Florian Kronawitter

@fkronawitter1

Followers

13,970

Following

526

Media

959

Statuses

7,681

Here to share what I've learned during 17 years on the frontlines of the economy and markets

London

Joined April 2021

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

こどもの日

• 537801 Tweets

#해피큥데이

• 104455 Tweets

Al Jazeera

• 84909 Tweets

GW最終日

• 80718 Tweets

Bernard Hill

• 71204 Tweets

Vlad

• 69993 Tweets

Spurs

• 58359 Tweets

West Ham

• 56810 Tweets

Tottenham

• 53834 Tweets

Sivasspor

• 44696 Tweets

سعد اللذيذ

• 43040 Tweets

#GSvSVS

• 40465 Tweets

Theoden

• 37081 Tweets

BBL Drizzy

• 33918 Tweets

#LIVTOT

• 31700 Tweets

Gallagher

• 26347 Tweets

Happy Cinco de Mayo

• 25303 Tweets

D-1 to BLOSSOM

• 21882 Tweets

Ange

• 20702 Tweets

Mertens

• 15816 Tweets

LOSE MY BREATH MV TEASER 2

• 14433 Tweets

Rohan

• 14283 Tweets

Tim Scott

• 13896 Tweets

Anfield

• 13597 Tweets

Gakpo

• 11038 Tweets

#محمد_عبده

• 10845 Tweets

Ziyech

• 10057 Tweets

Pinned Tweet

I just published a new post. In it:

- Why most of the AI value may end up with consumers and industrial profits

- Why upgrading the SME tech stack via "AI Buyouts" is a generational opportunity

It is free, if you like it, please share it!

5

8

49

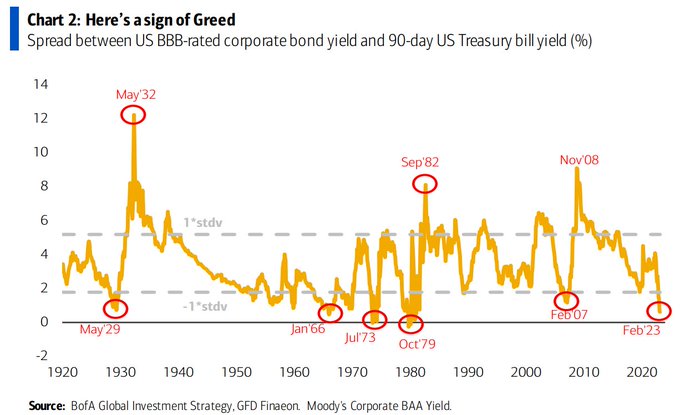

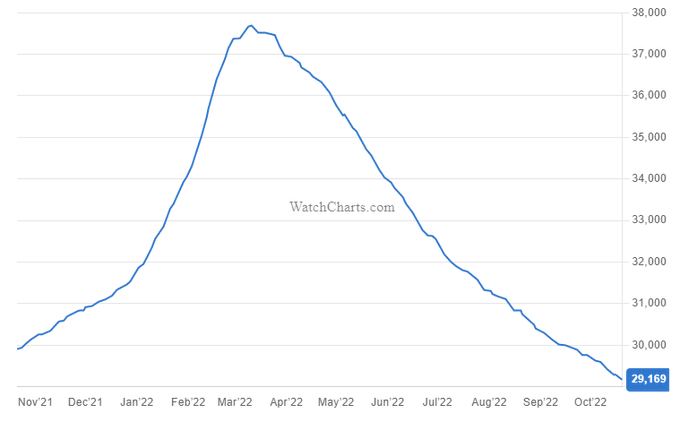

#Rolex

No relief in sight, prices continue to slide (ave. of 30 best selling models in USD)

47

66

928

"BLACKROCK SEES 'SIGNIFICANT INTEREST' AMONG PENSION FUNDS TO CUT EQUITY EXPOSURE, LOCK IN YIELDS"

There is always enough demand for Treasuries. You just need to sell equities for it

When do you sell equities? When you think growth slows down (1/2)

40

123

858

Over the past 12 days, hedge funds covered more US Tech shorts than at any point in the last decade (except meme blow up Jan 21)

With the cover bid gone, underperformance is now likely for the sector

25

140

722

QRA Update:

- The Treasury upped coupon auction size to $348bn in Q1 vs $338bn in Q4. This is below their own guidance of $396-$460

- They caved in face of difficult 10yr/30yr auction and are prioritising bills

This is a huge policy decision

(1/3)

17

120

562

The banking crisis is not over

4-week T-Bills are bid at 3.8%, a full 1% below FFR (!), as especially foreign banks scramble for access to this pristine collateral

Contrast this to 4.8% paid daily in the the RRP

What's next?

53

110

525

The most important overnight news

After Fed Gov Bowman, now Janet Yellen herself heavily alludes to allowing big banks to hold MORE US Treasuries

This is QE, just named differently. Expect it to happen AFTER midterms, as oil likely rallies hard on it

30

121

504

Yesterday's hedge fund short cover was the highest since January 2021 and ranks in the 99.9th Percentile since 2012 (GS)

8

101

443

@Gerashchenko_en

“According to some reports he is a neo-nazi”??

He has an SS tattoo on his right collar bone!!

22

12

410

#Rolex

prices trending down again (average of 30 popular models)

As you know I've been sharing this chart on a weekly basis

28

54

397

Mastercard July spending pulse - notice trailing furniture, luxury and electronics

7

74

395

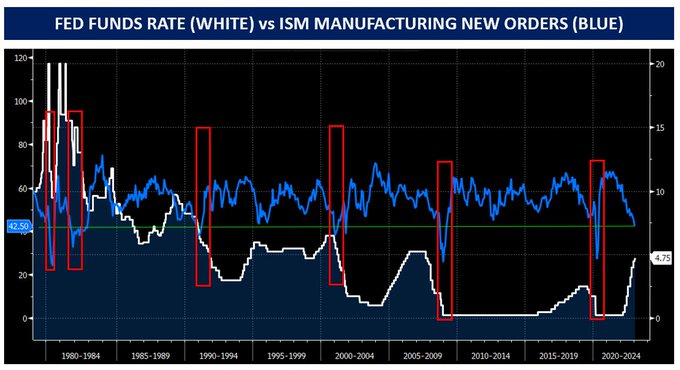

Whenever ISM Manufacturing New Orders were as low as today, the Fed had already cut rates

Even under Volcker

18

71

394

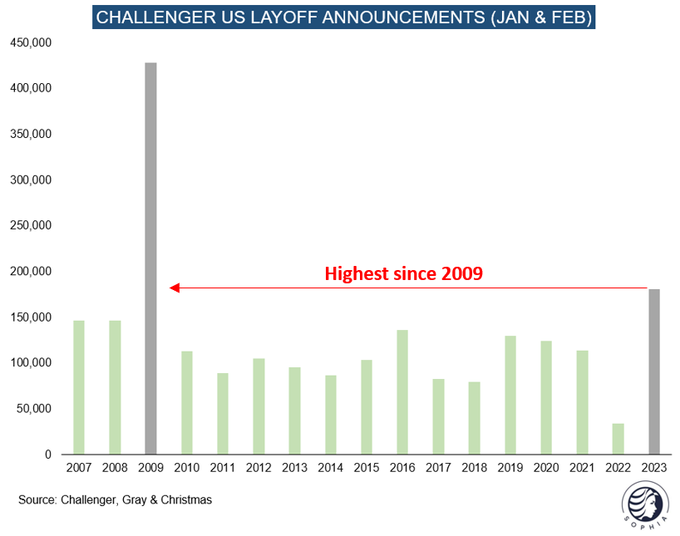

🇺🇸 January large bankruptcies highest in over a decade

Things you don't see in a soft landing?

12

94

353

First Republic is turning up the heat on bank deposit competition, now offering 4.5% on 60-day time deposits (CD)

Will other banks have to react?

49

66

312

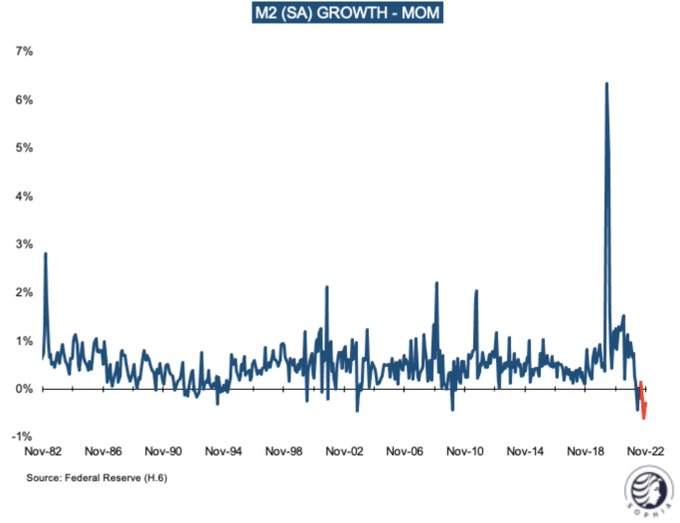

M2 saw the steepest month-to-month drop since 1982

No wonder the Fed is getting nervous

33

81

298

🇺🇸 Thirteen economists, NO ONE has acceleration on their bingo card

So guess that's what we'll get...

h/t

@darioperkins

30

49

298

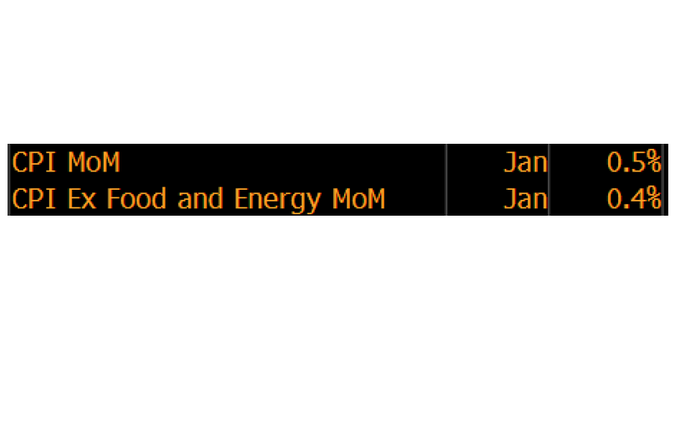

Today's CPI release is telling inflation's past

Recent oil price action is telling inflation's future

🚩

25

17

255

I have heard so many people say they want to buy the S&P at 4200

It makes me think we either never get there, or we blow way past it

35

17

252

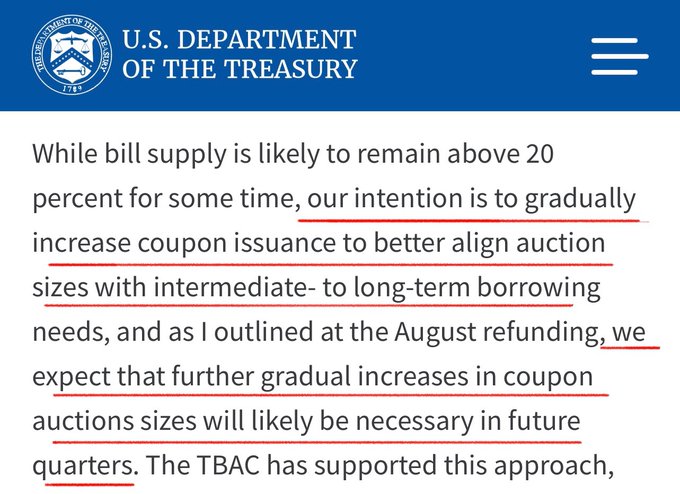

Are you hoping that the QRA will bail out the stock market this week via bills instead of coupon (=long end) issuance?

Then you should read Assistant Treasury Secretary Josh Frost‘s speech from the 21st Sept

He reiterates coupon auction size will continue to increase (1/3)

14

40

257

In the short run, this is positive for risk assets. In the long run, it is another step towards a world of structurally higher inflation

(3/3)

16

19

252

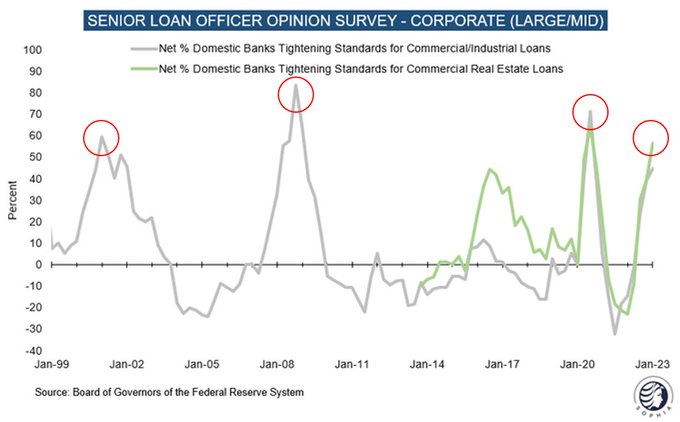

Banks tightened their lending standards to historical extremes

In the past, default waves followed within 6-12 months

Will this time be different?

13

58

242

@ianbremmer

Wild guess- it was both the Trump and Biden administration flooding the world with printed USD, encouraged by the Fed

34

4

202

The nominal growth deceleration in retail has been tremendous

Black Friday YOY 2022: +15%

Black Friday YOY 2023: +2.5%

10

42

219

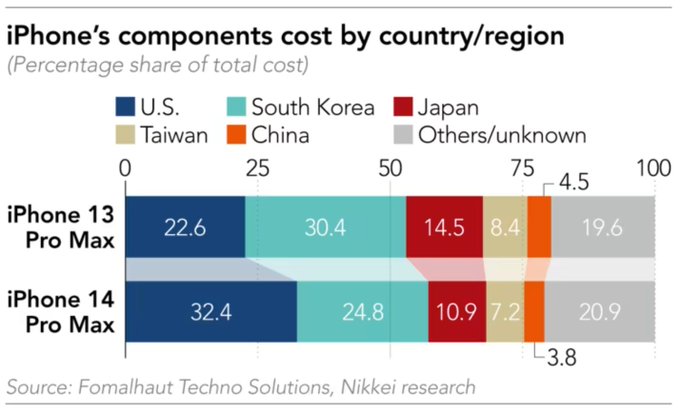

Apple iPhone 14 production costs are 20% higher than predecessor $AAPL

Why? More proprietary chips and more US content

This is before production is diversified away from China

Geopolitics is inflationary - Sign of the times

8

61

208

🇺🇸 Last week saw the biggest liquidity injection into financial markets since 2021

Treasury spending ($45bn) and RRP drawdown ($139bn) by far outweighed QT ($53bn)

12

38

206

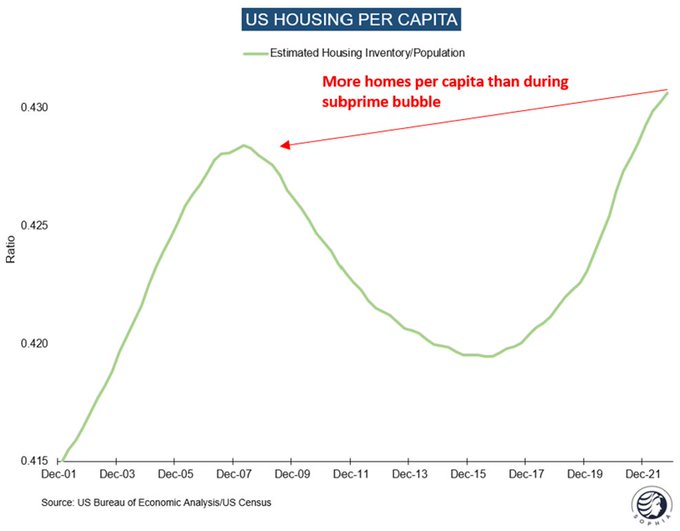

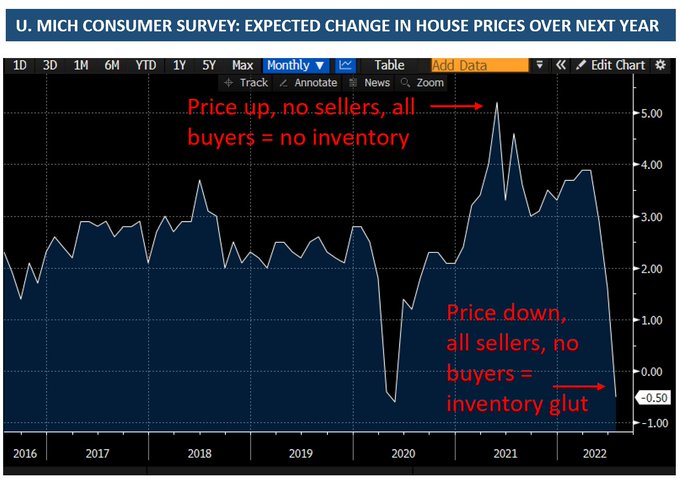

Lower rates will set US housing on fire

The industrial cycle is turning and inventories are low

Throw in the IRA

Sounds bullish commodities to me

14

24

197

🇺🇸 M2 Money Supply for February saw the largest month-on-month decline since 1982

Deflation is coming

7

54

188

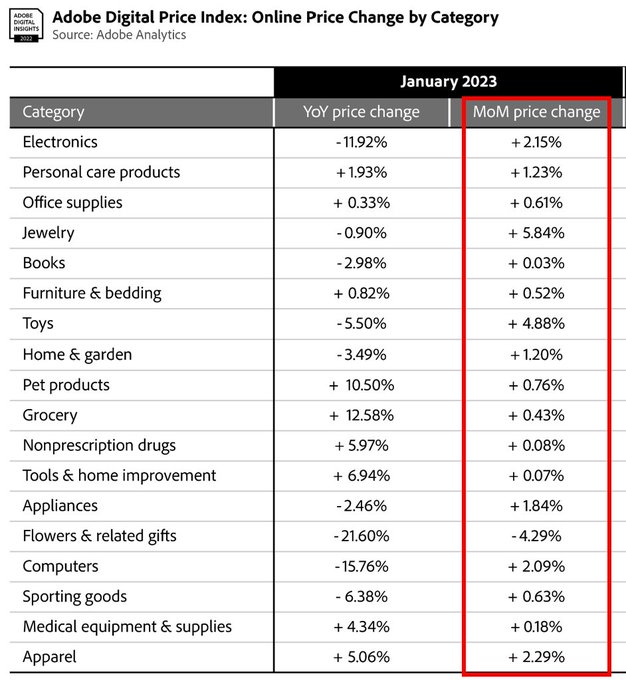

#Inflation

Adobe ecommerce price index sees month-on-month inflation across most categories

January seasonal bump in full swing

8

37

185

The risk?

Reflexivity gets to work. Equities sold to buy bonds. Lower stock prices get companies to cut. That slows the economy further. Etc.

This is why the endgame is *likely* more Fed liquidity. It creates additional Treasury demand - no one wants a downward spiral (2/2)

7

9

179

The Q2 liquidity vortex is now in full swing, as I predicted in this extensive post some time ago

It seems probable that all assets are affected, with cash likely the best performer over the coming weeks. Asset rallies should likely now be sold (1/3)

6

20

186

Milton Friedman: "Inflation is always and everywhere a monetary phenomenon"

M2 Money Supply currently shrinking - a historical anomaly

Deflationary prints ahead, in my view

8

23

175

1 -

#ConnectingTheDots

The Bloomberg economist consensus for January is out

Expectations are for a "hot" month-on-month number, that annualises at ~5-6%

A significant step-up from recent prints

8

21

174

Bond markets currently assume a calamitous event that forces the Fed to cut rates significantly by the Fall

Equities assume that said calamitous event has no impact on their earnings

One of the two is wrong 🚩🚩🚩

16

23

166

The Treasury essentially told us that whenever the market will get difficult (which it did around 5.5%) it will listen

The cost of this is that the inflation-taming effect of higher long-end yields gets neutered

(2/3)

2

16

167

I just published a new post. In it:

- Recapping the case for "Secular Reflation"

- What I look for to see if I'm wrong

- Still all cash and expecting market weakness, intending to use it to deploy into theme

It is free, if you like it, please share it!

13

27

166

A gentle reminder that no one knows anything:

In 2019, the overwhelming consensus in markets and academia: "inflation is dead"

Two years later, the highest inflation in 40 years

10

22

163

In their own slides, the US Treasury tells you that:

- It seeks the least cost (term premium!)

- It does not time the market

- Does not react to short-term demand fluctuations

- Bills mainly for rapid cash raises (eg Covid, TGA refill)

It's all there for those who care to look

6

20

160

⚠️ General Mills results for Q4:

Price: + 11%

Volume: -6%

Also known as “Pay more, get less”

How can anyone think this is a sign of a healthy economy?

What happens down the value chain, at supplier biz, as volume declines?

What happens once consumer excess savings run out?

23

25

156

Today is the second recent day that stocks fall while bond yields fall - the opposite of '22

Things don't change overnight, but a regime shift is under way. Pay attention to the market 🚩🚩🚩

15

8

151

1- German Chemical co Lanxess issued a drastic profit warning last night

- Demand is "worse than Lehman"

- Weakness "even from usually stable consumer products"

12

32

153

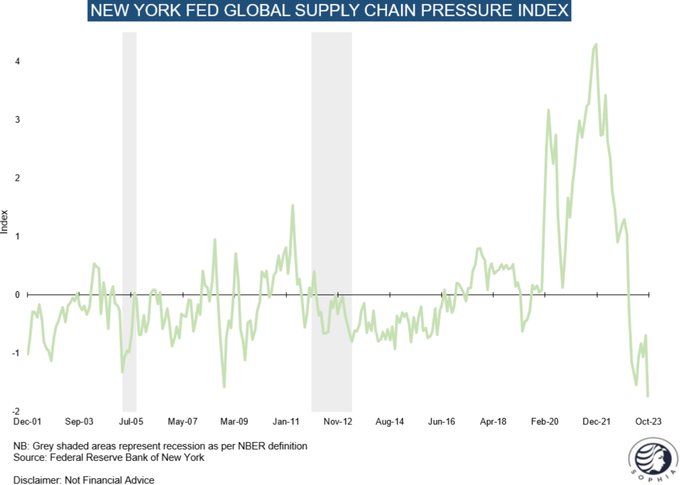

🇺🇸 The most important chart for 2024

Supply chains are getting tighter again, historically they have lead CPI by ~5 months

12

32

152

The market went up in a straight for 3 months

The QRA was bad, but most ignored it hoping Powell would bail them out

He didn’t, so now the sale begins

11

11

143

Some thoughts on Treasuries and TIPS:

The 30-Year Treasury ETF ($TLT) saw record trading volume yesterday, indicating forced liquidation which often occurs near a bottom (1/5)

Trading volumes in $TLT today set a record, breaking the March 6, 2020 pandemic peak.

6

6

26

12

12

143

Yesterday, politics panicked

The flood of bills will loosen financial conditions and stimulate the economy

Parts of the US market are pricing in recession and dropped 20% (eg small caps)

I like long Russell 2000 here as the fastest horse

Not advice

16

18

140

Powell basically ignoring the recent inflation hump should further fuel the already strong monetary debasement vibes

I've bought some Gold Miner exposure for it, which are at a multi-decade low vs Gold

Also sold some 30-yr

Not advice

22

5

137

The following three are at odds:

ES at 4400 with 25% earnings growth until ‘25

2Y10Y at -40bps

Oil at 75

They are either too cheap, or too expensive in relation to another

18

6

132

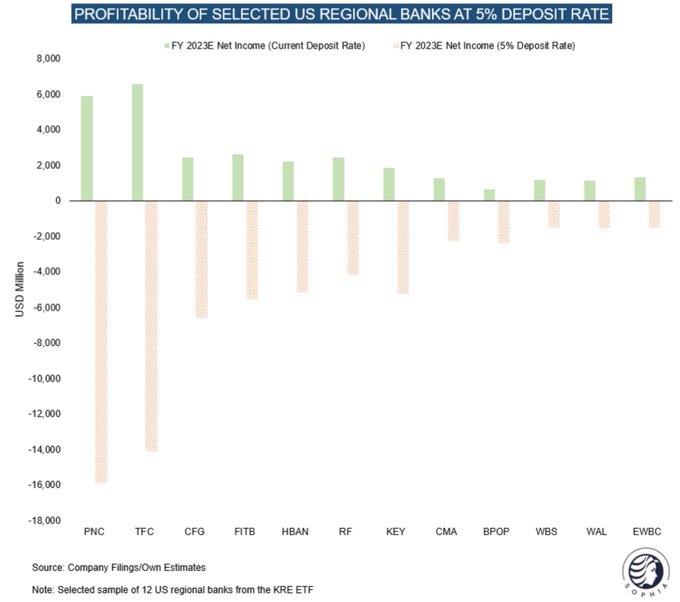

1- 🇺🇸 Why the US regional bank issue extends beyond Silicon Valley bank

Regional banks pay 0%-1% on deposits while the FFR is 5%

Many are unprofitable if they were to pay "market" rates (!) on these deposits

10

18

131

I just published a new "Next Economy" post. In it:

- What 13 years of QE have done to the financial system

- Why levered loans likely are the next crisis flashpoint

- Why I've shifted my view toward a "hard landing" on recent data

Enjoy the read!

21

24

131

🇺🇸 The issue with US regional banks in one *illustrative* chart

Profitability is gone once deposits pay market rates. No bank profits -> no lending -> credit crunch

Government deposit guarantees don’t fix this, only interest rate cuts do

19

34

128

Many signs the US economy is accelerating

Only reason to buy 30-year bonds is recession/slowdown fears (or matching liabilities if pension fund etc)

High supply

Path of least resistance for 30-year yields seems up

What am I missing?

46

10

128

I just published a new post. In it:

- Why demographic change could limit labor losses this time as corporates cut cost

- Why I am fading market consensus across equities, dollar, energy and vol

It is free, if you like it, please share it!

11

21

125

🇺🇸 In the inflationary 1970s, unemployment rose only many months after the start of a recession (e.g. 8 months in '73-'75)

Why? Assuming a tight labor market, companies "hoarded" labor, until their margins forced them to change course

Will we see a repeat in '23?

9

18

120

I just published a new post. In it:

- Recent data suggests the Fed's dovish worries have merit

- A corporate margin crunch is the key risk for '24

- How I adapted my positioning

It is free, if you like it, please share it!

14

13

120

🇺🇸 Treasury auctions next week

Also known as "the wall of money" 😳

9

11

123

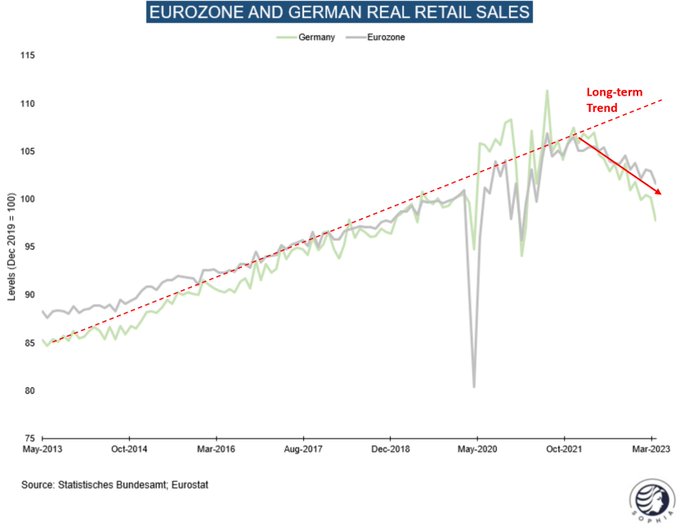

🇪🇺 European Retail Sales are trending down in real terms

With everyone focussed on the US, is Europe the more concerning story?

12

26

120

Small caps are saying loudly today that the current level of long-term rates is an issue for them

5

5

118

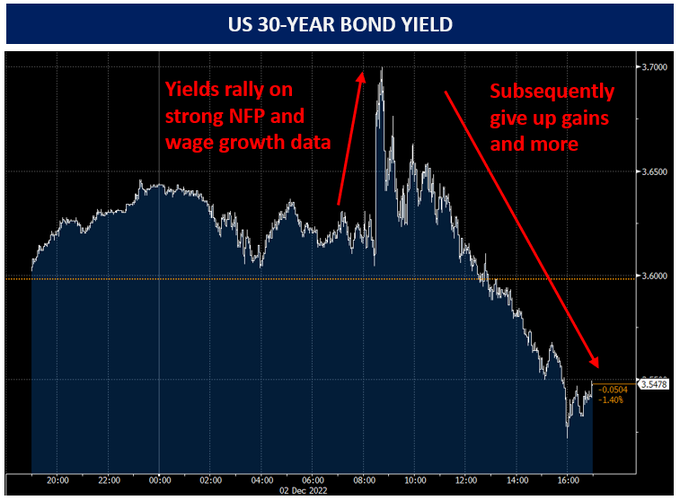

1-

#ConnectingTheDots

On Friday, the US released employment numbers

Of particular note was strong wage growth for November, +0.6% m-o-m (>7% annualised)

US bond yields should have RALLIED on this highly inflationary signal, instead they FELL

10

18

118

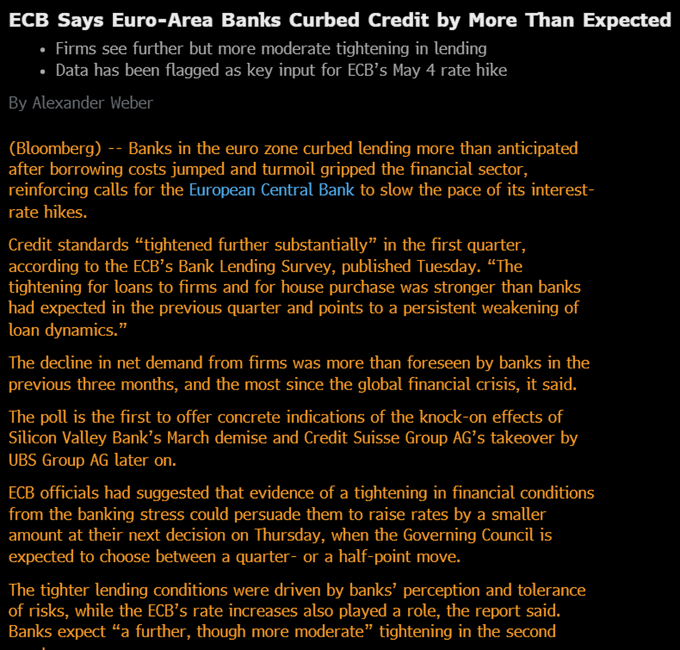

To be clear, even if banks recede from headlines in coming days, the credit crunch will continue

3

19

118

🇪🇺 While everyone's focus is on US banks and lending, EU credit already contracts at a persistent pace

4

22

120

I closed all bearish positions

Keeping the longs

22

1

112

My view on what's next:

- ECB won't hike 50bps anymore tomorrow

- US will give blanket guarantee for all deposits

- Fed will pause next week

All good for bonds. Equities may squeeze on this before falling apart, but uncertain on sequence

22

6

111

I just published a new post. In it:

- Why a recession may finally come in '24

- How I've positioned in light of a market that is very long equities and very short the US Dollar (not advice)

It is free, if you like it, please share it!

10

10

112

1-

#ConnectingTheDots

Commodities/Oil & Gas

We are currently in the ~4th inning of an economic slowdown

8

22

110

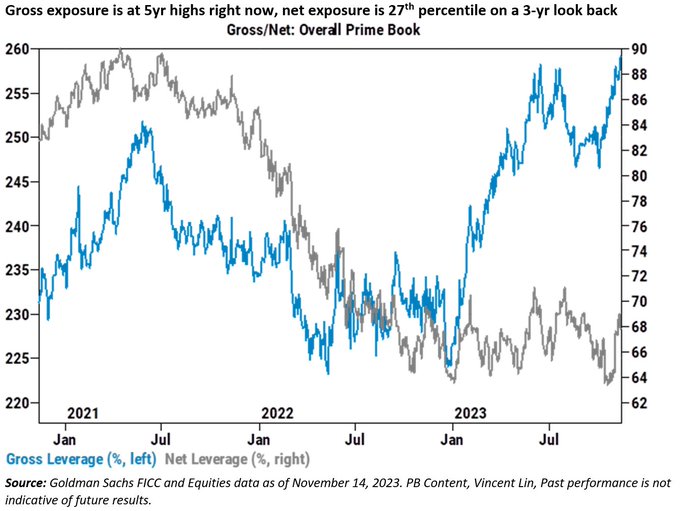

Equity L/S Hedge Funds have high gross and low net exposure

Their short side is stuffed with high beta "trash". Regional Banks, Solar, Unprofitable Tech, Small Caps etc.

Their pain trade is these areas squeezing. This can become self-fulfilling as they are forced to cover

6

17

111

So far this year, the drawdown of the Treasury General Account has de-facto neutralised QT

This changes from next week until mid-May, as taxes are paid and the TGA grows again

9

16

106

Hard to see how this 30-year auction is not bearish

Supply issue front-of-mind again and equity sentiment very bullish

I am adding to equity downside bets on this

Could be wrong, not advice

9

4

108

QRA:

Some coupon increase, especially in 2-7 year, but also 10-30 year

Removes the conspiracy bull case "The Treasury will manipulate markets to S&P = 6000"

Medium term = headwind on assets

Short term = FOMC tonight will dictate next move

10

8

100

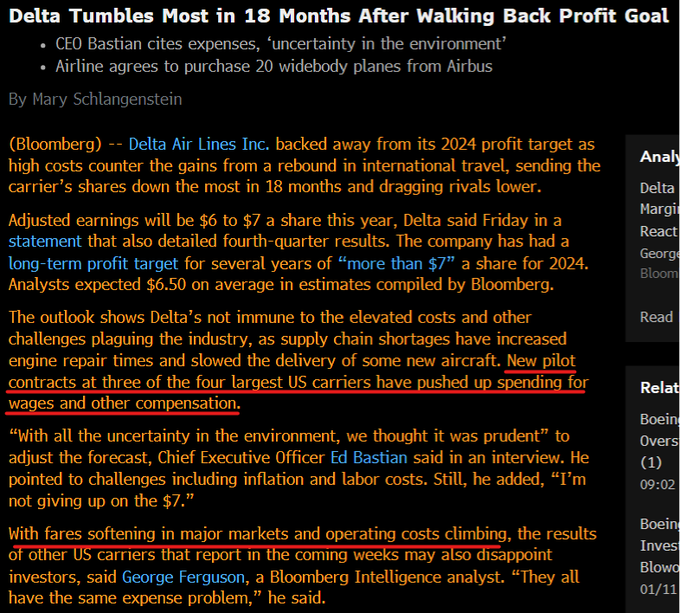

Delta Airlines is a great example for the margin crush corporates to come that I've discussed in many recent posts

Pricing power wanes but labor costs keep rising

6

24

110

Small caps down while yields are down this week = not a bullish sign

Could be consolidation after last week's squeeze. Still, something to pay close attention to

Remember, small caps employ 50% of Americans

10

10

106

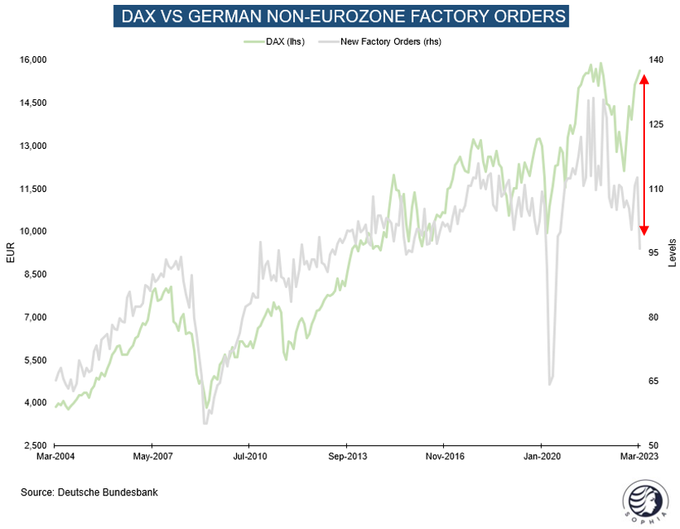

🇩🇪 German factory orders are rolling over - when will the DAX follow?

12

27

106

🇩🇪 Defence Minister Pistorius states in an interview today that Europe has 5 years to re-arm

Putin has the Baltics in sight, and is ramping up military production at a very aggressive pace

He is one of the few paying attention

20

6

105

The slack in the global supply chain now exceeds the '08/'09 financial crisis

Goods inflation is dead, for now

4

17

102

🇺🇸 US job cuts year-to-date are the highest since 2009

6

26

102

I just published a new post. In it:

- Politics panicked and loosened fin. conditions

- Near term relief is traded for higher LT inflation

- Long Russell now for a short squeeze (not advice)

It is free, if you like it, please share it!

8

10

102

I will be reaching for some US equity downside on the futures open. I see the very near-term path bearish into the week's first long-end auction on Wed

Beyond that I see several diverging, possible scenarios. I will lay these out in a post tomorrow

As always, could be wrong

9

1

103

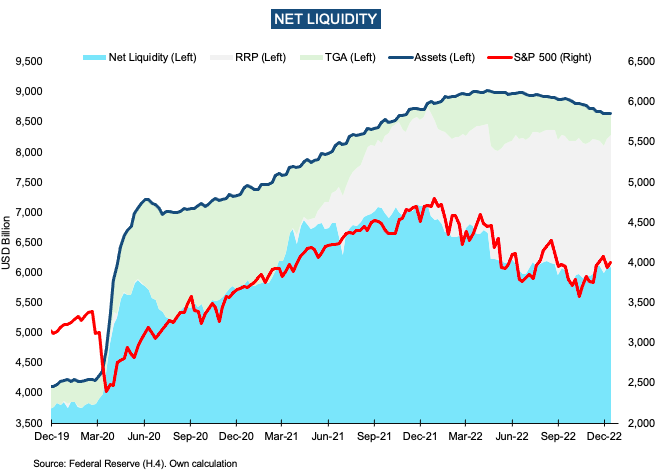

#Liquidity

This past year, the S&P 500 has tracked "Net Liquidity" closely

Over the next two weeks, this measure faces a ~$150bn headwind ⚠️

The Treasury Account increases by $80bn with tax payments + $60-90bn QT rolls off between today and month end

@kittysquiddy

7

14

102

🇺🇸Soft landing seems unlikely, at least for US corporate profits

Expect a significant step down by Q2 (still some months away)

1

27

100

🇺🇸 Dallas Fed Bank Survey shows a significant decline in loan volume post the Silicon Valley Bank crisis

The credit crunch is happening now, not at some vague date in the future⚠️

4

25

99

Think we are entering short squeeze territory

Hedge funds have low net exposure and are short small caps, unprofitable Tech, biotech etc.

A panic-cover bid seems possible here

2

5

100

1-

#ConnectingTheDots

Lots of focus on what the Fed will do next, and whether inflation comes down

That is the WRONG debate

Yes, inflation has PEAKED. Yes, it will come DOWN

But why is the 10-Year is UP, despite declining inflation expectations?

10

12

99

My current probabilities how the Treasury rout ends:

40% Equities sell off, growth outlook changes, gives bonds a bid

40% They drop until policy changes. UK gilt crisis playbook

10% Yields stabilise by themselves

10% Crack-up boom, yields and stocks keep rising

9

10

94

I just published a new post. In it:

- The treasury rout likely needs a catalyst to end

- Equities are at risk just as the market bats for a rebound

- How I plan to play the coming weeks (not advice)

It is free, if you like it, please share it!

12

18

98

The true measure of Central Bank liquidity?

Rolex prices stabilised since the Fall

3

10

97

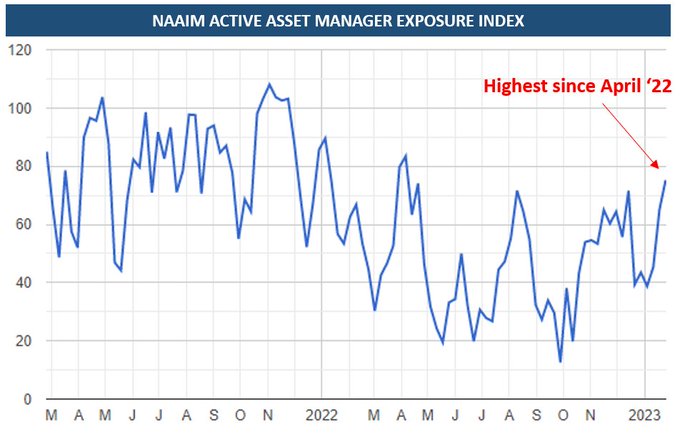

NAAIM Active Manager Exposure highest since April '22

7

19

95

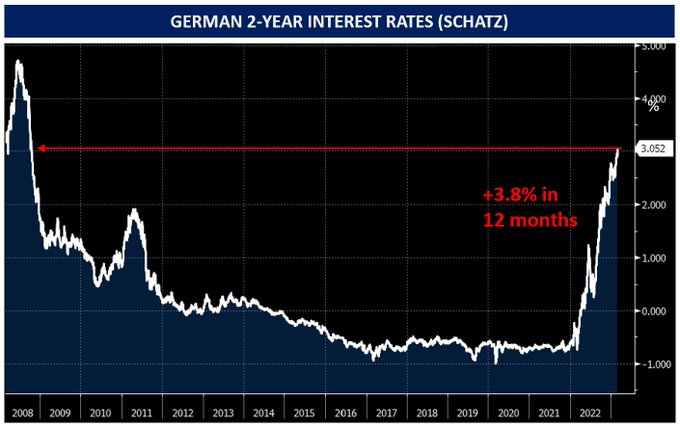

🇩🇪 German 2-Year interest rate now the highest in 14 years, from negative (!) just 12 months ago

The lags of monetary policy are supposedly "long and variable" - Milton Friedman

What could go wrong?

4

6

94

🇺🇸 I mentioned increasing signs of labor market weakness in my post yesterday

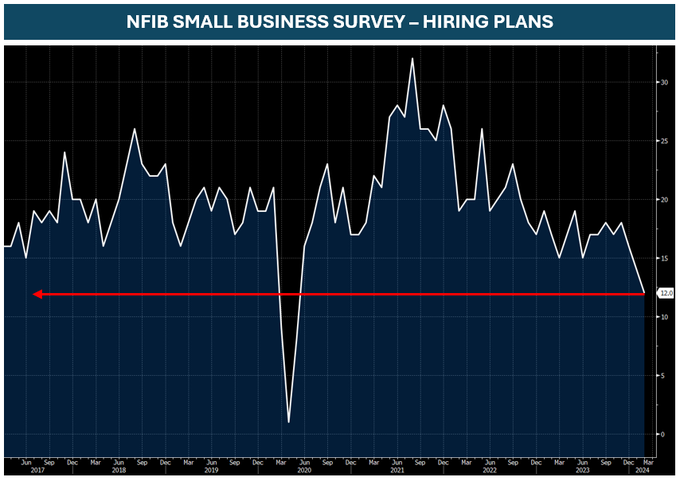

Today's NFIB survey provides another datapoint in that trend, with Small Biz Hiring Plans now the lowest in 7 years

9

16

97

Downside protection appears very cheap right now

"Hedge when you can, not when you must"

4

6

96

1- BofA sees March wage growth down to +2%, based on their deposit data

This is significantly below other recent measures of wage growth (e.g. Atlanta Fed, NFP)

4

15

95

Another argument that speaks for rotation within equities from leaders to laggards

Hedge Funds are maxed out on the Magnificent 7

9

13

95

Happy Thanksgiving!

I just published a new post. In it:

- Why I have exited my equity long exposure

- Why I see increasing risk to European economies

It is free, if you like it, please share it!

11

8

91

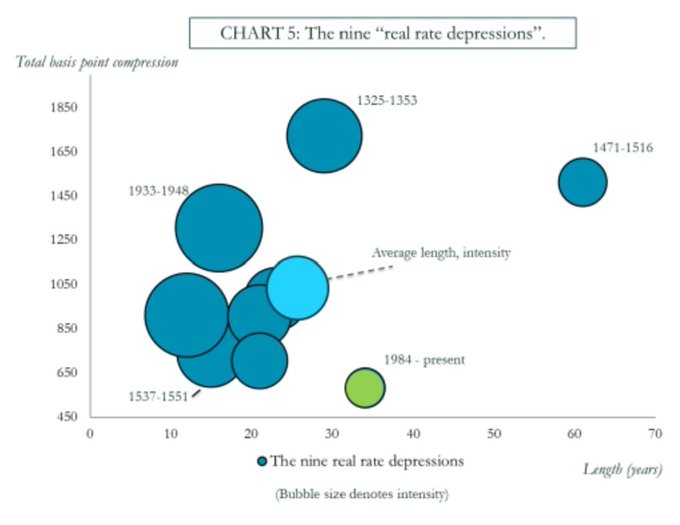

On the history of real rates (1/3)

Historically, many lengthy periods where real rates where depressed for a long time

Typically involved war or disease

1984-2021 the second longest on record

3

18

91

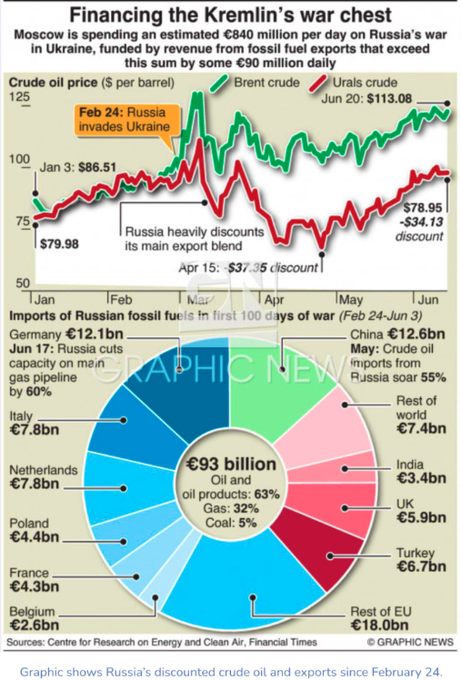

How will we explain to our children that Europe de-facto financed Putin's war?

14

20

91

Yesterday, equities sold off despite strong data and lower yields = good news in the price

Today, the NAAIM positioning survey shows a reading of 97 = near its historic max

Bond yields are pushing up

Equity downside risk now up materially, IMO. I've adjusted accordingly

6

4

89

🇺🇸 Consensus is now convinced that US bond yields can *only* go higher

Time to buy Treasuries $TLT (and time to cover equity shorts)

22

3

91

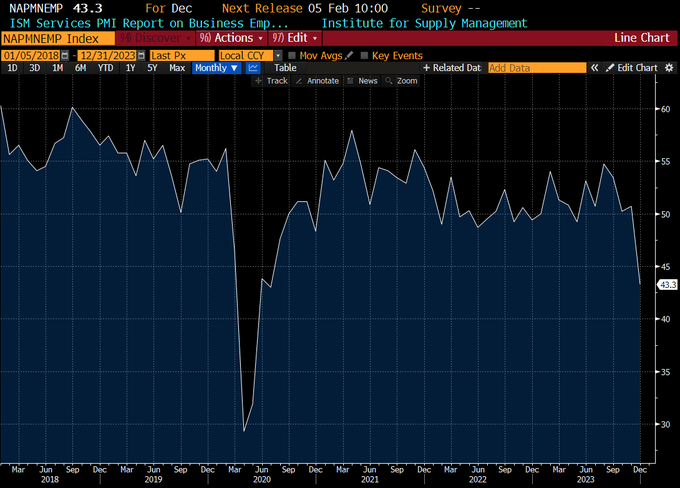

I wrote in my last post that I would buy the 2-Year on a bounce (in yield). I just did that

ISM Services employment component is falling off a cliff

Goods econ mislead everyone about direction of econ cycle in '22/'23, and think odds are it will again do so in '24

9

10

91

I just published a new post. In it:

- 3 critical questions for the path ahead

- 3 scenarios that follow from them

- Very near-term bearish again. Need to see the dust settle for view beyond

It is free, if you like it, please share it!

11

8

89