David Orr

@orrdavid

Followers

20K

Following

44K

Media

2K

Statuses

30K

I run the long/short $ORR ETF - https://t.co/VarMOIVCah I also run Militia Capital, a long/short hedge fund.

Osaka

Joined December 2009

The Militia Long/Short Equity ETF has launched! The ticker symbol is $ORR and it just began trading. The strategy is similar to my hedge fund, investing in global stocks up to 150% long and 100% short. This strategy will typically have lower correlation and beta to the market.

36

20

347

"The value is there, someday you will realize it! Mr. Market is just being irrat- Oh.".

0

0

5

They were stealing from shareholders in other ways before this, which lead to a beaten down multiple. And now this finishes the job. $FONR. Thieves. I don't know why I haven't been short the whole time. Sometimes, I really overcomplicate investing.

$FONR crook management announced takeunder offer for $17.25. Maybe they will lift it a bit but yeah, typical end to a deep value microcap shitco saga. Management kneecaps the right tail.

3

1

15

RT @markku_kurtti: @orrdavid Parameter uncertainty will decrease optimal leverage and its impact can be modelled by volatility of volatilit….

0

1

0

RT @ArkkDaily: Cathie Wood and Ark Invest's $ARKK just had its largest ever single day of inflows per @EricBalchunas. $800 Million https://….

0

20

0

RT @TidefallCapital: Sub $200 again. First time since the pandemic. Not going long $LULU until they fire CEO and CMO.

0

4

0

And if you want to be a bit arrogant and say I'm super sure, fine, go to 15% or something. But this 30% bet stuff is junk.

1

0

8

Zooming out, why I think I'm finally comfortable with the framing in this thread:. Even if you think a full Kelly bet is 50% - which most likely is just overconfidence - you still arrive at a 12.5% position size for a quarter Kelly bet. Outlier talent that truly isn't being.

2

0

7

$13 for a ticket to see a consumer brand's history and processes. Very crowded in there. 21x earnings and in a likely short term trough.

0

0

0

Makes me want to buy more of the stock. Seems a hard brand to recreate.

1

0

2

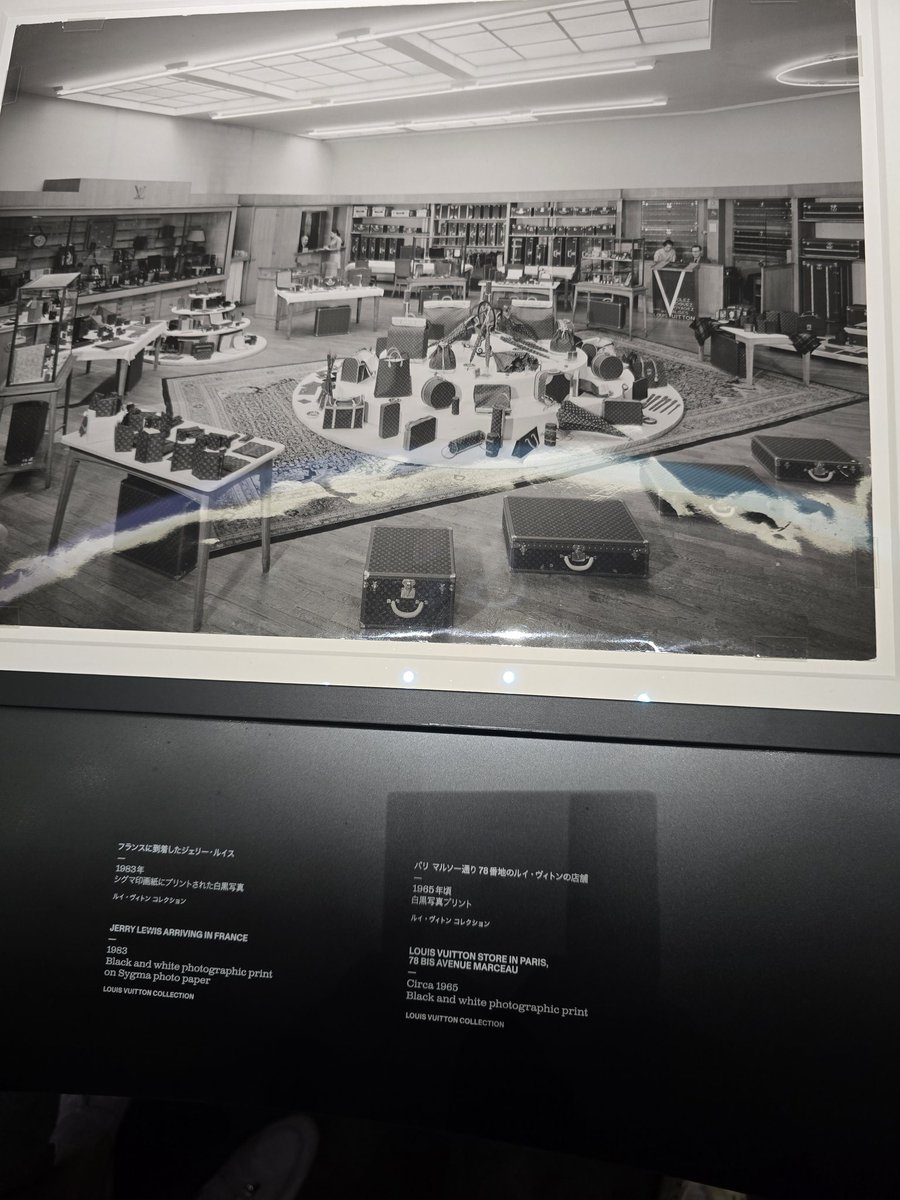

$MC Louis Vuitton doing an exhibit at the Nakanoshima Museum of Art. Pretty cool, shows the history of the company from early days to today.

1

0

7

6 months is a decent timeframe for not staying wrong in modern markets.

1

1

13

Listen to the best investors. Ignore them at your peril.

When something works, increase size; when it doesn’t, reduce quickly. - George Soros.

3

3

52

The only real counterargument I see is that the stock bet doesn't have the same 100% downside risk as the coinflip bet. But the upside isn't as big, either. The unknown correlation aspect, especially while using leverage, means the downside is often a lot bigger than it seems.

4

0

18

I've thought on this topic for years, and I finally feel comfortable with this framing of optimal bet sizing in stocks.

1

1

18

Steve Cohen trained an awful lot of traders. He said the very best ones win around 60% of their bets. Assume a favorable distribution of outcomes, maybe we adjust that to 65%. And for the higher edge bets, that's maybe 75%?. Kelly = 50%. Half = 25%.Margin of safety size with.

3

3

31

I think this is where the ~10% full bet size being good comes from. Even that is pretty aggressive, but most likely fine for a handful of bets like that. If someone regularly bets 30%+ on things with big downside risk, I will assume they don't need to improve risk management.

1

0

17