Skwigglylines

@skwigglylines

Followers

889

Following

90

Media

234

Statuses

1,577

Explore trending content on Musk Viewer

Rafah

• 1328043 Tweets

井上尚弥

• 276524 Tweets

Inoue

• 162781 Tweets

Stray Kids

• 125192 Tweets

RPWP IS COMING

• 82375 Tweets

ボクシング

• 70517 Tweets

#رفح_تحت_القصف

• 44047 Tweets

モンスター

• 38671 Tweets

Bruno Mars

• 36326 Tweets

#MetGala2024

• 29163 Tweets

Kim Namjoon

• 29024 Tweets

GW終了

• 27191 Tweets

井上選手

• 26673 Tweets

逆転3ラン

• 24972 Tweets

筒香のホームラン

• 21905 Tweets

20 YEARS OF MINJI

• 20200 Tweets

AESPA SUPERBEING TEASER 1

• 18511 Tweets

#GWを写真4枚で振り返る

• 18360 Tweets

Białoruś

• 17710 Tweets

Bernard Pivot

• 16036 Tweets

MIOTO NO VENUS PODCAST

• 15923 Tweets

#MIvsSRH

• 15143 Tweets

#VurPençeniKupaya

• 12723 Tweets

#Superman

• 11166 Tweets

横浜優勝

• 10044 Tweets

David Corenswet

• 10011 Tweets

Pinned Tweet

Finished reading Pulak Prasad’s book. I haven’t waited as desperately for a book as this one and it was really extraordinary. There are enough summaries of the book, so I am not gonna write another one, but I’ll share two overwhelming feelings I was left with after the book.

+

11

23

189

One common pattern I have observed with successful long-term investors is their (almost) complete disregard for sell side equity research. Disregard not disrespect. My first boss in investing told me “seek equity research for historical data and not for their opinion”

+

2

21

133

BSE Real Estate index is up 75% this year. It’s up 165% in 3 years. Here’s a cautionary tale for (especially young) investors getting excited about the space now.

+

6

13

87

Of all the investing related topics that I discuss with my close set of friends in the business, “hold forever/don’t sell on valuation alone” is the topic that we have the toughest time building a framework on in a way that makes intuitive/mathematical sense.

+

4

14

75

"Nothing sedates rationality like large doses of effortless money"

- BRK, 2000

(Good reminder for present times)

0

14

62

No wonder Anand looks forward to his Mondays.

Do not miss this book. Reading foreign investment legends is one thing. Reading someone who has lived through the same market cycles as we have and invested within the same listed universe as us, takes this to another level.

3

0

45

Just like Pulak and Anand believe reading Ben Graham’s book, reading Buffett’s essays and Chapter 12 of Keynes are all there is to required investment reading, I believe that Pulak’s book will become part of folklore as essential reading for every long term investor.

+

4

2

40

I am envious of the environment Pulak and his colleagues have created at the firm and what deep satisfaction it would provide to be in that space every day. I can only imagine and envy what it must be like to work in a group where you can ignore every bit of surround sound

+

1

2

38

First was gratitude. We’re truly lucky for the generosity with which Pulak has shared his knowledge and approach. It’s such an in-depth first person account into the mind of an extraordinary investor and human being and how he’s built a stellar organization.

+

2

1

35

Read this essay for the 5th or 6th time since

@SridharanAnand

wrote it. I revisit this often and feel amazed every time, for how counter intuitive and contrarian it is to the norm in our industry, but makes so much sense.

Can't recommend this enough!

2

4

33

4 use cases of attending sell side conf:

1. Free coffee, food and alpenliebe

2. Temp check of different parts of the mkt, the Howard Marks way

3. Seeing characters in our business – from slick Hong Kong hedgies in $500 blazers to dimwit gen Zs taking live notes on their phone

4

2

33

Listened to an endowment allocator managing $160B. Of this $100B is in global passive index, has reduced external managers from 150 to 15 over time, his mantra "life is hard, do simple things, be lazy and chill". Unusual clarity managing money at such scale. Refreshing.

1

1

30

Envious of not having to worry about high leverage blowing up a portfolio company, because there isn’t any to begin with. Envious of living with zero FOMO. Envious of focusing only on great buy decisions and not have to make sell “price” decisions.

+

1

0

30

Great case study on why nothing is worth paying a nosebleed price, no matter how stellar the management, business, track record, industry tailwinds etc.

Kotak Mahindra Bank is now trading at it's lowest price to book valuation in the last 10 years.

From 6x to 3x P/B in just 5 years, a stunning 50% valuation derating by Mr. Market.

However, both earnings and book value have compounded at more than 15% in the past 5 years.

45

38

415

1

0

29

Stoic company -> meet stoic investor.

Father-in-law owns Hawkins shares for 42 years. Few years ago he made me visit their Mahim office to buy a saucepan in exchange of discount coupons he receives every year as a shareholder.

"We make cookers & related stuff. We're very good at it & get stronger by the year. Since market fluctuates, our numbers fluctuate but we're doing fine on controllable factors. BTW, we're sending you all surplus cash. Ok bye, till next year. " - there's nothing to add to MD&A.

5

1

88

1

1

27

This. Is. It.

This is the job.

Say no to 98% things. Wait for remaining 2% to become unloved and trade below median valuation. Avoid shitty industries and people. Keep working hard to hone that 2% list. Sit on your ass.

So easy. Yet it's not.

@Doubledecacorn

Over 15-years & ~40 decisions, our average/median is 15x entry PE (on historic/trailing E) for 40% ROCE business. We've tried to not buy sub-20% ROCE biz. Tried to not pay >25x PE irrespective of how excited we are about biz. I think we'll stay within these bounds in future too

10

10

109

1

2

28

Discretionary growth will go through the roof once India crosses $2k/capita, is a thesis that's been peddled ad nauseum for last 10 years. How is this a helpful data point for investing anyway?

5

1

27

How to know someone's age (in markets) without asking their age? Exhibit A.

More money is lost by cribbing about High valuations & avoiding an opportunity, then by actually losing money due to high valuations.

Remember that downside is always 1x while upside couple be multifold.

3

0

30

3

0

26

Leaving Mumbai for good after living here exactly 10 years. Moving to a (relatively) quieter city, will work remotely from a couch, hoping to improve both my health and investing. Thank you, Mumbai. It’s been fun!

4

0

26

Do you know why young investors (career age not biological age) have a distorted sense of valuation guard-rails?

Look no further :

2

5

26

"We ignore EVERY piece of proximate macroeconomic information. Their weightage in our investment decision is a big zero" - Pulak Prasad

Another one worth pinning on the desk

2

1

24

It’s not just some loosely hanging meanderings put together. It’s got actual portfolio case studies, evidence that this method works, how they arrived at certain decisions, lessons from mistakes, what questions to ask and so on.

+

1

1

25

of macro, sellside, TV anchors, RBI announcements and focus day in and day out sitting on your desk and reading about companies. I am envious of a culture where you can filter out 90% of stocks within 10 mins and focus all your energies on sifting through the leftovers.

+

1

0

25

If a lending business is premised on lending to people who really need to borrow Rs. 15K, it’s not a business at all. As Fred Schwed wrote in 1940 - “A (good) banker’s business might be defined as lending of money exclusively to people who have no pressing need of it”

0

1

24

2023 wins and (humble) brags:

- switched 95% caffeine intake to black coffee, material fall in sugar consumption

- deleted Instagram

- learned to make exotic looking salads, minestrone soup, eggplant parmigiana and a kickass hummus (been cooking desi food forever)

+

2

0

23

For this analyst it’s an occupational prerequisite to wear recency bias tinted glasses while looking at a business. How often do you seen an equity research note with a buy call on a business which is undergoing pain that’s expected to last for a couple of years? Almost never.

+

2

1

23

Investing permanently might be a useful remedy for our contemporary evils.

- Keynes, Chapter 12, General Theory

1

1

23

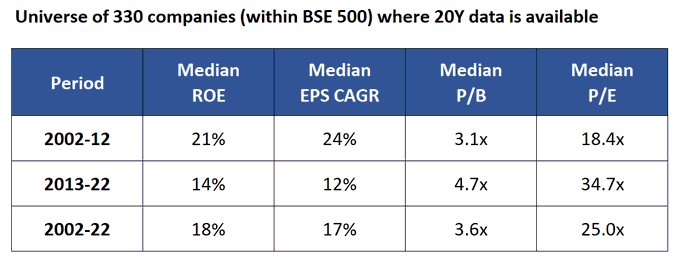

When I was growing up, no growth valuations were 6-8x earnings 😱

They don't make that kinda prices anymore.

Have seen a lot of decent midcap & smallcap at no growth valuation of 15-18x earnings

Mastek

Xpro

Aarti industries

Niit

Angel one

Vaibhav global

Imo if one can study & form even a 2 year view here (stock specific), many would create wealth

25

36

335

3

1

22

It’s advice I have come to appreciate more as I got older in this profession. Not because sell side does a poor job at research but because they have different audience and objective function. Their target customer wants to know what’s likely to work here and now.

+

1

1

22

My first boss thought of growth and valuation in a way I havent seen elsewhere. He said:

-any growth rate above ROE/ROCE is irrelevant

-value a business for what it is today and not for what it's going to become

I remind myself of these often and get amazed at the profoundness

6

0

21

"The origin of every lousy investment is a good story" - Pulak Prasad.

This is so true.

1

0

18

"To a fund manager, large and growing are two words that sound better than Beethoven's symphony."

- Pulak Prasad.

😂

0

1

18

Of countless notes in the mailbox and twitter explaining why HDFC has disappointed lately and why it’s a great idea from here on, didn't come across even one that mentions these two words – mean reversion.

+

2

1

18

In most cases that data is insignificant, usually included by the analyst to show needless rigor and can do you more harm than good, but on rare occasions it could lead to a useful insight.

1

0

18

75 pages in. Early warning if you haven't started - read this at your own peril. There's a 90% chance the book will induce major existential crisis. The What-am-I-doing-in-my-career-and-life kinds.

To my (and Pulak's) surprise, Pulak's book released on March 13, ahead of it's planned May release. Amazon India shows Kindle edition available. Unfortunately, no separate India edition (and pricing) yet. In US, hardcover should available in a few weeks.

14

6

88

3

0

17

Equity research can be useful only after you’ve read every piece of publicly released information by the company on its own and developed an independent view.

+

1

1

18

Hold “for how long” must be in NEAR COMPLETE HARMONY with hold “what”. The probability that long hold periods will translate to better returns goes up materially ONLY if you have a very high bar on business quality, management integrity and promoter ownership structure.

+

1

1

17

(Almost) Every sell-side analyst report should come with a standard 4 word disclosure right at the top:

"Beware: Recency bias ahead"

2

1

18

@SridharanAnand

Market's so bad that...family whatsapp groups are back to exchanging good morning messages instead of discussing grey market premium on new IPO

1

2

16

The second feeling I had was of extreme envy. I know envy is the worst of the 7 sins, but I couldn’t help it. I am NOT envious of Nalanda’s track record, their AUM or personal wealth that the team would have accumulated.

+

1

0

16

Highlight of the conference season has been CFO of a cement company shutting up the room with: "I know why you folks won't get it. You are thinking 12 months, we are thinking 20 years"

3

1

16

Thread: London based Nick Sleep and Qais Zakaria of Nomad became well known in last couple of years when some of their letters to their investors and their stellar track became public. Subsequently they decided to make all their letters public. Here’s my summary from the letters:

1

4

16

Worth pinning this line from Pulak Prasad on your desk:

"A strong balance sheet is not the one that

maximizes debt to minimize the cost of

capital, but the one that minimizes debt to

maximize the safety of capital."

🙏

0

1

15

When you’ve read everything that’s out there (website, AR, investor presentation, con-calls, promoter interviews) and then you get to a note written by a third party, it makes for an incredibly satisfying feeling to be able to tell apart objective analysis from gibberish.

+

1

1

15

@contrarianEPS

They will take IPO subscription money from one nostril and throw out shareholder value from the other

1

1

16

1/ Thread on IPOs. Investor behaviour in IPOs fascinates me. I understand retail investors enthusiasm for the lust of making listing day gains, but seeing a slew of professional money managers lining up to get IPO allocations baffles me.

1

3

15

Even though those are some of the best opportunities for long term compounding. Likewise, how often do you see a cautionary note on a business that’s done incredibly well lately but is priced up to its eyeballs.

+

1

1

15

In fact its quite the opposite. If you avoided every one of those industries like a plague, you are one step closer towards becoming a better investor (not punter).

As the brightest amongst us all said - "good investors are good rejecters"

4

0

14

@Suhanaenae

American colleague - going camping for summer, see you in sep

European colleague - going skiing in winters, see you in March

Indian bloke - going for my kidney transplant, available on phone if urgent.

0

3

14

"If we are to disappoint you, we would rather it be with our earnings than with our accounting"

- BRK, 1998

0

2

14

Only after that will you be able to parse through a sell-side note for what is thoughtful analysis of the business and what is just an opinion that may not be wholly rational for long term thesis.

+

1

0

13

Small talk is exhausting. I have to make prep notes before a work trip to the US -

- temperature in Fahrenheit of city i am in (weather topic in US is equal to traffic topic in India)

- did their local team win baseball/footy/NBA recently

- elections/gunfire/coffee fads

A huge reason indians are so poor at professional networking is because they’re bad at western style small talk. They either communicate too transactionally or become too personal.

371

610

8K

2

1

13

A very senior analyst asked a management - "what are some positive surprises we should expect in the coming year?"

Kamaal hai yaar.

3

0

12

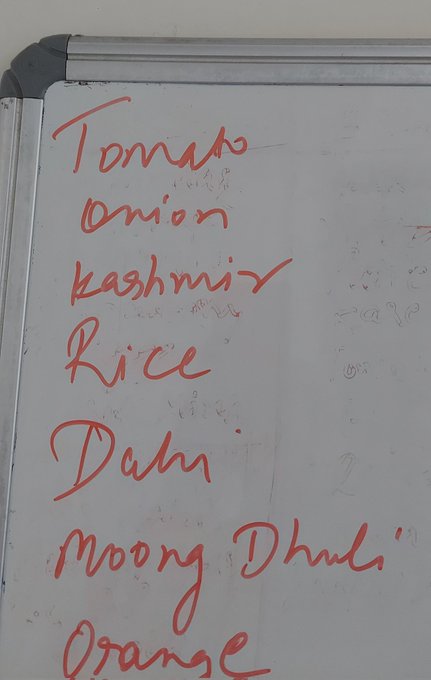

Me: Isn't your shopping list too aspirational?

Wife: Shut up, it's Kashmiri lal mirch

5

0

13

Buffett's ability to make serious investment arguments with the most beautifully crafted metaphorical prose is bar none.

This is him talking of M&As

- BRK, 1981

3

0

13

Was hoping to see you at the kachori station today at a big sell side conference. Happy teachers day

@SridharanAnand

. Following Nalanda closely over the years has been formative and reading your essays has helped solidify(ing) a lot of those learnings. Thank you.

1

0

13

ICICI Bank:

2002 - 2007 – Quality private sector bank

2007 - 2012 – PSU bank

2012 - 2019 – PSU bank with tie and cufflinks

2019 - 2021 – Private sector bank

2021 - 2023 – Quality private sector bank

2024 - Quality private sector bank with a tuxedo

1

0

13

In my experience, this trifecta is easier to spot in others' portfolio and not in one's own.

What is one of the best times to sell a stock?

When we have triple peak

Peak margins

Peak valuations

Peak enthusiasm (you feel dumb selling the position)

May not work in 100% of cases, but the odds are good. At a minimum, reducing weightage makes sense

5

12

125

1

0

13

Nothing happened in capital goods companies share prices from 2013 to 2020. Most of them are up 3-5x in last 2 years, even though underlying earnings have still not improved meaningfully. The only thing that's changed is optimism visible through order books, commentary etc.

1/4

1

1

12

In contrast, some cyclical industries such as engineering or capital equipment yield ROICs north of 40% in good times and 5-10% in bad, resulting in long term ROICs of >20%, making them high quality cyclicals.

+

1

0

12

It also helps you recognize and reflect on your own bias. Though limited utility, why I still recommend reading these notes after your independent work instead of dismissing them outright, is because they sometime contain data that you might not find easily.

+

1

0

12

Visuals on the screen put our careers about sloshing money to make more money into perspective.

#Chandrayaan

0

0

11

RE isn’t just cyclical, it’s a poor-quality cyclical. BEST years mean 15-20% ROIC, but poor years come with <5% ROIC. Averaged out almost nobody makes more than 12% through-cycle ROIC.

+

1

0

11

Debt free businesses with terrific ROCEs that have gone out of people's mind just coz of 5-7 years of underperformance due to low growth are a great place for research. Remember - business quality is lot more persistent while growth goes up and down in cycles.

1

1

11

RE is amongst few industries where capital allocation mistakes have very long feedback loops. The fact that a company bought a shitty piece of land or overpaid for it will only be known 5-7 years out, even as every new land purchase is celebrated in present

+

1

1

11

Lastly, in lived experience, there is way less temptation to sell a frothy winner when there is high comfort that I have partnered with decent people and business, but feels much jittery if there was a speck of dodgy-ness in the business niggling at the back of my head.

4

0

9

@Kritesh_C

It's not a luxury. It's a right they have earned due to what Charlie Munger calls a "seamless web of deserved trust". Their investors allow them the capital call option because they have "behaved" well with that option. Most others , if bestowed with the option, would misuse it.

2

2

11

What are we pricing in:

- SIP flows are unstoppable force

- abhi FII to waapis aane baaki hain

- duniya mein aur kahan hai itni growth

- trailing chhod, 5Y forward dekh

There are 1200 firms with a Mcap of 1000cr or more on NSE. Ex of the first 500, the firms from 501 to 1200, have an average PE of about 70. If you remove the 5% outliers the avg is about 40. What are we pricing in?

Data source: Bloomberg, trailing PE numbers.

16

21

194

1

0

10

In public service, can all people who love their work stop tweeting about it, for common folk to not feel miserable about their lives?

If you love your work, Mondays wouldn’t bother you

Nothing and no one can possibly bother

All botherations, if any will have one fate - disappear

0

0

0

2

0

11

Every bottom up bet has an assumption that Indians will consume more, borrow more, cos. will build more capacity and govt will put infra etc. But none of this makes it macro investing. Macro that Swensen refers to is betting on int. rate, currency, economy, inflation type bets.

"People always forget that 50 percent of a stock's move is the overall market (macros), 30 percent is the industry group and maybe 20 percent is the extra alpha from stock picking."

Do you agree?

14

8

105

2

1

10

Highlight of the conference season:

“Sir, I had a question for the medium term, pertaining to next 9-12 months”

2

1

10

"I have one standard set of advice for all difficulties, suck it in and cope. That's all any human being can do, suck it in and cope."

- Charlie Munger

0

0

10

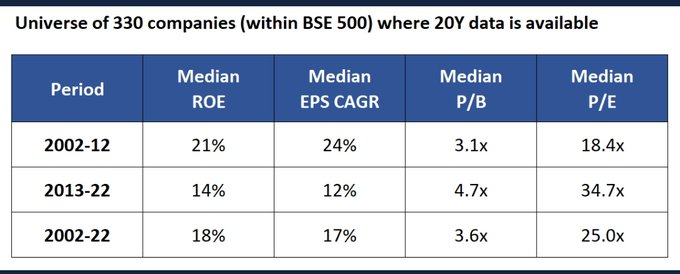

One clarification here: The EPS growth number I used were 5Y moving average over 20 years, to avoid start or end point bias.

Do you know why young investors (career age not biological age) have a distorted sense of valuation guard-rails?

Look no further :

2

5

26

0

0

10

1 poor capital misallocation, irrespective of intent, can wipe several years of strong returns. Look at how many developers are still licking their wounds from stupid land deals based on hope or developments done in middle-east 15 years ago.

+

1

0

10

In summary, hold

“what”

“for how long”,

“for what kind of investors”

“from what starting valuations” and

“with what return expectations”

all need to be in very high degree of synchronization to work well.

+

2

2

10

Thread (more like a rant) on FMCG valuation! For a while, I have gawked at the valuations of Indian FMCG stocks and never been able to rationalize them. However, I have tried now to consider them from a few more dimensions:

1

6

10

Hold forever would not work if you don’t allow valuation to be a long term tailwind or at least not a clear headwind from your entry. Buying quality at top quartile starting valuations is a recipe for subpar returns, because all the goodness would be negated by mean reversion.

+

3

0

8

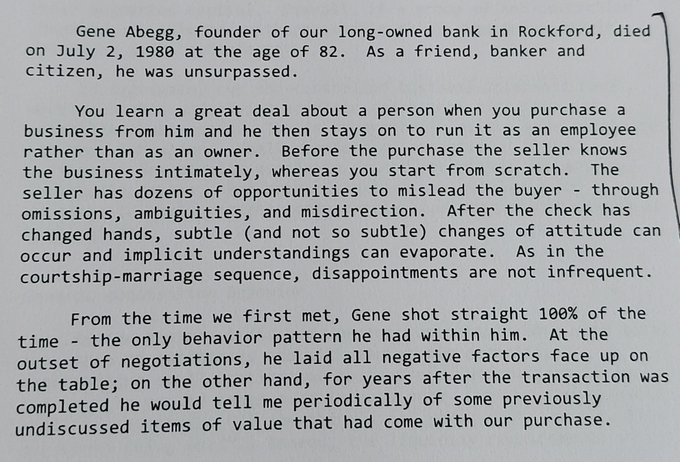

They don't make bankers like Eugene Abegg anymore.

BRK, 1980

1

1

8

Nothing really comes close to the intellectual satisfaction derived from filing income tax returns without taking help from a C.A.

0

0

9

"Tell people what they want to hear and you can be wrong indefinitely without penalty." - Morgan Housel

0

1

8

The only good thing VCs have done for public equity investors. We can now afford to make a decent avocado toast on sourdough at home. 😋

1

2

9

Loved this exchange from Munger's podcast chat. Especially how he ends it.

3

0

9

Holding period also needs to sync with the nature of your capital flows. Prashant Jain is a stellar money manager. In his MF career, the nature of his capital flows and his limited control on the same meant he had to choose an investment style that can loosely be defined as:

+

2

0

8

@FalakKalyani

Until last year, I had only read stories, quotes and books about Buffett & Munger written by others and believed that I understood their approach well. But reading original letters in chronology, with proper context to each investment, seeing B&M's thinking evolve over time..

1

1

9

On twitter as well as in the mailbox, suddenly everyone has become excited about large well-run private banks (you know which ones I mean) just because share prices have started to move up after a long lull. The level of intellectual dishonesty in our brethren is jarring.

2

0

8

If you are like me and find analyst reports on insurance overwhelming with low signal to noise ratio, read 1990 letter to shareholder from Berkshire. It’s a masterclass on insurance 101.

1

0

9

Existential crisis alert:

PSU banks and other unloved stocks blazing this year makes for such a strong case for why index investing should work for most.

+

3

0

9

Continuing to own a wonderful business at toppish valuations fully knowing that from that point the returns are likely to be modest at best is not an easy decision. The reason this still works is because a portfolio of high quality business probably unfolds in two ways, IMO.

+

1

0

7

"We invested more in the next three months than we had in the previous six years."

Charansparsh!!!!!!!

In my latest not-so-humble-brag essay, I look back at March-2020. It feels a while back, but 3-years isn't that long. I rehash some investing lessons that served us well during March-madness & which hold true at all times. As always, nothing new here.

13

24

111

1

0

8

I have come to love things like cold brew coffee, croissants, undercooked omelettes, dark chocolate, avocado toast, crepes. My wife finds it incongruous to my desi upbringing. She calls it wannabe. I call it a refined palate. 😀

3

0

8

Returns since then: A = 1.8x, B = 4x.

(Not invested in either.)

Cherry picking? Yes, I know. Think of it as a smell test to judge what's super hot and therefore PROBABLY priced in vs. what's currently despised and therefore MAYBE a bargain.

2

0

8

@SridharanAnand

Tell me a short Private Equity joke.

Value-add

Tell me a short M&A joke.

Synergy

Tell me a short LP joke.

Uncorrelated portfolio

Tell me a short Investment Thesis joke.

Earnings visibility

Tell me a short Underperformance joke.

The joke is on you, Mr. investor

1

1

8