🇺🇸 GammaLab

@gammalab_tweets

Followers

7,960

Following

323

Media

1,832

Statuses

4,823

We analyze tens of thousands of option contracts daily to provide data that enables you to get a better picture about market liquidity.

United States

Joined October 2021

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Bridgerton

• 405091 Tweets

Butker

• 242969 Tweets

Colin

• 122093 Tweets

billie

• 90086 Tweets

Catholic

• 79914 Tweets

Penelope

• 75926 Tweets

Xavi

• 60251 Tweets

Daniel Perry

• 52818 Tweets

#岩本照誕生祭2024

• 35516 Tweets

Greg Abbott

• 34481 Tweets

Fermin

• 33890 Tweets

Marcelo

• 29755 Tweets

GTA 6

• 29370 Tweets

Megalopolis

• 26881 Tweets

Leeds

• 26354 Tweets

iMessage

• 26103 Tweets

#SVGala11

• 25303 Tweets

優三さん

• 19061 Tweets

ひーくん

• 18001 Tweets

Laporta

• 15391 Tweets

Norwich

• 13572 Tweets

Miri

• 13067 Tweets

SIEMPRE QUE LO BESO

• 12178 Tweets

Gorka

• 11069 Tweets

@MikeBenzCyber

This guy got everything wrong and mislead generations of politicians, and now he wants to get rid of competing ideas?

4

8

240

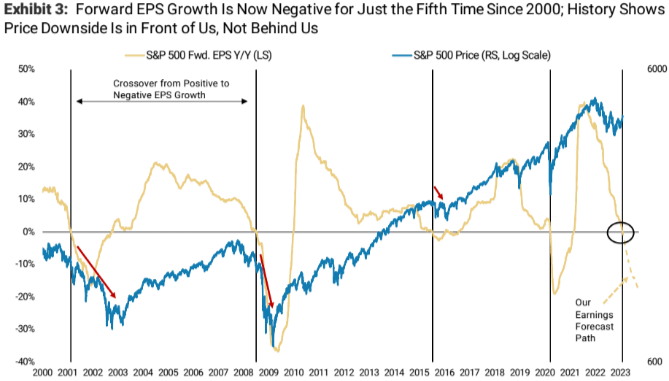

Michael Wilson points out that forward EPS growth has turned negative last week. This has only happened 4 times over the past 23 years.

6

76

222

JPM estimates that a market shock of -1 to -5% would cause a 0DTE delta unwind of -7 to -14B, which would translate into a -4 to -8% move. In the worst-case scenario, a -5% market shock could lead to -$30B of delta selling and a -20% crash.

16

46

172

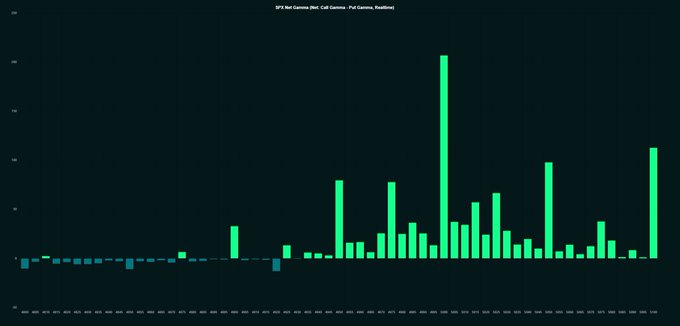

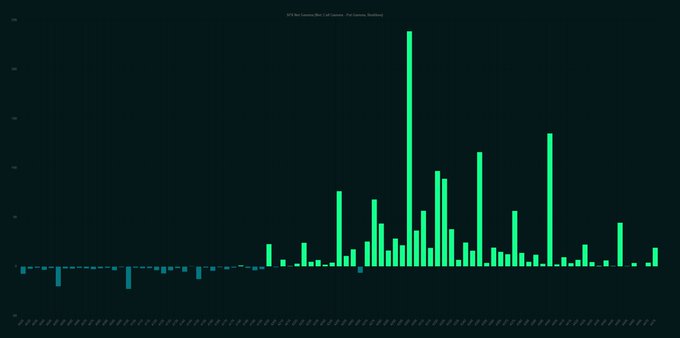

Massive gamma wall at 5,000, meaning dealers are selling a ton of $SPX futures every time the market tries to rally. Systematic buyers are exhausted meanwhile and are not able to give market a push.

7

18

109

@seanmdav

This senior executive needs to speak to the public on X for an hour instead of Elon Musk only.

4

3

107

According to GS the pain trade is now lower. Shorts are covered, CTAs are 100% long globally, retail is euphoric again, yearly inflows are completed, and liquidity is disappearing fast. Next week CPI + OPEX. Buckle up, worst-case CTAs sell 214B on a one-month horizon.

2

20

90

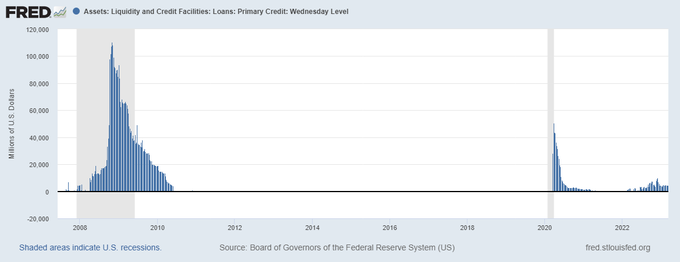

Here is something interesting for the nerds.. If you want to track stress in the banking system there are multiple ways (e.g. FHLB advances, discount window, H.8, FRA-OIS - we pointed those things out before and track them here occasionally).

But how about REAL-TIME data, and…

7

15

92

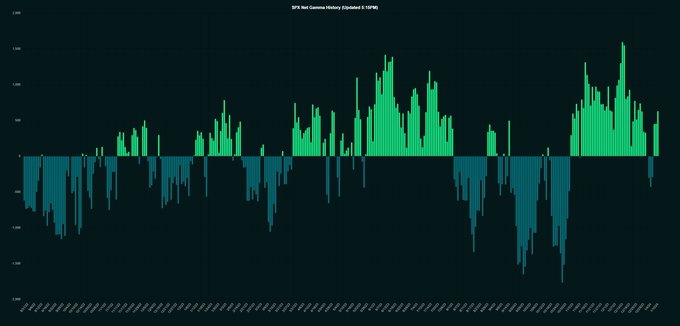

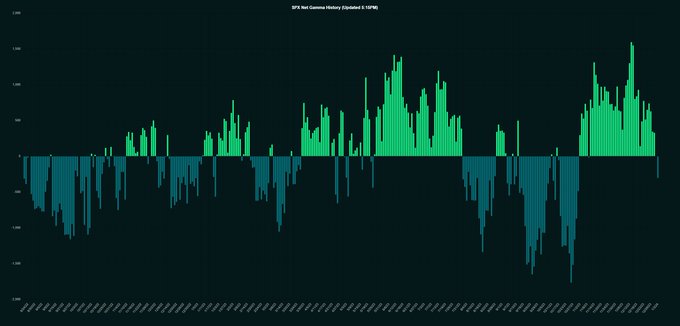

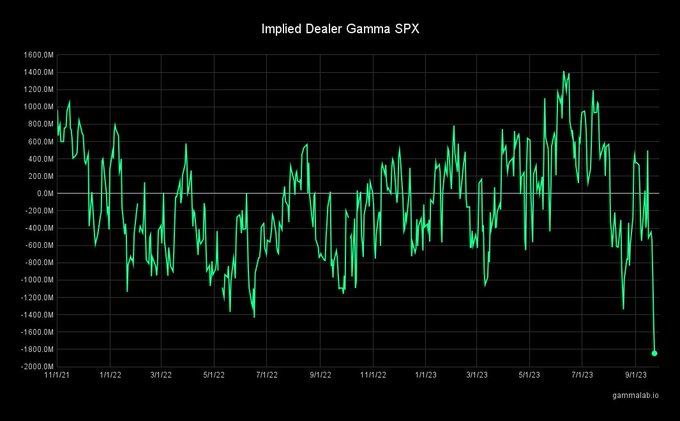

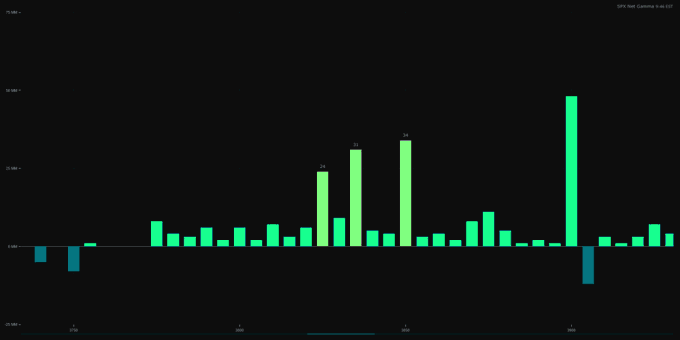

$SPX dealer gamma back in negative territory -> dealers will sell weakness/buy strength. 0DTE floor at 4,100.

7

14

88

Super-bear Hartnett figured out the world formula that will result in an epic liquidity crunch: '$100 billion QT from the Fed, ECB, BoE, BoC, RBA, and RBNZ per month + $1 trillion T-bill supply + $200-$300 billion rise in the Treasury General Account (TGA) + MMF outflows (from…

13

27

78

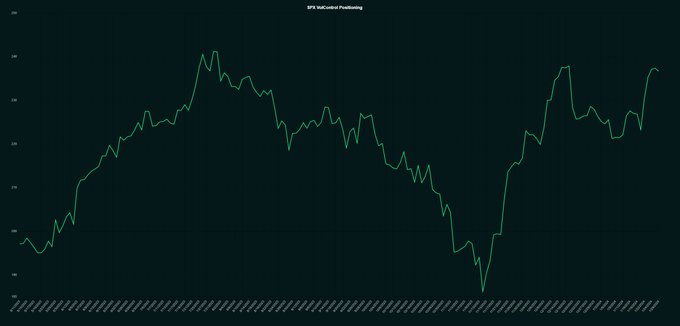

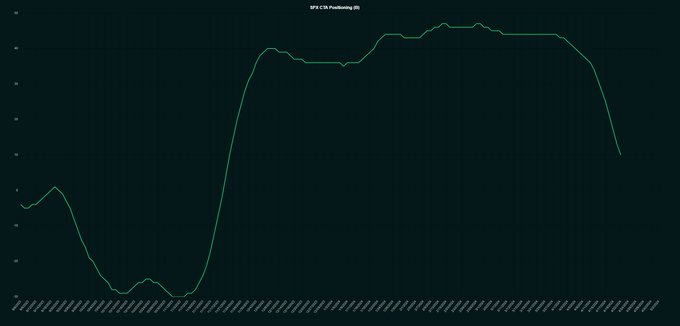

$SPX vol control positioning almost maxed out. CTA positioning in US equities 97th percentile. Price agnostic buyers ex option dealers are exhausted.

5

18

81

Goldman: Liquidity is at a premium with SPX liquidity (touch sizes) is -40% over the last week. Flows are still asymmetric to the upside with little offsetting supply: CTAs buying, buybacks fullsteam & a big option expiry on Friday.

3

8

75

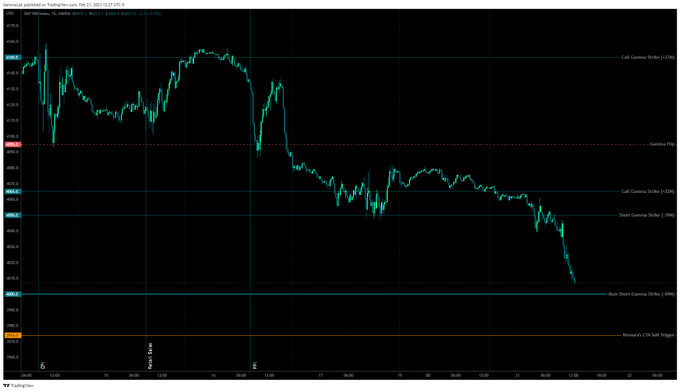

The MASSIVE $SPX gamma call wall at 4,300 is limiting further upside and might create a strong pin as we move towards OPEX (Frida, June 16th). Other factors are the questions regarding the chinese stimulus (where is it?), and the upcoming TGA refill. According to GS bill issuance…

4

15

73

The gamma squeeze is has run its course and dealers are now switching to counter-cyclical delta-hedging (selling strength, buying weakness). This is adding liquidity/reducing volatility, which in turn is giving vol control a chance to enter the market again. Additionally the $SPX…

4

10

70

McElligott on why volatility is dead: 1) Persistent overwriting from large asset managers for yield enhancement. 2) HFs reduce equity exposure, which results in less need for buying optionality. 3) 0DTE options compressing end-of-day vol due to same-day monetization.

3

12

67

$SPX dealer gamma -542M, gamma flip 4,095. The main short-gamma wall at 4,000 comes into play now. Below that level, CTAs start selling.

2

11

66

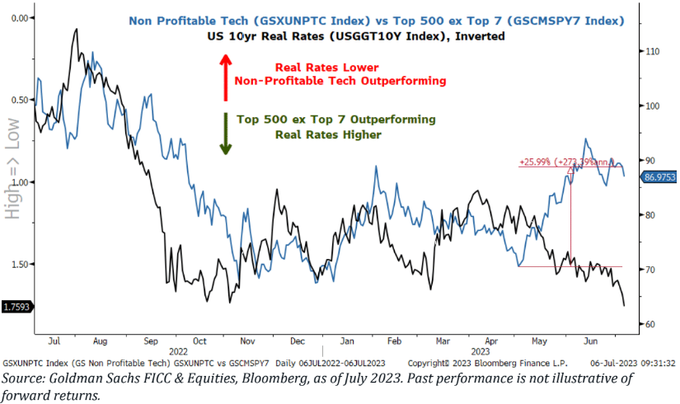

Goldman's chart of the day. Non-profitable tech is outperforming the broader market despite real rates rising. This is not supposed to happen, what could be the reason?

11

10

65

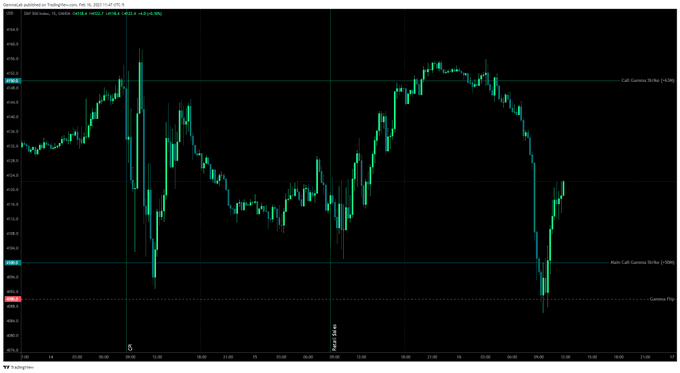

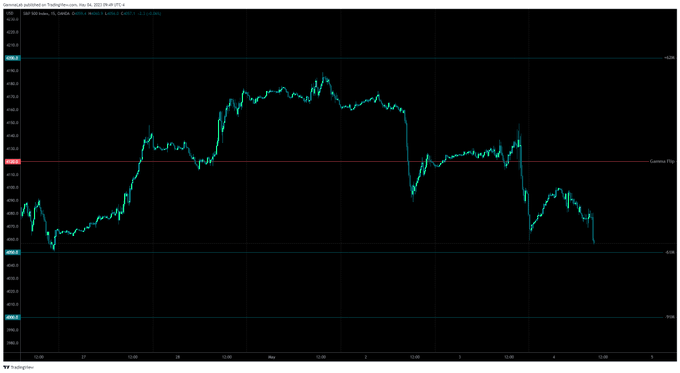

Only three levels matter. 4,090 ('gamma flip'); 4,100 (support) and 4,150 (resistance). Gamma at 4,100 is almost entirely concentrated in 0-2DTEs and will disappear shortly, while at 4,150 half of gamma is in ultra-short dated contracts.

5

5

64

Goldman: Hedge funds have net sold US equities in 9 of the past 10 trading sessions (99th percentile over the last five years).

1

16

61

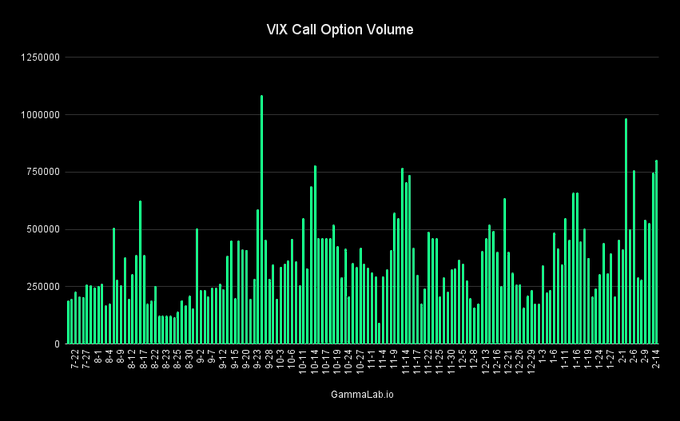

2nd highest VIX call volume of the year today despite 'VIX crush'. Consinstent flow of big call orders with strike 40 and (way) higher, mostly June expiry though.

4

10

61

The $SPX is hovering in the vincinity of the Call Wall at 4,800, but according to the gamma imbalance of ~630M the market is not oversold. Most interesting thought came from McElligott today: What if consensus is wrong and Yellen does not increase coupon issuance, but lets bills…

6

13

59

The buyback window is closing, dealers will not be the white knight much longer, rate cut expectation are evaporating and the vol curve is implying rougher waters next week. Buckle up.

4

13

56

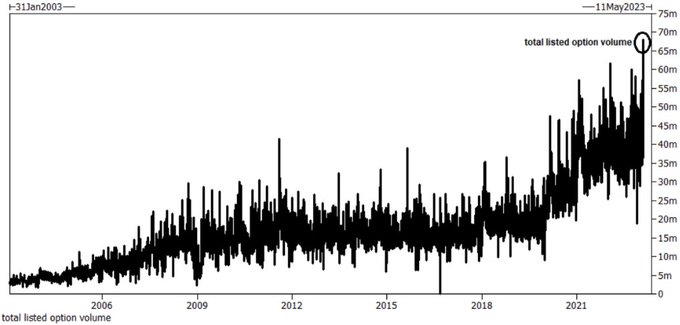

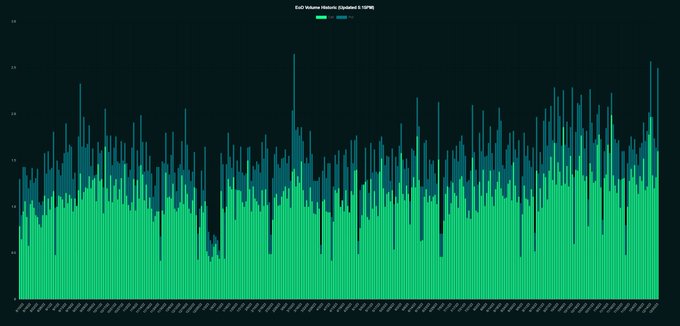

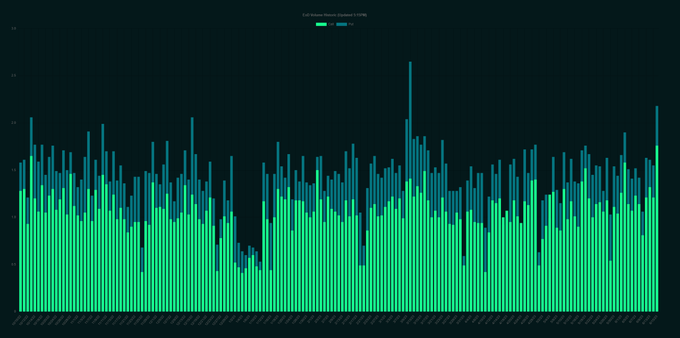

Today was the largest option volume session of all time, according to Goldman. 68 million contracts traded. 40 million calls/28 million puts.

5

27

55

$SIVB is not the problem, the danger lies in a more systemic issue, namely unrealized losses in High Quality Liquid Assets (HQLAs), which are indeed staggering (600-700B, see tweet below), even though we are nowhere near a GFC scenario (unrealized losses back then at the height…

4

14

56

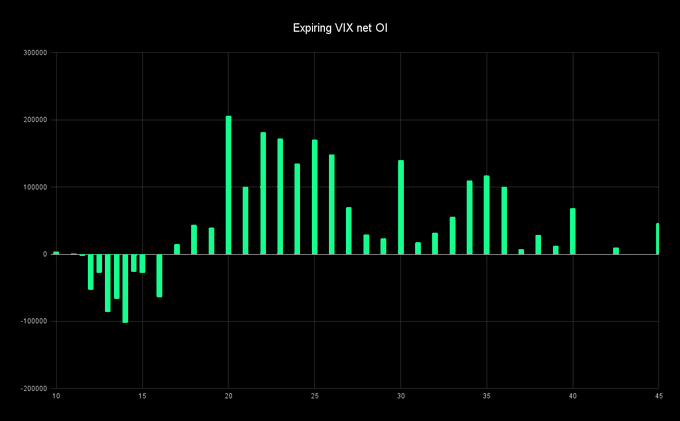

Tomorrow, the gamma at the 'VIX pin' of 17 will evaporate. Vol will be able to move more freely, while VIX dealers might sell SPX futures back into the market that were established as offsetting hedges.

1

5

53

CTAs have sold about 30B in S&P 500 and will remain sellers in all scenarios (up or down) over the next 5 days.

3

14

56

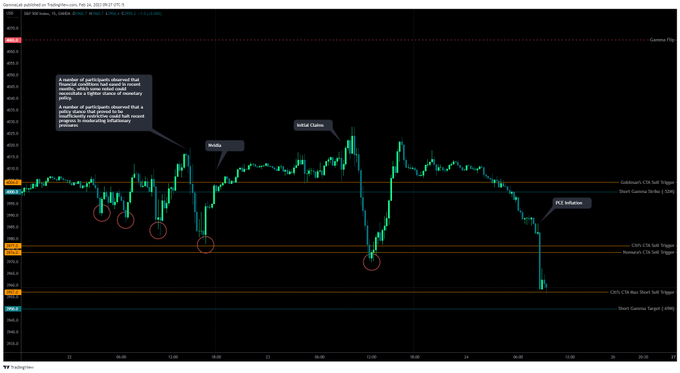

Below 4,050 0DTE is thinning out, which could lead to a acceleration of the sell-off, while 4,000 is solid support. $SPX

3

3

53

If the banking system starts to break it is game over for everybody. Banks sitting on unrealized bond losses of 600B, up from only 8B a year ago. This is a wake-up call for the Fed.

3

12

54

Learned a new acronym today: JOMO, the 'Joy Of Missing Out'. Buy a 6-month T-Bill, receive 5%, and enjoy the nice weather instead of wasting your life on Fintwit.

4

1

51

Can implied volatility lead the stock market? Some observations regarding the inverse relationship between the VIX and SPX complex.

SPX option dealers are required to constantly delta-hedge their option positions via SPX futures, which causes significant non-fundamental flows -…

2

14

50

McElligott: Yolo’ing into 0-1 DTE options has now been institutionalized by vol traders at many of the largest funds on the street. It’s not about retail alone playing this game anymore.

2

14

49

$SPX dealer gamma with a yearly low of -670M. 3,950 most prominent 0DTE strike. CTAs about to turn short.

6

8

50

30-year bond yields experienced the largest basis point spike since March 2020 today, after a failed auction.

1

18

49

SPX dealer gamma is negative again. Market makers will sell weakness and buy strength to re-hedge their option portfolios. This sucks liquidity out of the market. Expect increasing volatility.

5

8

45

I mean come on. Banks are imploding, yield curve stuck at -100 bps and Epstein back on the front page together with Dimon, but VIX still sub 20?

6

4

46

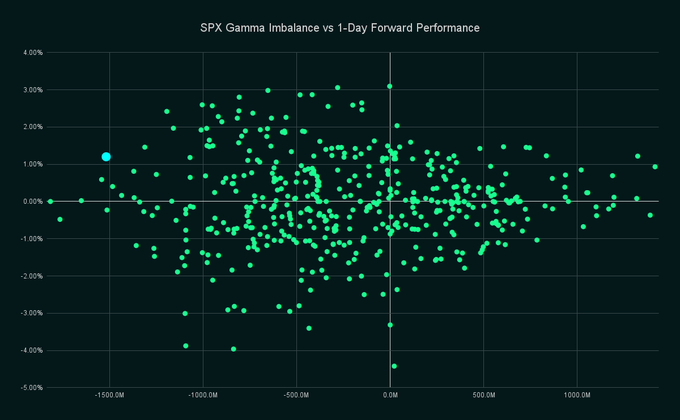

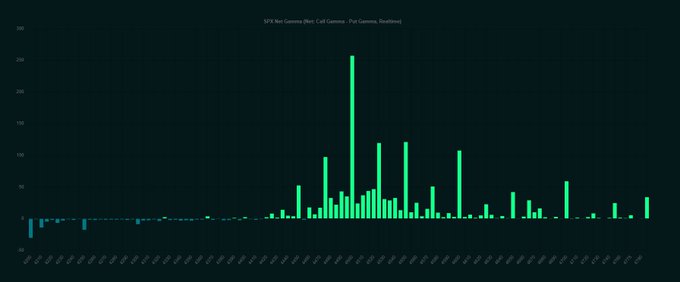

Don't get overly excited about today's performance. From a pure gamma perspective this bounce (cyan dot in chart below) was to be expected, and with an $SPX gamma imbalance of 1,160M we are now right back in the danger zone were drops of up to 4% are plausible.

0

11

46

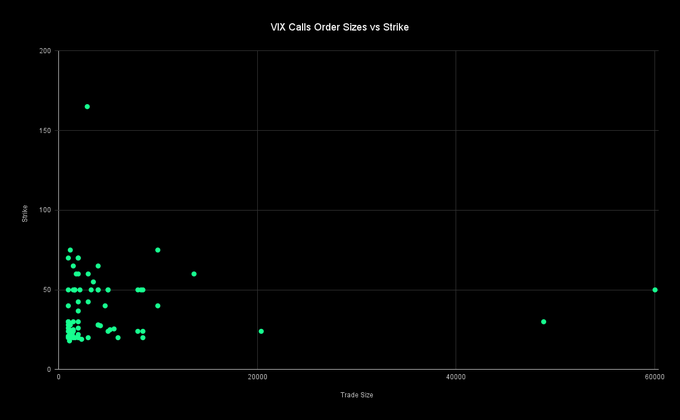

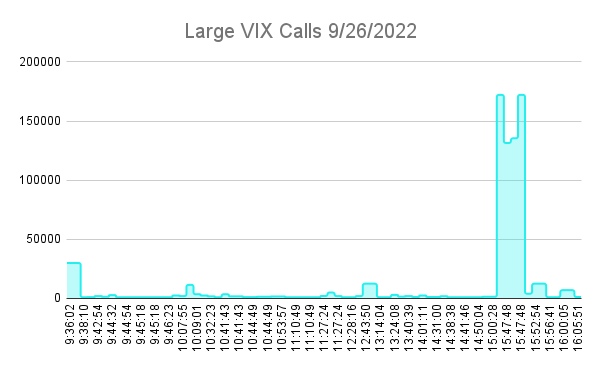

At 2:00 PM a MASSIVE $25 VIX call trade was entered. 270,700 contracts expiring in March.

3

4

47

@VigilantFox

@ManInAmericaUS

If it is an attack it has to be multipronged because the US population is too diverse genetically. Simplified scenario: 1) Initial attack, 2) Vaccination response, 3) Follow-up attack based on vaccination patterns. It's been well-described in academic literature.

3

9

44

Goldman in one sentence: Bottom is in, CTAs out of ammo, institutional macro hedges have reached extreme levels, mutual fund cash on the sideline at all-time high. CTAs flip levels 4055/4130.

11

7

44

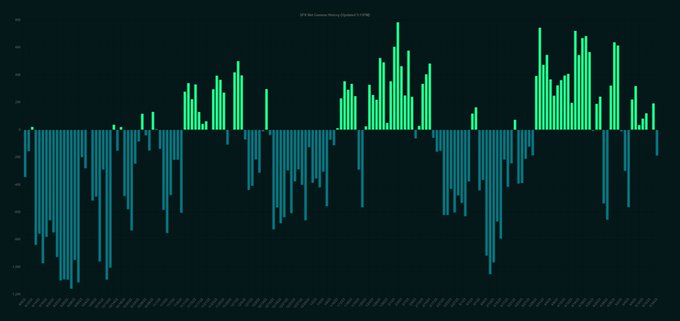

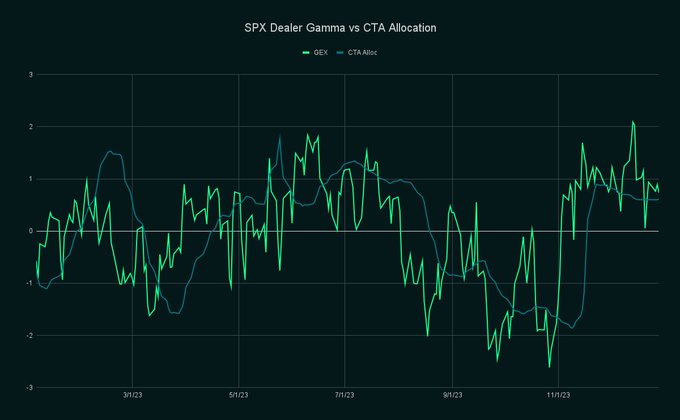

Aaand we are back in negative gamma land. Historically the gamma imbalance is a reliable early indicator for the positioning of price agnostic investors like CTAs/volctrl funds. Currently CTAs are max-long in $SPX and have allocated about 40B which is in the 75th percentile. So…

2

6

45

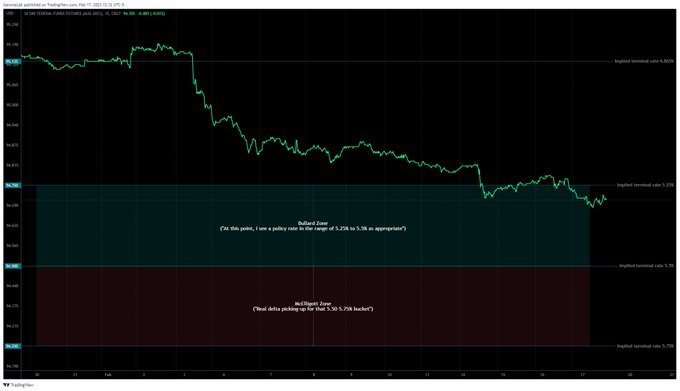

Nomura's McElligott is sensing demand for OTM FF options which would imply a terminal rate of 5.5-5.75% and even floats a 6% rate. It is safe to say that the market is not even remotely prepared for such a tail event.

1

9

45

$SPX put volume was 3rd highest of the year, while $VIX volume was 4th highest. We registered a numer of very large $VIX call orders due to OPEX, but those didn't affect the market and were cleared between 11:00 AM and 2:00 PM, although large SPX put orders started to show up at…

4

6

45

Instead of the overdue bounce, we got another drop in implied SPX dealer gamma to -1,846M. Sell-off still very orderly, no flash crash vibes or anything. Surreal.

2

11

42

Negative gamma imbalance means option dealers are delta-hedging by selling weakness and buying strength. They therefore take liquidity out of the market, which creates self-reflexive intraday trends. This is the largest systematic and price-agnostic force in the market. Stay…

5

7

44

The $SPX is back in a short gamma regime. CTA risk on deck now.

2

5

43

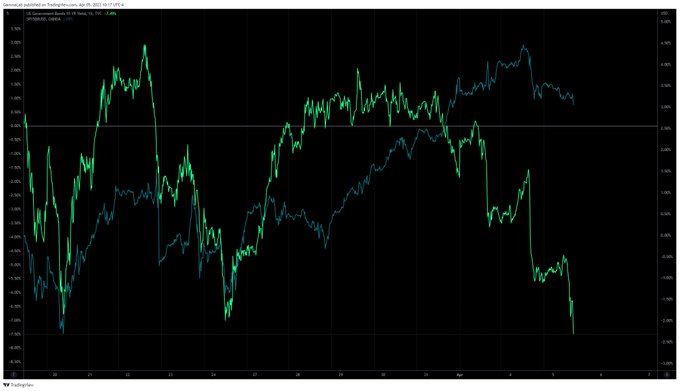

10-year yields are taking large steps lower, without a corresponding rally in SPX (blue line). Things are not looking good.

3

12

43

As the SPX is dropping to new lows.. 4,100 is not a terribly supportive gamma strike and a breach of this level would open the door for a resumption of the short gamma regime that has haunted the market for most of the last year.

4

5

43

Problem: VVIX up 23 handles since January 6th, but according to GS this should suggest -200 to -1,300 bps in SPX (index is up 7.7%). We keep pointing out another big disconnect between rate hike expectations and the index -> be careful.

1

11

42

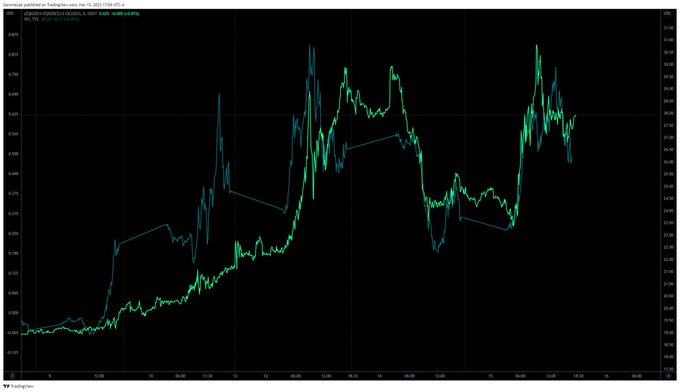

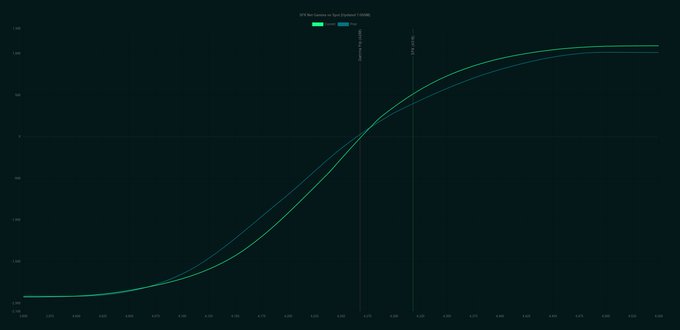

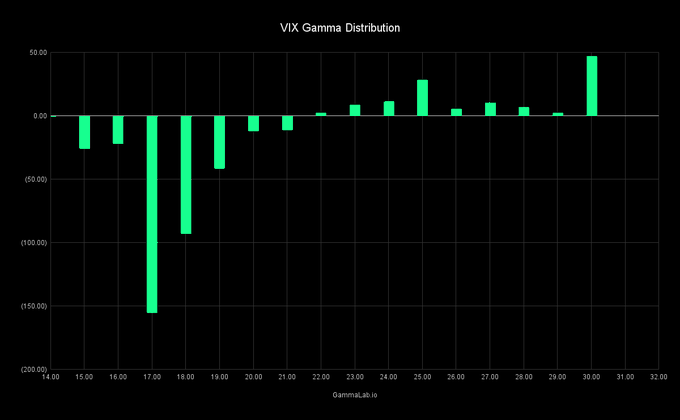

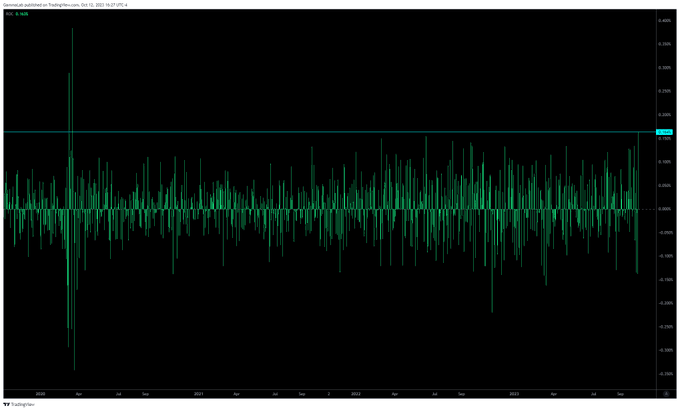

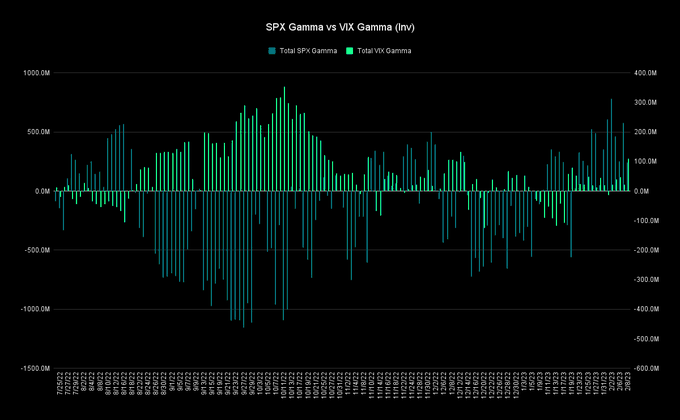

To expand on the VVIX issue. VIX gamma mirrors SPX gamma usually. Now as you can see from the chart below VIX gamma jumped higher without a corresponding move lower in SPX gamma -> investors hedging via VIX optionality.

2

5

41

Hartnett: The big risk is that recession and higher unemployment will cause higher, not lower long-term government bond yields as markets discount fiscal policy panic, politicians spending to avert social and political unrest. Yields then rise to punishing levels, causing a long…

4

10

40

Marketing... Nomura's McElligott is saying that the 'marketing lords', are exploiting investors 'fear of missing out' (fueled by 4-5% MMF returns) by selling vol against mega-cap tech stocks. McElligott notes that options-selling strategies have seen their assets increase by 60%…

1

13

38

Last time 2Y yields were at this level SPX was trading at 3,750.

3

5

40

Happy birthday to the most beautiful daughter in the world. Sorry for wasting so much time with meaningless things (like markets and stuff, ha) vs seeing you growing up. Much love, and back to work.

2

0

39

CTAs are the real danger here, but don't think we saw systematic traders selling into the close. The $SPX lost only ~2% over the last couple days give or take, that is not enough to convice trend-followers to change their stance. Think 4,600 is the level to watch, because a) this…

1

9

37

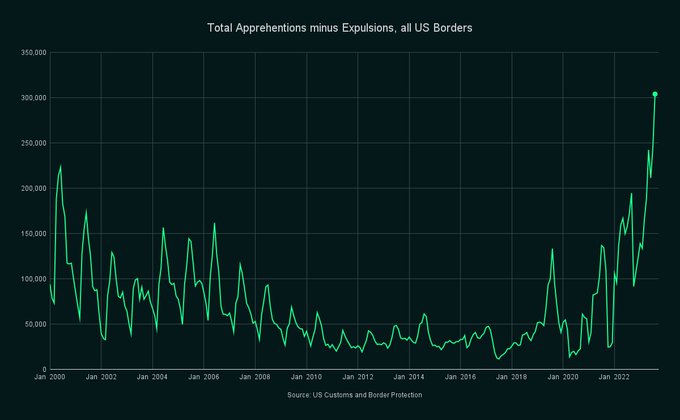

Chart: Illegal net migration into US. This might have massive implications for inflation but given the stigma, this issue is not well discussed. Q: How will this impact JOLTs, given that most migrants are single, male, young? Two ways this could play out: 1) Average hourly wages…

11

10

37

4 massive VIX calls ($50/$60 strikes) were hitting the market just before the close.

2

9

35

Institutional entities have become full-tilt day traders, using the certainty of dealer hedging flows that their orders create to then amplify and juice the intended directional market move before closing-out positions mere hours later by EOD.

2

7

36

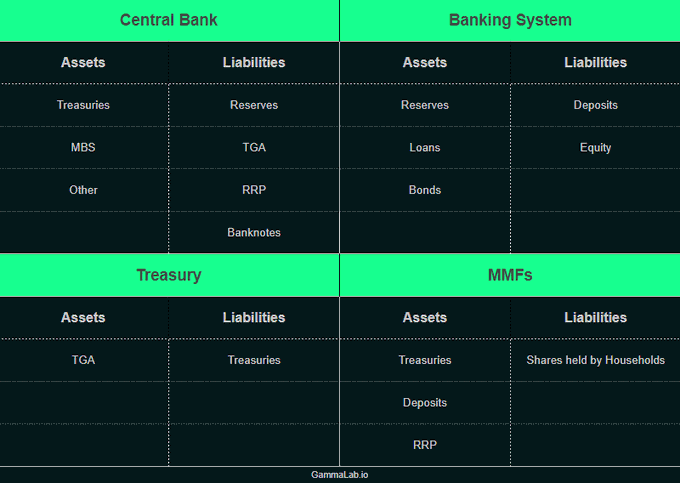

Cheat sheet to help you visualize how money moves around the financial system.

0

10

36

Tomorrow, quite a bunch of OTM $VIX calls expire. VIX dealers are short those calls, and thus hedge their exposure by going long VIX futures. As iV declines dealers are forced to sell futures, which suppresses volatility even more. Most of the adjustments are executed and we…

2

13

33

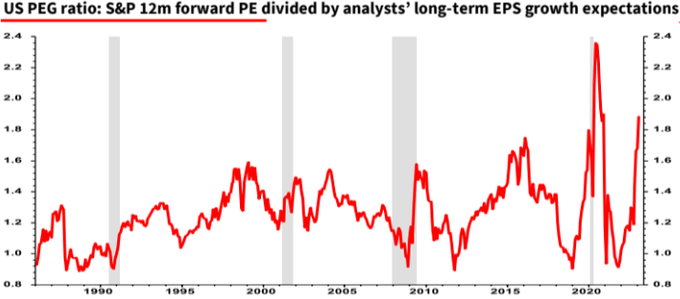

Albert Edwards: US valuations have ascended above the clouds into the thin and dangerous atmosphere of the ‘Death Zone’. (Chart below: S&P PE divided by estimates for long-term EPS growth).

1

15

35

Insane counter-rally. Lots of negative 0DTE gamma at 3,975-4,000 providing fuel.

2

11

35

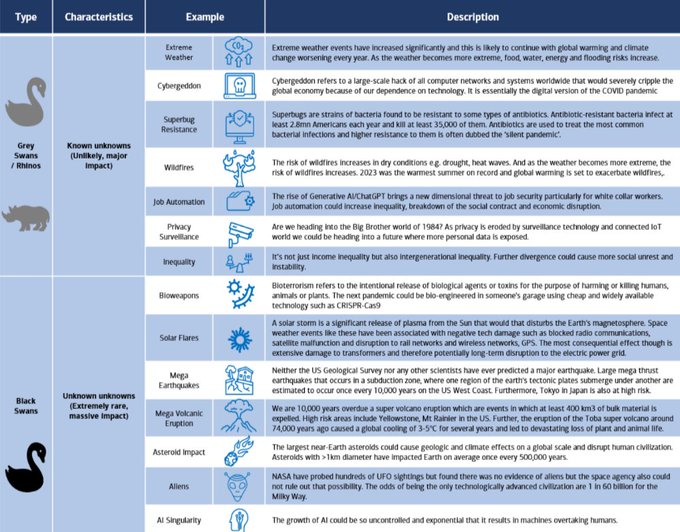

BofA goes full doom in new report. Covers every grey and black swan from Cybergeddon to Superbug Resistance, AI Singularity and Aliens.

2

6

35

Nomura's McElligott: We are in the midst of an angst-ridden pain-trade higher in stocks, which is pushing us back into increasingly “unstable” FOMO-type behavior, because nobody is there for this move.

2

6

35

$SPX realized vol was extremely suppressed since June thanks to intraday reversal flows/vol selling. The gap between implied/realized is getting too big to sustain, and we could very well see a new systematic seller in the form of vol control funds emerging soon.

3

7

32

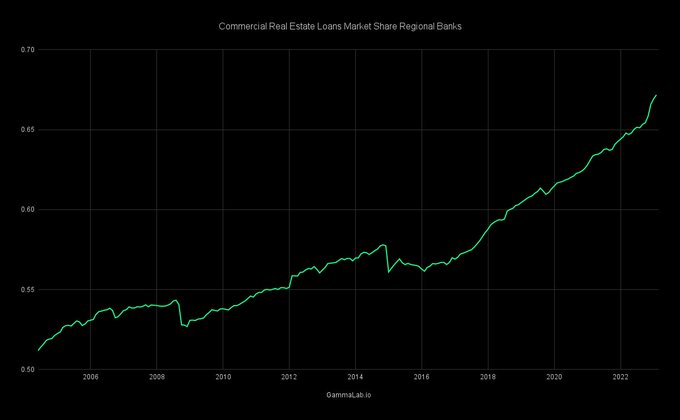

Regional banks have expanded their footprint in the commercial real estate market (CRE) since 08 from ~50% to 67%. Assuming $SIVB wipes out the start-up industry in CA, the CRE market on the West Coast will become a systemic risk channel that could endanger other regional banks…

2

10

34

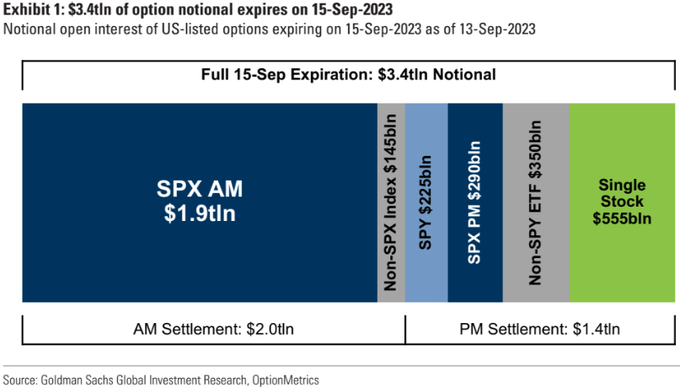

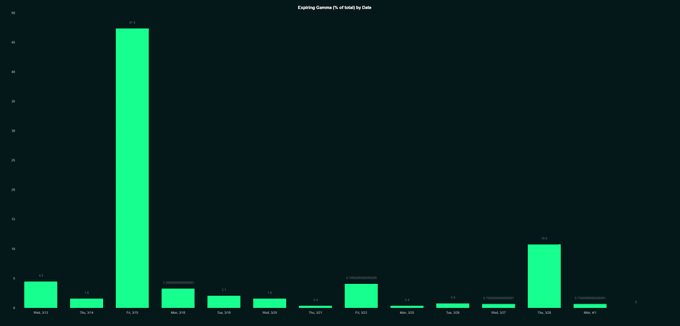

GS: We estimate that this Friday will be the largest September options expiration on record, driven by growth in index and ETF options volumes. We estimate that over $3.4 trillion of notional options exposure will expire this Friday, including $555 billion of notional single…

2

18

33

On Friday about 47% of gamma is expiring all else equal, which is quite a lot. We expect the $SPX to be boxed in between 5,170-5,200 or getting pinned at 5,200 until then.

4

8

34

@zerohedge

Stop it. Every time Dimon and Epstein appear in the same headline a bank fails shortly after (and gets rescued by JPM).

4

4

30

Never have momentum stocks been more overbought. Not even in 2020. It's a panic.

2

7

33

The pool party is over. Retail bought 3.9B in cash equities last week, according to JPMorgan, with most money flowing into $NDX, while $SPX was not in demand. In single stocks retail bought 1.3B, and the inflow was almost entirely accounted for by $TSLA (613M), $AAPL and $NVDA.

6

4

33

According to GS, CTAs will sell the $SPX in all scenarios over an one-week horizon.

3

6

33

Hurray, we have a new narrative: "6% terminal". The only asset class with a clear understanding of the situation seems to be the dollar index, which is getting ready to break out.

2

4

31

According to GS, CTAs are only minor buyers next week on a flat tape (700M in E-minis), but will sell up to 11B on a 2.5 STD sell-off. Nasdaq will be sold, no matter what.

1

7

32

According to GS, CTAs will sell 7B in S&P 500 E-minis on a down tape over a one week horizon. Up tape -4.4B, flat tape -5.6B.

6

7

32

JPM notes the US has never escaped a recession after yield curve inversions (10Y/3M): 'The damage has been done, and the fallout is likely still ahead of us. US mortgage payments as a share of income doubled, from 13% to 26%, and the savings rate has gone down almost to zero.'

5

12

33

Since 10:25 traders accumulating VIX calls with strikes between 50-70. Not seeing any news, and don't want to blow this out of proportion though..

1

5

31

JPMorgan: In options, retail net bought +$3.6B of delta and +$2.7B of gamma. The delta imbalance was the highest since Jul 2021. SPX/SPY call option buying contributed to $2.5B delta imbalance, in turn 70% of which were 0D and 1D to expiry.

4

7

32

Food +10%, electricity +12%, piped gas +26%, shelter +8%. Real Americans are dying a death by a thousand cuts and the Fed is doing victory laps? Maybe inflation is not their main concern?

1

5

31

$SPX gamma now at an insane -1,680M, touching down on the 2nd largest gamma strike at 4,350. Everything still astonishingly orderly.

2

3

31

$SPX dealer gamma 1,270M, that's a number in the 95th %ile. Gamma gravity at 4,500 is strong, expect a pin.

2

12

32

According to GS, this morning’s sell-off in bank stocks began as HF-centric (shorts), but starting to see L/O supply (passive) now too.

3

6

32

It is getting serious: $SPX gamma about to turn positive (flip level at 3830). Additionally, the market has now cleared short-term CTA triggers and STIRs are moving aggressively higher as investors are embracing the idea of more dovish Fed.

3

1

31

Terminal yield is moving higher. SPX future using blackout period as cover to move higher as well. Sneaky..

1

4

31

Vol control bought another 7B in equities today as the market remains stuck in a high-gamma, low-vol environment. Upside is limited due to the massive 'Call Wall' at 4,600 and price-agnostic flows will not be a tailwind much longer all else equal according to GS.

1

5

30

GS expects sees CTAs buying E-mini in all scenarios over a one-week horizon: Down tape +7,7B, flat tape 29B, up tape +30,9B.

4

8

29

Ok, how about we see the rally of our lifetimes into Armageddon (assumed that CPI plays along)? Goldman says that CTAs are short $289B in global bonds (0th percentile) vs a theoretical max of +$444B. Not convinced? Equity CTAs are also max short.

3

3

30

CTAs are running out of bullets according to GS, but call option volume in 'meme stocks' is exploding higher. -> According to JPM the buying impulse of young retail investors is the highest since last August, but also boomers are back and have injected over 100B YTD.

5

6

28

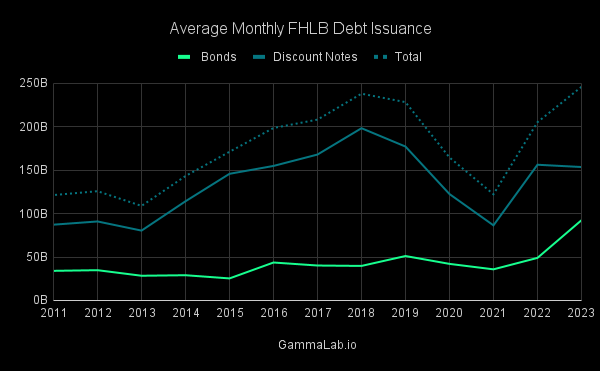

Yes, regional banks might have systemic funding issues, and here's some evidence: Small banks can either tap the discount window or Federal Home Loan Bank advances when funding shortfalls arise. FHBL advances are not available on a real-time basis, so let's look at FHLB debt…

1

9

30

McElligott: It still seems to me that the conditions simply aren’t there yet for any sort of equities crash risk because we just aren’t seeing funds long enough in the market yet. It’s only when funds are 'brick long' that this forces them into a position where hedges are…

2

6

30

CTAs are now big buyers over the next week and the next month even on a flat tape per GS.

2

5

30

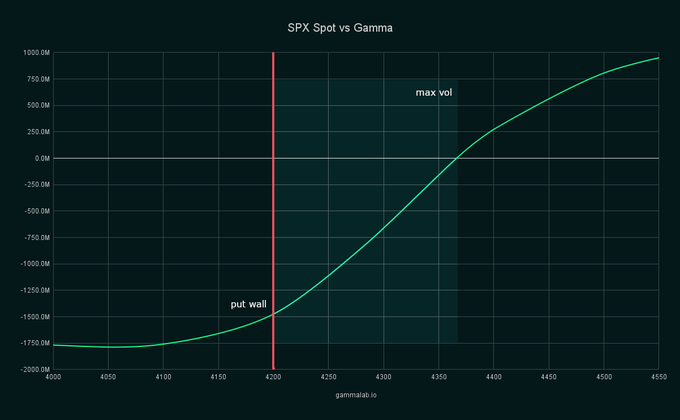

The $SPX currently trading at 4,280, while dealer gamma is running at -570M, (high-vol environment/room to drop fast), and major support is located at 4,200 (put wall). Vol control fund exposure is still in the 80th percentile looking back 360 days (which poses a downside risk),…

2

8

28