Brad Setser

@Brad_Setser

Followers

97,638

Following

953

Media

8,842

Statuses

62,053

CFR senior fellow. Views are my own. Retweets are not endorsements. Writes on sovereign debt and capital flows.

Joined May 2016

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Davido

• 514537 Tweets

Baba

• 116859 Tweets

Valencia

• 80399 Tweets

Abeg

• 77510 Tweets

Peruzzi

• 76169 Tweets

Nancy

• 69103 Tweets

Madonna

• 59256 Tweets

Wetin

• 58105 Tweets

Francis

• 53659 Tweets

Burna

• 49641 Tweets

Lewandowski

• 49185 Tweets

Rock in Rio

• 48120 Tweets

Araujo

• 46143 Tweets

Seinfeld

• 42040 Tweets

Jesus is King

• 39713 Tweets

Katy Tur

• 30231 Tweets

#WWERaw

• 26600 Tweets

Grammy

• 25632 Tweets

Luciano

• 16755 Tweets

ANA CASTELA NO RIR

• 14944 Tweets

PRE SAVE FOI INTENSO

• 14691 Tweets

#WWEDraft

• 10555 Tweets

カレンダー通り

• 10362 Tweets

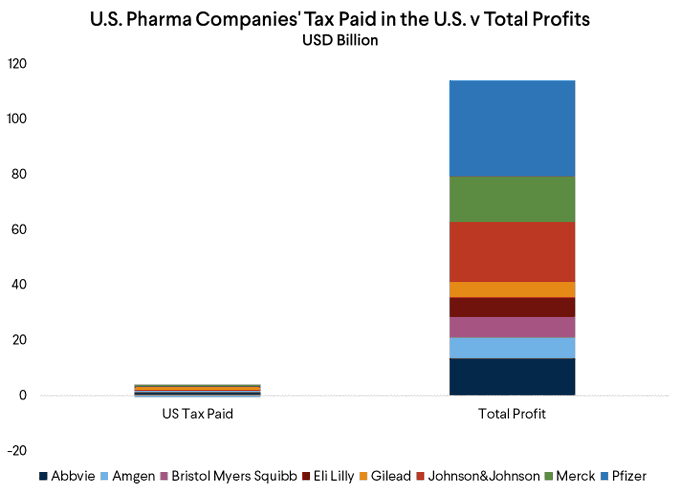

US pharmaceutical companies charge Americans more than anyone else. They report generating the bulk of the revenue in the US.

But they apparently earn almost no (taxable) income in the United States.

Rather remarkable.

1/

51

801

2K

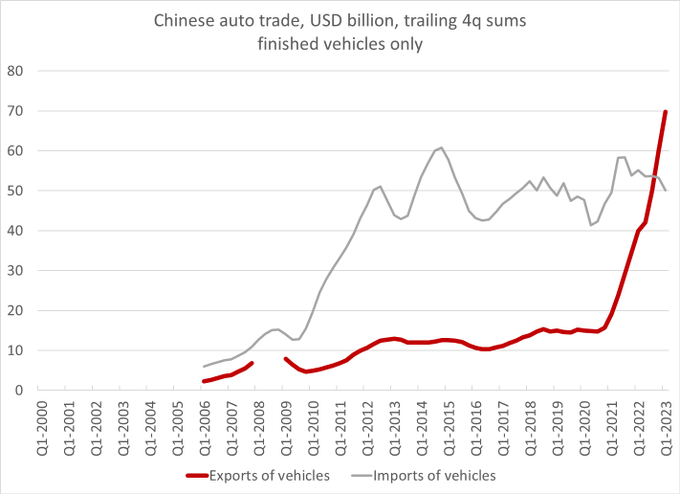

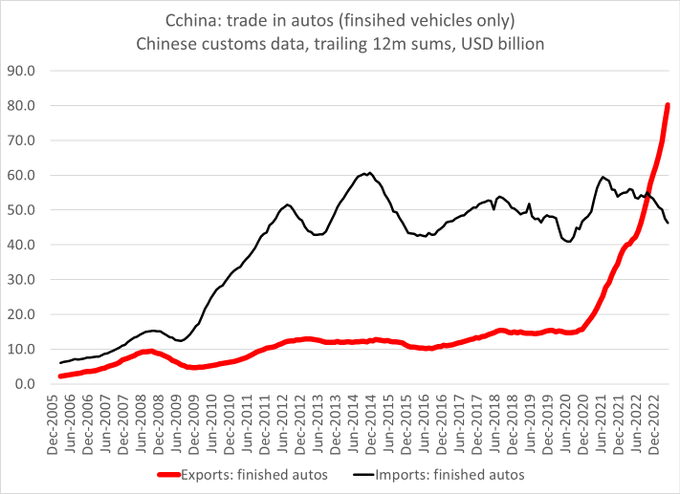

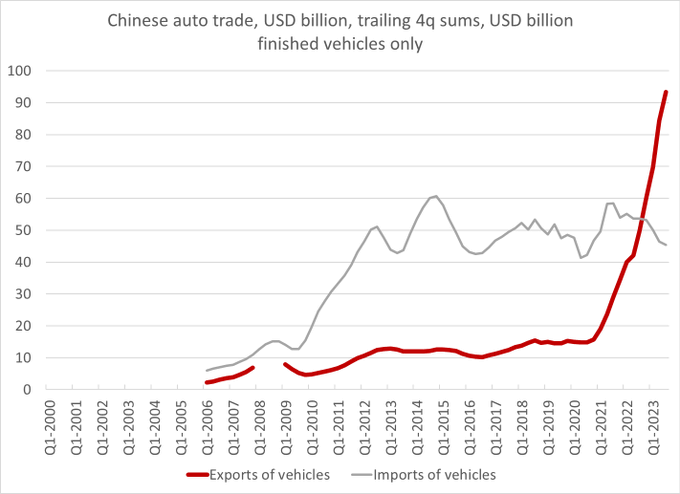

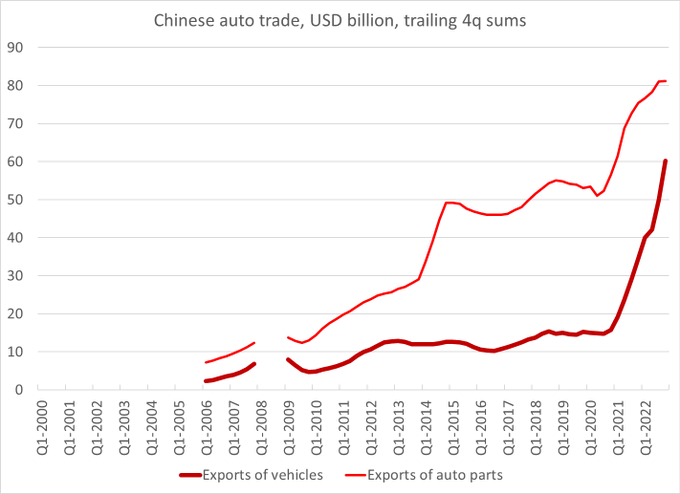

The pace at which China has emerged as a major auto exporter -- and now a major net exporter of autos -- is stunning.

1/3

92

590

2K

Stunning.

Happened incredibly quickly.

And happened while most international institutions were talking about "deglobalization"

"China overtook Germany in auto exports in 2022 and is set to eclipse Japan as the world’s biggest car exporter this year."

64

511

2K

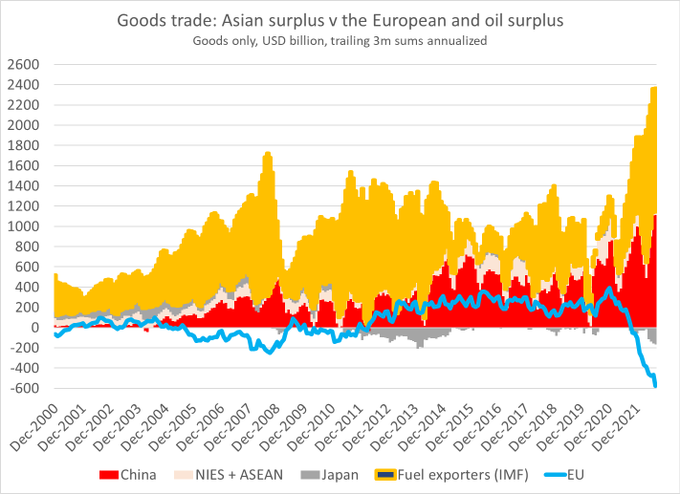

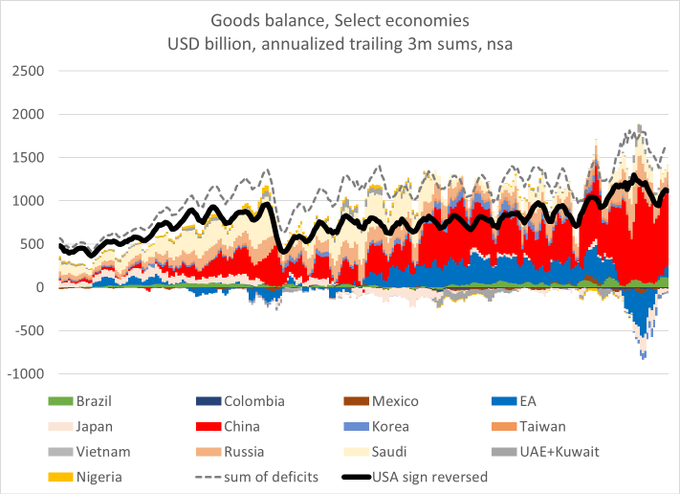

A reminder that Europe (and Germany) now relies on the US for security, relies on the US for energy -- and also relies on the US for demand.

Euro area exports to the US are over two times euro area exports to China --

1/

63

540

2K

I am taking a leave of absence from the Council of Foreign Relations, a leave of absence from Exante data – and yes, a bit of time off from twitter too, for what I assume are obvious reasons.

Agency review teams are an integral part of the transition process, responsible for evaluating the operations of federal agencies.

Our teams are composed of diverse experts with deep policy expertise, ready to ensure we're prepared to lead on Day One.

253

2K

9K

230

58

2K

The collapse of Silicon Valley Bank highlighted the risks posed by "underwater" long duration bonds -- particularly when those bonds funded with short-term liabilities.

Who else in the global economy holds a lot of underwater bonds?

Asian insurers and policy banks ...

1/

55

466

2K

Nice summary of China's economic troubles from the Economist.

Think this Goldman chart more or less nails the core problem

1/3

53

381

1K

The outline of the US government's response to the failure of Silicon Valley Bank is now clear, and the US didn't mess around. Clearly there was real concern about deposit flight and funding driven contagion.

The response has three legs --

1/

41

473

1K

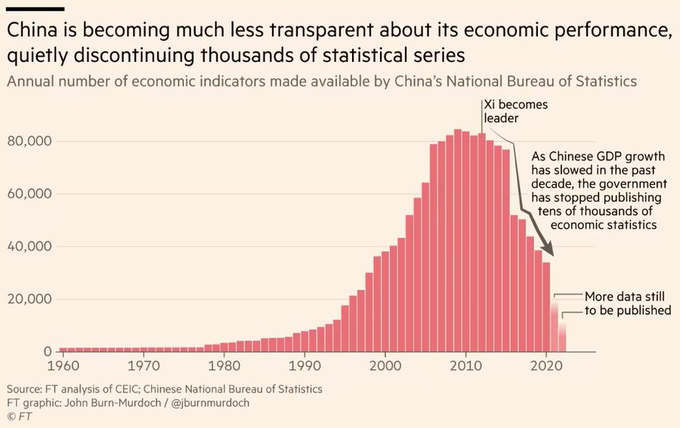

Stunning chart from

@jburnmurdoch

.

China has reduced the quantity of the economic data that it publishes over time.

There are also more and more questions about the quality of the numbers that are still (?) released.

1/x

27

346

1K

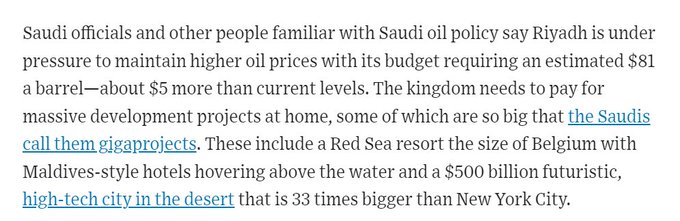

Looks like Saudi Arabia's balance of payments breakeven oil price (oil price that avoids a current account deficit) is now close to $85 a barrel. No wonder NEOM has been scaled back ...

1/

32

217

1K

And it is hard, at least for me, not to notice the gap between the decisive response of the US Federal Government and the lack of any coherent response (other than complain and ask for help) from the VC and tech world.

11/

19

242

1K

Stunning.

Spectacular, if somewhat depressing, reporting by

@Lingling_Wei

and

@yifanxie

"top leader Xi Jinping has deep-rooted philosophical objections to Western-style consumption-driven growth, people familiar with decision-making in Beijing say."

1/

108

297

1K

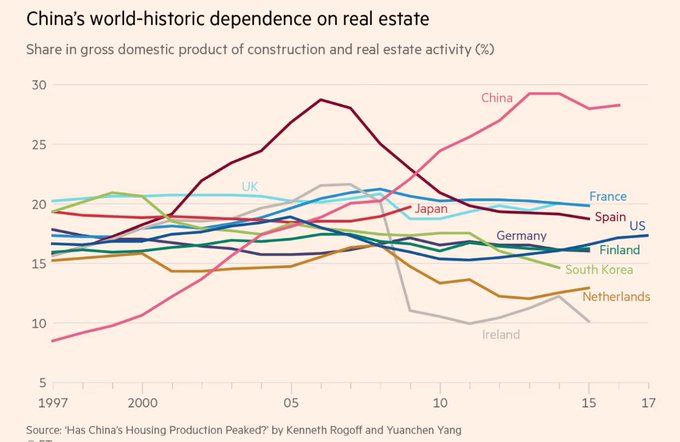

After the global financial crisis, China become a construction dependent economy.

Great Rogoff and Yang chart highlighted by

@MESandbu

today

1/

28

293

1K

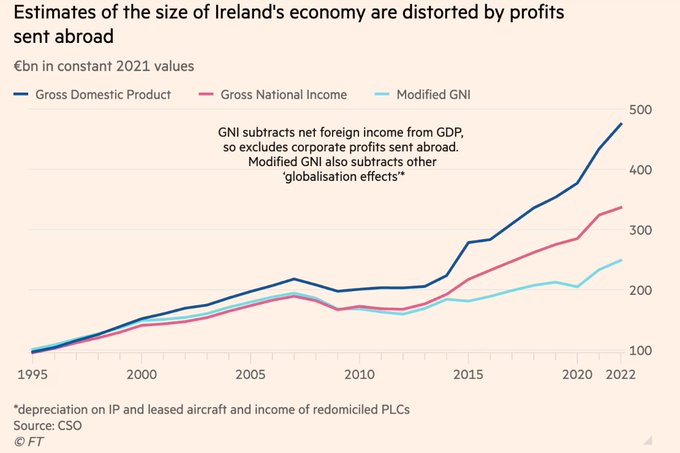

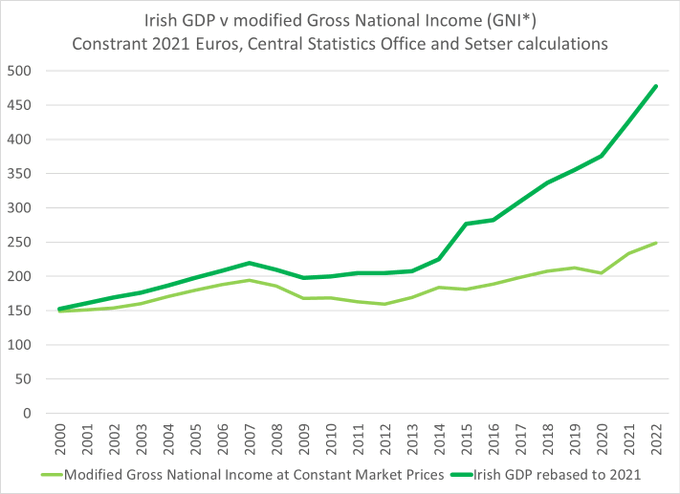

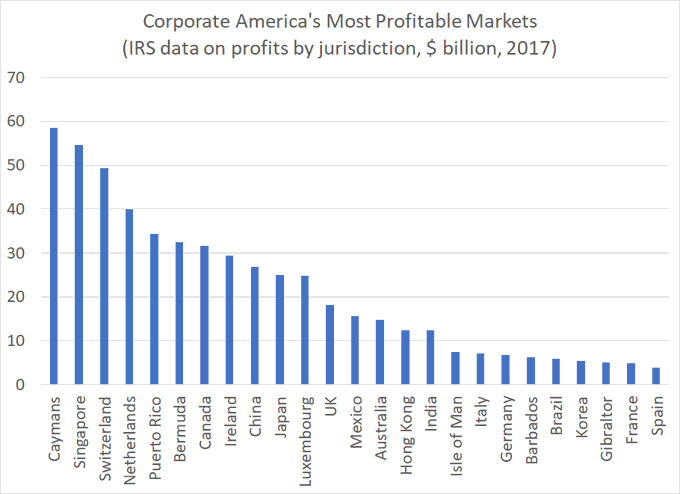

The real Irish economy (GNI*) is about half the size of the reported Irish economy -- the gap is a measure of profit shifting by big US companies, and it continues to grow ...

1/

28

315

1K

While the advanced economies talked about deglobalization, China's auto industry ... globalized.

And in a big way.

Amazing chart from Gavekal

1/

46

332

970

Whoah Nelly.

China on track to go from a trade deficit in finished cars of $30-40b before the pandemic to a 2023 auto surplus of $50b or so ...

Crazy.

Monthly trade data shows no sign that China slowed in q2.

1/2

45

247

971

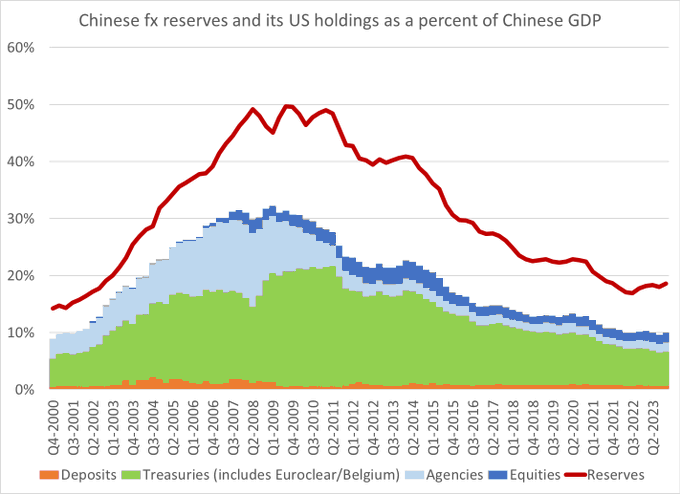

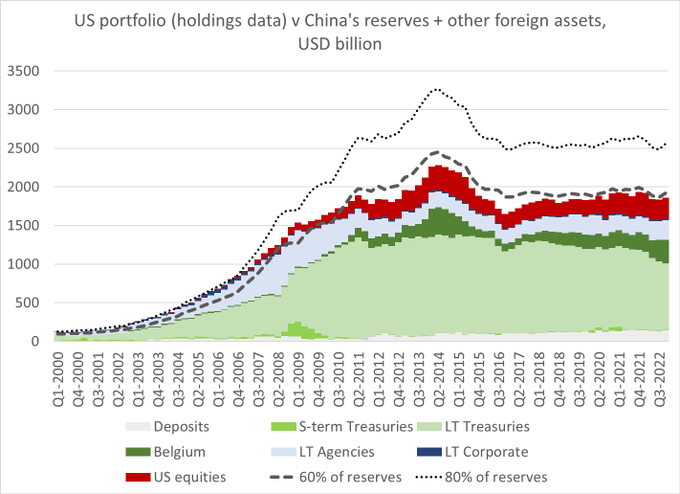

Was kind of surprised by this: China's holdings of US financial assets, as a share of China's GDP, are back down to where they were when China joined the WTO ...

1/

44

241

981

Exciting day for connoisseurs of statistical measures of international tax avoidance. Ireland released its measure of the "real" Irish economy (GNI *). It is EUR 200b smaller than the reported size of the Irish economy (GDP)

24

338

973

"It [China] has built enough auto factories to make every car sold in China, Europe and the United States"

Stunning stat from

@KeithBradsher

of the NYTimes

1/

61

329

964

A chart that illustrates how it is fundamentally impossible for China to construct a block centered around the developing world that replaces the US/ EU ...

there is an obvious problem, namely the size of China's surplus

1/x

1/8

Agree with Brad. That's because trade can only be resolved systemically, and not incrementally. As long as savings in China (and other surplus countries) vastly exceed domestic investment, the country must resolve weak domestic demand by running large trade surpluses.

20

119

450

41

318

973

It seems pretty clear after tonight's numbers (and the surprise PBOC rate cut) that China is in a recession (one of course with Chinese characteristics, so technically a growth slowdown) ...

1/

20

156

943

Hold the presses. The odds are that China isn't actually selling dollar bonds. Or even moving its reserves out of the dollar.

A new blog on how to interpret the US TIC data

29

252

934

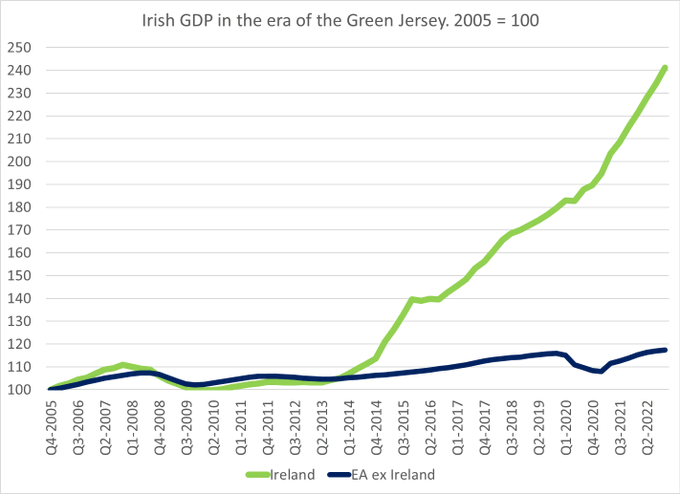

In honor of St. Patrick's day, a brief thread on Ireland's economy -- which has essentially decoupled from the rest of the euro area since 2015, and entered its own tax and economic zone in the middle of the North Atlantic ...

1/x

28

246

921

According to the WSJ, the Saudis fiscal break even oil prices is now close to $80 ...

1/

40

156

917

Only Martin Wolf could summarize China's economy so perfectly in a single sentence.

"The fundamental macroeconomic problems are excess savings, its concomitant, excess investment, and its corollary, growing mountains of unproductive debt"

22

220

902

Let's just say that I disagree with this pretty strongly ...

"USD is losing its market share as a reserve currency at a much faster rate than is commonly believed."

The dollar's share of reserves didn't actually change at all in 2022.

1/

34

228

908

Dedollarization continues to be especially popular in countries with no dollars left in the foreign exchange reserves ...

31

227

875

Just a reminder: The US generates the bulk of the revenue of US pharmaceutical companies, thanks to high drug prices in the US. But the major US pharmaceutical companies report earning most of their profit abroad ...

1/

20

250

887

The UK looks to be experiencing a form of the kind of crisis that Nouriel Roubini and I posited that the United States could face back in our (in)famous 2005 paper –

1/

22

195

869

Turkey's crisis has some similarities with the 1997 Asian crisis.

But only some. In key ways the balance sheet of the Turkish banking system differs from past crisis cases.

21

302

830

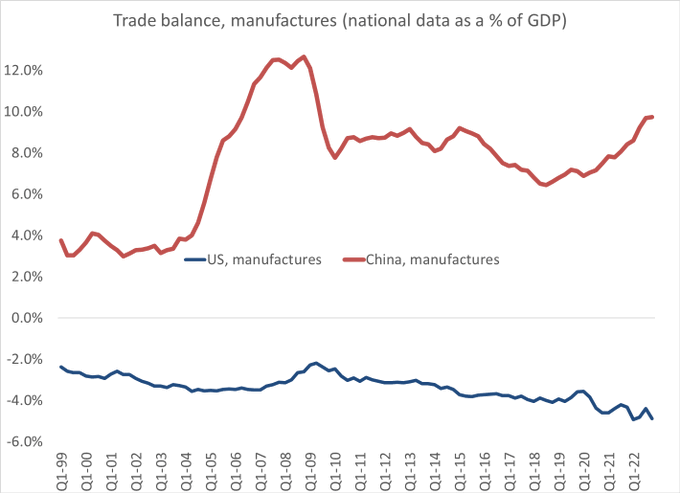

Someone should tell the trade data that China has lost manufacturing competitiveness

1/

Geopolitics is not the only reason investors are leaving China, it’s simply much cheaper to produce in other countries

77

552

2K

21

170

842

A striking statistic highlighted by Michael Schuman of the Atlantic:

"China’s automobile industry, figures Bill Russo ... has enough unused factory capacity to make more than 10 million cars ((sufficient to supply the entire Japanese car market—twice)"

60

238

799

Despite all the talk about how the world is standing in the way of China's growth, the world (including the US) continues to supply China with one thing it cannot generate domestically -- demand for its manufactures.

China's surplus again topped 10% of its GDP.

1/x

53

262

816

Milei is the next President of Argentina --

Will be interesting: dollarization without any usable dollars at the central bank is a technical challenge (to put it mildly)

48

178

806

The pithy formulation that Germany has relied on China for growth is now taken as gospel.

But, well, it actually hasn't been true for over a decade.

And things are changing fast ...

Some data

1/

31

218

779

The scale and pace of China's transformation into an auto exporter remains astonishing: it has swung from running a $30-40b deficit in finished vehicles to running a $50b surplus in roughly 2 years.

1/2

47

260

755

American pharmaceutical companies are American in name only. They charge high prices in the US, but they don't report making much money in the US (their profits mysteriously are all in low tax island economies) and they certainly don't pay much US income tax.

24

255

752

China is currently underlying going what

@adam_tooze

calls "a gearshift in what has been the most dramatic trajectory in economic history" --

And we have to try to understand it with what is by far the worst economic data produced by any of the major global economies.

1/

31

158

748

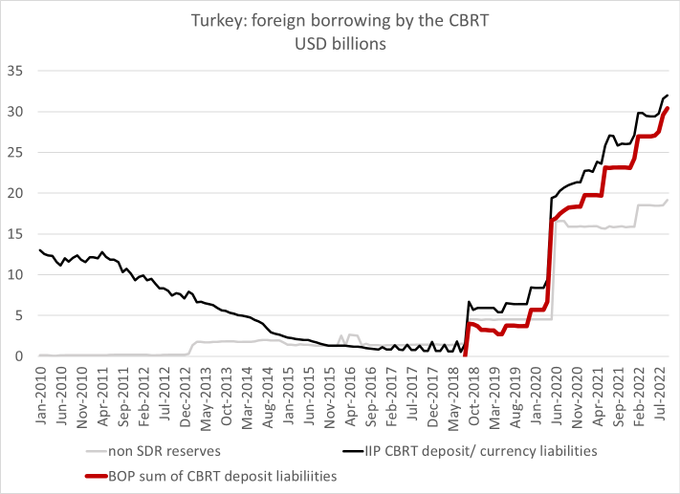

The ability of Turkey's President Recep Tayyip Erdoğan to get financing from “friendly countries” is really quite impressive -- even countries that themselves aren't exactly friends have lent large sums to the CBRT ...

1/

26

210

732

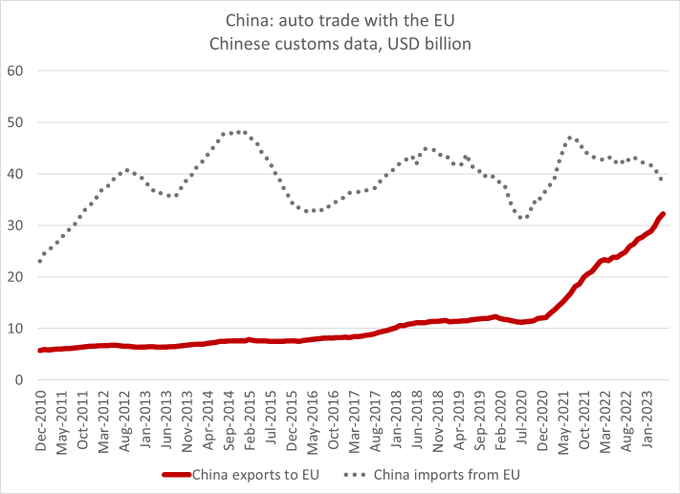

China's auto exports are going global with incredible speed. China is now a net exporter of finished cars to the world (a huge shift).

It is also on track to become a net exporter of autos and auto parts to the EU by the end of the year. Germany take note!

27

277

740

A fact that may surprise some --

The euro area countries collectively export over 2x as much to the US as they do to China

(yet no one talks about how the German economic model depends on the US ...)

1/

33

200

718

Perhaps the most boring chart in the world

The shares of the major currencies in global reserves, as reported to the IMF.

1/

34

201

723

Dedollarization seems to be quite popular in countries that don't have any dollars left in their reserves ...

1/

24

139

679

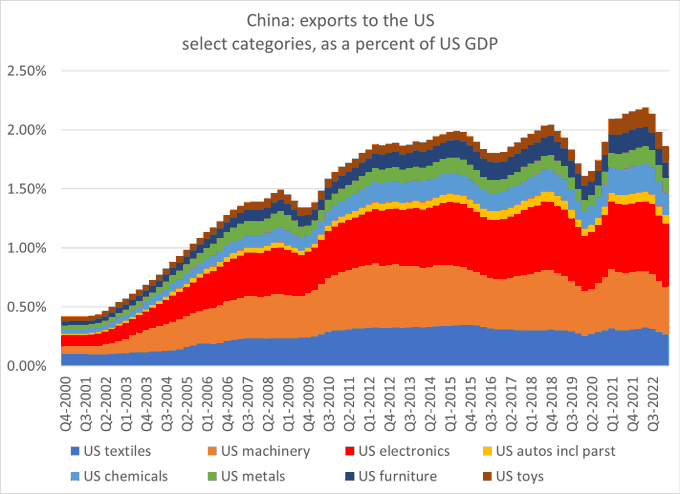

How significantly have US tariffs on Chinese goods changed bilateral trade flows between the U.S. and China?

A long thread

19

184

685

(Academic) economists no longer obsess over the balance of payments. And talk of global imbalances is now considered a bit stale.

That is a shame, because imbalances have actually exploded in the last few months, in an interesting way.

1/x

14

173

680

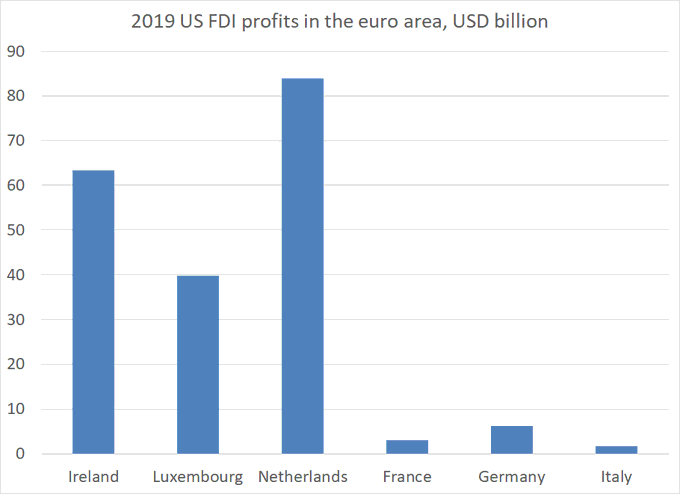

A little bit on the geography of the profits U.S. firms earn abroad ...

Say in the euro area.

Notice a pattern?

There is no real correlation between the size of the profits of US firms and the size of the country's economy ...

1/n

26

380

675

I am often surprised to learn that the tax avoidance shenanigans of large US companies aren't well known, even in DC.

And there are some rather egregious examples.

Take one large pharmaceutical company that gets the majority of its revenues in the US

1/

30

180

676

There is an enormous hole in the US trade data.

The New York Times reports that a billion (a billion, not a million) small value (under $800) packages entered the US last year.

$100 a pop, that $100 billion in unrecorded imports ...

1/

41

162

654

It is an enormous honor to be asked to volunteer for any transition, and I am excited to have been asked to help out this time around - but also very cognizant of the scale of the challenge we now face.

86

14

648

Musk really is testing the limits of the network effect. I have benefitted enormously from Twitter over time, and I don't have a comparably way to reach so many folks who actually understands fx, bonds and global flows.

But stripping out the link to a blog? kind of lame

30

78

649

China's December trade data is out --

And that is an excuse to take stock of the state of the world's export superpower.

Vehicle exports topped $100b this year for example (up from $15b or so in 2020)

1/x

24

180

624

Probably more than one chart crime here (from an unusual source -- the FT)

24

57

620

Argentina's plans to dollarize its economy should generate a lot of meetings in Beijing.

The pro-dollarization leading candidate for President may not realize that most of Argentina's remaining reserves are actually in yuan ...

1/

I know nothing about Argentinian politics other than that every four years they vote on which party will default next. However, I do know Argentina wanting to dollarize its economy is creating a lot of meetings in Beijing

24

46

251

19

160

615

Japan has been a big part of the global bond market for quite some time – both unhedged investors (the government, mostly) and hedged investors (the banks, the lifers ).

And Japan’s financial system report is still the best guide to really understanding the associated risks

1/

21

133

610

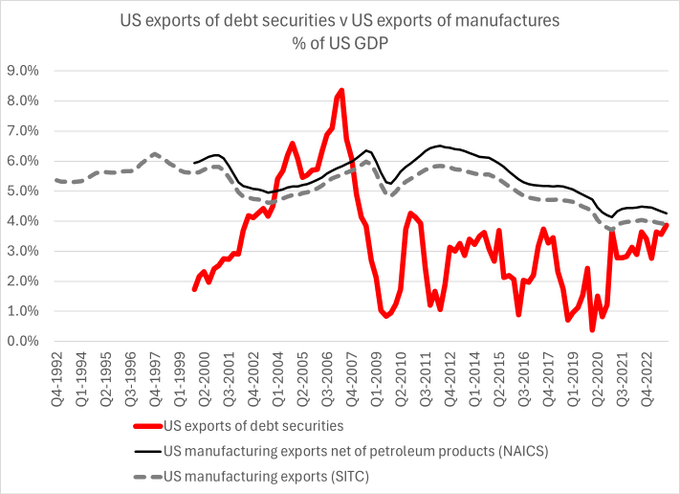

Lot of talk about the dollar as a US superpower.

What's undeniably true is that the US is especially good at exporting its debt securities, and uniquely bad (relative to its European and Asian peers) at exporting manufactures ...

1/

24

140

603

Proud to be joining

@USTradeRep

as counselor, and proud to be a part of the Biden-Harris Administration. Lots of important work to do.

70

62

602

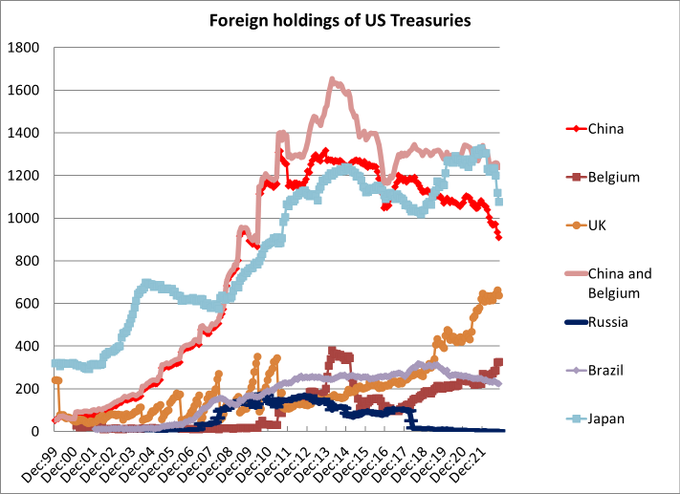

The most important thing to know about the US data on foreign holdings of US Treasury securities is that the US doesn't really know who holds US Treasuries --

The biggest holders (after Japan and China) are ...

1/x

32

140

591

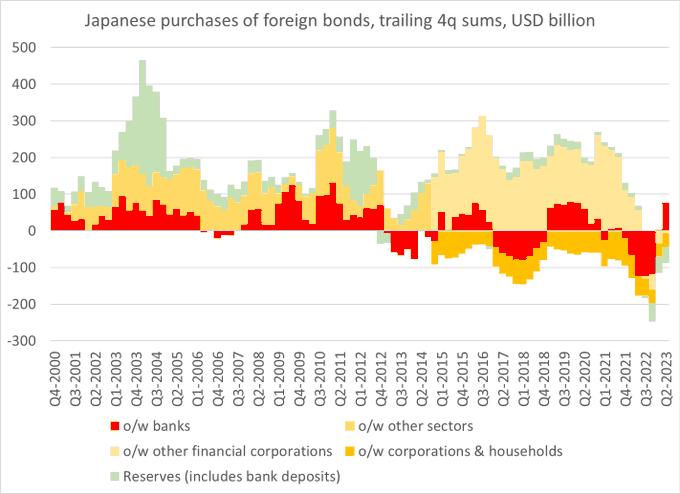

The fixed income flow from Japan is both huge consequential, and also (imo) very poorly understood.

The possibility that 10y JGB yields might be allowed to rise above 1 matters, but not precisely in the way many think ...

1/ many

10

126

599

There is now a bit of pushback against concerns about Chinese overcapacity. That is in part because the notion of overcapacity is itself poorly defined (capacity v domestic demand, v global demand or v the demand needed for decarbonization)

But there is a real issue imo

1/x

43

163

598

Turkey has blown through a lot of reserves this spring trying to prop up the lira -- reserves that it really doesn't have.

All its reserves and then some are borrowed.

A new blog

11

153

565

The underlying liabilities are in yuan, not dollars -- and the central government of China has a positive net worth (per the IMF's excellent recent paper) and no shortage of fiscal capacity to backstop China's financial system.

1/2

Bailing out China will literally take TRILLIONS of USD. $10 trillion wouldn't be a crazy number. Even if we wanted to, the numbers we are talking about are far beyond anything we could do

28

33

166

39

116

561

Excited to join

@USTradeRep

and the Biden Administration.

This change of course means I will no longer be writing a blog for

@CFR_org

. I want to thank all those who followed my blog -- and joined in the discussion of its key themes here.

56

35

560

Apparently, the folks at Davos debated whether the world is deglobalziing or reglobalizing …

I actually have a great deal of sympathy for the argument made by Niall Ferguson – namely that it is hard to “reglobalize” when there hasn’t yet been any real deglobalization …

1/x

23

161

550

I am back at the Council on Foreign Relations, and have returned to commenting on emerging market vulnerabilities ...

See this piece by Chelsey Dulaney of the WSJ

44

98

545

China faces a problem of internal balance -- inflation is low, and youth unemployment is high.

China also faces a problem of external balance -- even before the current slowdown. China's trade surplus (using the customs data) was at a record high v WGDP

1/

20

128

539

I have spent almost twenty years of my life looking at China's balance of payments data in one way or another.

Right now neither the current account numbers nor the financial account numbers quite fit together.

1/x

13

143

531

A hypothesis: there can be no durably stable Chinese and global economy so long China's national savings rate stays around 45% of GDP ...

(note that, contrary to the IMF's forecasts, savings has been rising since 2020 ...)

1/

40

124

537

Forecasts that the oil trade will de-dollarize are trendy ("For starters, a lot more oil trade will be done in renminbi"/ Rana Foroohar channeling Zoltan Pozsar)

But the petro-yuan faces one small problem: neither the GCC countries nor China needs financing from each other.

1/

22

142

540

Bloomberg has picked up on my China Project story outlining all the pools of foreign assets that China's government holds that aren't counted as formal foreign exchange reserves ...

1/

19

105

529

I think my bar for declaring that the US and China are really decoupling is far higher than that of the WSJ (or for that matter the IMF) --

I will believe it when the ultimate outlet for China's surplus isn't the United States

1/

19

133

531

Wow. There is really almost nothing new in the currency provisions. China has agreed to disclose material that it is already disclosing (basic information on its reserves and balance of payments)

1/2

26

291

494

Corporate America "earns" more money in the Caymans than in Canada (or China).

More in the Barbados than Brazil

More in the Isle of Man than in Italy

Almost as much in Gibraltar as in Germany

And more in Luxembourg than in France, Germany, Italy and Spain combined …

1/x

29

393

507

European criticism of the Inflation Reduction Act's narrow definition of friend-shoring isn't a surprise.

But it is strange that most of Europe now believes the IRA is a massive threat to European industry, while even more discriminatory Chinese policies are largely ignored

1/

20

147

518

Me, in the

@nytimes

(a first), with a simple message:

The offshoring of U.S. corporate profits is a real problem, and Trump's tax reform if anything made the problem worse.

39

282

499

The "dedollarization" of global reserves is in the news today. Geopolitical fragmentation too.

But there is one surprise in the US data that hasn't been reported -- China doesn't appear to have changed the dollar share of its reserves since 2012.

1/

12

153

513

It is a bit hard to believe that any story involving China has been underreported, given China's large role in the global public debate.

But China's transformation into a major auto exporter has been wildly underreported.

(see the hockey stick in exports of finished cars)

1/

19

150

505

The "deglobalization" of the world's auto industry continues.

Chart from the WSJ, h/t

@scienceisstrat1

1/

28

144

510

President Macri was elected on a program of ending Argentina's capital controls and getting Argentina out of default (on its international bonds). So there is a deep irony that Argentina will have come full circle by the end of his term ...

1/x

13

203

498

Waiting for the day when the tax avoidance strategies of US multinationals generate as much sustained attention as "de-dollarization"!

10

98

502

Great line from Jörg Wuttke:

“People always talk about how China is a big market — no, China is a huge economy with a small accessible market"

Wuttke is the head of the European Union Chamber of Commerce in China

1/3

14

139

498

Strange timing from Fitch. US debt to GDP is heading down, the term premium is negative (suggesting strong demand for long-term bonds), and the only likely point of bipartisan consensus in this Congress is to avoid a an avoidable default ...

1/

36

106

501

The market thinks -- correctly in my view -- that an Erdogan victory would increase the risk that Turkey ends up defaulting on its (non-trivial) stock of dollar bonds ...

1/

21

150

494

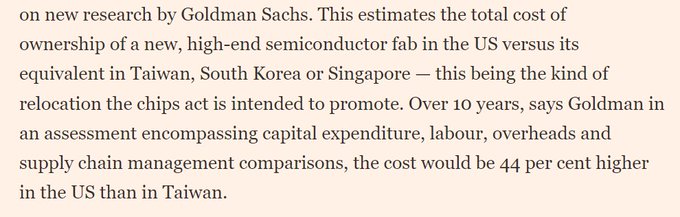

I am a bit of a broken record on this topic.

But the economics of semiconductor production in the US relative to Taiwan and Korea (or Singapore for that matter) cannot be entirely divorced from discussions about these countries' exchange rate policies over time.

1/x

22

112

478

More evidence that President Xi is personally opposed to household stimulus:

-- One Chinese told Raimondo that Xi fears “consumer fiscal stimulus might make people weak.”

From the David Ignatius story on Raimondo's trip

68

128

476

The fact that a profitable company like Nvidia (now valued at around a trillion dollars) pays next to no US federal income tax should be much better known.

15

158

487

I tip my hat to Martin Wolf's chart game, which remains unsurpassed.

Great, great chart --

Massive swings in China's bilateral balance with the EU, the UK and Japan over the last three years.

8

108

482

I know this is a somewhat controversial position, but I have trouble taking Singapore's defense of "pure" globalization seriously ...

Singapore defends its interests of course. But its tax policies have done more to distort global trade than the US inflation reduction act.

1/

33

153

484

Seems like Apple, Microsoft and Big Pharma have decided to gift Ireland a sovereign wealth fund.

1/

13

111

480

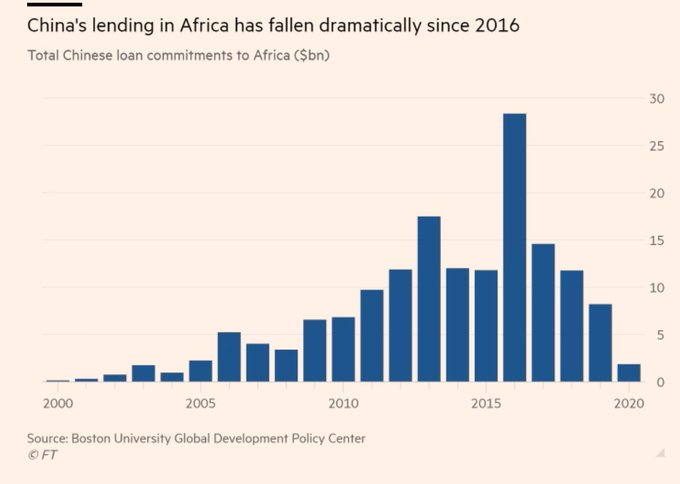

Strongly suspect that if we had the current data, China's net flows to Africa have turned negative (repayments exceed new loans).

Most China ExIm loans have a 5y grace on principal so the 16 loan spike is now reversing

1/

19

157

471

The World Bank's international debt statistics highlight a fact that is both well known, and gets insufficient attention --

Financial flows to low income countries (and Africa) have dried up

1/x

11

209

478

All banks borrow short and lend long, playing the (typical) shape of the yield curve (& drawing on the stability of most short-term funding most of the time)

But anything taken to the extreme can become a source of risk. Silicon Valley Bank clearly took things to extreme.

1/x

19

115

473

The U.S. Treasury it seems has decided to name China a currency manipulator roughly 12-13 years after it should have first named China, and roughly 5 years after China stopped manipulating ...

(1/x)

17

221

463

With China defending the yuan (so far through the state banks) and the yen approaching levels where Japan might intervene, the impact of foreign central bank reserves on the Treasury market is getting new attention ...

So it is worth reviewing the basics.

1/

8

95

458

Novo Nordisk:

a) pays income tax at the Danish corporate tax rate -- an effective tax rate of 20% v the 22% headline rate ...

b) pays the bulk of its global income tax in its home country (Denmark)

1/x

Two gold stars for Denmark:

🌟for the highest capital gains tax rate in Europe according to this

@taxfoundation

compilation

🌟for being the home to Europe's largest, most valuable company (Novo Nordisk)

Taxes are not at odds with innovation and growth. They actually support it.

6

17

46

13

106

465

China likely lost its chance to stop the US from pivoting towards a policy that tries to compete with Chinese subsidies in key sectors (rather than get out of the way and exit) when it didn't accept real constraints on its subsidies during the negotiations with Lighthizer

Bidenomics with Chinese Characteristics: The US is now embracing an industrial policy strategy that is comparable to the same approach it has long criticized China for. See my latest blog dispatch.

40

94

327

26

91

457

I agree with Pettis.

Pozsar gets this one wrong. The US to my knowledge has never asked for countries to run bigger trade surpluses, to engage in more currency manipulation and as a result to buy more Treasuries.

1/3

Interesting article, but with a pretty bizarre quote from Zoltan Pozsar: “The west dreamt of the Brics as a lapdog, that they would accumulate dollars and recycle them into Treasuries, but instead of that they are renegotiating how things are done.”

62

353

1K

39

62

458

A new blog with the details of how China has hid a significant portion of its reserves over the last 20 years.

Technical, with tons of links to source documents.

25

120

458

The VCs didn't step up with the equity infusion needed it seems, or (best I can tell) even really try.

The USG did the right thing to protect the economy -- using its emergency authority to save (big) deposits and assure that payrolls are met. Only the government can ...

12/

24

74

446