Martin Bruns

@mbecon1989

Followers

169

Following

32

Media

33

Statuses

61

Lecturer at University of East Anglia School of Economics

Joined May 2022

"Comparing External and Internal Instruments for Vector Autoregressions" (with Helmut Lütkepohl) is now available online at the Journal of Economic Dynamics and Control. We compare two approaches to identify multiple shocks in SVARs via multiple proxies. https://t.co/x3BduScZLo

0

5

26

Thanks to all the presenters at the workshop for sharing their research and for a lively debate.

0

0

2

The workshop ends with three great presentations by Marko Mlikota (Geneva Graduate Institute), Luca Pedini (ENI Milan), and Ralf Brüggemann (University of Konstanz).

0

0

1

The next session had presentations by Nikolaos Angelopoulos and Gustavo Frist Dias (both University of East Anglia) and Saeed Zaman (Cleveland Fed).

1

0

1

The second keynote speech is by Christiane Baumeister (University of Notre Dame).

0

0

4

The best paper award goes to Marko Mlikota (Geneva Graduate Institute). Congratulations!

1

0

2

Day 1 ends on a high with presentations by Daniel Lewis (UCL), Martino Ricci (ECB), and Andrea Viselli (University of Milan).

0

1

2

The afternoon starts with Mirela Miescu (University of Lancaster) and Damiano Di Francesco (Sant'Anna School of Advanced Studies).

0

0

5

Followed by a keynote by Ambrogio Cesa-Bianchi (Bank of England).

1

1

2

The 3rd edition of the UEA Time Series Workshop is off to a great start with presentations by Martin Geiger (Liechtenstein Institute) and Luca Benati (University of Bern).

7

3

15

📢 Tomorrow is the last day to register for the 3rd Time Series Workshop! 🚨 Register now through the UEA store page! https://t.co/hoLGp5sSQb For more information on the workshop, please visit

lnkd.in

This link will take you to a page that’s not on LinkedIn

A program update is available for the 3rd edition of the UEA Time Series Workshop, May 22-23, at University of East Anglia, Norwich. Registrations are open until April 29th via https://t.co/AyxgZgfLOf

0

1

5

A program update is available for the 3rd edition of the UEA Time Series Workshop, May 22-23, at University of East Anglia, Norwich. Registrations are open until April 29th via https://t.co/AyxgZgfLOf

0

4

8

The program for the 3rd edition of the UEA Time Series Workshop is now available. Registrations close on April 29th. More information is available here: https://t.co/cEBNaPvOzE

#econtwitter

0

4

10

Registration is now open for the 3rd Time Series Workshop on 22-23 May! Register now here: https://t.co/340MqAzJbI The workshop is open to both presenters and external participants. Both presenters and non-presenters will need to register by 𝗧𝘂𝗲𝘀𝗱𝗮𝘆 𝟭𝟱 𝗔𝗽𝗿𝗶𝗹 2025.

0

3

3

🚨 Call for Papers deadline: 𝟏𝟓 𝐌𝐚𝐫𝐜𝐡 𝟐𝟎𝟐𝟓 🚨 Only 4 days left to submit a paper for the 3rd UEA 𝐓𝐢𝐦𝐞 𝐒𝐞𝐫𝐢𝐞𝐬 𝐖𝐨𝐫𝐤𝐬𝐡𝐨𝐩 (22-23 May)! Please send a full paper to eco.timeseries@uea.ac.uk For more information please visit: https://t.co/0c6WyJ17KX

0

1

1

Call for papers reminder: 2 weeks to submit to the 3rd edition of the UEA Time Series Workshop, May 22-23, University of East Anglia with Christiane Baumeister (U of Notre Dame) +and Ambrogio Cesa-Bianchi (Bank of England). Submissions: eco.timeseries@uea.ac.uk until March 15th.

0

5

15

Check out our latest ECO working paper: 𝐂𝐨𝐦𝐩𝐚𝐫𝐢𝐧𝐠 𝐄𝐱𝐭𝐞𝐫𝐧𝐚𝐥 𝐚𝐧𝐝 𝐈𝐧𝐭𝐞𝐫𝐧𝐚𝐥 𝐈𝐧𝐬𝐭𝐫𝐮𝐦𝐞𝐧𝐭𝐬 𝐟𝐨𝐫 𝐕𝐞𝐜𝐭𝐨𝐫 𝐀𝐮𝐭𝐨𝐫𝐞𝐠𝐫𝐞𝐬𝐬𝐢𝐨𝐧𝐬 @mbecon1989 (UEA) Helmut Lutkepohl (DIW Berlin and Free University of Berlin) https://t.co/x0q1sAOStt

ideas.repec.org

In conventional proxy VAR analysis, the shocks of interest are identified by external instruments. This is typically accomplished by considering the covariance of the instruments and the reduced-form

0

2

11

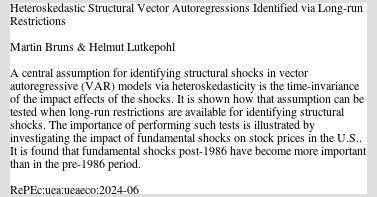

Check out our latest ECO working paper: Heteroskedastic Structural Vector Autoregressions Identified via Long-run Restrictions @mbecon1989 Martin Bruns (University of East Anglia) Helmut Lutkepohl (DIW Berlin and Freie Universitat Berlin) https://t.co/unU8nSKZOX

ideas.repec.org

A central assumption for identifying structural shocks in vector autoregressive (VAR) models via heteroskedasticity is the time-invariance of the impact effects of the shocks. It is shown how that ass

0

2

5

Hi #EconTwitter, Excited to share that our paper "Testing for strong exogeneity in Proxy-VARs" with @mbecon1989 is now published in the Journal of Econometrics. Paper: https://t.co/ofUzv3ErYr Illustration: https://t.co/Pn2s6QbEkP

2

1

7

The third edition of the University of East Anglia Time Series Workshop is going to take place in person on May 22nd-23rd, 2025. The deadline for full paper submissions is March 15th. More info here: https://t.co/txtxOghw2M

#Econtwitter

@UEA_Economics

@UEAResearch

0

4

16