Loonie Doctor

@LoonieDoctor

Followers

1,454

Following

73

Media

75

Statuses

358

A Canadian physician blogger helping Canadian physicians and other high income professionals improve their financial health while not boring them to death.

Canada

Joined April 2018

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Leverkusen

• 421293 Tweets

#Comebacktome

• 267550 Tweets

RM IS COMING

• 209480 Tweets

メイドの日

• 85735 Tweets

Celtics

• 77211 Tweets

Luka

• 69445 Tweets

Maranhão

• 61388 Tweets

WIN CENTRAL FAMILY

• 54610 Tweets

#ดวงใจเทวพรหมSportsDay

• 47589 Tweets

Rangers

• 44119 Tweets

メイドさん

• 40145 Tweets

Cavs

• 37859 Tweets

भगवान परशुराम

• 37670 Tweets

Tatum

• 33394 Tweets

メイド服

• 31495 Tweets

ドラマ化

• 27797 Tweets

Safe Campaign

• 25535 Tweets

भगवान विष्णु

• 22702 Tweets

Canes

• 22600 Tweets

PRISCILLA

• 17931 Tweets

RTTT

• 13805 Tweets

#VileirosNaMansão

• 12652 Tweets

Pumas

• 12443 Tweets

Rex Murphy

• 12403 Tweets

Cruz Azul

• 12333 Tweets

Zavala

• 11690 Tweets

Aleska

• 10859 Tweets

I made an online tax table to show tax rates and integration for corporation vs personal. Adjustable for province and different tax brackets. Updated it for the new capital gains changes. Also has integration for other active and passive income types. Will link to the beta below.

4

2

40

This week on The Money Scope,

@benjaminwfelix

& I discussed some practical challenges with portfolio design & execution. Knowing all of your risks, overconfidence, DCA vs lump sums, and rebalancing when it hurts real good. And more big decisions with real money. Link in comments

3

5

22

Corporate class funds are very tax efficient. Until they aren’t. Last week’s post showed how much open water Horizons corp class ETFs have. This week I unpack what hitting a tax berg could look like. Peak beneath the surface.

3

2

20

Strategies to Withdraw Big Money From Your Corporation Tax Efficiently

3

1

20

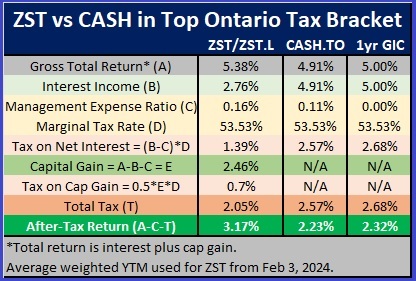

People chase tiny interest rate differences for saving. However, choosing something with a small amount of risk or more tax efficiency could make a bigger difference. I compare ZST, CASH, and a GIC in a personal and corp account. Link in comments.

5

3

20

Markets are not perfectly efficient and that is touted as an opportunity to make excess profits. Learn why trying to beat it still fails & why people try anyway. Use that to win by not losing. Link in comments.

2

1

20

@AaronHectorCFP

In 2017, I had 53.5% tax, 5% fee clawback & 7% tithe to fund our university. A terrible return on time, but I was doing important work. The PM & Wynne said we should "do a little more". People cheered. My family & I looked at what we were sacrificing in light of that. I cut back.

2

1

19

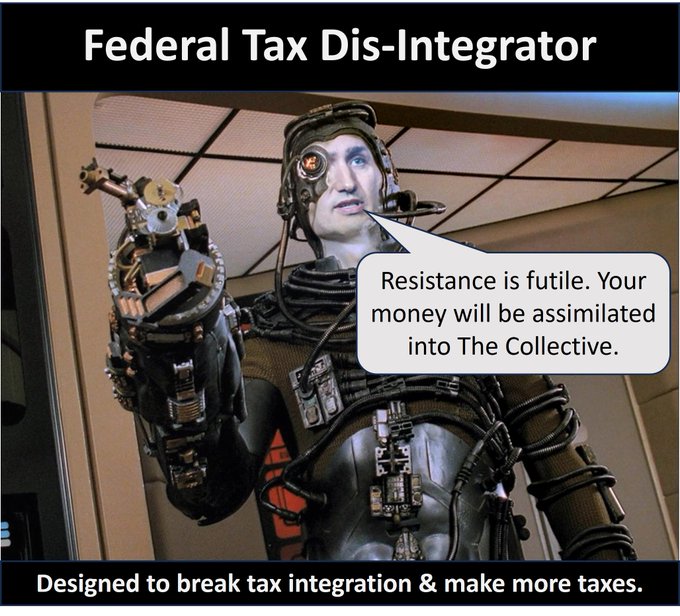

Resistance is not futile. Learn about capital gains tax changes. Don't be an impulsive human. Digest it and make a deliberate tax plan. A link will be in the comments.

2

1

19

Calculator comparing personal capital gains. Sell before June 25th vs not? Impact on after-tax portfolio value and future drawdown income. I put CCB in just for

@AravindSitham

. More planning tools coming from my friends at

@PWLCapital

too. We're sharing notes. Link in comments.

2

3

20

This week on The Money Scope,

@benjaminwfelix

and I covered the rules, benefits, and common mistakes using registered accounts (RESP, RDSP, FHSA, TFSA, RRSP). There is audio, video, and an annotated transcript. A comprehensive guide to come back to. Linked in the comments.

1

2

17

Incorporated & wondering what to do with the June 25th capital gains change? I made a simulator to test three strategies. Desktop or Tablet. Hopefully gets you thinking about strategies to help your clients or to be an educated client. For entertainment purposes only. Link below.

1

1

16

Last week

@benjaminwfelix

& I detailed how to pay an approximately optimal salary & dividend mix from a CCPC on The Money Scope. I spent the weekend updating my online tool. Enter income, spending, investing. Get a draft plan to discuss with your advisor. Ep 13 & tool links below

2

2

19

@AaronHectorCFP

It is actually a genius political move. They’ll pull forward capital gains taxes to get a bump this year and make the budget look better going into the election.

1

1

16

Ep 6 Cases:

@benjaminwfelix

& I explore some common ways people miss out on investment returns. Fear of recessions or impending pullbacks. Fear of taxes to switch to a more effective portfolio. Chasing hot tips (even in your field) or managers. I'll put a link in the comments.

3

2

16

@benjaminwfelix

and I unpack cases on The Money Scope Podcast about taxable investing.

*Dividends

*Discount vs Premium Bonds

*Criteria to use leverage

*The nuts and bolts of tracking leveraged investing

*Attribution rules with home equity

Link to the episode page in comment

3

1

15

@JarrettHolmesFP

@benjaminwfelix

and I have pooled our resources to really unpack this over several upcoming episodes of The Money Scope Podcast. We've made new models to examine nuances too. It is such a common problem. A long-term planning & compensation strategy avoids the "need" for products.

3

1

14

I had the pleasure of chatting with

@Benjaminwfelix

and

@CameronPassmore

on their

@RationalRemind

podcast. Great hosts and wow we covered a lot of ground!

Episode 73: Finance for Physicians: Personal Finance for High Income Earners with the Loonie Doctor

0

1

2

0

3

13

Narrators get paid to tell great stories. Unfortunately, your investment return doesn't register on that metric. This week, I will share two stories that listening to will hopefully save you money. The second one cost me thousands. Link in the comments.

2

1

12

This past week on The Money Scope

@benjaminwfelix

and I discuss how business owners get paid via taxable benefits, salary, and dividends. Learn more to make sure that you don't leave money on the table, but don't stick out like a thumb for the CRA buzzsaw. Link in the comments.

6

2

11

Scams can snare people from any level of wealth or financial sophistication. These Tales of Charlatans & Chagrin illustrate some red flags to identify and avoid Ponzi & other schemes.

-Charlie & The Charger Factory

-The Emperor Has No Crypto

Link in the Comments

2

2

12

Price matters and contains important information. Understand how assets like stocks or bonds are priced to get paid, not played, when you invest. Recognize hidden risks or bad instincts. A link in comments

3

2

12

Horizons’ corporate class ETFs are very tax efficient in a personal or corporate investing account. However there is also embedded tax management risk. Is it smooth sailing ahead or is a tax-berg looming?

3

5

12

Corporation owners face some common investing dilemmas. This week,

@benjaminwfelix

and I discuss a few on The Money Scope Podcast.

Meshing a Corp, TFSA, & RRSP

Will your corp suffer from bloat?

Attraction & troubles of capital gains and dividend-focused corp investing

Link below

2

2

11

People love stories. Unfortunately, there are some expensive story tellers out there. They cost investors billions. I will fight fire with fire and tell some stories to help you avoid that. Here is a picture I made as a teaser. More tall tales to come.

3

0

11

You want to get paid for taking investment risk. Unfortunately, there are also uncompensated risks that can get in the way. Win by not losing - diversification helps you to do that in multiple ways. A deep understanding helps you to resist the pressure to deviate. Link below.

1

1

11

The countdown to the release of The Money Scope Podcast by

@benjaminwfelix

and me is on. The prep for the scope is done. It will be much more than a podcast. Enjoy the trailer and memes. If you are >50, talk to your doctor about colon cancer screening.

0

2

11

This past year, I focused on the collaborating & connecting plank of The Loonie Doctor mission. Find out why, how, and what the means. Spoiler: there is a trailer for a major upcoming project buried in there.

0

2

11

In this series of posts, I will share our family’s wealth journey. How we think about, spend, and manage our money. How that has changed over time. I will start in the early years when we built our financial foundation.

1

0

11

@BoomerandEcho

@mverbora

My concern is actually more about the rhetoric than the numbers. When this gets added with a "do more of your share", then piled on by sarcasm and jealousy from the public we serve. It is demoralizing and disproportionately contributes to burnout. It is actually precarious.

1

0

9

@benjaminwfelix

Homeownership comes with the freedom to renovate it how you like and not worry about moving. Renting comes with the freedom to movewithout worrying and not bother with renovation and maintenance.

When we were young, renting was freedom. Undecided for retirement: roots vs wings?

1

0

10

In follow-up to our episode on Debt, Saving, & Investing, this week

@benjaminwfelix

and I walk through a couple of common debt scenarios for professionals. Case 1: Early career debt. Case 2: Keep it in the Corp vs pay the personal debt.

0

2

10

Working on a blog post for next week, but thought this was cool. ZST is dominated by discount bonds currently. For taking some small risks, the after-tax return could be much higher than alternatives to parking cash for a few months.

4

1

10

Of all the corp class ETFs, HXDM has the most potential for an advantage in a corporate account. It could be huge in some cases. Still, that must be considered against management risks. Both in the fund and complexity compared to an asset allocation ETF.

0

3

10

This past week on The Money Scope

@benjaminwfelix

and I discussed using debt like a time machine, accounts/products for saving, and transitioning to invest.

2

2

10

This week's Money Scope episode is even more relevant given the capital gains changes. An optimal salary & dividend mix not only spreads your risk out to other accounts like an RRSP and TFSA. It also does that more tax efficiently for current and future buying power. Link below.

1

2

9

If you need to hold bonds in a personal or corp account as part of your portfolio. Then, using a discount bond ETF instead of a regular one could serve the same role for risk management, but more tax efficiently. One of those rare free lunches in investing. Link in comments.

3

0

9

Join

@benjaminwfelix

and me for Episode 2 of The Money Scope. Learn about common money traps and how to recognize, avoid, or extract yourself.

0

2

9

Here is a link to the tool. Have done some cross-checks with other, but report any bugs for me to squish please.

1

0

9

@benjaminwfelix

& I explain how stocks, bonds, and funds are priced. Even good products can be used in bad strategies. Understand key concepts to spot the differences and develop the intuition to avoid the allure of costly financial bullshit.

0

0

9

Some products rely heavily on the story used to sell them. Learn more about The Legend of Permanent Life & Pandora's Private Equity Box. Otherwise, you may buy what is ultimately an expensive story. Or if you buy the product, at least know the full story. Link is in comments.

2

0

9

Wealth is relative, but as your family shifts to a meaningfully different level of wealth, unanticipated issues come up. How you respond affects your success and that of your offspring. Will you be a denier, ditcher, or adapter?

0

1

9

Here is a link to the dynamic tax integration tables

0

0

8

I will be there to help open the TSX on Feb 8th as part of DIY ETF Investor Day 2024. You can join me for what should be a unique experience for DIY investors. And cheer me on too. There will be an ETF rumble afterwards.

0

0

8

I have been hearing a lot of this since about January. I talk about this and more expensive investor self-talk this coming Friday on The Loonie Doctor.

0

0

8

@TheTaxHeroes

"In some cases, the courts have held the appropriate taxable benefit to be equal to a reasonable return on the amount of funds invested in the property. This might be considerably higher than the market rental value"

2

1

9

@t_wooly

@AravindSitham

@PWLCapital

As long as you are investing enough in the corp (on top of using RRSP/TFSA), I think that corporations will still be a valuable account for long-term. As before, it requires a life-time plan - including an exit strategy (which is often underappreciated by rules of thumb).

1

0

7

@MarkMcGrathCFP

Have most of my calculators with an adjustable future inclusion rate. Figured it was only a matter of time..

1

0

8

@BoomerandEcho

Nope. Instead they can plan using their predictable income stream and lack of business overhead subject to inflation. Knowing that their retirement will be secure. Corporations smooth income and expenses over years and a lifetime. Tax integration helps make it fair. But different

0

0

8

Part 2 of My Wealth Journey: The Wonder Years. This post details the finances of my first decade of practice. Investing in my business. Finding out I wasn't special at investing. Spending without guardrails. The hedonic treadmill is set to plaid speed.

0

1

8

In a private corp (CCPC), interest is not very tax efficient & cap gains are. Passive income can be extremely inefficient if the tax werewolf shows up. Is the corp class bond ETF HBB a silver bullet or just expensive ammo?

0

1

7

This week I model HXCN (corp class ETF) vs a Conventional ETF invested via a CCPC (a private corporation). Sometimes HXCN is like a silver bullet for the tax werewolf. Or you may shoot yourself in the foot with it.

0

2

7

Discount bond ETFs are an easy way to get the risk reduction of bonds in your portfolio. But a more tax-efficient mix of capital gains instead of mostly interest. There are also many discount bonds currently in short-term bond ETFs to park cash short-term. Link to follow.

1

0

7

@TheTaxHeroes

@JarrettHolmesFP

@benjaminwfelix

Me too! I made a tax integration table (adjustable by province) and showing all the tax brackets to model this out. And tax integration for other corp passive and active income. It is wild.

0

0

7

There are hidden costs to investing. One of them is the bid-ask spread. If it is an illiquid investment, that spread is larger. How does that apply to ETFs? Are lower-volume ETFs liquid or are you getting secretly hosed? Use best practices to minimize

0

1

7

@CameronPassmore

@PWLCapital

and

@benjaminwfelix

have been great partners in crime on this front. Having fun and it will be impactful.

0

2

6

@BoomerandEcho

@mverbora

We are expected to sacrifice ourselves and our families to do whatever is required to meet the public need. It is why labor laws don't protect us. But, the other side of that social contract is some respect and reward. The rhetoric undermines that side of the relationship.

1

0

7

Here is a link to the post.

1

1

6

@BoomerandEcho

I agree. People need to know some basics to identify good advisors and advice. With that base, they could probably DIY ETF invest or pick an advisor that adds value for cost. The teaching/coaching to get people there requires patience/persistence for sure.

1

0

6

@AravindSitham

It does feel good.

@benjaminwfelix

and I did a segment on escaping a group plan if you were taken in. First time my wife got excited about our pod because we have friends who got sucked in.

2

1

6

@BoomerandEcho

@mverbora

This is an apples to oranges comparison. Adjust for hours worked (quantity and convenience). Opportunity cost - money and the time to be top of your class to get in and progress. Not easy to compare. I don’t teacher bash. Why do people doctor-bash (except when they need one)?

1

0

6

@AaronHectorCFP

@STANDUP_Today

All the people who have relatively low to average incomes, but have had a cottage in the family for years are about to find out what AMT means when they sell. With a low income normally, they may not recoup the pre-paid taxes before the credits expire in 7 yrs.

0

0

6

@MarkMcGrathCFP

This is how I used to mow my lawn. Three mowers and ~70HP in fighter-jet formation. No one could reach me and I mowed over my pager twice in five years.

2

0

6

Horizons' corp class ETF HXEM covers emerging markets for diversification into the fringes of public markets. Used in a CCPC, it offers tax savings. But also some compromises and risks. Quantify that to consider whether there be tax savings. Or serpents.

0

2

6

@TheTaxHeroes

I have my lower-income spouse do ours. It is functionally income-splitting for us and keeps some money in the family.

1

0

6

@j_stock_

@MarkMcGrathCFP

@jonrgibson

@JamieGolombek

@benjaminwfelix

We are actually looking at another RV in the spring. The other option to consider before pillaging a TFSA is if you have a personal taxable account with some holdings that you can sell with minimal cap gains or gains that can be offset by losses. That is what we are planning.

1

0

5

@benjaminwfelix

Thanks Ben! It has been super-interesting unpacking and thinking about this issue together. More to come.

1

0

5

@MarkMcGrathCFP

@j_stock_

@GooseStoned

Exactly why capital gains and corporations are the perfect political target.

0

1

5

@MarkMcGrathCFP

They have special hitches you can buy to offset them and are made to be towed behind a tractor or ATV. I had to weld some reinforcements to the main mower hitch to handle the weight though.

1

0

5

@BoomerandEcho

@mverbora

I have perspective. My objection is the politics. It is sold as affecting 0.01% of Canadians with an average income of 1.2MM. The average person says "Their rich - pay more". The average doctors says "That's not me."

2

0

5

@benjaminwfelix

Thanks Ben. Was really interesting to work through this. I appreciated your insights.

1

0

4

@BoomerandEcho

@mverbora

Not sure that is completely true. We've had subinflationary fee increases while our costs have increased at much faster rates. Taxes are just one part. It needs a wider perspective - hard for most people not in it to truly understand.

0

0

5

@AravindSitham

@j_stock_

@tfedds

Totally. That look is familiar. They know when I go into what they call "mad professor mode". Happened Tuesday. I get a glazed look as Excel models run through my head.

1

0

5

@MarkMcGrathCFP

@j_stock_

@jonrgibson

@JamieGolombek

@benjaminwfelix

Definitely. We don't know that tax rates for even the same income level won't be higher in the future. Corp or personal. Having some after-tax investments is a hedge against that. For the TFSA in particular it is a small amount, but still a hedge against future tax changes.

1

0

4

@MarkMcGrathCFP

Totally. Narrators get paid to tell stories. Exciting or scary stories pay extra.

1

0

5

@BoomerandEcho

@mverbora

The post comparing teachers and doctors. I don't begrudge anyone their pension. Whatever the contribution rate, it is part of their compensation. A pension just makes it mandatory and pools risks. Younger members should talk to their union if they are paying extra for the benefit

1

0

5

@MarkMcGrathCFP

@sheldon6600

Another way around the issue of not selling stuff and not spending is ZGRO.T It is an 80:20 asset allocation ETF that distributes 6%/yr from the income and automatically selling as needed to decumulate.

1

0

5

Risk, reward, discounts, expectations, and other factors

0

0

4

@MarkMcGrathCFP

This is an important issue. People are reluctant to take money out and pay tax. So they pay more when dead. Spend it or give it while alive as you get older if there will obvious surpluses.

1

0

4

0

0

4

Specialization and diversification are opposing strategies. Specializing may improve success sometimes. If you pay attention to the aspects that give specialists an advantage. Knowing about that also helps you understand when to diversify- not specialize

0

0

4

As you move to meaningfully higher levels of wealth, you must identify and retain some core values and skills while integrating new ones. Plus, pass them on to the next generation. Learn more about that and some strategies to help.

0

0

4

@AaronHectorCFP

@JarrettHolmesFP

This is how my wife and I set ourselves up. Gives us lots of options, easy to track attribution, no real extra hassle.

0

0

4

@LooniesAndSense

@BoomerandEcho

When drug companies name drugs, they like to use Z's and X's because they are perceived as more powerful. Guess BMO ETFs beat the to the Z and Blackrock got the X. At least they have an X in the name now.

1

0

4

@CameronPassmore

@benjaminwfelix

@RationalRemind

Thanks for hosting me. It was a pleasure and privilege.

0

2

4

@BoomerandEcho

@MarkMcGrathCFP

@benjaminwfelix

That would be a great slide for a talk I did last week. I love it!

0

0

4

Here is a link to Money Scope Ep 13 page.

1

0

5

Here is a link to the simulator and some notes about it. For entertainment and to stimulate planning and discussion only.

1

0

4

Here is a link to the blog post. Please share with your incorporated friends, business owners, and planners who help them.

0

0

4

@AravindSitham

@JarrettHolmesFP

@benjaminwfelix

I keep going back to them - and I helped write them. They are indexed. So, when someone asks you a question you can give them a link straight to that section of the transcript. With footnotes embedded too.

0

0

3

@benjaminwfelix

@JarrettHolmesFP

Totally! There was smoke coming from my brain and my computer trying to process the Excel sheets.

2

0

4

@tylermeredith

Giving up prime years of your life studying to hope for a limited spot. Accruing debt and delaying income. Yeah. Totally risk-free.

Salary, benefits, and workplace protection that employees get would be great. Governments know it is cheaper to not have that accountability to us.

0

0

4

Here is a link to the article.

0

0

4

Here is Ep 7's Case Conference Episode.

0

0

4

Invest For Your Long-Term Security

2

3

4

@CameronPassmore

@benjaminwfelix

Yeah. My mind is blown too. Even my teenagers think I'm cool now. 🤯 At least until my next Dad-joke anyway.

0

0

4