Kshitij Anand

@kshitijandquant

Followers

3K

Following

282

Media

99

Statuses

750

Quant Risk Analyst | Someone who loves Quantitative Finance

Gurgaon, India

Joined November 2024

VIX derivation explained:- A really good mathematical exercise. Please DM me in case of any doubt. https://t.co/DT6ResAGXb

drive.google.com

0

3

62

Maths time!! Derivation of VIX:- A really good blog written by Mr. Gregory Gundersen. https://t.co/KhK2XKFdXB I will soon release a video explaining the derivation, along with the derivation of the India VIX as well. #Quant #QuanitativeFinance

0

2

51

Lambda functions from C++11 to C++23 by Quasar: https://t.co/JG4QHDrWnv Do bookmark his blog for really good insights on C++ for Quantitative Finance.

1

10

90

Algorithmic Differentiation:- > Multiple Risk Factors > Need to calculate sensitivities across all of them > AD makes it fast Do read the notes I have prepared on AD:-

linkedin.com

Algorithmic Differentiation: An Extra Mile Toward Efficient Computation In Quantitative Finance, we often deal with multiple risk factors and need to compute sensitivities to those factors, whether...

0

2

8

A good collection of blogs on Cpp for Quantitative Finance written by a guy who is working at Citadel as Quant trader. https://t.co/NjdnGyU4L8 If you have more such blogs on cpp, do share in comments.

6

49

741

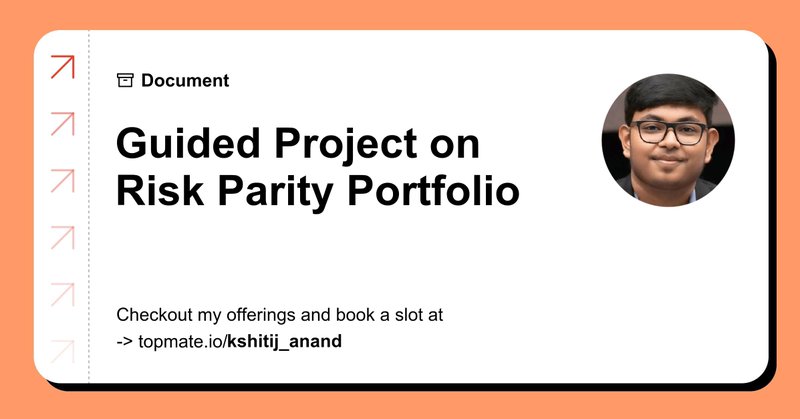

I remember a project that I did long back using KKT; it was risk parity portfolio optimisation. The mathematics behind risk parity portfolio and this particular Optimization made me learn a lot. Absolutely amazing!! Project material btw:-

topmate.io

Risk Parity Portfolio Implementation

Karush–Kuhn–Tucker (KKT) conditions characterize optimal solutions of constrained optimization problems by linking gradients, constraints, and multipliers. In probability, they guide maximum-likelihood estimation under constraints. In machine learning, they shape SVMs,

0

3

24

A frame which will display live volatility surface while I cook (the trade?)!

2

2

14

Can someone familiar with Hedge Funds confirm whether hedge funds still use index-rebalancing strategies, or has the opportunity become too dry to extract any juice? #Quant #Hedgefunds

4

0

50

I support Quant Club at @febsiitbbs because I am one of the founding member and they are doing quite good in Quantitative Finance. 🙂🙂

0

1

12

Suppose the ATM implied volatility is 25% when the index is at 200. If the index rises to 220, the sticky-moneyness rule says the 220 strike option (now the new ATM) should carry the same 25% implied volatility. That’s exactly why we call the behaviour sticky moneyness / sticky

0

0

0

Sticky Delta, or Sticky Moneyness, implies that the implied volatility will adjust so that the Delta of the option remains constant even when the underlying stock price changes.

1

0

0

You hold a put option on stock ABC with a strike of $100, and the stock is currently trading at $100. Now the stock drops to $95. Under a sticky strike assumption, the implied volatility for the $100 strike put stays the same, even though the underlying price moved lower.

1

0

0

Sticky Strike Vs Sticky Delta Sticky Strike refers to a situation where the implied volatility (IV) of an option remains constant for different strike prices, even as the price of the underlying asset changes.

1

0

0

Both sides of the market (importers/exporters, global funds, banks) hedge moves in both directions, which lifts volatility on both wings. Because of this two-way hedging and generally more symmetric return distributions, IV ends up rising on both sides of the strike axis, giving

0

0

0

An interesting but easy question, why do we observe an Implied Volatility Smile rather than skew in FX Options? FX options usually show a smile instead of a strong skew because the currency market is naturally more balanced than equities. In equities, everyone worries about

2

1

1

Learn and implement with peers!!

How to be insanely good at C++ like able to build low latency systems

621

51

1K

If you are interested in sell-side quant roles, learning Partial Differential Equations and how to solve them using Finite Difference Approach is a must. You can also learn new age methods like ADI ( Alternate Direction Implicit ) and have projects based on it. #Quant

2

2

54