Martin Castellano

@mcastellano44

Followers

8,779

Following

1,023

Media

417

Statuses

725

Head of Latam Research @IIF . Opinions are my own.

Washington, DC

Joined September 2010

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

México

• 631713 Tweets

Uruguay

• 64463 Tweets

Yuta

• 57724 Tweets

#jjk262

• 49802 Tweets

#ช้อปถูกที่Lazada66xZNN

• 47499 Tweets

JULIANA AL 9009

• 34292 Tweets

Asian Value

• 33233 Tweets

VIRGINIA AL 9009

• 28447 Tweets

Gege

• 28350 Tweets

悪魔の日

• 25116 Tweets

Hannity

• 23365 Tweets

Yinlin

• 22891 Tweets

Jiaoqiu

• 21750 Tweets

Rika

• 20314 Tweets

ショウキュウ

• 18660 Tweets

Bielsa

• 15677 Tweets

インリン

• 15630 Tweets

chivas

• 14757 Tweets

悪魔の数字

• 12479 Tweets

Ben Carson

• 10471 Tweets

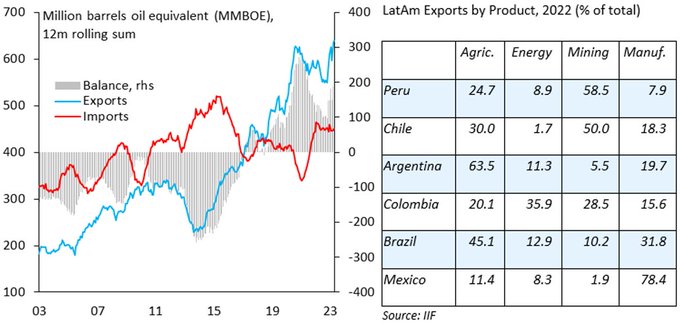

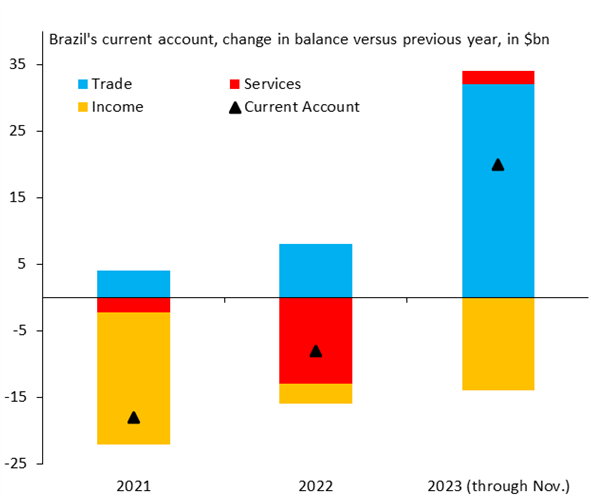

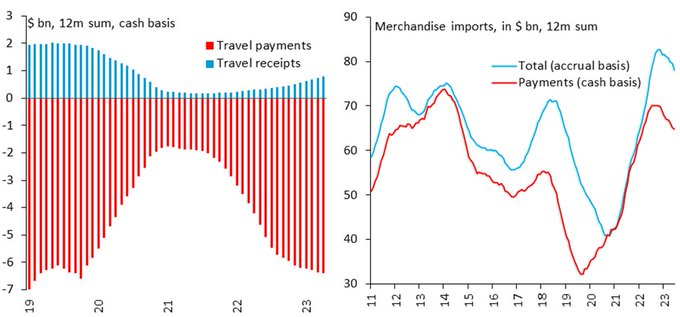

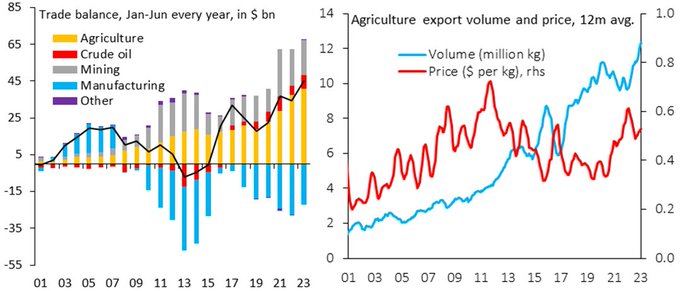

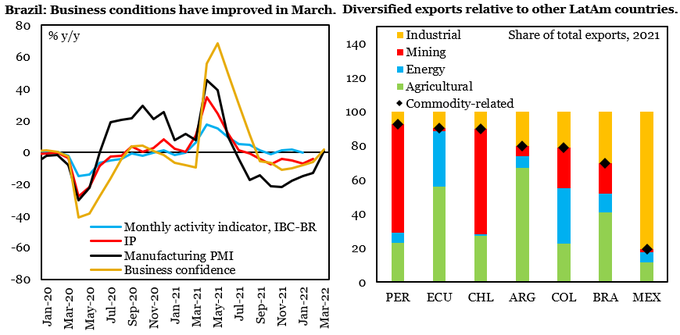

Brazil's record-high trade surplus in May is not all about agricultural exports. The country's export base is more diversified than most major LatAm economies. Surging energy, mining, and manufacturing shipments will help bring the current account deficit below 2% of GDP in 2023.

24

275

1K

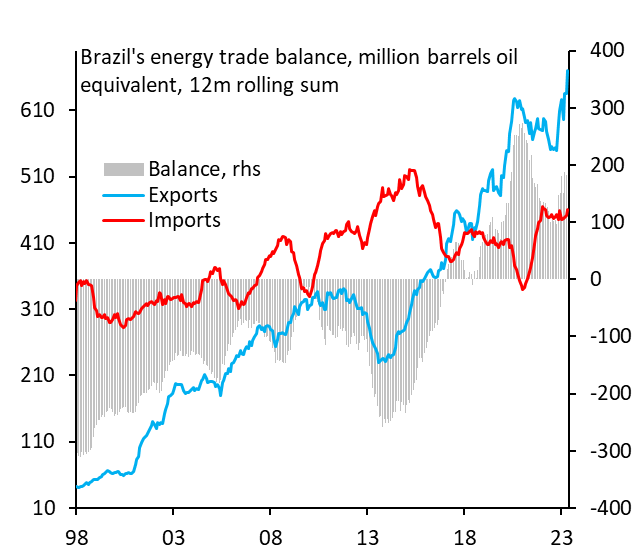

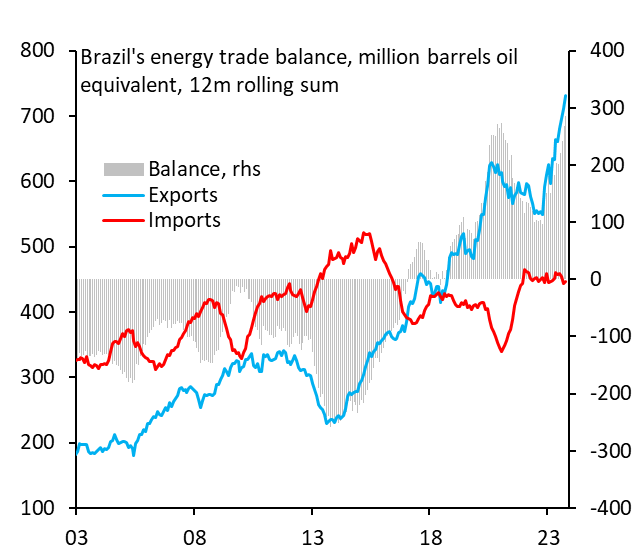

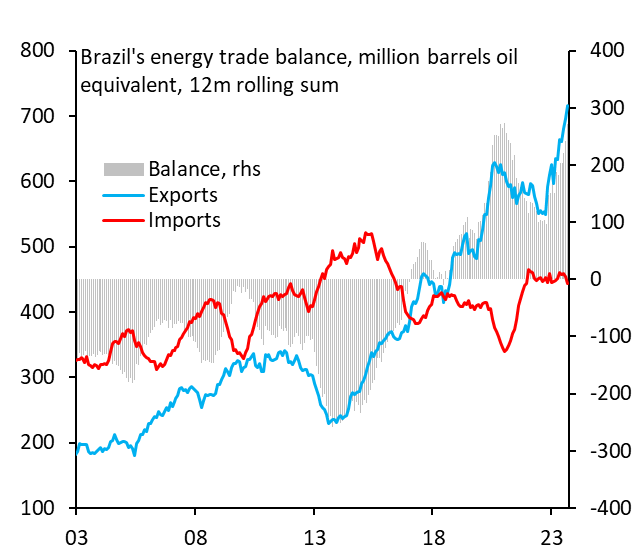

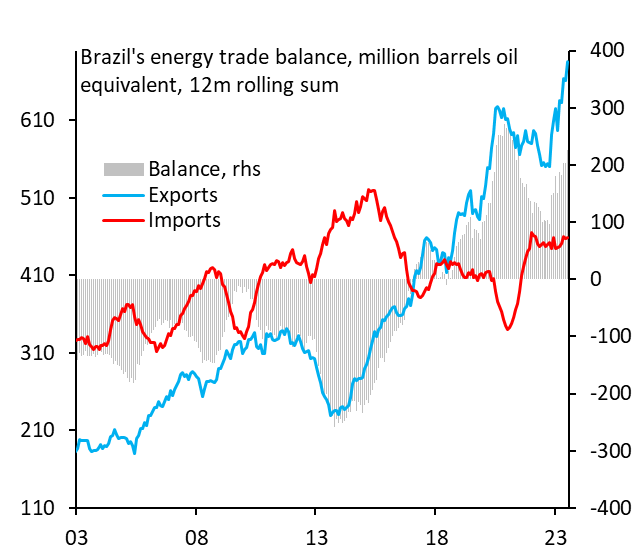

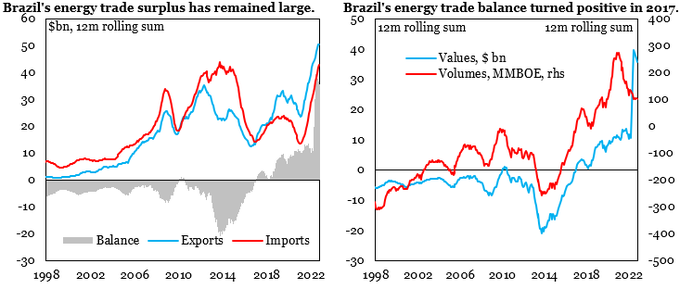

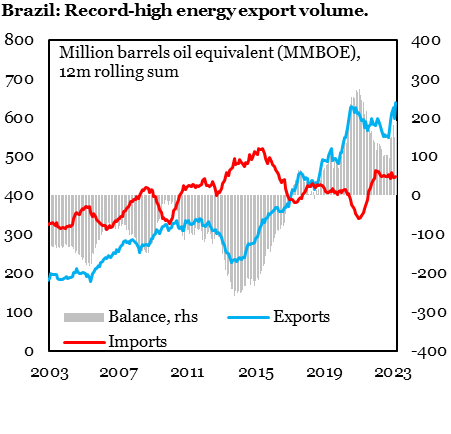

Oil has become Brazil's most relevant export driver after soybean, surpassing iron ore. Regaining net energy exporter status has led to steady hard currency inflows since 2018. The recent energy export volume surge makes external accounts even more resilient, supporting the BRL.

16

199

910

Brazil has become a key player in the global energy market, as reflected by recent talks to join OPEC. The country's energy trade volume surplus reached a new high in Oct, topping the end-2020 peak. The sector will help ease the current account deficit to about 1% of GDP in 2023.

10

109

633

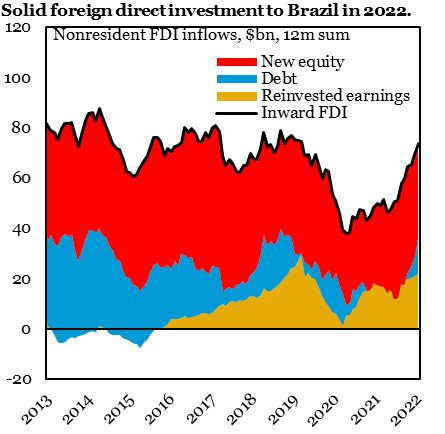

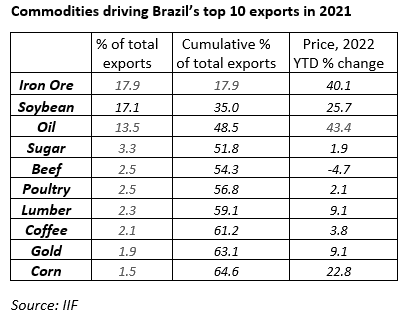

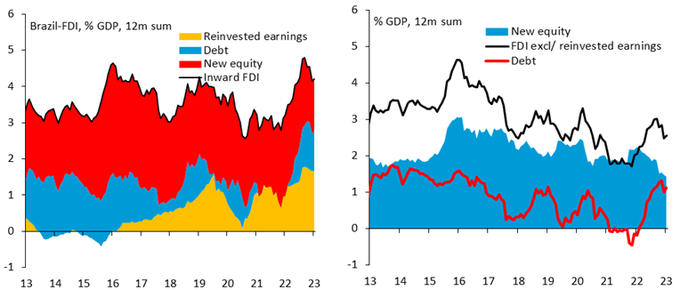

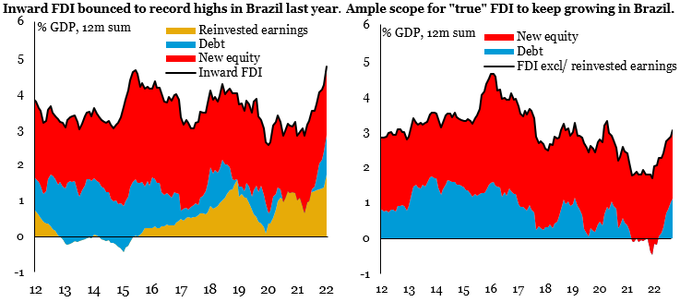

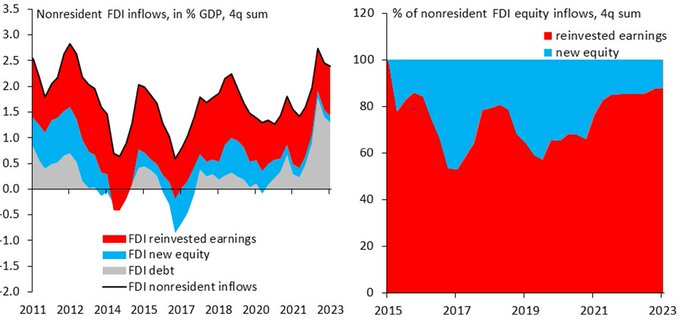

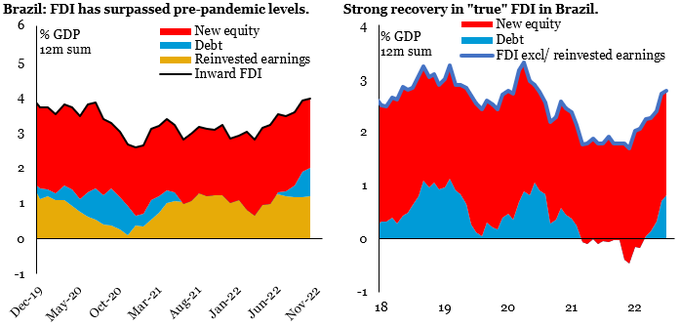

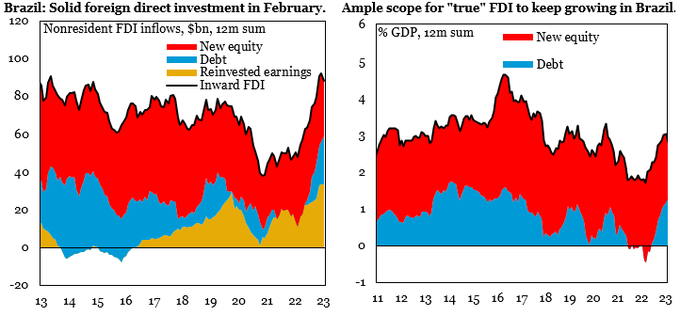

In 2022, foreign direct investment to Brazil will likely be the highest in the last decade, doubling 2021 inflows. Is it just commodities? The primary sector has, so far, received only 6% of the new equity this year. The core goes to manufacturing and services, supporting growth.

11

73

375

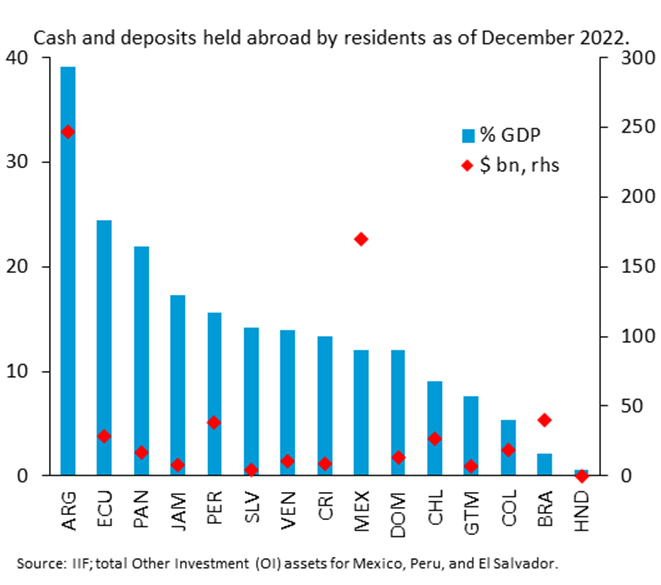

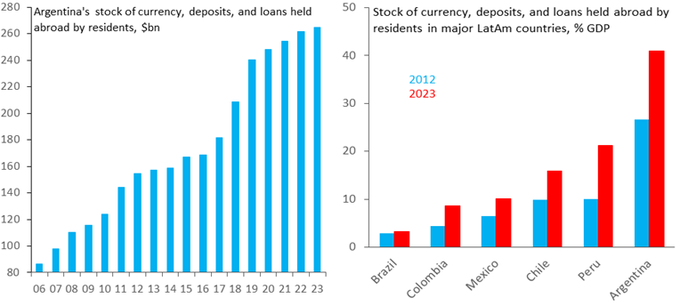

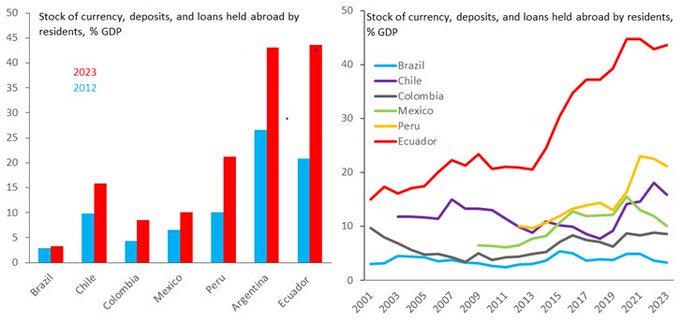

Takeaways from IIP data on money held abroad by locals across LatAm:

▪️Argentinians, by far, hold the most cash abroad.

▪️Brazilians' holdings are among the lowest.

▪️Mexicans' holdings remain average.

▪️Chileans and Colombians have doubled their positions abroad since 2019.

11

115

373

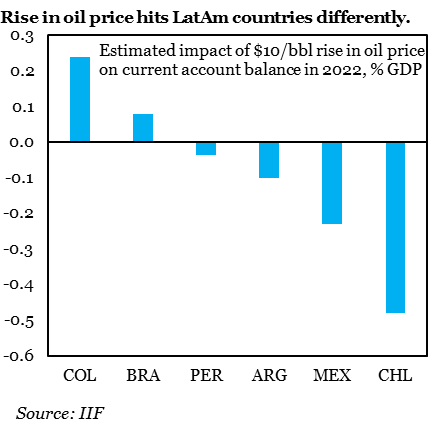

What is the impact of rising energy prices on external accounts in major LatAm countries?

(+) Colombia→ biggest winner.

(+) Brazil→ moderate gains.

(-) Peru→ mild losses.

(-) Mexico & Argentina→ net energy importers since long ago.

(-) Chile → largest adverse effect.

9

125

348

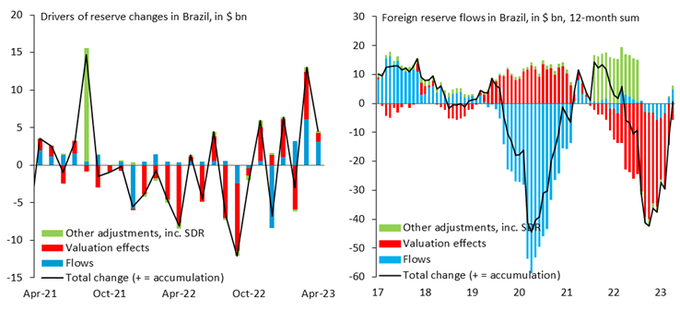

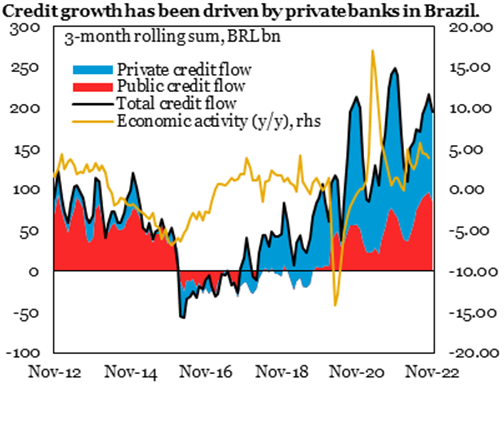

Brazilians have pulled much less money out of the country in 2023 than last year. Smaller resident capital outflows, a big trade surplus, and valuation gains have boosted foreign reserves so far this year. Strong external accounts support our above-consensus 2023 growth forecast.

6

76

314

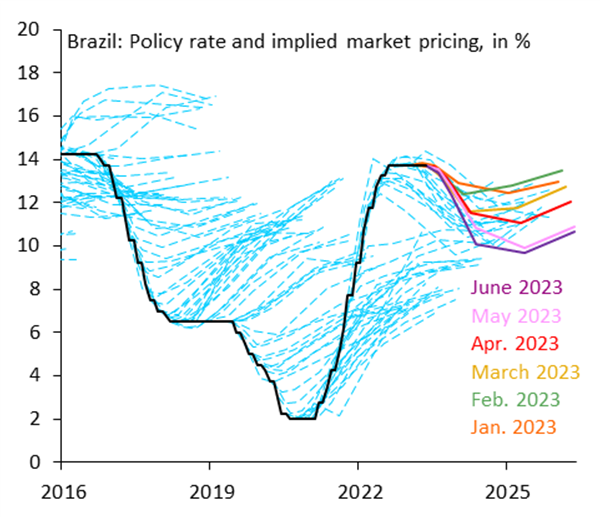

In Brazil, the steady downward shift in the curve amid improved disinflation prospects will prompt a less hawkish monetary policy stance in June. We expect the language shift to be moderate but strong enough to open the door for a rate cut in August, in line with market pricing.

11

52

320

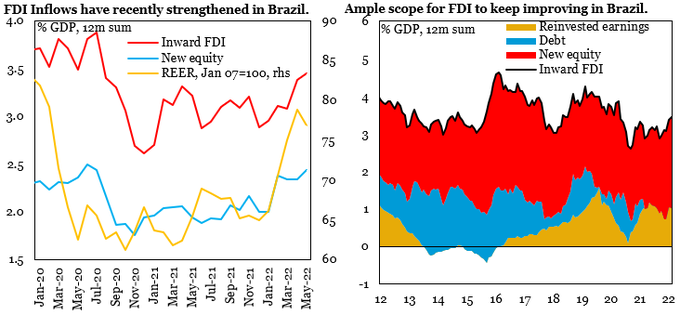

In Brazil, foreign direct investment (FDI) has strengthened this year after a protracted recovery from the pandemic. Improved growth prospects and robust new direct equity inflows suggest FDI will keep outperforming in the near term amid ample scope for further gains.

6

51

282

Brazil’s exports are highly dependent on three commodities: iron ore, soybean, and oil. These accounted for almost half of total exports last year. The broad-based commodity price surge due to the war widely improves the current account, which should further support the BRL.

3

67

275

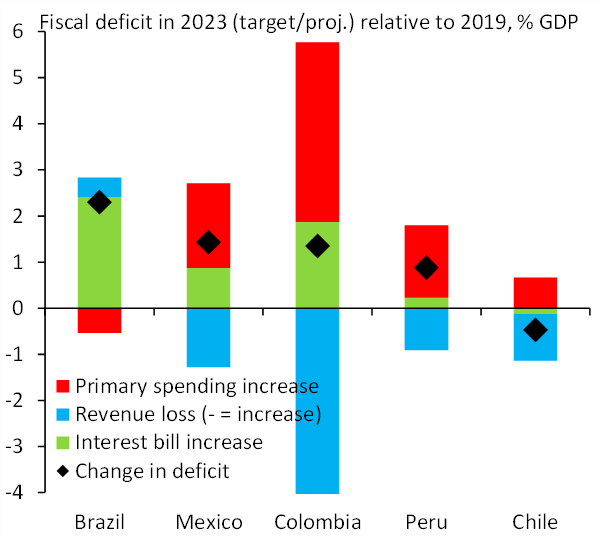

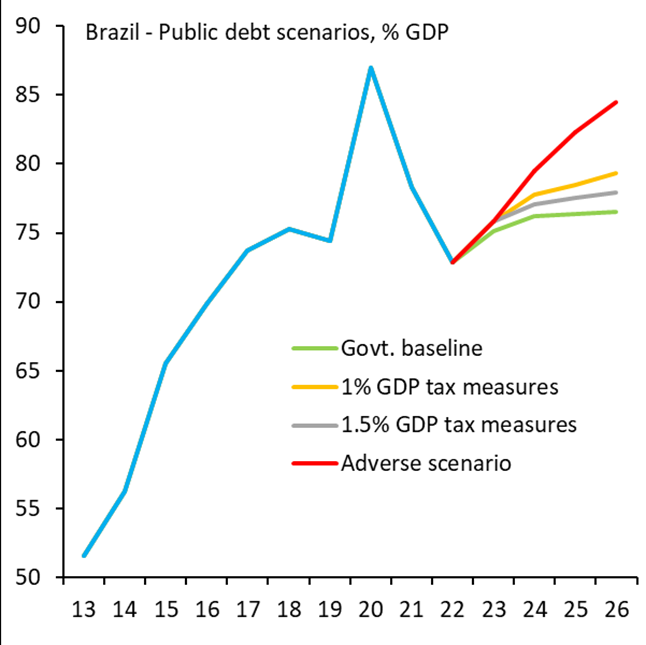

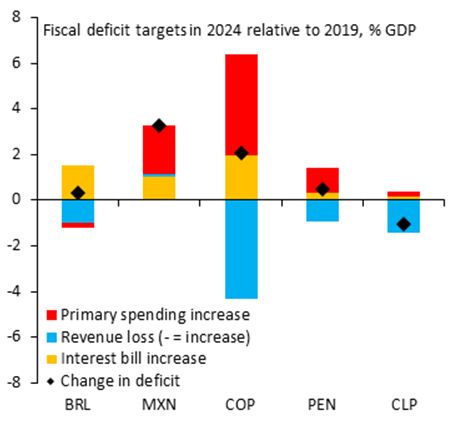

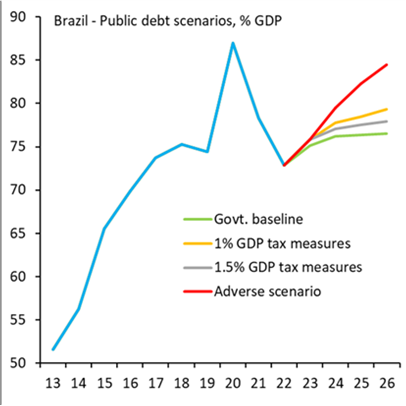

Brazil is often labeled "worst in class" when it comes to fiscal discipline. But primary spending will remain below pre-Covid levels in 2023. No other major LatAm country will achieve that. Despite its shortcomings, the new fiscal rule will help avoid the most adverse scenarios.

14

60

270

#ElSalvador

: Will President-elect

@nayibbukele

be able to deliver policy improvements, despite limited legislative support? Early signals in the transition, which include the will to make the relationship with the US a key priority, suggest reliance on pragmatism to work it out.

12

56

228

The Central Bank of Brazil stayed put today. The press release was more cautious than expected. Yet, hawkish language from previous statements ("…will not hesitate to resume the tightening cycle if the disinflationary process does not proceed as expected") was partially removed.

9

33

228

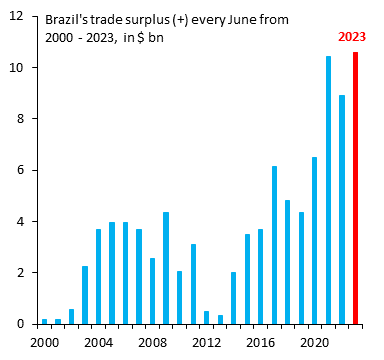

Subdued export prices have not prevented Brazil from posting a double-digit trade surplus in June. A trade surplus of over 3% of GDP in 2023 will be the largest since 2006. While soybean contributes the most, a diversified export base makes Brazil a key global commodity supplier.

Brazil's trade surplus in June 2023 reached a new all-time high. Important to note that this surplus isn't an outlier. The surplus in June 2021 was almost as big. Brazil is morphing into a trade and current account surplus country. The Real will be the anchor currency of LatAm...

107

499

3K

7

57

221

Record-high energy export volumes have bolstered Brazil's trade surplus in 2023, supporting the BRL. Oil has become the most relevant and dynamic export driver after soybean. A diversified export base will help bring the current account deficit down to about 1% of GDP this year.

3

38

218

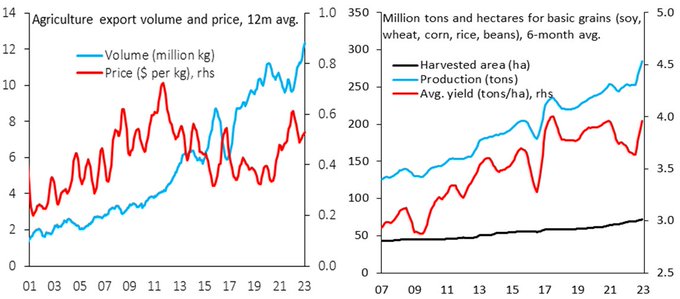

Brazil’s trade surplus remained solid in July at $9bn, supported by farming exports. The surplus is on track to exceed 3% of GDP in 2023, the highest since 2006. The country is reaping the benefits of the remarkable expansion of agricultural output that began in the early 1990s.

1

46

210

Tax reform approval in the lower house of Congress is positive for Brazil. Tax simplification should lift medium-term growth, key to avoiding the most adverse fiscal scenarios. Consensus on the elusive tax system overhaul signals political will to tackle structural shortcomings.

7

37

199

The new Argentine government adopted emergency measures (fiscal, devaluation, financing) on its first week in power to clear a minefield of imbalances and avoid a full-blown crisis. This is a first step to a subsequent stabilization program amid high implementation risk...1/7

4

52

180

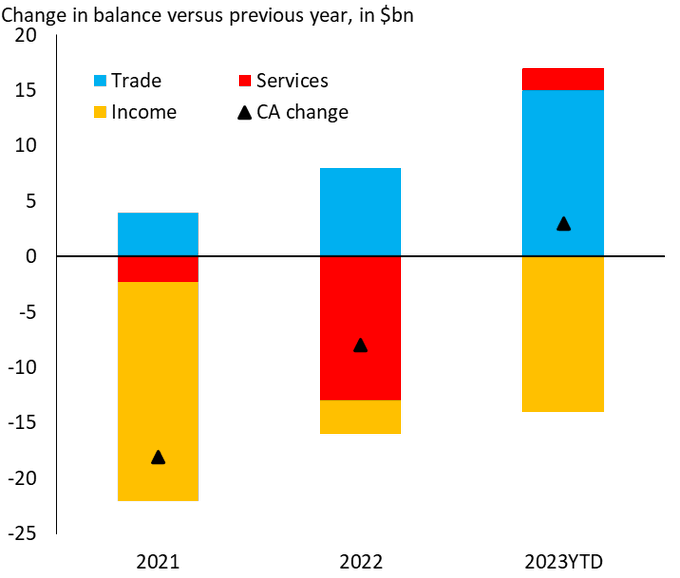

Brazil's massive trade surplus helped reduce the current account deficit to 1.6% of GDP in 2023. We estimate the farming transformation in the last decade has lifted the underlying trade surplus by 1.2 pp of GDP. Agriculture and energy will keep financing needs contained in 2024.

3

23

166

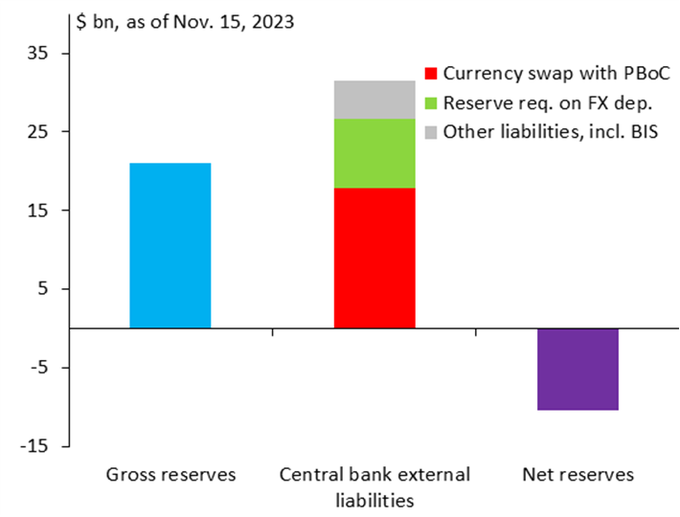

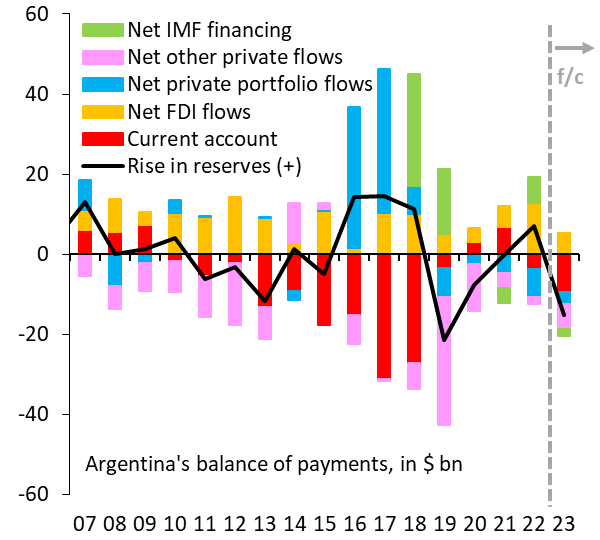

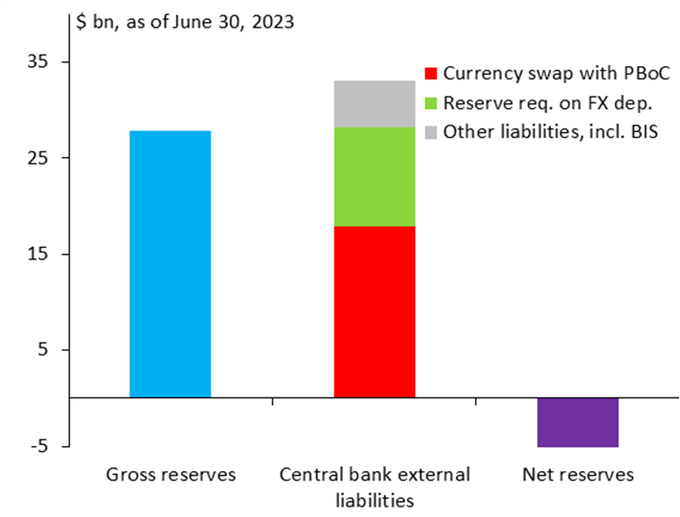

Argentina's net reserves are at -$10.4bn ahead of today's runoff. No matter what policy framework prevails in 2024, rebuilding buffers will require harsh FX/fiscal measures amid a credible plan to ease the inflationary impact. A good grain harvest won't improve things by itself.

4

53

157

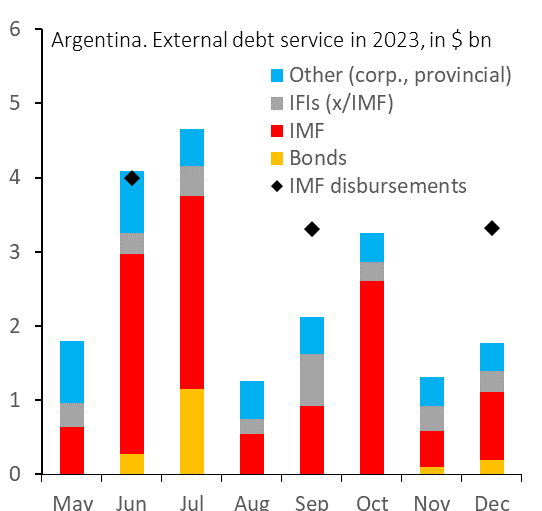

Argentina will pay $3.4bn to the IMF this week using borrowed money from several sources like the China currency swap. Amid negative net reserves and limited IMF disbursements, avoiding debt arrears will require a sharp import decline in the coming months. FX pressure will rise.

6

50

159

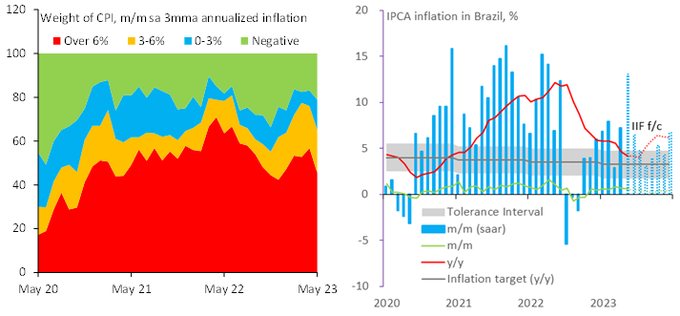

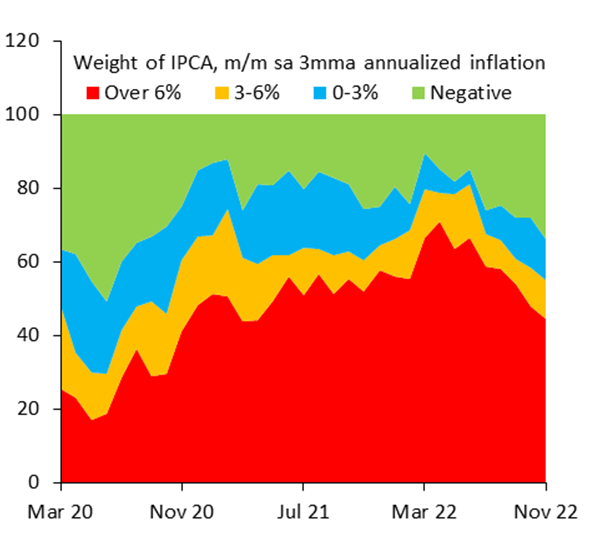

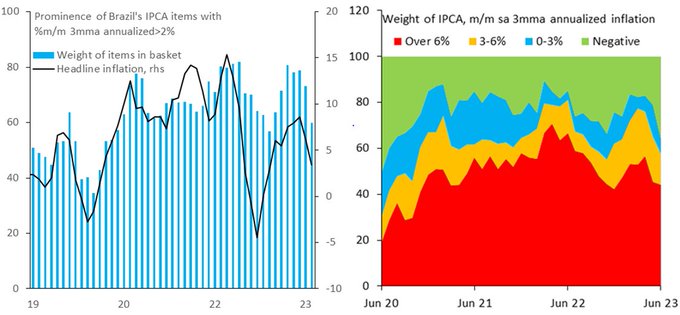

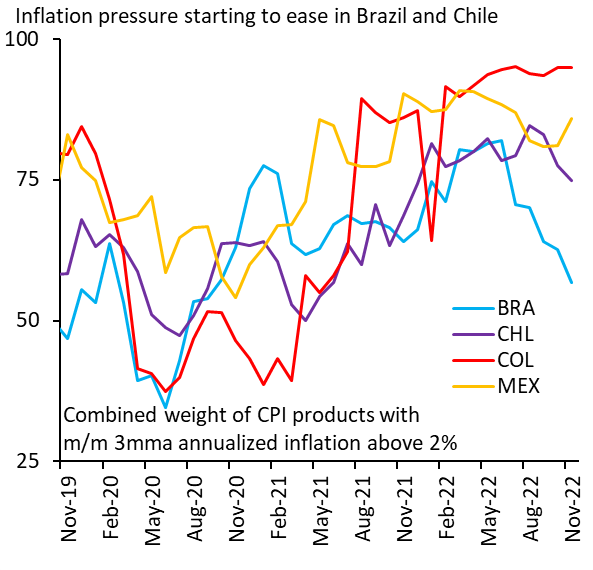

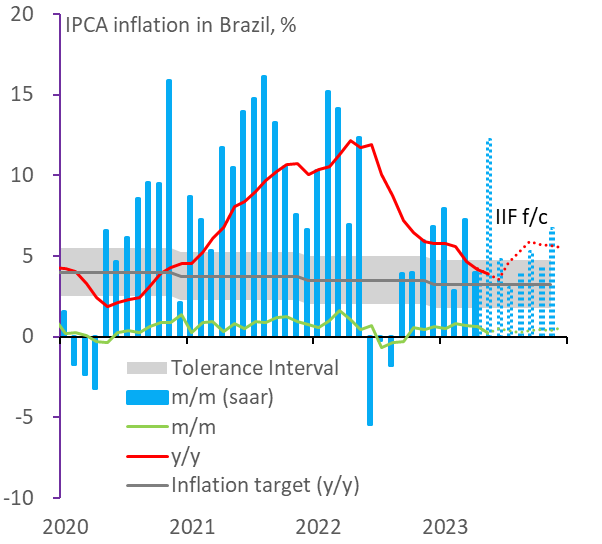

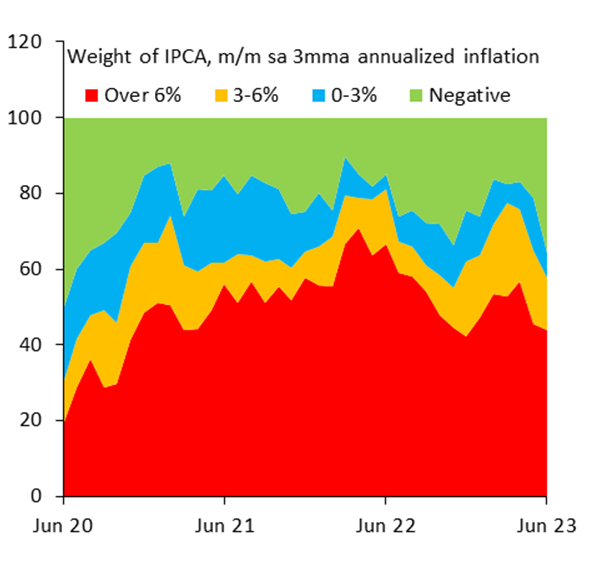

In Brazil, the combined weights of IPCA items with inflation>6% dropped to 44% in Nov., down to the end-2020 level after peaking at 71% in Apr. 2022. Headline and core inflation dynamics suggest fiscal risk could be the only thing preventing fast monetary policy easing in 2023...

11

23

148

Brazil’s external accounts remained solid in May. Inward foreign direct investment (FDI) totaled 4.2% of GDP, well above a current account (CA) deficit of 2.4%. “True” FDI (x/reinvested earnings) was also larger than the CA deficit, reflecting both strength and upside potential.

2

26

144

Our Brazil inflation generalization trackers show pressure has declined sharply in recent months, allowing for the beginning of monetary policy easing. While markets are pricing in 41bps in cuts, we think the central bank will rightly go for a prudent 25bps move this week.

3

17

143

Argentina's next administration, lacking dollars, will be unable to implement full dollarization immediately. But the regime could be put in place later on. What would it take to get the needed dollars? Long story short: a painful recession on top of higher inflation…1/5

6

40

141

Brazil’s inward FDI has gained traction in July and seems back on track to return to pre-pandemic levels. Nearly all inflows were equity with two out of three dollars being new money. Net FDI was also positive. There is still a long way to go, but latest figures are promising.

4

23

135

Brazil is not “worst in class” when it comes to fiscal discipline. But public finances deteriorated big last year. While meeting the 2024 zero primary deficit target looks tough, it is worth the effort. It would boost confidence and help monetary policy easing, lifting growth.

7

18

137

Brazil's new fiscal rule gained legislative approval yesterday, which is good news. Despite its shortcomings, the framework helps avoid the most adverse scenarios. But higher tax revenue is required to make it work. We think 1-1.5% of GDP in extra income in 2023-24 is doable.

4

26

120

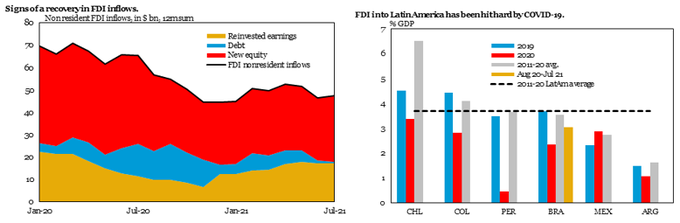

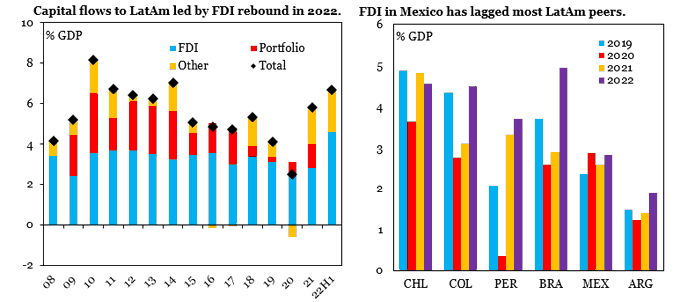

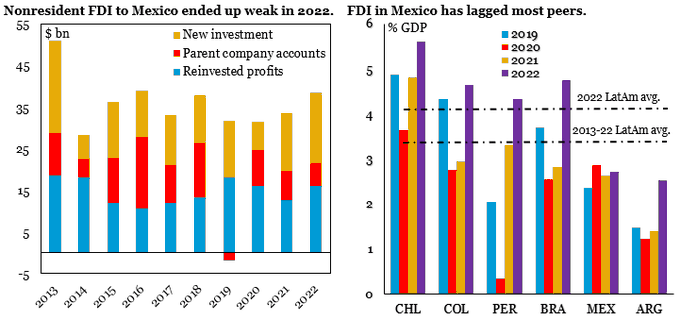

Foreign direct investment to LatAm countries is solid this year. But Mexico -best positioned to gain from global geopolitics and nearshoring- remains far from its potential. Getting the LatAm avg. in % of GDP would mean $52bn for Mexico in 2022, much more than we will likely see.

3

41

110

We put Argentina's external financing gap at $15bn this year, relying on conservative assumptions. The gap is close to the annual shortfall we estimated under the 2018 IMF program. Policy adjustments and IMF refinancing are urgently needed to help stabilize expectations...1/2

3

37

108

Farming boosts Brazil's external accounts. Flows decomposition shows agricultural export volume as the catalyst of large trade surpluses. We estimate farming productivity gains have lifted the underlying trade balance by 1.2% of GDP, which means 3% of GDP surpluses in 2023-25.

2

21

110

In Brazil, the decision to suspend energy tax cuts in 2023 shows a new administration willing to pay some political costs. Solid public finances mean more scope to cut interest rates faster. The use of public banks for quasi-fiscal spending is another key thing to monitor.

8

15

108

Despite headwinds such as a temporary oil export tax, Brazil’s energy sector remains a key trade balance driver as increased output has led to higher export volumes. A well-diversified export base will help achieve a trade surplus of >3% of GDP this year, the largest since 2006.

2

29

108

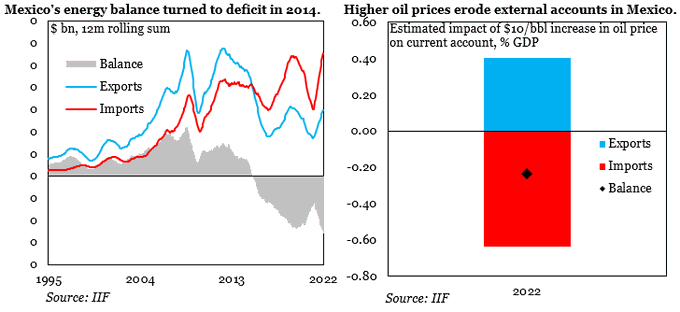

Does Mexico benefit from surging energy prices?

(-) External → net energy importer since 2014.

(+) Fiscal→ mild gains as subsidies offset the revenue windfall.

(-) Inflation → large energy weight in CPI basket.

(-) Growth → modest losses amid policy tightening.

2

33

107

Inflation in Argentina remains well above 100% despite a m/m slowdown in June. Having sound and autonomous monetary institutions is a lesson LatAm policymakers learned long ago. Stabilization plans should be at the forefront of the policy discussion ahead of the August primaries.

3

29

105

In Argentina, the latest incoming govt statements seem to acknowledge dollarization is not viable (no reserves, debt appetite, big new IMF money, resident external financing). With dollarization off the table, the focus should be fiscal and central bank/FX market normalization...

Argentina's next administration, lacking dollars, will be unable to implement full dollarization immediately. But the regime could be put in place later on. What would it take to get the needed dollars? Long story short: a painful recession on top of higher inflation…1/5

6

40

141

3

34

106

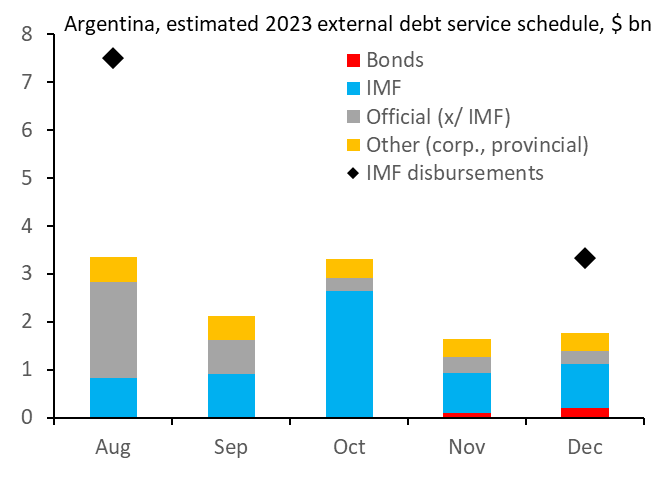

The IMF plans to disburse $7.5bn to Argentina in August and do a next review in Nov. Scheduled IMF debt repayments total $4.4bn until then, but the govt. must also repay $2bn in bridge loans. Further action needed to protect reserves will leave no room for pre-election stimulus.

4

33

104

Regaining net energy exporter status has helped Brazil get a sustained hard currency windfall due to high oil prices in 2021-22. We estimate it at $1.4bn for every $10 rise in oil prices. This unprecedented factor will keep providing support to external accounts and the BRL.

2

31

104

Argentina paid $2.7bn to the IMF using SDRs and borrowed cash while talks to adjust the program remain. This pushed net reserves deep into negative territory. Keeping things afloat until the election requires unavoidable policy corrections along with a revised IMF agreement.

1

28

104

Argentina's vanishing trade surplus has left IMF disbursements as the only source of hard currency. Adopting tough corrective fiscal/monetary measures is the key to bringing more IMF money forward and stabilizing expectations. This should be in place before debt payments in July.

4

31

101

Argentina's net reserves turned negative in May. Borrowed dollars can be used briefly (risky), but there is a long way until the October election...Advancing IMF money, which will require a dose of orthodox policies, is the key to stabilizing things ahead of the August primaries.

5

28

99

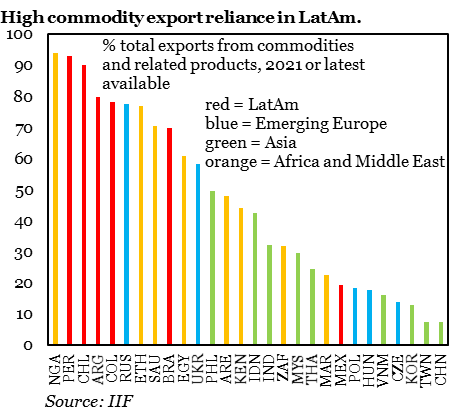

South America's export exposure to commodities stands out from other EM regions. So, the ongoing broad-based commodity price surge should bolster external accounts regionwide. Despite lower reliance, Brazil could notably benefit from its more diversified commodity export base.

0

39

95

In Brazil, markets are pricing in an 80% prob. of a 25bps rate cut in August. Improved external and fiscal prospects have helped a downward shift in the curve. Base effects could push y/y inflation below 4% in the coming months (before rising again in Q4), adding pressure to cut.

7

14

96

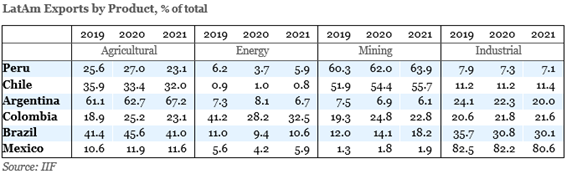

Surging food and energy prices due to Russia's invasion could provide relief to LatAm. Commodity export dependence (from highest to lowest) goes as follows:

•Peru→ copper, gold

•Chile→ copper

•Argentina→ soy, corn, wheat

•Colombia→ oil, coal

•Brazil→ iron ore, soy, oil

4

34

92

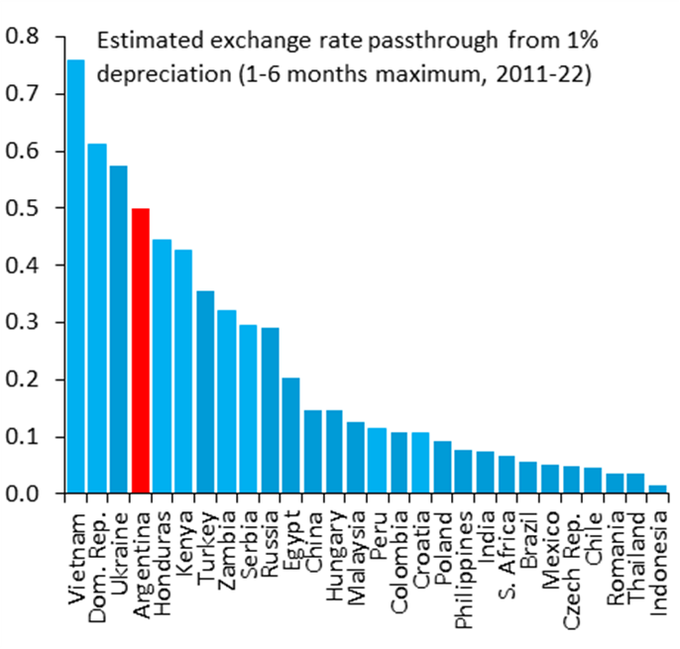

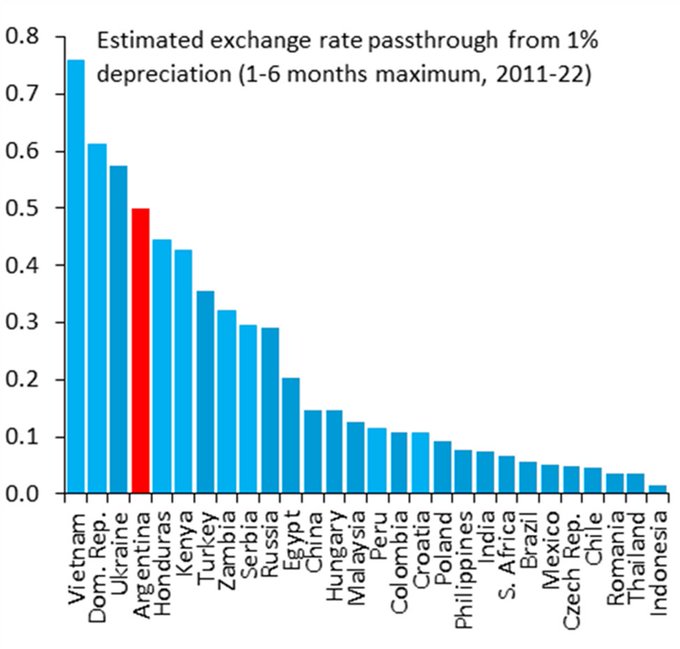

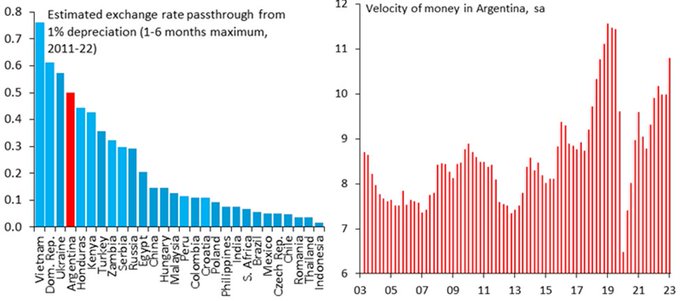

Argentina’s exchange rate passthrough is among the highest in EM. So, the inflation print of 6.3% m/m in July is totally backward-looking amid sharp peso depreciation in August. Clear communication and a roadmap, even just for a three-month timeframe, could help ease FX pressure.

1

27

91

Takeaways from Milei's inaugural address in Argentina:

▪️Starting conditions are critical due to past policy mismanagement.

▪️Massive fiscal austerity is needed to avoid hyperinflation.

▪️Shock therapy is the way to go to regain market access.

▪️No reference to dollarization.

3

21

93

Argentina’s 23Q1 BoP figures show the largest current account deficit since 18Q3, resulting in reserve losses of a similar magnitude. This is consistent with our 2023 external financing gap estimate of $15bn. Policy corrections as part of a revamped IMF agreement are much needed.

2

24

90

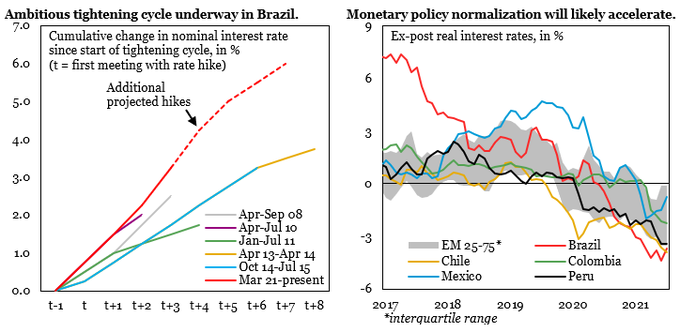

The Central Bank of Brazil reaffirmed its inflation-fighting commitment this week. The ongoing tightening cycle has shown, so far, a much more ambitious trajectory than past episodes. And, there is still a long way to go...

2

22

86

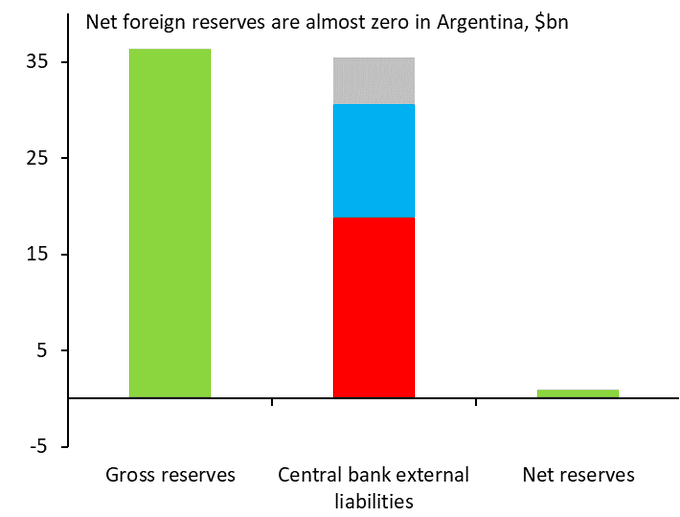

Argentina's central bank balance sheet shows the lack of firepower to contain depreciation pressure. On the asset side, net reserves are almost zero. And liabilities include a large stock of interest-paying securities making rate hikes costly. A broad set of measures is needed...

3

18

81

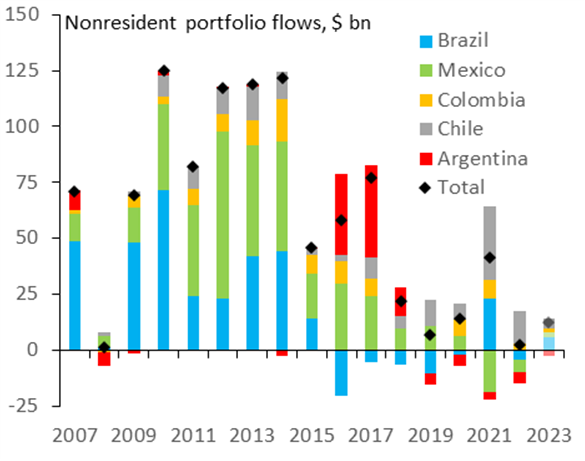

Turmoil in Argentina is idiosyncratic this time. FX controls now cover the whole BoP (goods trade, services, income, capital flows), leaving the country highly isolated. Contagion risk for the rest of LatAm is much lower than in 2018 when participation in global markets was big.

4

21

82

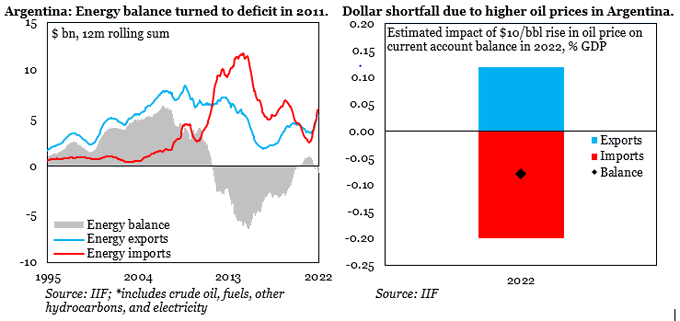

Argentina became a net energy importer in 2011, so high oil and gas prices erode the current account. We estimate a hard currency shortage of $388 million for every $10 rise in the oil price. Nonetheless, surging agricultural prices should help offset the adverse impact.

2

26

83

Brazil’s record-high energy export volume boosted the trade surplus in March despite the new temporary tax. But that was only part of the story. Soybean and other grain exports also rose sharply last month. A robust agricultural sector should keep supporting external accounts.

0

24

76

Brazil's inward FDI reached a record high of 4.8% of GDP in 2022. "True" FDI (ex/reinvested earnings) was large enough to finance the CA deficit. Services & mfg. sectors (not commodity-linked primary activities) got 92% of total inflows, showing ample FDI growth potential.

1

16

78

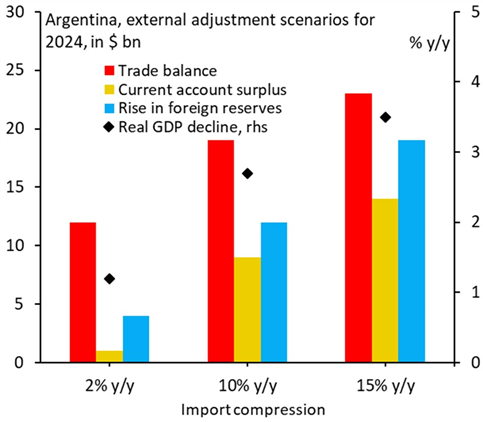

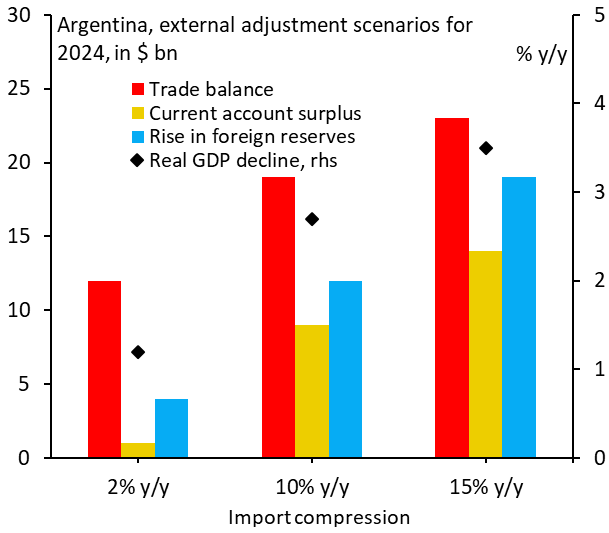

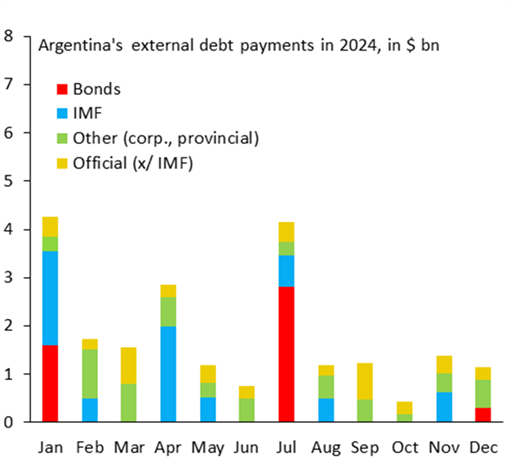

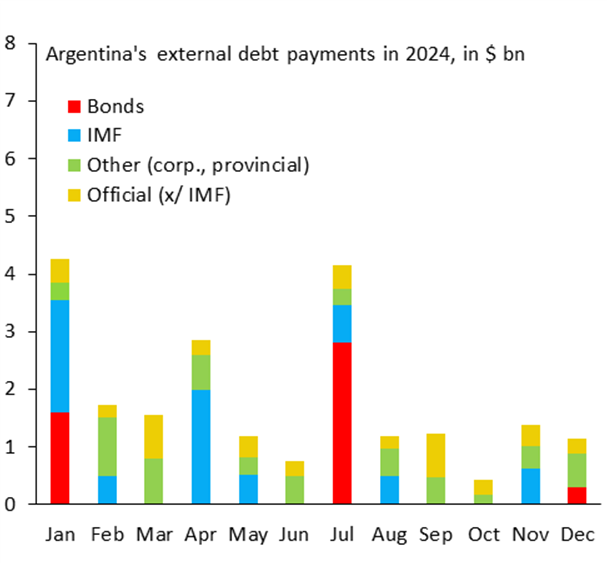

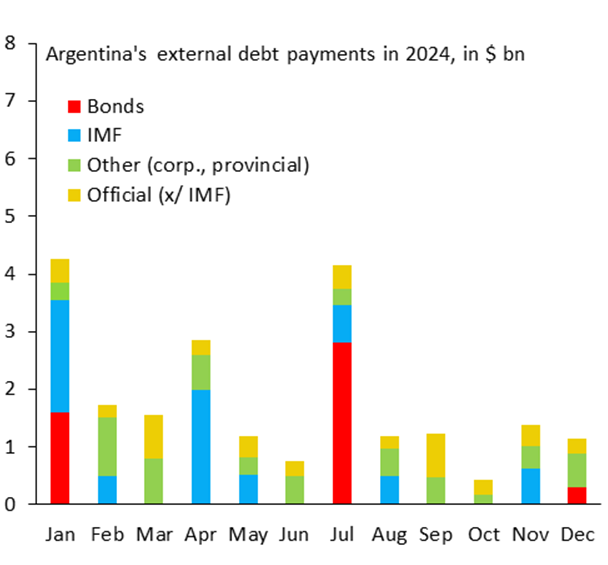

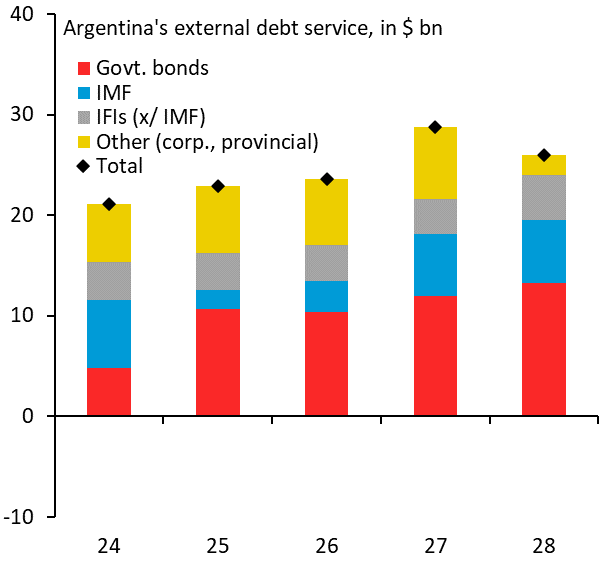

In Argentina, meeting external debt payments of $22bn in 2024 will require a big current account surplus amid a stabilization plan. On top of mounting imbalances, the debt due in Jan. ($1.5bn in bond interest and $2bn in IMF debt principal) should prompt the new govt to act fast.

2

23

80

Inflation in Argentina was 12.4% m/m in August, the highest since 1991, fueled by the post-primary step FX devaluation. Without expenditure adjustment, recent tax cuts mean extra peso printing. So, these measures will further lift inflation, a more harmful and regressive tax...

1

17

79

Argentina’s external debt payments scheduled for 2024 total $21.9bn. These include $1.5bn in interest owed to bondholders and $2bn in IMF debt principal due in January. Redoing the IMF program should be a priority for the next govt amid negative net reserves and no market access.

2

18

80

Brazil’s central bank cut the policy rate by 50bps to 12.25%. The slightly more hawkish press release 1) anticipates cuts of the same magnitude in upcoming meetings (until Jan. 2024, at least) and 2) reiterates the need to meet the fiscal targets (relevant given current talks).

Brazil's central bank will likely deliver a 50bps rate cut today in line with market pricing. Forward guidance is key to watch. Markets have recently priced in more cautious easing despite improved inflation dynamics. Financial conditions should gradually start supporting growth.

0

1

20

4

16

76

We lifted our above-consensus Brazil growth forecast for 2022 as high-frequency indicators suggest activity will regain traction. Reasons include 1) high commodity prices, boosting domestic demand fundamentals; 2) positive investor sentiment; and 3) increased fiscal stimulus.

1

18

78

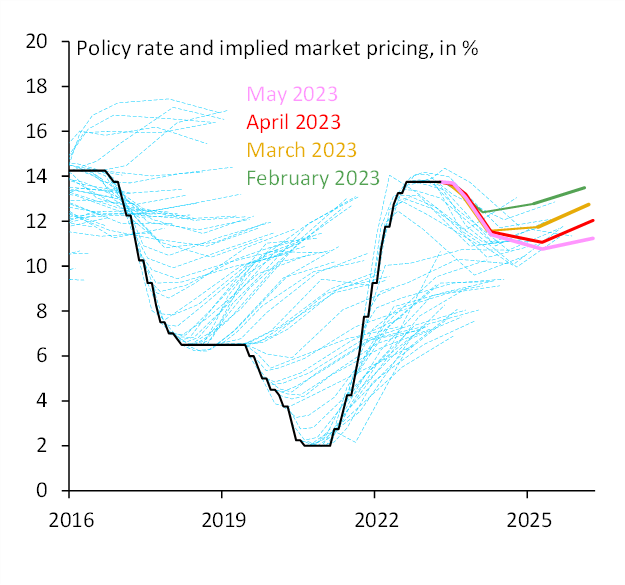

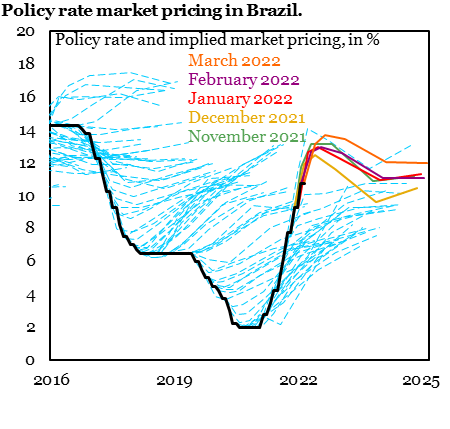

The policy rate in Brazil is on its way to reaching double-digit levels early next year following today’s decision and forward guidance. We expect the central bank to end this quite forceful tightening cycle in March 2022.

1

17

80

Markets in Brazil have started to price additional rate hikes in 23H1 amid fiscal woes. Given increased opportunities stemming from global geopolitics, reinforcing a framework that fosters macro stability could go a long way toward easing financial conditions to boost growth.

6

9

79

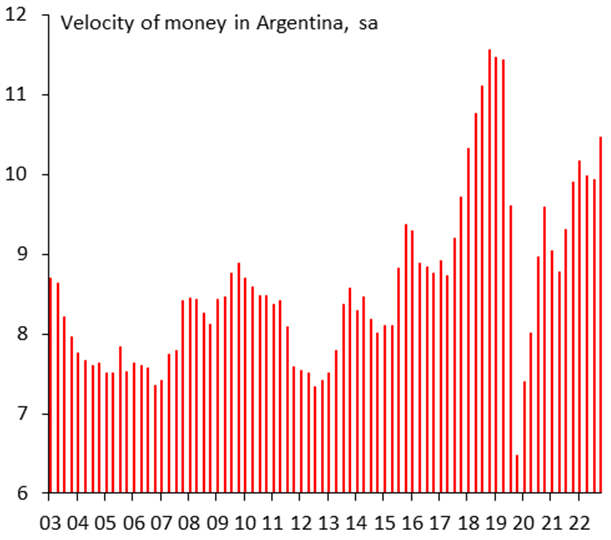

Rising money velocity in Argentina reflects people trying to protect themselves from inflation. Recent tax cuts will not only lead to more peso issuance due to a larger fiscal deficit but also weaker peso demand. Beyond government control, the latter could fuel inflation fast...

3

17

75

Brazil- Main takeaways from BCB minutes:

1) The possibility of a faster tightening pace in the next meeting is on the table.

2) Improved recovery prospects have significantly eased downside risks to inflation.

3) Fiscal risk remains an issue despite recent improvements.

0

13

76

Argentina-IMF talks to revamp the program remain unsettled. We still believe a temporary “damage control” deal will be achieved. This means more FX controls and little adjustment. Imbalances will keep mounting. True policy corrections will be left to the new administration.

2

20

72

LatAm’s central banks have turned to unconventional measures amid widening fiscal deficits and policy rates approaching historical lows. QE-type programs have aimed at avoiding disruptions in the credit market, as opposed to the massive monetary stimulus we have seen in DMs. 1/5

2

22

72

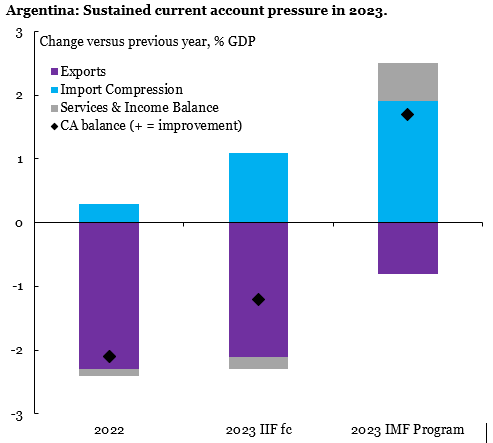

We project Argentina’s current account deficit to widen in 2023. This means a larger financing gap than in the last IMF program review, which includes a surplus. Hard to see imports compressing enough to offset export losses due to the drought and policy woes in an election year.

2

15

71

Inflation in Argentina was 12.7% m/m in Sept., the highest since 1991. Expansionary policies, facilitated by massive central bank peso printing, have further eroded peso demand. A fully unanchored inflation expectations scenario is the worst possible way to face the election...

2

26

71

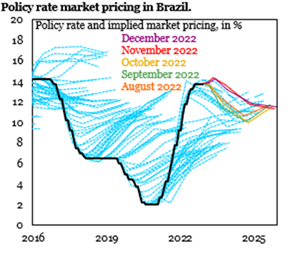

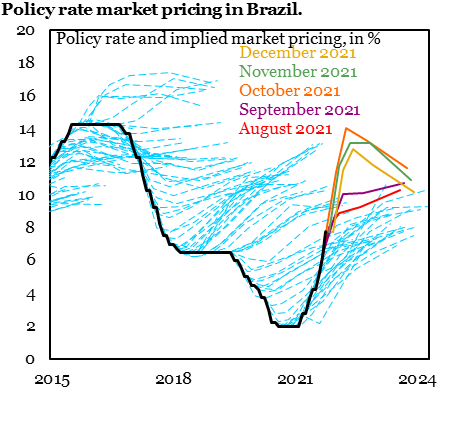

Markets pricing is in line with a policy rate hike of 150bps tomorrow in Brazil. It also shows a noticeable ongoing downward shift in the curve since it peaked in October. We stick to our view of the SELIC climbing to 11.25% through March 2022 after 200bps cumulative hikes in Q1.

0

11

74

Brazilians head to the election on an improving economy. Factoring in weaker activity in the coming months, growth will be close to a robust 3% this year. We are more positive than consensus on 2023 prospects as Brazil will likely maintain a sound macroeconomic policy framework.

3

13

70

Brazil’s 12-month sum current account deficit declined to 2.5% of GDP in July from 2.8% of GDP in Dec. 2022. The transformation in farming, which we estimate has lifted the underlying trade surplus by 1.2 pp of GDP in the last decade, will keep easing external financing needs.

1

10

70

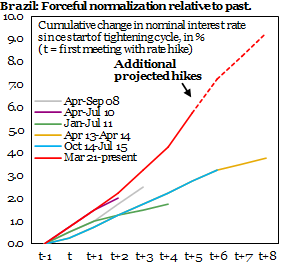

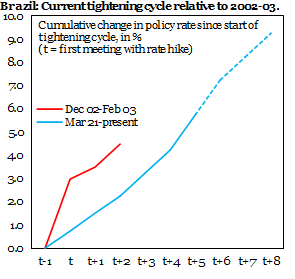

Brazil's terminal policy rate could reach 11.25% by March 2022, reflecting aggressive tightening relative to recent cycles. Tightening was also quite forceful in 2002-03 ahead of Lula's first term. Back then, pragmatic policies helped quickly improve market conditions.

3

16

70

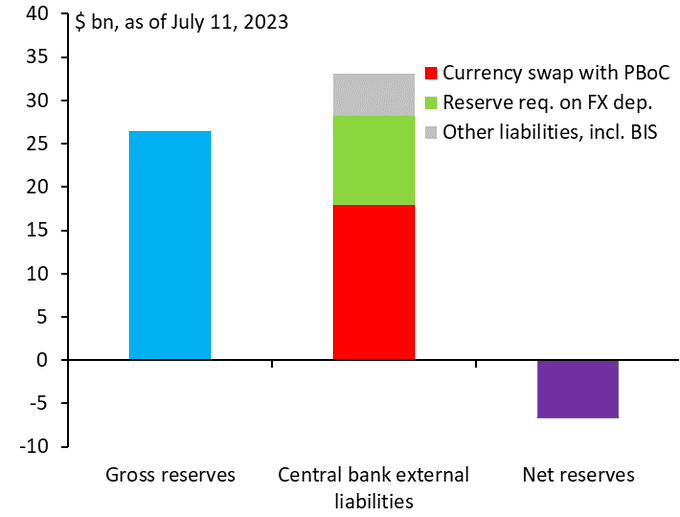

Foreign reserve depletion remains in Argentina. Using borrowed cash (China swap and reserve requirements) to repay debt and keep the peso artificially strong will not last. There is no substitute for a new IMF program/ policy corrections to stabilize things until the election...

0

18

71

The Argentine peso is sliding again in the parallel market, playing catch-up with inflation. It remains stronger than in mid-2022 in real terms, though. Still, highly ineffective FX controls and the drought will make it tougher for the govt. to muddle through until the election.

3

15

65

We track inflation generalization in LatAm by calculating the combined weight of items in CPI baskets. Our bottom-up approach shows:

▪Lower pressure in Brazil and, more recently, in Chile.

▪A broad-based process in Colombia and Mex., consistent with the need for higher rates.

0

19

67

In Brazil, the spillovers from war should support the current account and lift growth while adding to inflation pressures. Markets expect the central bank to hike the policy rate by 100bps tomorrow in line with forward guidance but are pricing in higher yields than a month ago.

2

18

65

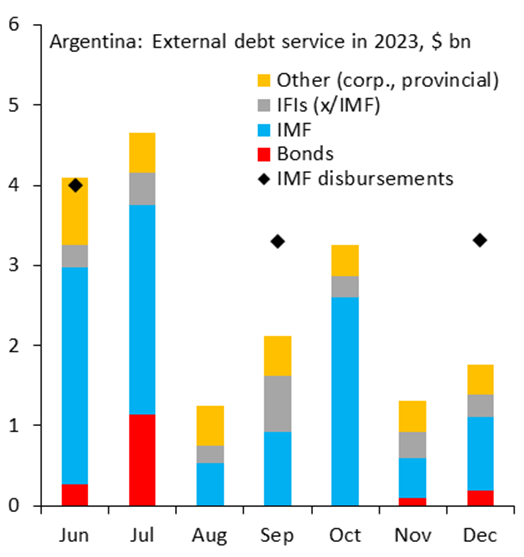

The China swap upgrade and more FX controls announced last week buy Argentina little time. Things will get tougher soon. External debt service of $4.7bn (IFIs, global bonds, corporates, provinces) and no IMF money in July mean a new repayment/disbursement plan is urgently needed.

1

23

64

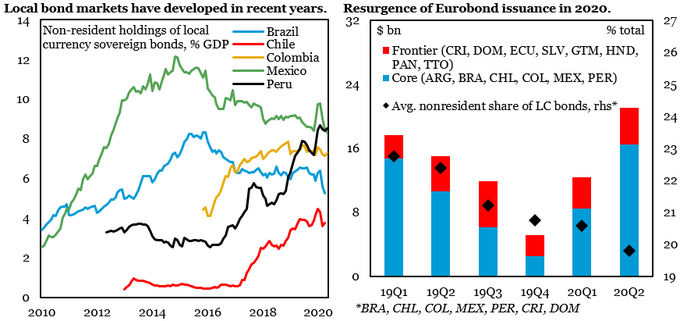

“Original sin” is another well-documented EM macroeconomic challenge that LatAm countries have tried to surmount. Even though the capacity to borrow abroad in local currency has recently increased, the response to COVID-19 suggests there is still a long way to overcome it. 1/6

2

27

65

Argentina's FX controls have led to multiple distortions. FDI has been artificially lifted by 1) forced reinvested profits and 2) increased intercompany loans amid restricted official FX market access. But new equity was only 0.1% of GDP (5% of total) recently, lowest since 2015.

0

15

63

In Brazil, foreign direct investment (FDI) has remained robust at 4.1% of GDP in November. Controlling for reinvested earnings, inflows have recovered remarkably this year, providing ground for balanced and investment-driven growth. FDI should also help sustain activity in 2023.

1

9

63

The scope to keep hiking rates is ample in Brazil amid a robust recovery underway and upward inflation risk. Fiscal and global developments have spurred investor concerns this week, although nothing too different from other episodes Brazil has weathered in the recent past.

1

20

62

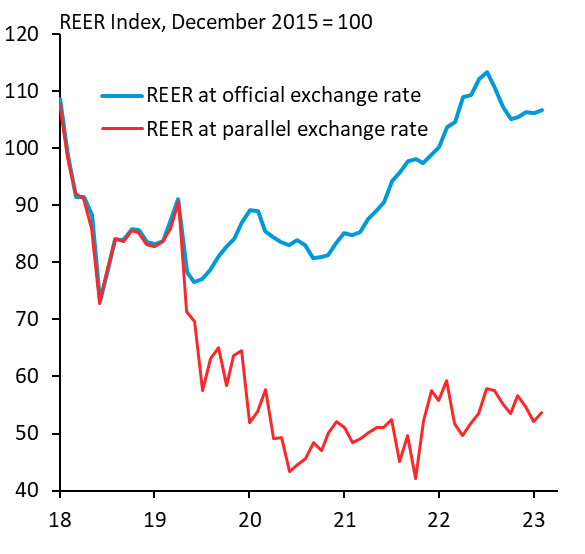

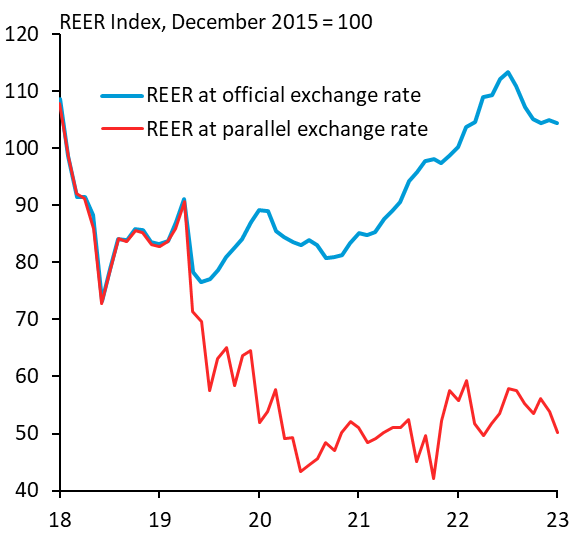

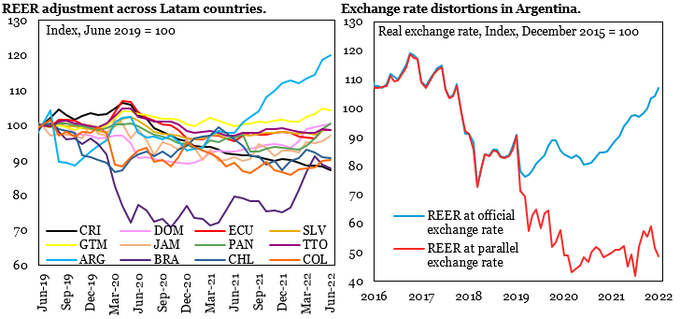

Argentina’s steady real exchange rate appreciation, measured by the official FX, has become such an outlier in the region. The main reasons are high inflation and self-inflicted policy wounds, including foreign exchange controls that only exacerbate distortions and imbalances...

Argentina's parallel exchange rate (white) is now 110% weaker than the official rate (orange). Back in 2018, we worried greatly about potential for contagion from Argentina to the rest of EM. Not anymore. Markets have retrenched and given up. With

@mcastellano44

&

@SergiLanauIIF

13

42

244

3

19

59

Implementing dollarization in Argentina would require locals to bring home their dollars held abroad. These cash external assets, among the largest in LatAm at $265bn (41% GDP), have been built steadily over time to protect from policy woes, something dollarization won't fix...

2

25

60

Mexico's growth story remains solid, driven by services. The Q1 flash GDP growth reading was an upside surprise at 4.5% q/q saar, leaving a carryover of 2.2% for 2023. Despite tight policies and weak US activity, growth is set to be the highest in major LatAm countries this year.

0

15

59

Foreign direct investment in Mexico-the LatAm country best positioned to gain from nearshoring- ended weak last year, despite being solid regionwide. Lagging its peers, Mexico would have gotten $50bn in 2022 instead of only $39bn just by getting the 10-year LatAm avg. in % GDP...

3

13

61

Brazil’s central bank cut the policy rate by 50bps to 11.25%. The press release:

✅Reflects comfort with the current easing pace, which we think will be maintained through July.

✅Highlights disinflation progress.

✅Reinforces the need to meet the fiscal targets.

1/2

1

8

64

Brazil's inflation was well-behaved in May. Base effects will bring it further down to about 3.5% on a y/y basis in June. This would be close to target and lowest since Sept 2020, adding pressure to cut rates. But base effects will make it quickly rebound to end above 5% in 2023.

0

17

58

Inflation generalization has eased in Brazil amid a cautious monetary policy. In June, the weight of IPCA items with >3% inflation receded to the end-20 level. Base effects will make y/y inflation rebound in Q4, but favorable dynamics should allow for a 25bps rate cut in August.

5

9

58

Dollarization has yet to persuade Ecuadoreans to stop sending cash abroad. In contrast, other monetary regimes have proven effective in fighting inflation while bolstering policy credibility. Hard to think that good alternatives to dollarization are beyond Argentina’s reach…

2

20

58

Argentina announced the activation of another tranche of its China currency swap. The line acts as a costly short-term BoP loan with limited uses. This short-sighted move could help delay the adjustment and meet upcoming IMF payments at the expense of higher imbalances in 2024...

3

22

58

The first presidential debate in Argentina showed agreement on the need to cut the fiscal deficit. But we have yet to hear specifics. Meeting external debt payments will require a big current account surplus via import compression. A grain export rebound in 2024 won’t be enough.

1

11

58

Brazil's central bank has been on hold for a year after a long tightening cycle. While still tough, improved inflation dynamics provide room for a prudent 25bps rate cut today. Following Chile and Brazil, we also see monetary policy easing in Colombia, Peru, and Mexico this year.

0

9

55

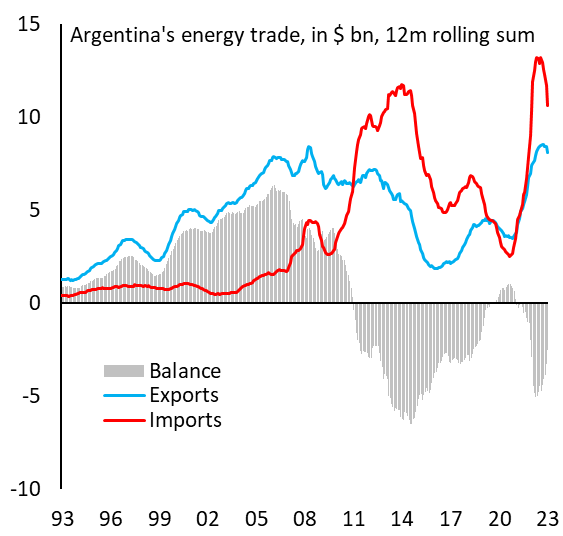

Despite recent improvements, Argentina’s energy sector remains a drag on external accounts, adding $2.5bn to the 12-month rolling trade deficit. Attractive market/resource conditions are no substitute for sound economic policies to regain net energy exporter status sustainably...

0

13

54

In a tight split decision, Brazil's central bank reduced the policy rate by 50bps and indicated cuts of similar size in upcoming meetings. The move was above our 25bps cut call, which was also the minority's preference. We now expect the policy rate to end at 11.25% this year.

1

12

54

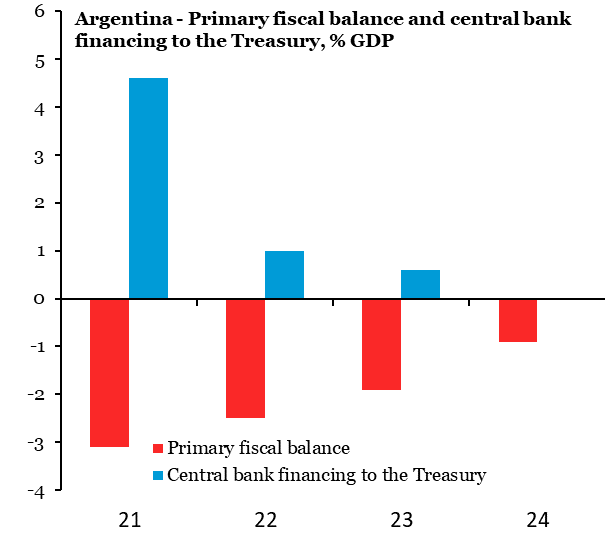

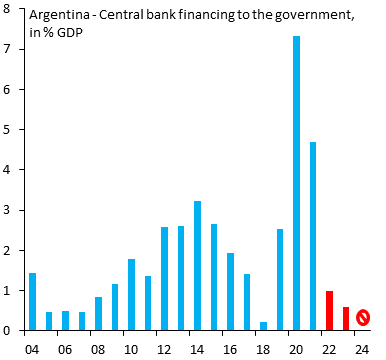

Moderate fiscal consolidation and ambitious rollback of monetary financing in 2022-23 would mean heavy debt issuance in a shallow local financial market, adding pressure on interest rates. Global debt is not an option, and further official funding will be tough to get.

Argentina's description of the preliminary agreement with the IMF sounds like quite a bit of effort on some fronts. Monetary financing falling from more than 4% of GDP to 1% this year and 0.6% in 2023. Looks like one of the areas where implementation will be a real struggle.

5

24

85

2

11

50

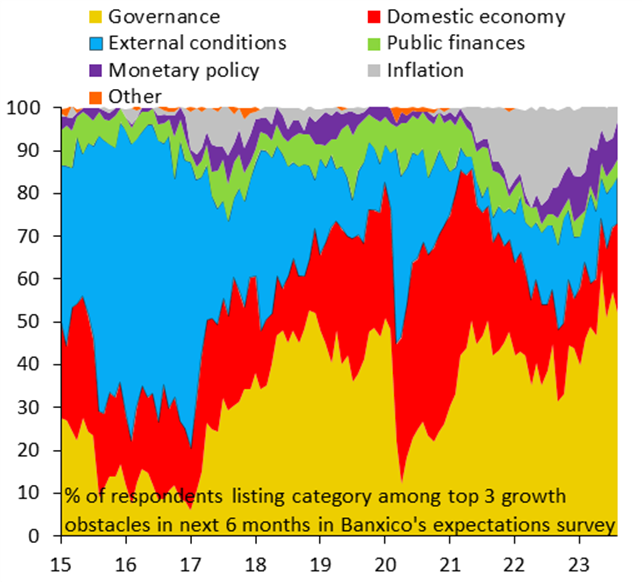

In Mexico, once again, domestic hurdles (yellow, red) are at the top of public concerns as we approach the 2024 election. These include crime and the weak rule of law. External factors (blue) and inflation (grey), key sources of uncertainty last year, are less relevant in 2023...

4

15

53

Brazil’s external accounts remained solid in Feb., showing robust inward FDI and smaller resident capital outflows. Main thing to watch is the upcoming release of the fiscal framework. A confidence-boosting proposal is key for lifting investment and unleashing policy rate cuts...

2

18

52

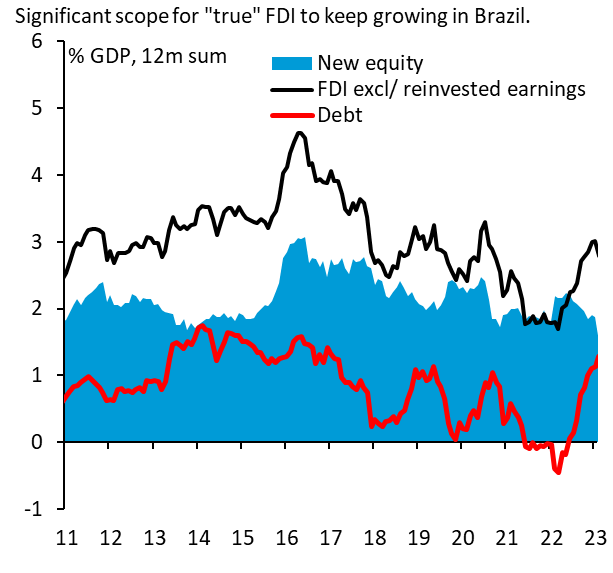

In Brazil, “true” (x/ reinvested earnings) 12-month foreign direct investment (FDI) was 2.9% of GDP in March, large enough to cover the current account deficit. This is mostly new money invested in services (not commodity-related activities), signaling ample FDI growth potential.

6

12

53

Things to cover in our Mexico investor trip this week

@IIF

:

1) Super MXN, for how long?

2) Is the core inflation decline sustainable?

3) Will activity keep surprising on the upside?

4) Is nearshoring already showing up in the data?

5) What policy changes should we expect in 2024?

4

12

52

Key monetary policy meeting next week in Brazil. We see further acceleration in the tightening pace, which could bring the policy rate into double-digit territory early next year. Factors supporting this view include our above-consensus growth forecast and persistent fiscal woes.

2

12

52

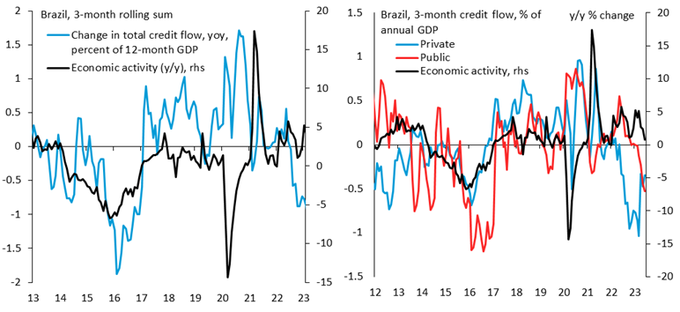

Credit impulse in Brazil remains negative, but it has recently stabilized. Financing conditions should gradually improve in the near term, becoming less of a drag on growth. We expect a policy rate cut of 50bps this month, in line with BCB forward guidance and market pricing.

0

5

50

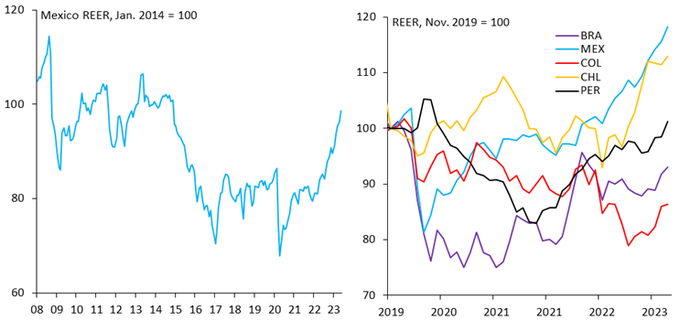

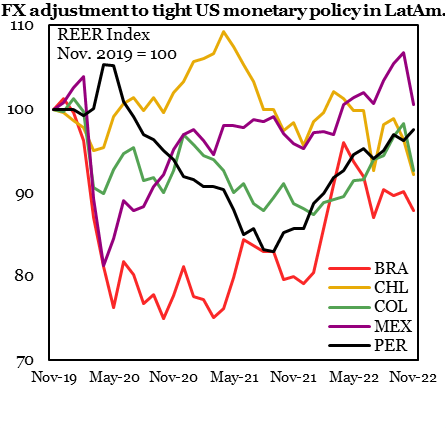

The real exchange rate in Mexico has returned to pre-pandemic levels this year amid tight policies. Favorable current account and FDI dynamics have helped offset persistent portfolio outflows. But sustained peso strength could weigh on external accounts and growth in 2023...

0

7

51