

115

Ultimately, it seems unlikely that both monetary policymakers and elected lawmakers will join forces to unleash both the Volckerian firestorm and the fiscal austerity that it would actually take to bring inflation under 2%.

3

4

110

3/ As regulators accelerate their efforts to bring transparency to the stablecoin space, anyone even tangentially exposed to digital assets should be watching closely.

1

2

111

The fact that it was successful yet uneventful is an incredible testament to the people involved, what they've done for the world of crypto, digital assets, and decentralized computing. Massive congrats to the ETH core devs from Cumberland.

6

4

112

When traders are unsure about crypto prices, they flee to stables and bank deposits. When they are unsure about stables and bank deposits? It's crypto's time to shine, and BTC and ETH rallied 14 and 15% respectively over the weekend amidst uncertainty in the banking sector.

13

16

108

Ultimately, markets involve trust and the events of last week damaged trust in the crypto industry. That said, FTX’s insolvency absolutely must be differentiated from the viability of blockchain technology.

4

6

107

The events of last week triggered a handbrake turn, and while it’s still too early to predict, crypto market structure now seems likely to mirror FX – a world where assets and capital aren’t parked on centralized exchanges.

2

11

105

The author subsequently speculates that by revising the target upward (to 4%), central bankers can simultaneously engineer both a budgetary windfall and an off-ramp to the impending disinflationary purge/crisis/etc.

2

5

102

Monday was largely block-size voice trades with a heavy sell ratio. Since then activity has gone electronic, with less directional bias – volumes on our API have reached sequential year-to-date highs this week.

1

1

103

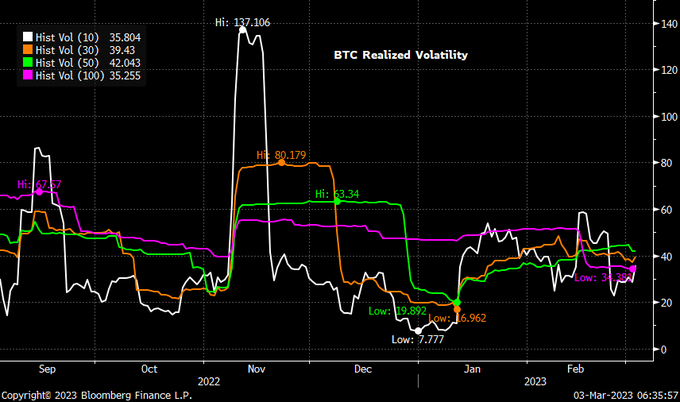

Last night’s move notwithstanding, realized volatility in crypto has dropped off a cliff – spot has been locked in a tight range since the 20th of January, and the benchmarks of the space are now far less volatile than commodities like natural gas. 🧵👇

10

19

103

1. It is unlikely that FTX would take customer deposits and then cowboy those assets into unhedged risk token length. As an audited entity in the wake of recent crises, it would seem beyond odd for a platform with the organic success of FTX to bet everything on a roll the dice.

9

4

100

This is hardly a novel phenomenon; excessively levered finance companies have been punished in bear markets for hundreds of years. While this current cycle raises eyebrows because the assets are digital, the underlying economics are no different than the examples in textbooks.

2

8

96

In the face of daunting (at best) or even insurmountable supply-side challenges, expecting a higher inflation target now seems like a rational base case. If this policy change is implemented, tacitly or otherwise, it would be a watershed moment for bitcoin.

5

7

96

Yesterday was a record day of trading volumes for all of the wrong reasons. While we had virtually no exposure to FTX and our operational controls enabled us to provide deep liquidity to a market in search of it, the exchange consolidation we saw was unfathomable 60 hours ago.

7

9

95

Digital assets currently sit in a bizarre no-man’s-land between the cascade of liquidations in June and a series of macroeconomic and crypto-fundamental catalysts on the near term horizon 🧵👇

8

17

88

Ultimately, the swing vote will be cast by regulators. We think that thoughtful, well-structured regulation will spur a Cambrian explosion of technological innovation and a secular bull market. Senseless and/or overly punitive restrictions threaten to do the opposite. -

@jvb_xyz

2

6

90

The most frequent question we're asked on weeks like this is "what does the flow look like?"

OTC flow gives some insights into how the market is handling these major moves.

🧵👇

2

8

91

Desk Update: Historically, our trading volumes have been more evenly weighted across BTC and ETH. However, our recent flows have been heavily skewed towards BTC - with approximately 70% of our transactions in BTC.

6

13

86

As long as large and opaque off-chain liquidation flows are looming in the backdrop, participants will be hesitant to commit capital. This reduces liquidity and increases volatility.

2

4

92

Thus, in 2023, we expect to see the emergence of a variety of regulated entities who will become the trustworthy providers of various well-defined market services.

4

7

91

FTT should remain volatile for some time. If, hypothetically, it were to trade down to $0 on forced selling (again, highly unlikely – most of it is locked), it would seem like bad risk/reward to bet that FTX relies on a positive EV for FTT to remain a going concern. -

@jvb_xyz

5

5

87

The speed at which markets return to a healthy state will be determined by the rate at which distressed assets are transferred from the balance sheets of the insolvent onto those of the solvent. Off-chain, this process is messy, time-consuming, and fraught with legal complication

2

7

84

Since Thursday night, global risk on helped push crypto higher as BTC rallied some 15%, far outpacing ETH now posting a more modest 8% increase. Interestingly, risk asset gains come against a backdrop of hawkish fed speak and cementing of higher rate expectation:

10

12

70

Meanwhile, there are 1M+ depositors who thought they held crypto but now hold only distressed claims on assets which are locked for years (at best) or permanently lost. Eventually, some of these people and entities may decide to rebuy/replace.

3

4

85

it’s becoming increasingly evident that in most scenarios, the market is actually facing a deficit of crypto, not a surplus.

5

11

84

Major technology companies with billions of users continue their onboarding blockchain technology. The volatility of this asset class has captivated the attention of the entire spectrum of investors – retail and institutional alike.

1

4

86

Yesterday the SEC rejected Grayscale’s bid to convert

#GBTC

into a spot ETF. While widely expected, this decision contributes to an increasingly challenging investment backdrop: Powell is now openly telegraphing that he is more concerned about inflation than a recession. 🧵👇

7

13

78

Centralized exchanges had every incentive to push the all-in-one model. In hindsight, some of those incentives were perverse – FTX was happy to offer 20x leverage because doing so increased the probability that a user would be force-liquidated by Alameda at an unattractive price.

3

6

81

Against this backdrop, volumes remain explosive; this is not the bear market of 2018 when activity evaporated altogether. Instead, it is evident from our perspective as liquidity providers that the number of entities who care (and transact) is steadily on the rise.

3

8

79

Over-the-counter trading is the lifeblood of spot FX liquidity and will only become more important for crypto going forward; after all, currencies are bearer assets and so is crypto.

3

5

81

dozens of crypto companies are either severely curtailed or out of business, and the future of the industry is as cloudy as ever. That said, prices have reached a surprisingly buoyant equilibrium which is well off the lows of the year.

1

4

77

Unlike the apathy which was a defining characteristic of crypto winters past, the current market (despite its many challenges) boasts a spectacular amount of trading activity.

6

16

77

The impact of this has yet to be felt, but as we’ve seen from previous cycles, strong adoption narratives can lead to parabolic rallies. Thus, the current risk/reward feels meaningfully asymmetric. -

@jvb_xyz

0

0

78

And the dominant interest in the options space has been upside calls, with deeper strikes than we’re accustomed to on BTC and ETH. ~PK

2

1

71

Cumberland and

@xbtogroup

are proud to trade the first block of CME ETH/BTC future. The ETH/BTC cross has been the topic of many conversations between market participants for years. It defines how the market thinks about alts vs Bitcoin and DeFi vs. store of value. This contract…

2

10

72

Month-end is upon us – normally this is a bullish moment for digital assets as ratable inflows hit the screen, but with some very large funds effectively shuttered by the LUNA collapse, perhaps we are in for redemptions (and selling) this time. 🧵👇

5

15

69