John Paul Koning

@jp_koning

Followers

27,969

Following

635

Media

3,715

Statuses

21,480

monetary economics|history of money|central banking|financial privacy|payments|gold|financial inclusion|cryptocurrency|monetary law|financial crime

Montréal, Québec

Joined November 2012

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Pinned Tweet

My thoughts on the Tornado Cash defence team's arguments and what happens when other payments companies adopt them.

8

0

6

Sure, I'm happy that my bitcoins are rising in price. But let's not fool ourselves. We aren't "changing the world" or "fixing money." We're a bunch of degenerate gamblers addicted to the world's first digital chain letter game, and waves of new players are joining the chain.

229

197

3K

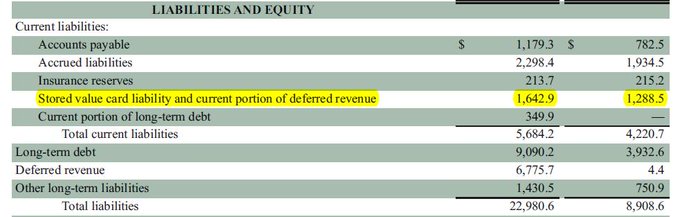

Wow Starbucks, what a great gig.

Starbucks has ~$1.6 billion in 'stored value card liabilities' i.e. the Starbucks Card. So ~6% of the firm's liabilities are comprised of coffee addicts paying 0% for the privilege of lending to their supplier.

Source:

73

556

2K

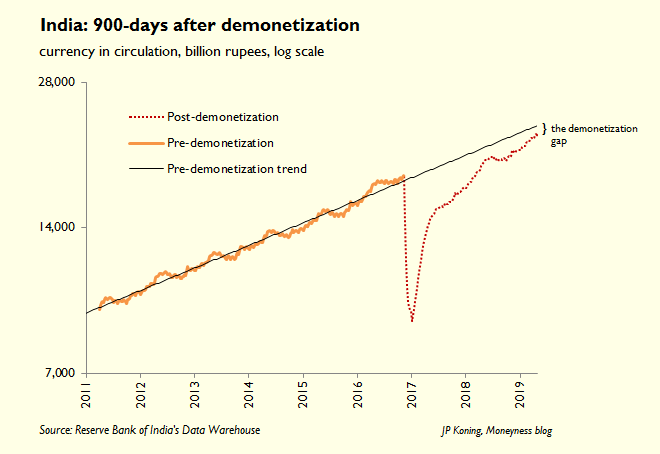

Modi's demonetization after 900 days.

Indians have almost entirely readopted cash. The demonetization gap—the difference between India's current banknote count and where it probably would have been without demonetization—has shrunk to a speck. All that effort, for what?

89

856

1K

$30: The amount that Bank of America charges customers for a domestic wire transfer:

25¢: The amount that Bank of America pays the Federal Reserve to do the wire transfer:

That's quite the markup.

43

407

996

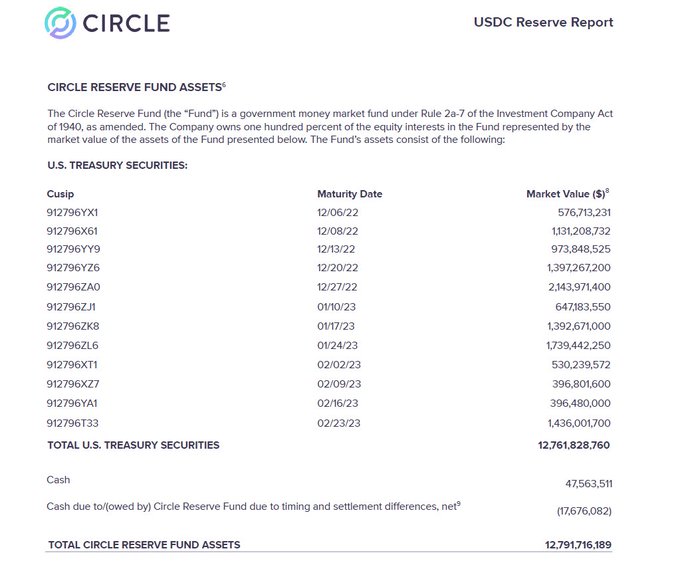

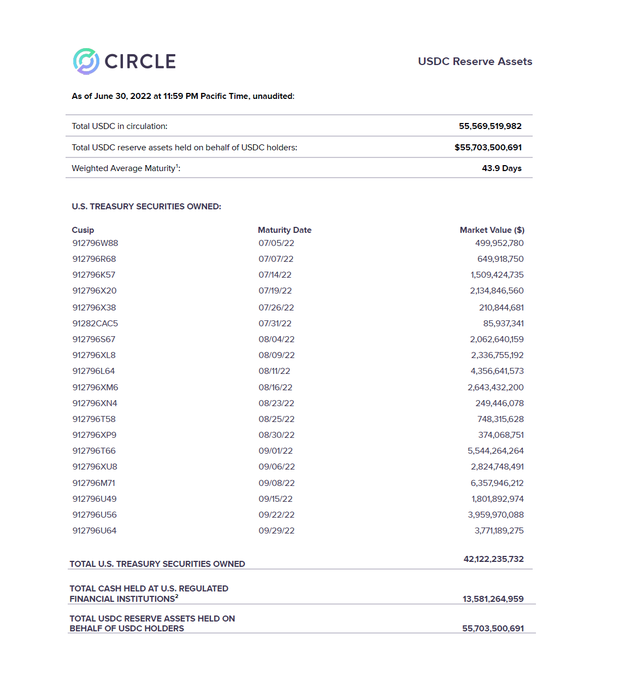

Circle's most recent attestation report shows 30% of USDC's reserves – or $12.79 billion – are invested in its government money market fund, the Circle Reserve Fund, managed by BlackRock. This is up from 0% in October.

37

171

839

The Fed recently asked a sample of 382 American crypto owners why they own crypto.

Answers are in the screenshot below 👇

The top reasons: price appreciation and curiosity about the tech. Almost no one mentions remittances, payments, or distrust of banks/government.

83

179

865

It's telling that the crypto lenders that have malfunctioned are the big centralized ones (Celsius, Blockfi, Voyager) while the transparent non-custodial lenders (Compound, Aave, Maker) are still working.

34

125

825

A lot of the stuff people are building on DeFi would be illegal if tried in real life. Can't start an exchange (like Uniswap) in meat space without registering with the SEC/CFTC, or build a bank (Maker) without getting a charter, or an MSB (Curve) without getting an MSB license.

77

97

790

Sure, own a bit of gold and bitcoin. They are short positions against society. Stagnation, dysfunction, war... bitcoin and gold provide a hedge. But never own too large a position. You risk becoming a misanthrope, incentivized to root for whatever dystopia makes you rich.

173

51

620

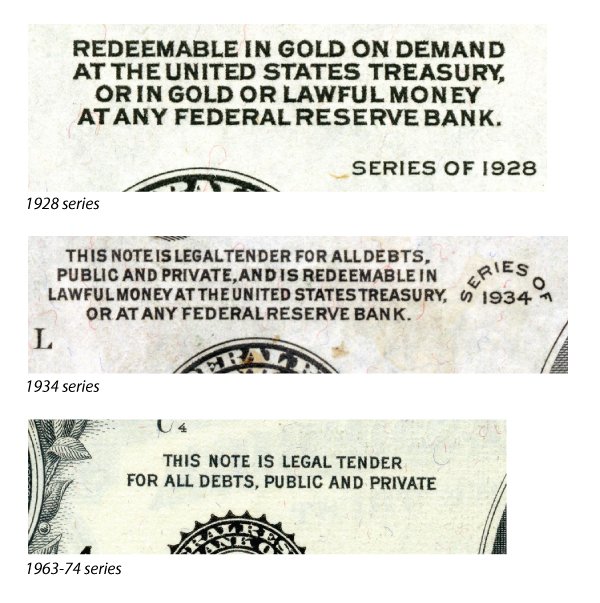

How the Fed's promise on the face of its banknotes has changed over time:

28

395

589

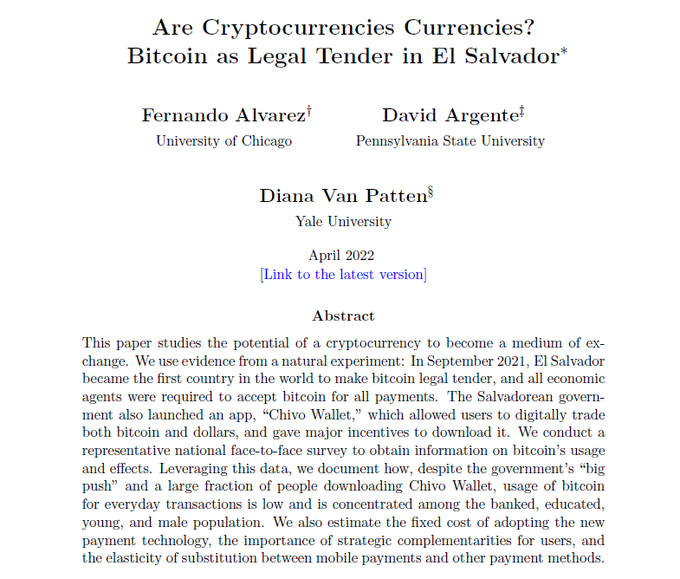

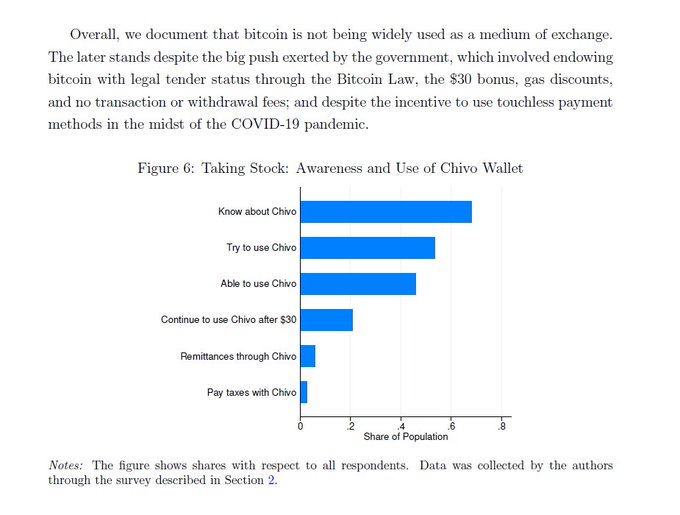

Here's the definitive study of El Salvador's bitcoin experiment. To measure bitcoin usage, the authors rely on survey data gathered from face-to-face interviews with 1,800 Salvadorean households.

ht

@alvafer64

26

179

567

The SBF case got all the attention but the Tornado Cash case may end up being the seminal crypto court case. Which is why you should read the government's response to the defence's motion to dismiss, published last night.

👀👀

23

127

519

Time to stop treating algorithmic stablecoins as an engineering challenge ("after a few failures a successful iteration will emerge") and start seeing them as fundamentally flawed product ("no amount of engineering can fix 'em").

38

45

484

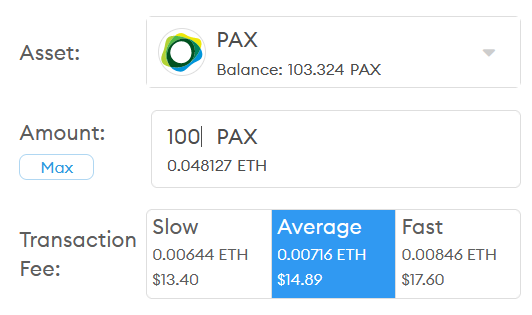

To send $100 in stablecoins I have to pay a fee of $14.89. But to transfer $100 in cash via Western Union it'll cost me just $7. Wasn't crypto supposed to be a cheap alternative to the incumbents? How is is this helping the low-income & unbanked? 😕

147

61

493

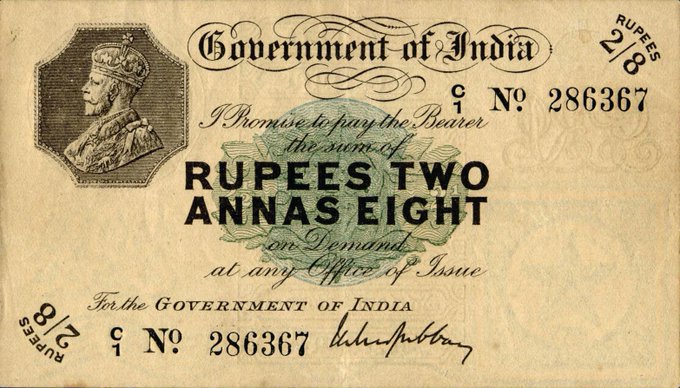

We don't think of the Indian rupee as a global currency, but at one point Bahrain, Kenya, Qatar, Oman, Uganda, Kuwait & more were using it.

27

456

468

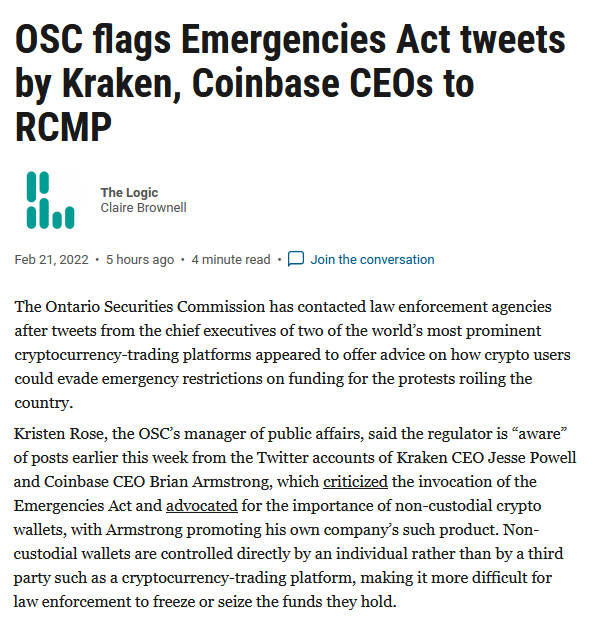

The Ontario Securities Commission recently reported crypto CEOs

@jespow

&

@brian_armstrong

to the RCMP. I don't imagine this bodes well for the ongoing process of registering Kraken/Coinbase under Canada's new regulatory framework for crypto marketplaces:

53

103

425

Why aren't anti-money laundering regulations adjusted for inflation? Over time, ceilings such as currency transaction reporting for amounts over $10,000 (in place since 1970 in the US) become more onerous. It's a constant drip-drip loss of privacy that we never signed up for.

27

96

422

Gensler: "...stablecoins also may be securities."

PayPal, Wise, Payoneer & Skrill all create dollars. So do Paxos, Tether & Circle. Regulators have never deemed the first set of dollars to be securities. Why should the second set be deemed as such?

40

50

428

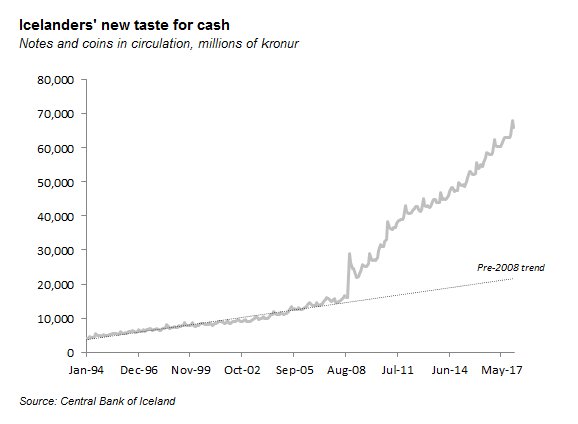

Not all Scandinavian countries are going cashless. You can see precisely when Icelanders lost trust in their banks and began cashing out of deposits into notes.

15

199

388

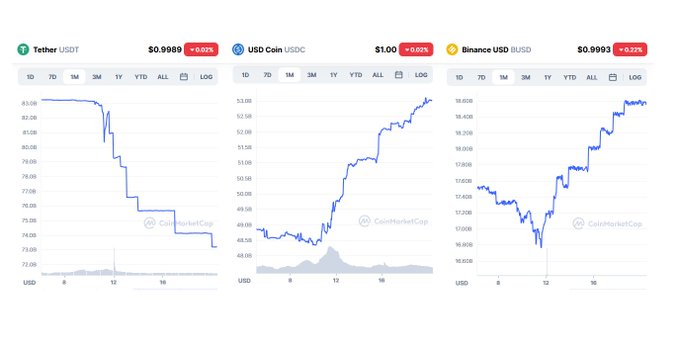

I hate to be the one to bring this up but at what point do we admit that this isn't just a healthy rebalancing out of Tether into safer stablecoins USDC and BUSD, but a run on Tether itself?

40

55

394

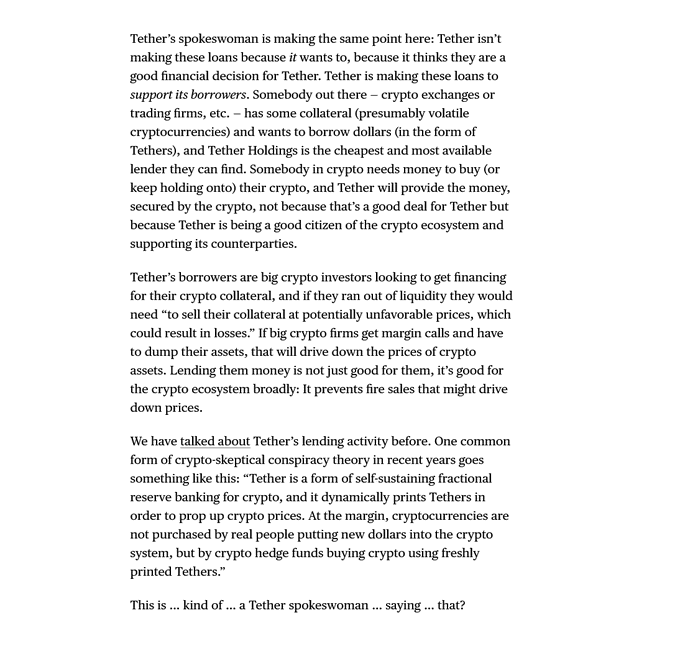

The Tether conspiracy theories weren't conspiracy theories after all? Because it sure sounds like Tether's spokesperson just admitted to them.

via

@matt_levine

37

98

403

Go far enough down the bitcoin rabbithole and you'll tumble out the other side as a state-chartered bank with direct access to the Fed.

9

34

361

I haven't looked much at the economics of proof-of-stake blockchains. Isn't the term "staking rewards" a bit of a misnomer? They're not really a reward to stakers, but a penalty on those who don't stake, right? That is, non-stakers face death by dilution.

87

25

366

The Fed didn't start issuing $1 bills till 1963. Before then, all $1 notes were in the form Treasury-issued silver certificates (see top).

14

200

332

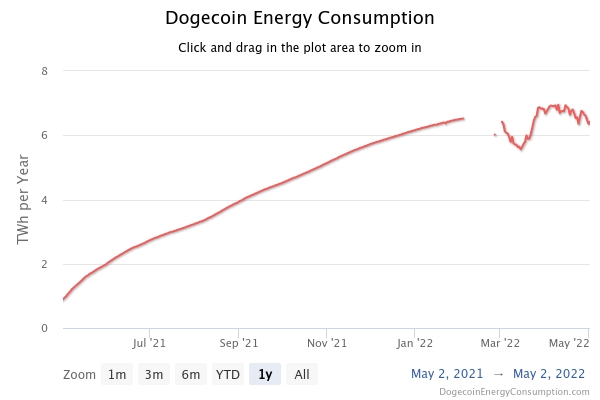

Dogecoin serves no purpose other than gambling yet it somehow uses up more electricity than the entire state of Vermont, home to 620,000 people, tens of thousands of businesses, hundreds of schools and dozens of hospitals.

28

95

345

Does that mean a stablecoin was effectively the biggest beneficiary of the FDIC bailout? Recall that Circle said it had $3.3 billion stuck at Silicon Valley Bank going into the weekend of March 10.

Gruenberg: The ten largest deposit accounts at SVB held $13.3 billion in the aggregate.

40

126

500

32

79

336

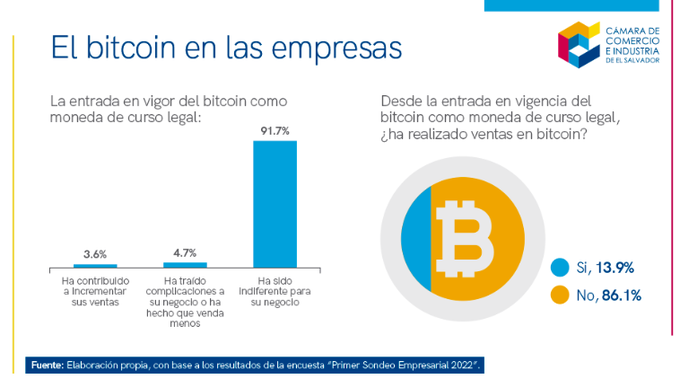

Since El Salvador adopted bitcoin, 86% of Salvadoran merchants have not processed a single bitcoin transaction:

Not surprising. Bitcoin is not a good payments medium. Even when propped up by government coercion, people avoid using it.

ht

@davidgerard

38

96

335

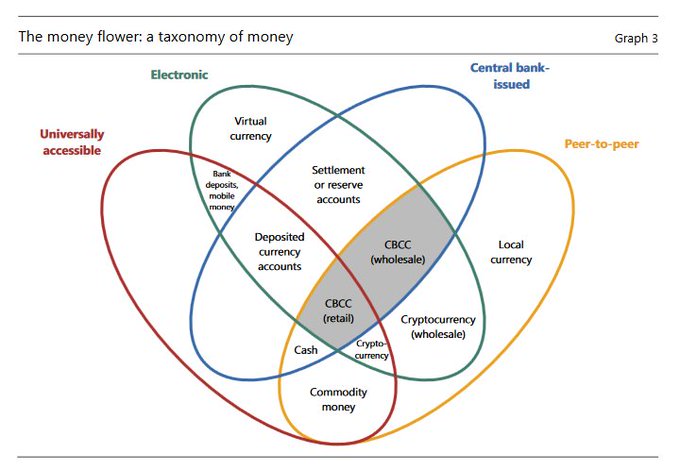

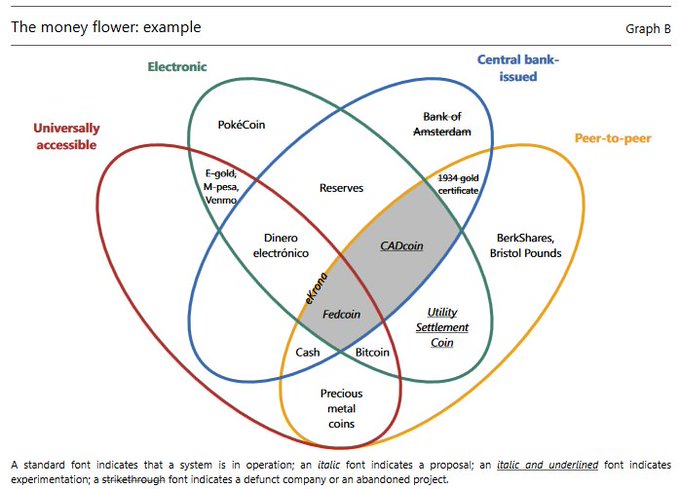

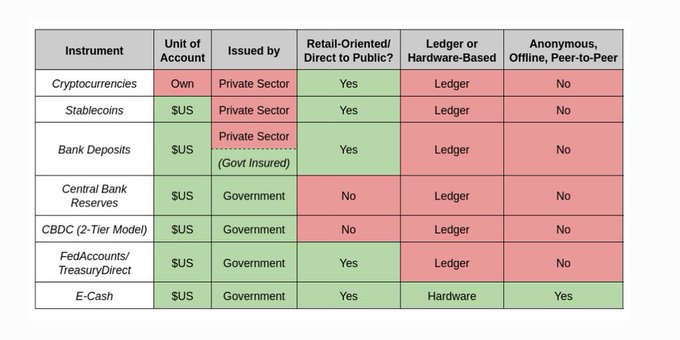

This new paper from the BIS really nails the distinction between various types of money. Very helpful.

9

169

324

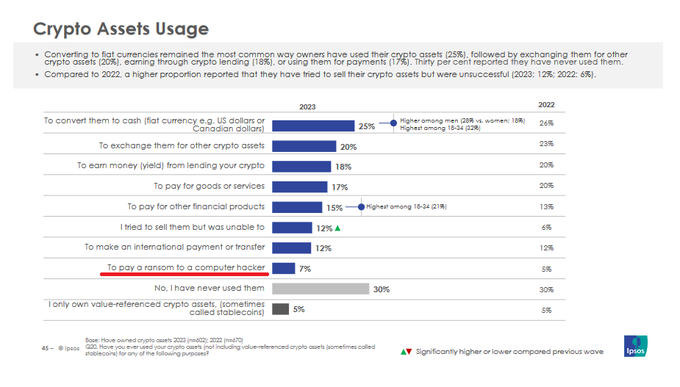

7% of Canadians who reported owning crypto assets in 2023 used their crypto to pay a ransom, according to a recent survey by the Ontario Securities Commission.

👀👀

27

97

329

Value of transfers sent in 2020, by network.

Zelle: $307 billion

PayPal: $963 billion

Stablecoins (on-chain): $1.04 trillion

Fedwire: $840.4 trillion

Sources: 1) 2) 3) 4)

8

80

320

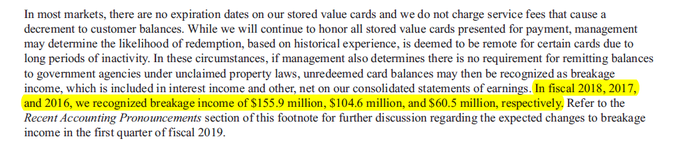

Few companies can get that much free financing. But don't forget breakage—balances that will never be redeemed. In 2018 Starbucks recorded breakage of $155 million,~10% of all card balances.

So the true rate at which customers are lending to Starbucks is probably closer to -10%.

13

70

313

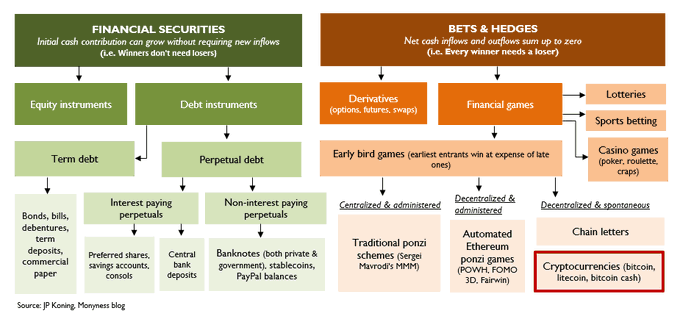

No, I don't think cryptocurrencies like bitcoin are ponzis.

But I do think they are distant relatives. Cryptocurrencies are a decentralized & spontaneous type of early bird game. Ponzis are a centralized & administered early bird game (usually run by scammers).

53

54

318

I can't think of a single socially productive use for Litecoins. Yet the market cap of Litecoin just hit $5.8 billion. What am I missing?

155

12

306

The supply of Tether stablecoins in circulation has contracted by another 1.45 billion. That brings the total supply of USDT down to 74.3 billion from a peak of 83.2 billion last week, an 11% reduction.

28

47

287

A leader should not be gambling with their country's wealth. The table below shows how

@nayibbukele

, President of El Salvador, has lost millions on bitcoin wagers.

via

45

80

284

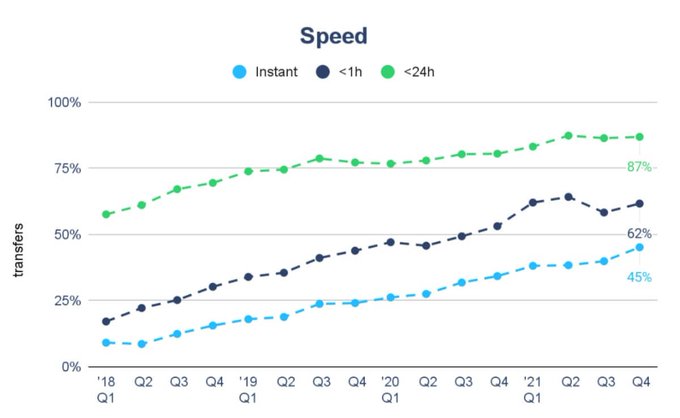

Wise (ex-Transferwise) is now processing 45% of all remittances instantly, and 62% under an hour. (No CBDCs, stablecoins, or blockchains required).

34

49

286

The difference between Bitcoin and Dogecoin is that Dogecoin's memes are fun and friendly. Bitcoin relies on very very serious monetary memes. But in the end, Bitcoin and Dogecoin are both memecoins.

28

26

271

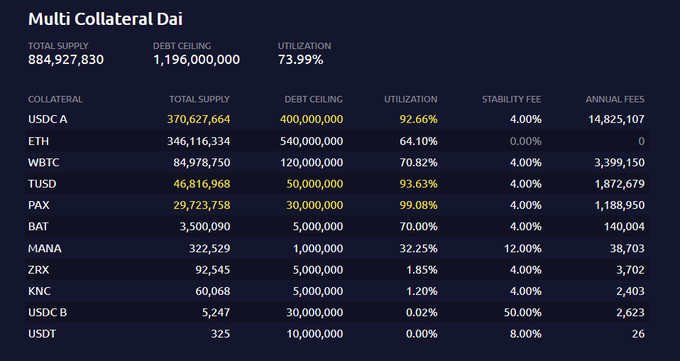

MakerDAO, the issuer of Dai stablecoins, is paying competitors Circle and Paxos a huge subsidy. Maker backs Dai with $4 billion worth of USDC and USDP stablecoins. At a t-bill rate of 1.7%, Circle and Paxos earn $68mm per year on this $4 billion, of which Maker gets zero. 😬

20

26

265

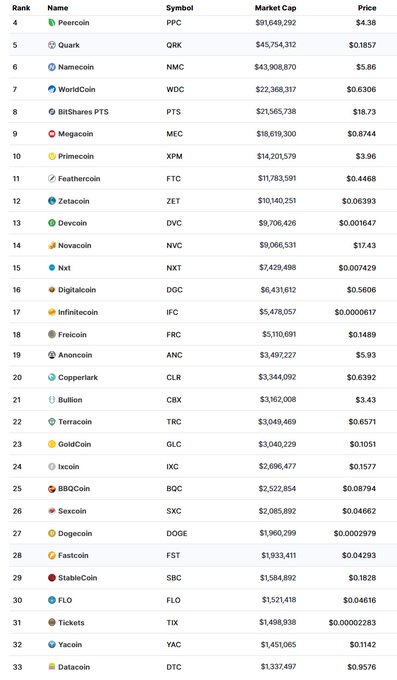

Here's the December 2013 list of top cryptocoins. After the first 3, all of them are pretty much dead/inactive except for the one that was started as a joke and is now worth $17 billion. 🤷

32

50

257

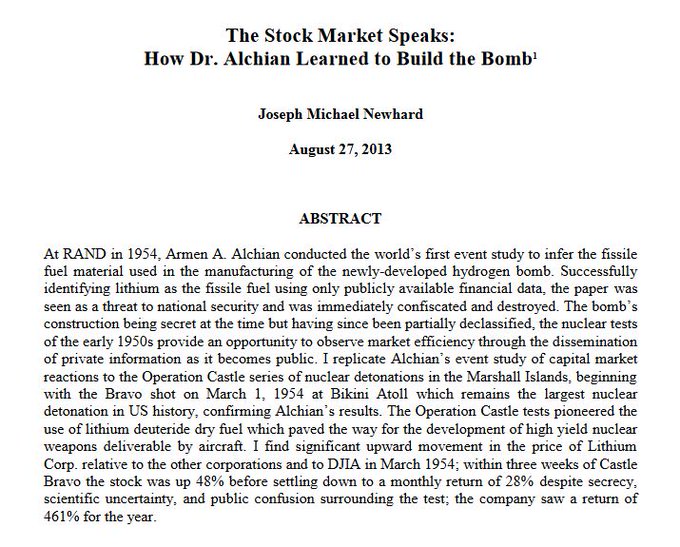

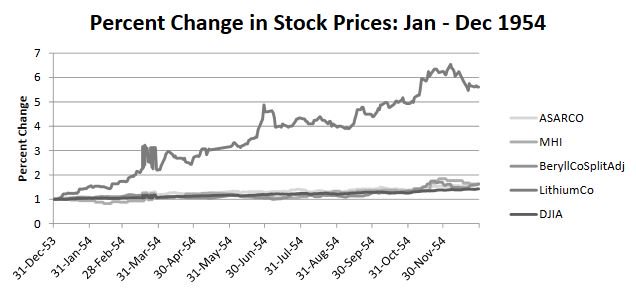

By watching stock prices, Armen Alchian correctly guessed the secret fuel used in the new H-bomb ht

@david_glasner

6

168

259

The fact that FTX just collapsed but decentralized exchange Uniswap still works perfectly fine is yet another demonstration that DeFi is the safest forum for trading rug pulls, scam tokens, and various ponzi coins.

82

28

260

We've come full circle. Cryptocurrency began as a response to the 2008 implosion of residential mortgages rolled into conduits, SPVs, MBS, CDOs, etc. And now MakerDAO is investing in the senior tranche of an SPV-securitized residential mortgage portfolio.

12

38

265

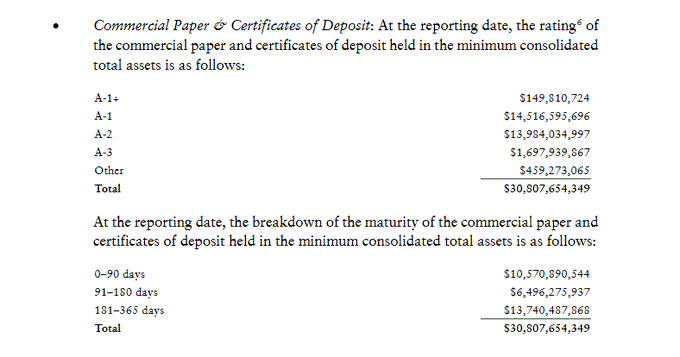

Nice. Tether's latest attestation report provides much more detail on the composition of its assets, including its commercial paper (most of it which is rated A-1 or A-2). It's very well footnoted, too.

23

62

250

This seems like a win for USDC users. Circle is yielding some of its control over USDC's reserves to an external manager subject to SEC regulation, which ultimately makes USDC safer. Transparency improves too, since USDC users can now get regular updates from BlackRock.

11

24

245

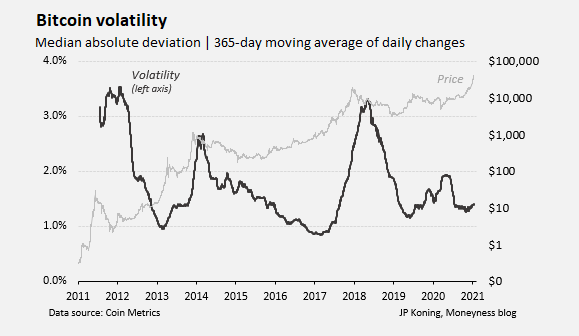

Bitcoiners have been telling me for years that as bitcoin gets bigger, its price swings will soften so that it becomes usable by regular folks for payments. But this isn't happening. Bitcoin is just as crazy volatile at $35,000 as it was at $3500, and $350, and $35.

57

49

240

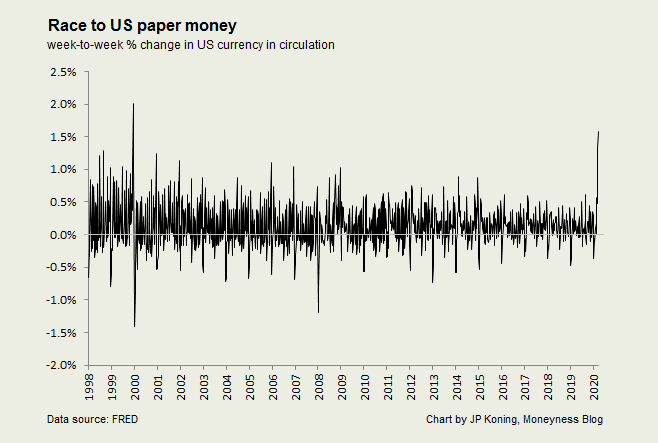

We've seen the largest weekly increase in US banknotes in circulation since the Y2K jump in December 1999.

15

116

231

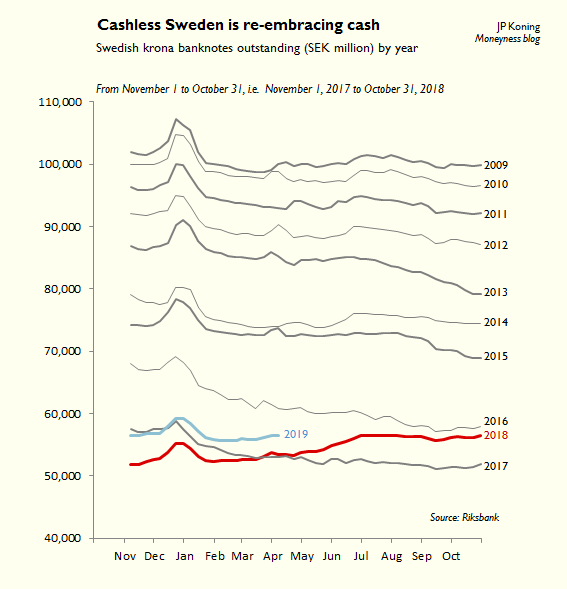

Sweden, the world's first cashless society, is re-embracing cash!

Banknotes in circulation is up 5.8% from last year, far in excess of population and economic growth. What's going on?

21

124

232

Flushed out another one.

It's amazing how persistent the '27-year' myth is. People really want it to be true, so they don't bother to do any back-checking. I traced out the myth's history here:

Bitcoin has already reached 40% of the life expectancy of the average fiat currency (27yrs). The most successful fiat currency has lost 99.5% of its value.

29

376

1K

26

54

227

Big announcement today about 16,796 bitcoins being sold for $175 million! CoinDesk interviews the sellers to find out why they are betting big on fiat.

12

6

222

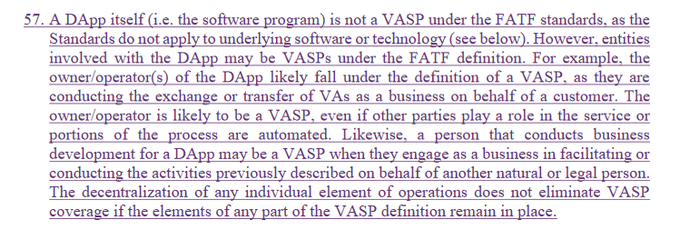

If you're a shareholder of Uniswap (or MakerDAO), then you're likely a VASP. And VASPs (i.e. Virtual Asset Service Providers) are responsible for setting up anti-money laundering controls.

This comes courtesy of yesterday's FATF draft guidance:

27

56

220

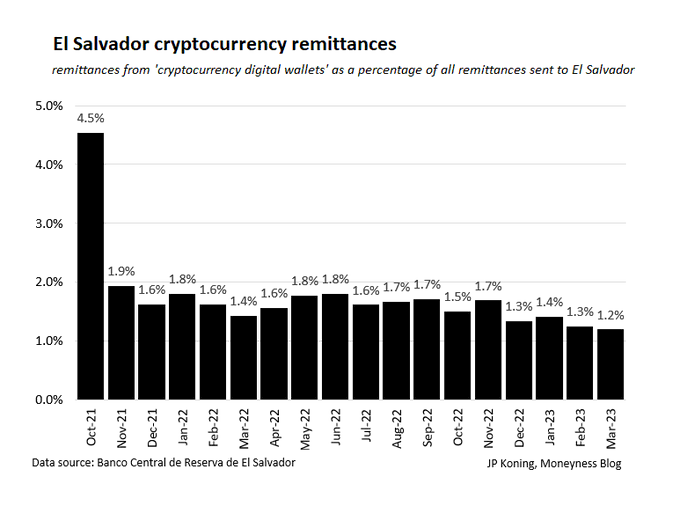

You can't blame the IMF for advising nations like Argentina to avoid copying El Salvador.

The ongoing stagnation of Salvadorean crypto-based remittance flows is a clear sign that El Salvador's

#bitcoin

-as-legal tender experiment has failed:

83

49

221

Surely a big disappointment for the ten people who had been planning to buy a Tesla with bitcoin in 2021.

10

14

225

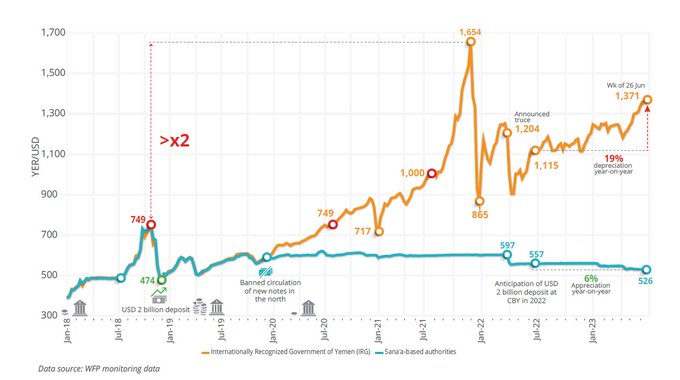

The rebel-controlled Yemeni rial is made up entirely of a fixed supply of notes printed prior to 2016. In the chart below you can see it appreciating in value (the blue line) against the dollar, issued by the world's most powerful state.

11

54

224

This is a dumb metaphor. There is no "space race towards digital currency." The U.S. dollar's dominance is determined by the strength of the U.S. economy and its institutions, not the medium on which it is issued.

23

32

213

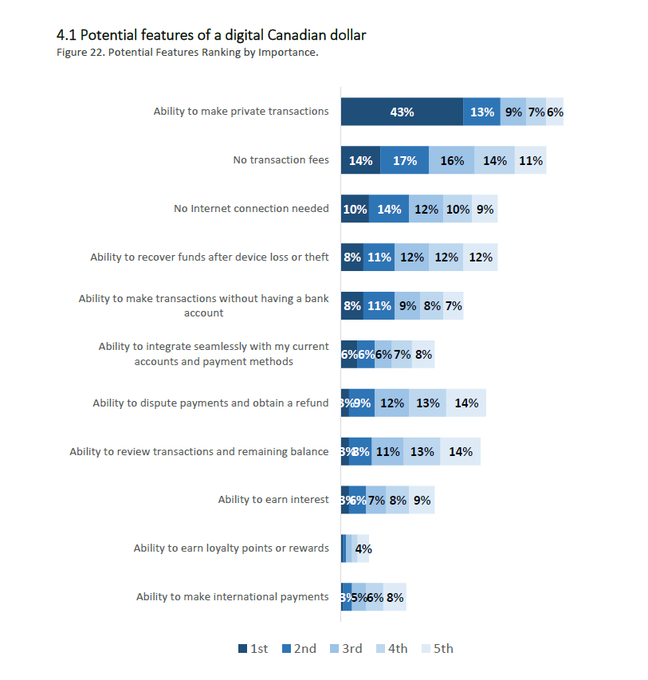

The Bank of Canada recently asked Canadians to rank the top features of a potential CBDC. The most popular feature by a long shot was "ability to make private transactions."

31

41

216

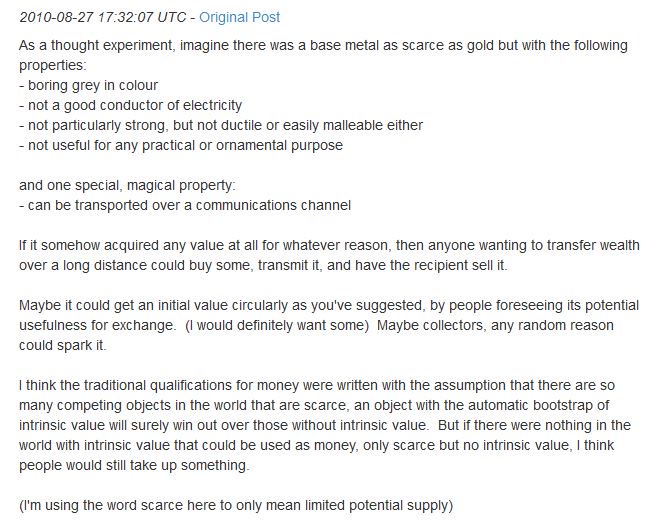

Satoshi Nakamoto's thought experiment about how intrinsically useless objects might acquire value

11

93

209

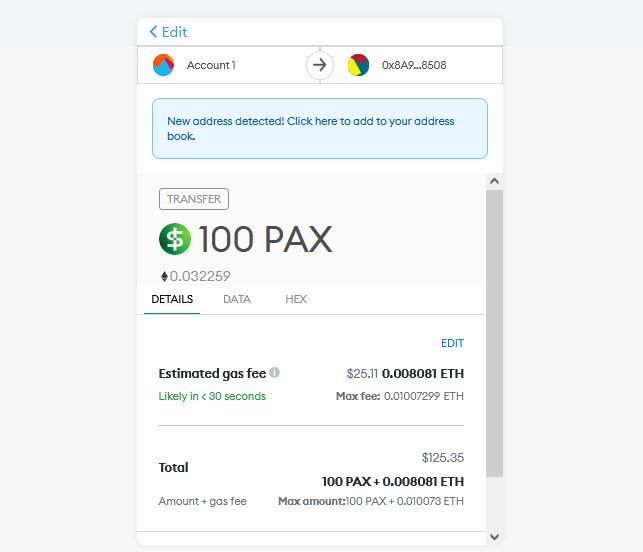

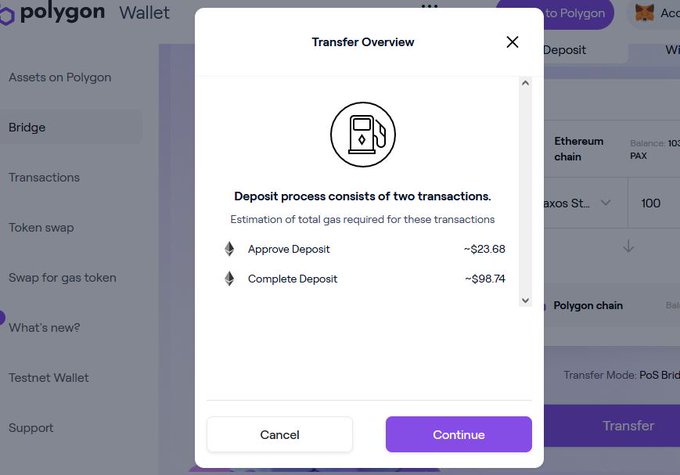

If someone wants to make a $100 stablecoin remittance on Ethereum, it'll cost $25 in fees. Yikes.

Layer 2 transfers are cheaper. But it costs $122 to bridge $100 to L2 (Polygon). 😬

Can people who need to make frequent remittances to their home country afford this technology?

89

30

207

To cut down on tax evasion, beginning in 2022 third-party settlement platforms like Zelle, PayPal and Cash App will report transactions totaling more than $600 to the IRS, down from $20,000.

Here is PayPal's explanation:

61

66

195

It's mind-boggling how US crypto exchanges and the SEC seem incapable of coordinating on a way for Americans to get access to regulated staking.

In Canada, exchanges worked with the CSA (our version of the SEC) and have been offering regulated staking since last fall.

21

35

206

Krugman is wrong. Up here in Canada we place the following tariffs on US goods: 270% on milk, 245% on cheese, 238% on chicken, and 298% on butter. As a result, my family pays $100s more per year than we should. It would be nice if Trump won this particular battle.

Really, really bad. Trump is throwing a temper tantrum, threatening dire retaliation against our allies for high tariffs THAT DON'T EXIST. You can't reach a deal with someone who demands you stop doing something you aren't doing 1/

510

5K

8K

27

101

178

The entire crypto economy has been built on the legal assumption that by not taking custody, one needn't register as a money transmitter.

But then Samourai & Tornado, both non-custodial, were charged for failing to register.

Huge implications for crypto if the Feds are right.

41

31

206

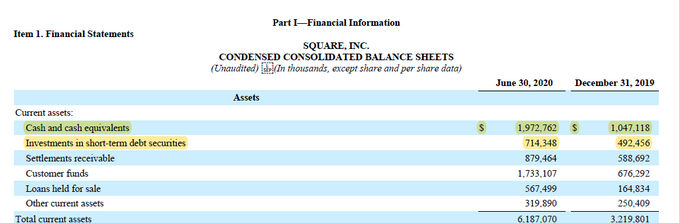

Square has about $2.7 billion in cash. Investing $50 million of that in bitcoin is a good way to attract publicity, without the CFO or board getting too upset about gambling corporate funds.

28

41

198

So you're hoping bitcoin shoots to the moon so that you can afford a lambo?

Don't.

Because in that same world the roads will be falling apart, soldiers will pull you over every 100 metres for bribes, and armed bandits will compete to murder you for your precious car.

90

16

184

Something strange is happening in Yemen. The entire Yemeni monetary system has bifurcated on the basis of banknote age, with old rial notes being worth more than new ones. I wrote about it here:

12

55

191

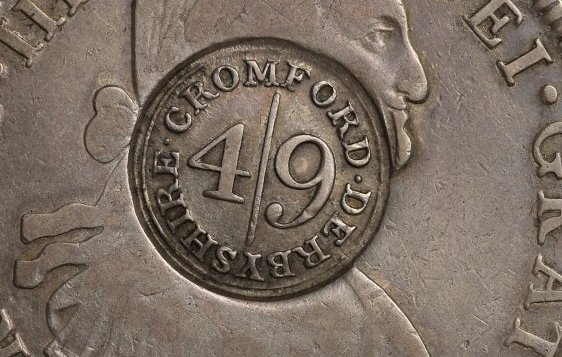

Here's a wild coin. An 1803 Spanish dollar minted in Mexico City that ended up in Derbyshire, England, where the Cromford cotton mill countermarked it to pass locally at 4 shillings 9 pence. Coin shortages encouraged private forms of money like this one.

4

57

179

This is going to blow your mind, but depositories like the DTCC have been digitizing securities for decades now.

Every stock, bond, currency, and commodity will be digitized.

Asset allocators won’t be able to ignore digital assets in the future.

67

150

768

13

34

180

Archeologists just found a Russian "beard kopek" from 1699, the first year they were issued: Peter the Great banned all facial hair unless people bought one of these coins, which exempted them from the rule.

8

84

187

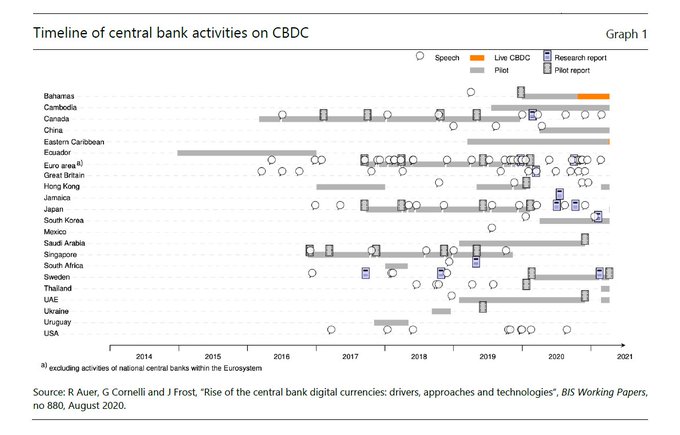

A timeline showing how central banks have been kicking the tires of central bank digital currency (CBDC).

snipped from

3

104

186

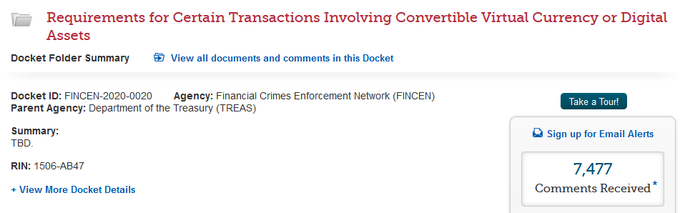

Going back to 2008, FinCEN has received 11,183 submissions from the public in response to various rule proposals and notices. It has received 7,477 of those comments—or 67% of all public responses—in just the last three weeks.

7

39

184

Transferwise, why so fast?

I wrote about the technological changes that allow remittances to be processed in seconds, not days. Public service announcement: fast remittances don't require blockchain or central bank digital currencies.

24

46

188

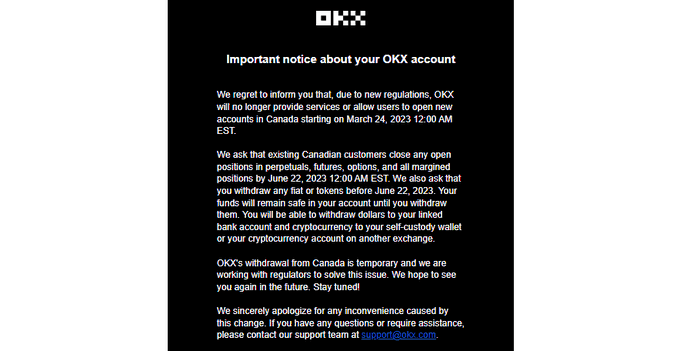

OKX stopped serving Canadians this morning. It couldn't meet today's deadline for filing with securities regulators.

Next up: Coinbase, Kraken and Gemini.

Unless they file by today, all three will have to exit Canada, else they'll be operating here illegally.

8

46

183

Even though El Salvador has imbued bitcoin with forced tender status and rewards subsidies to adopters (such as a $30 bonus, discounts, and no withdrawal or transaction fees), usage is minimal and declining.

23

62

182

Silicon Valley Bank is a very American mess. The Basel rules that protect against these sorts of banking flameouts were not applied in the the US, or at least, they were only applied to very large banks. Silicon Valley Bank was exempt:

4

52

181

A stablecoin reporting $4.5 billion in profits in Q1 with just a few dozen employees is a great illustration of how insanely profitable it can be to engage in regulatory arbitrage of the U.S.'s AML framework.

34

25

183

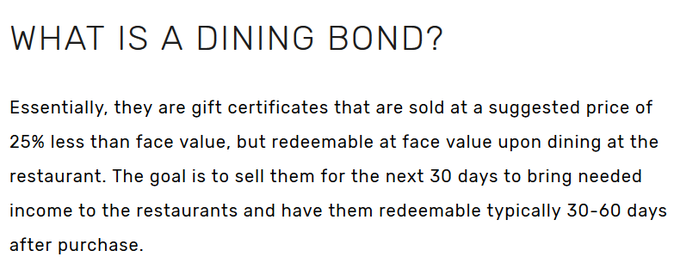

Here's a great idea. To help survive the crisis, restaurants are issuing "dining bonds," i.e. gift certificates at a 25% discount to face value.

Your favorite restaurant gets cash now. You get a meal in two months:

12

89

176

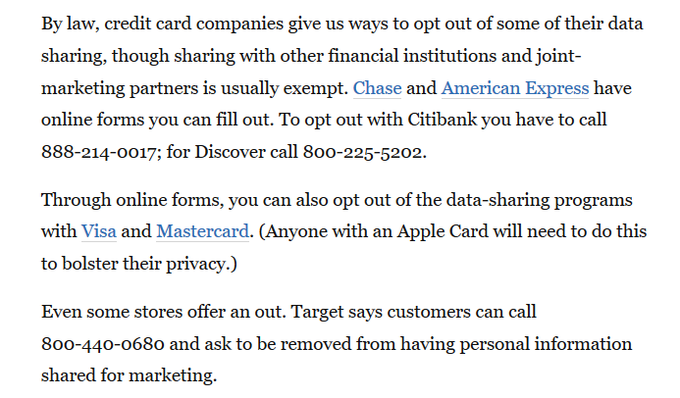

Yikes. When you swipe your credit card, here's who gets your data:

-your bank

-your bank's marketing partners

-co-branded card partners

-Visa/MasterCard (who may onsell it)

-the store (who may share it)

-the store's bank

-swipe machine company

Source:

10

109

175

USDC is shrinking and Tether is growing because folks who hold USDC are generally savvy enough to know they're getting screwed by USDC's 0% interest rate, whereas Tether holders aren't savvy enough to know they're getting screwed by Tether's 0% rate.

21

18

169

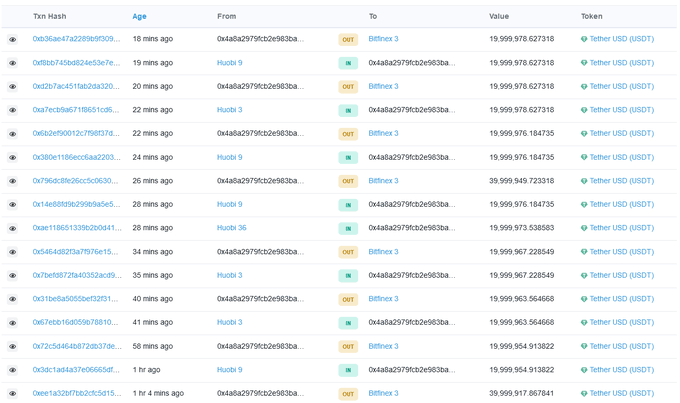

Tether redemptions are just pouring into Bitfinex right now. This wallet alone has done around 180 million in redemptions in the last hour:

It looks like version 2.0 of the run on Tether has begun. Version 1.0 petered out last month.

11

36

171

If bitcoin is sufficiently cash-like that a $10,000 bitcoin payment triggers a Form 8300 reporting requirement, it's also cash-like enough to enjoy a de minimus exemption from capital gains (say for transactions where the gain is less than $300.)

11

13

174

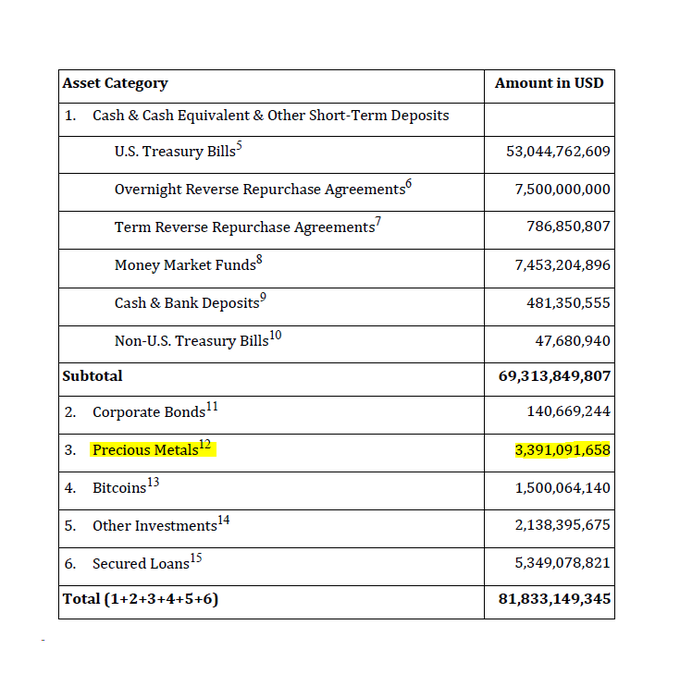

Tether's newest attestation report now discloses gold holdings of $3.4 billion. Since Tether has issued just $240 million or so in XAUt tokens, that means Tether's flagship product – USDt – is backed by ~$3 billion worth of the yellow metal. 👀

24

37

174

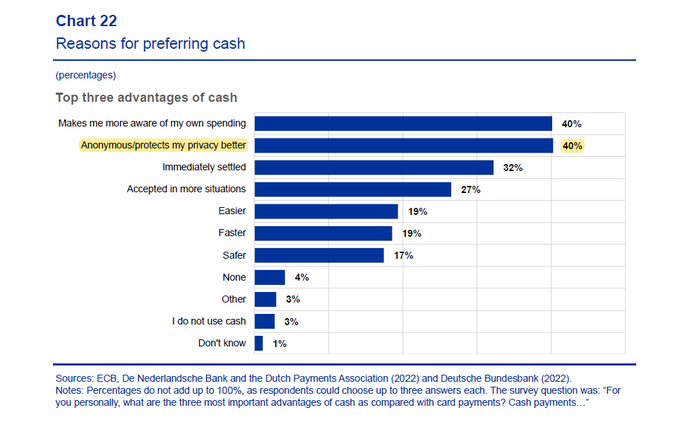

Europeans are getting more concerned about their financial privacy. The

@ECB

periodically asks citizens for their top reasons for preferring cash. In 2016, just 13% of Europeans cited privacy/anonymity. In 2022, that number rose to 40%.

13

57

166

Circle is now publishing a list of all securities that back USDC as well as the names of the banks that hold its cash:

With Paxos already making this information public,

@Tether_to

is now the laggard. Any plans to disclose this data,

@paoloardoino

?

13

24

152

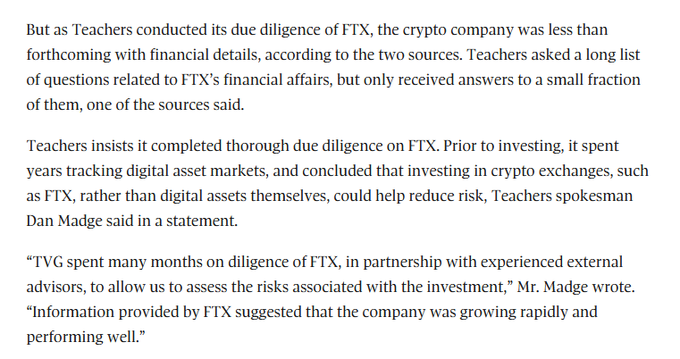

Apparently the Ontario Teachers' Pension Plan asked a long list of questions related to FTX’s financial affairs, but only received answers to a small fraction of them, yet it invested $95 million in FTX anyways.

via

9

27

173

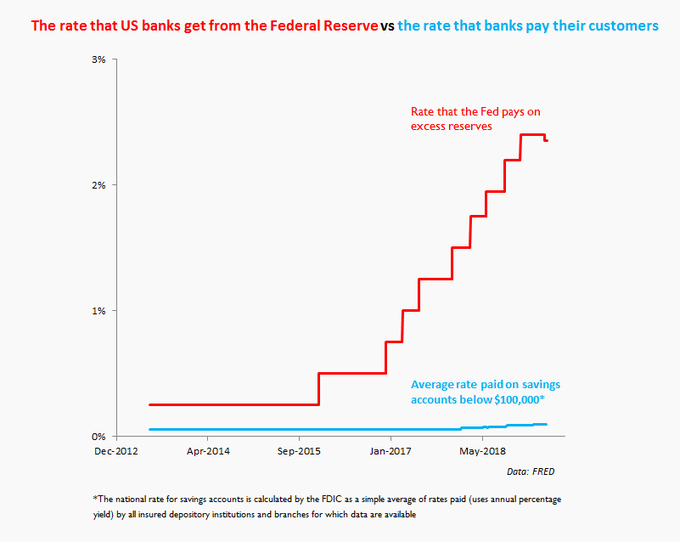

Any day now, banks.

I understand why the rate that banks pay to savers is below the rate that the Fed pays banks (they need to cover costs). But I find it kind of shocking that banks don't match the pace of Fed rate increases. Shouldn't savings accounts by yielding ~1% by now?

26

54

170

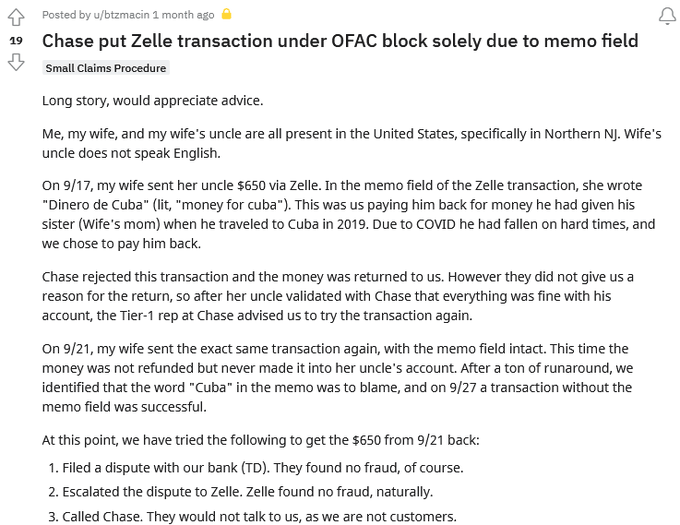

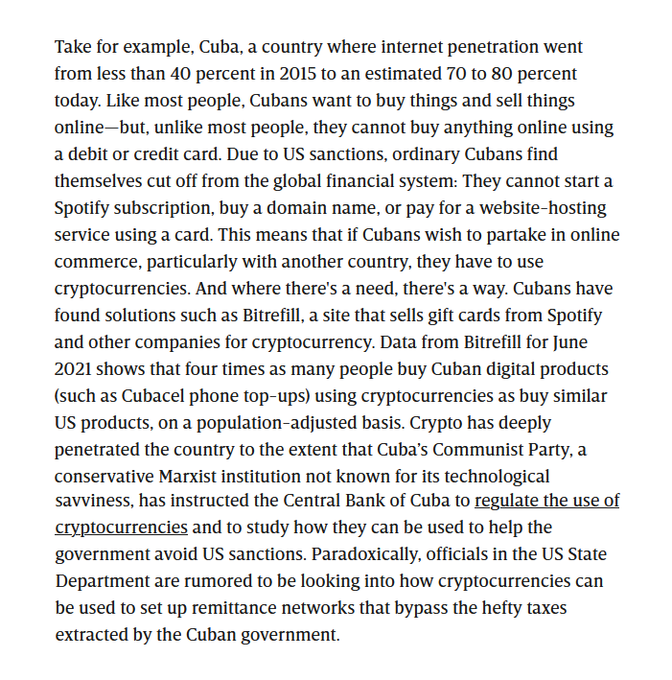

Someone puts the word "Cuba" in the memo field of a Zelle payment, it gets blocked:

25

24

164

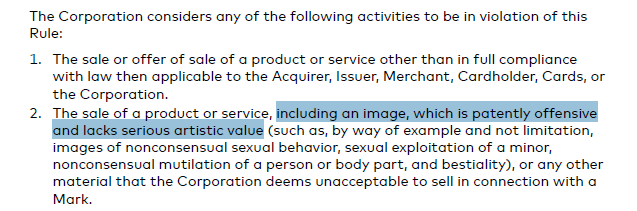

Mastercard prohibits the sale of any product or service that is "patently offensive and lacks serious artistic value." That could be literally anything. What does "patently" mean? What is "offensive"? How does Mastercard litigate "artistic value"?

24

21

168

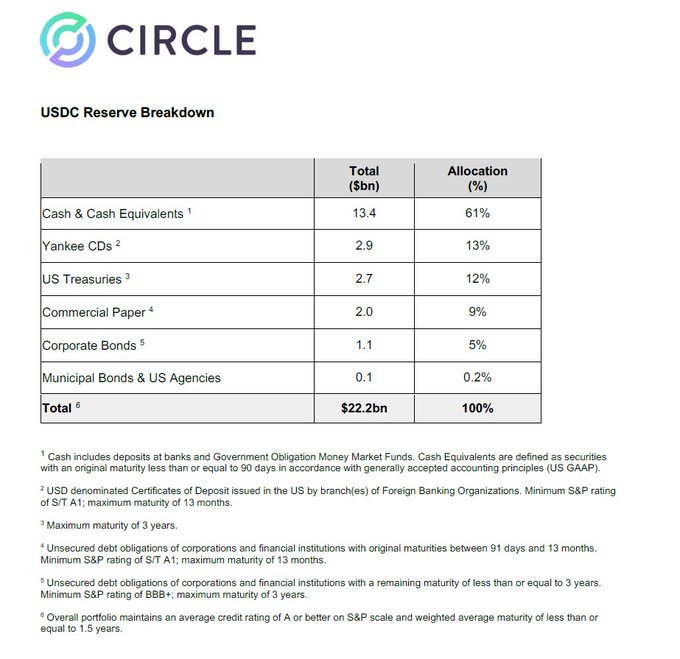

Great news. USDC's latest attestation report has a full breakdown of its investments and plenty of explanatory notes to help address further questions.

In terms of transparency, the other stablecoins now have some catching up to do.

9

40

165

Satoshi Nakamoto never intended for bitcoin to supplant regular payments. The card systems work "well enough for most transactions," he granted in the whitepaper. And Satoshi was proven right. Today, bitcoin serves as a niche last-resort payments option, not as a replacement one.

22

18

161

In many of the CBDC whitepapers, the biggest worry was always that a retail CBDC would be incredibly popular with citizens, and this would hurt commercial banks.

In practice, it looks like biggest problem is the opposite: no one wants to use CBDC:

23

36

162

See the strange symbol on the bottom half of this 1769 Spanish piece of eight? It's derived from superimposing the four letters PTSi, indicating the coin was minted in Potosi, Bolivia. Looks like an early version of the dollar sign ($), no?

11

34

158

The ECASH Act has just been introduced. It would direct the U.S. Treasury to pilot a payments product, e-cash, that replicates the privacy-respecting features of physical cash.

E-Cash is not a blockchain, it's not a CBDC, and it works offline:

17

48

159

Two big Tether redemptions totaling 950 million USDT have just reduced the number of USDT in circulation by 1.2% to 73.3 billion. This is down from a peak of 83.2 billion, a 12% contraction.

Meanwhile, competitors USD Coin and BUSD continue to see inflows. 😬

15

38

155

Rebel no more. Dai now contains more straight-laced USDC collateral than unruly ETH collateral:

At this point I suppose you'd have to be pretty much indifferent between owning Dai or USDC, no? Same stablecoin, different name?

19

32

157

One observation from today's Tether attestation report: we just went through a crypto bloodbath yet the value of Tether's opaque "other investments" – which almost certainly included its stake in failed lender Celsius – somehow rose from $4.96b to $5.56b? 🤔

18

13

157

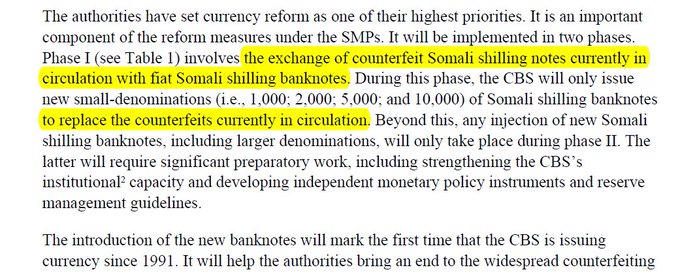

One of the world's strangest monetary reforms is occurring right now in Somalia...

The Central Bank of Somalia is buying up twenty-five years worth of counterfeit Somali shilling banknotes with new legitimate notes. The most recent IMF update is here:

5

86

153

Tether now holds $35.4 billion in customer funds, more than PayPal held at the end of last quarter.

Does that make Tether the largest fintech in the world ranked by US$ customer balances held?

Source 1: 2:

17

29

149