Alberto Gallo

@macrocredit

Followers

23,955

Following

1,470

Media

1,966

Statuses

6,635

CIO, Andromeda Capital Management

London, England

Joined October 2013

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Bills

• 142117 Tweets

#WWERaw

• 109587 Tweets

Bengals

• 98344 Tweets

Washington

• 92360 Tweets

Commanders

• 82385 Tweets

sabrina

• 75035 Tweets

Jayden Daniels

• 69124 Tweets

連休明け

• 59408 Tweets

Terry

• 50333 Tweets

John Deere

• 49599 Tweets

Josh Allen

• 44656 Tweets

Jaguars

• 39121 Tweets

津波注意報

• 36779 Tweets

Jey Uso

• 35877 Tweets

呂布カルマ

• 32003 Tweets

うまい棒

• 28429 Tweets

ブロック機能

• 25746 Tweets

Jags

• 24528 Tweets

Dera Sacha Sauda

• 24057 Tweets

Trevor Lawrence

• 20769 Tweets

Bron

• 16727 Tweets

VOTA X KARIME

• 15987 Tweets

Joe Burrow

• 15043 Tweets

#RaiseHail

• 14864 Tweets

ラッパー

• 13685 Tweets

lorde

• 13100 Tweets

ブロック改悪

• 11694 Tweets

Pinned Tweet

The Silver Bullet | The Limits of Monetary Magic

1

6

20

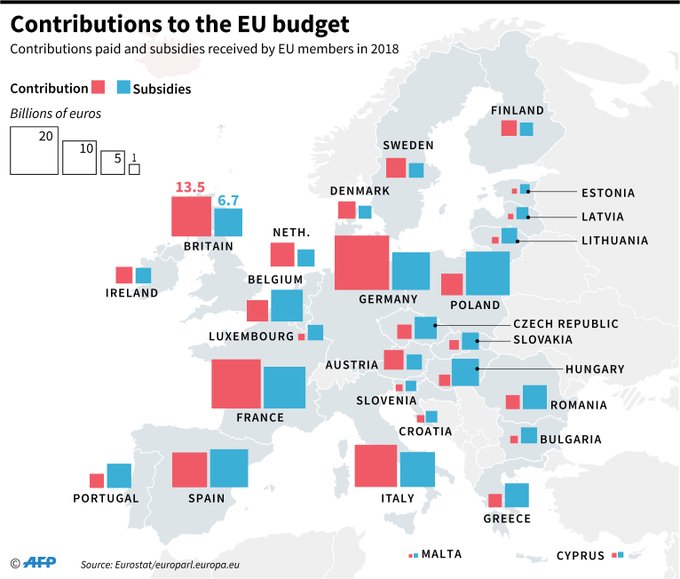

Tax lost from firms domiciled in the Netherlands, per year:

France: €2.7bn

Germany: €1.5bn

Italy: €1.5bn

Spain: €1bn

Dutch net contribution to EU budget in 2018: €2.375bn

(Sources: EU, Tax Justice Network)

79

2K

4K

It is rare for central bankers to be blunt.

Huw Pill's "people need to accept" they're poorer is more than a slip of the tongue.

What central bankers are telling you, is they will not be able to do their job.

13

128

609

ECB:

"Now, you asked me a question about the spreads: I would like to just observe that we are not seeing any such development. While yields have moved up, spreads have not widened in any significant manner. "

Markets:

20

108

527

The UK is now de facto a periphery country: a government on the brink of collapse, constant sunshine and a good football team

#Brexit

24

155

381

Some used to call them "PIGS" economies.

Euro Cup winners since introduction of the €:

2004 🇬🇷

2008 🇪🇸

2012 🇪🇸

2016 🇵🇹

2020 🇮🇹

14

54

359

Leaders Standing up to Trump:

Cuomo NY

McAuliffe VA

Hollande FRANCE

Schauble GERMANY

Trudea CANADA

Sturgeon SCOTLAND

Endorsing him:

May, UK

32

398

297

We now have a Divided Kingdom outside of a European Union.

13

299

299

Which countries have been net contributors vs receivers of EU funds?

Surprising for some, 🇮🇹 has been a net giver, while the balance for 🇪🇦 has been flat.

Grants under the

#EUco

#recoveryfund

are far from a gift - but can be seen as a few years of contributions given back.

21

143

307

In their typical playbook, populists sell people a dream, polarise anger at an enemy, and implement unsustainable economic policies.

The playbook usually results into a four-stage economic and political cycle.

15

82

238

After getting transitory wrong, central banks will hold on to what credibility they have left. No one wants to be Arthur Burns.

Conclusions

- 🚫 pivot

- Volatility ⬆️

- Safe havens ⬇️

- Long/short > long only

- Credit > govies

- Real assets > paper assets

7

20

233

Help

My friend is missing since Friday.

He suffers from memory loss and often believes he's David Cameron. RT pls

11

183

207

#GreekCrisis

negotiations now a pure power play between German block, IMF/US & France/Italy

A country is being used as pawn in a chess game

31

451

209

The five stages of inflation grief

1. Inflation risks are skewed to the downside

2. It's transitory

3. It's here but households won't notice price overshoots

4. It's supply-driven so we shouldn't overreact

5. We need to understand these various transmission channels better

7

58

195

The Netherlands, leader of the frugal four, ranks 4th globally as a tax avoidance centre, with EU countries losing over $10bn in taxes.

Today's

@FT

editorial points out - too kindly - PM Rutte's fragile attempt to take the high moral ground:

3

96

190

US 10yr inflation swaps (blue, rhs) at over 2.7% are now as high as they have been in a decade, while UK 10yr inflation at 4.1% is now at a multi-decade high.

4

62

180

That moment when you realise

#Brexit

was only a way to shift power from the top-left to the bottom-right

10

216

178

"Married or divorced, but not something in between. We are not on Facebook with 'it's complicated' as a status."

Luxembourg PM on

#Brexit

6

173

172

I heard two debt sustainability analyses from taxi drivers in Athens.

And both make more sense than some creditors' arguments.

8

204

173

- Inflation is a social and distributional conflict, as O. Blanchard has pointed out. Why should people accept being poorer when QE has made the rich richer? ()

- They won't. And governments will have no choice but to spend.

3

23

170

Today, England plays Iceland. It's a small island with bad weather and a self-inflicted financial crisis, but I'm sure it can beat Iceland.

9

142

158

"What's the limit?"

Many have asked this question, in relation to central bank balance sheets, as the ECB and Fed asset purchase programmes reach new highs.

Monopoly's Rule

#11

provides a useful, intuitive answer:

#QEinfinity

7

61

159

Fed: neutral stance

ECB: discussing new TLTRO

PBOC: new stimulus

Bye bye Quantitative Tightening

Welcome back to

#QEinfinity

15

86

159

GBP -14.5%

Inflation +2.4pp

Real wages growth rate -2.7pp

Investment -0.9% (Q4 '16)

Happy

#BrexitAnniversary

14

191

156

The Vigilantes are back.

Markets will give a harsh reality check to governments who advertise make-believe policies, denying economic reality:

Turkey, Italy, Britain.

7

119

147

There's no recession on the horizon. The jobs market is still going strong, and investors are again pricing too many cuts too quickly from central bankers.

14

23

148

The US economy keeps rolling.

Financial conditions are loose.

There's no need for Fed rate cuts.

13

30

147

2021 Q2: 2.6%

"Inflation is transitory"

2021 Q3 5.4%

"It's supply-chain bottlenecks"

2021 Q4: 6.2%

"We are not in stagflation"

2022 Q1: 7.5%

"The Russia-Ukraine war is exacerbating inflation pressures"

2022 Q2: 8.5%

"Inflation is peaking"

2023

7

35

140

With persistent inflation and central banks constrained by persistent fiscal deficits and inflation, markets remain optimistically priced for a pivot.

But the pivot might not come. The RBA, which tried to pause twice, has just hiked again.

1

19

140

Theresa May

Knew about the

#MuslimBan

Knew about the

#Tridentmisfire

But kept quiet

Now she keeps quiet about the cost of Brexit

#ResignMay

4

103

128

#Brexit

box update

£/$ <1.3

FTSE250 -10%

4 funds suspended

0.5% bank capital spent

AAA rtg gone

Gilt 10y<0.75%

14

149

121

Good morning from negative yield land, where a fifth of global bonds now trades below 0%

(Source: ICE/Baml)

4

55

118

- Fiscal deficits will be persistent and drive demand, but also erode risk-return in tight government debt (e.g. France downgrade).

- Investors used to a goldilocks environment of low yields, low inflation and rising corporate profits will have to rethink their view of the world.

1

9

123

UK tabloids are like the Pound: if you thought they couldn't reach a new low, think again.

10

88

112

Keeping front-end rates high, while tapering QT, is like pulling the handbrake while pushing the accelerator pedal.

Long-end rates affect asset prices and large fixed income borrowers, as well as wealthy households.

Poorer households and smaller firms, instead...

6

23

115

Balancing price stability vs financial stability in a post

#QEinfinity

world is a difficult act.

“There is no trade off between price stability and financial stability", said ECB President

@Lagarde

in March.

That is true, until something breaks.

1

6

117

Political risk premium is back in bond markets.

The consensus narrative for govt bonds has been: "buy because you won't get another chance as central banks cut rates"

Wrong.

We are in a higher for longer regime, and we will live with persistent inflation and persistent fiscal

5

23

110

As discussed earlier, the combination of higher inflation per unit of growth suggests central bankers won't be able to get a goldilocks free-lunch soft landing, will soon have to choose between price stability vs financial markets stability.

4

23

108

The United Kingdom (1707-2016)

The Divided Kingdom (2016- ...)

6

240

105

The BoJ pause bought time for other central banks to curb inflation without excessive shocks. Ueda might be signalling the extra time is running out.

2

28

103

The Bloomberg US Financial Conditions Index is at record highs.

Risk premia in stocks and credit are near all-time tights as commodities are breaking higher.

Meanwhile, the Fed says its policy is restrictive, after tapering Quantitative Tightening.

8

31

101

Greece says no.

Germany says no.

One has cash-strapped banks, the other a lower euro that boosts exports

Who do you think will blink first?

33

228

90

The difference between this year and the past decade is central bankers are no longer in the driving seat - inflation is.

7

18

100

Turkey's economy is now heading towards phase 3 of the populist playbook: Erdogan's cannot kick the can with more debt/low rates - his only option is to blame foreigners.

8

16

100

6

71

92

But the recent SVB, CS and FRC crises show us that after over a decade of low rates and low volatility, the financial system is fragile.

And that the solution inevitably involves some degree of government support.

What are the conclusions?

3

5

94

Since Brexit

£ at 31-year low

10y yield record low

£100B wiped off FTSE

AAA rating lost

Factories leave

But, you got your country back

7

71

89

Tax dumping/tax havens get defended in the name of economic liberalism. This argument keeps failing.

No-rules capitalism isn't capitalism.

It generates inequality, low productivity and eventually unhappiness. The old model is broken.

The EU exists to level the playing field.

Tax "lost" must be one of the most ludicrous concepts in history. As if those alleged tax revenues would have existed at all if the Netherlands was a high tax nation like others in the list.

The extractive and confiscatory view of business and taxation never cease to amaze.

5

16

71

14

17

86

Raising the inflation target to 4% using the same QE tools is a bit like raising the highway speed limit up to 250km/hr when all you're driving is a Fiat 500.

2

26

88

Who's still against Greece? And who supports Greece in Europe

#GreekCrisis

http://t.co/CuAyALC36g

16

241

86

Bond markets in liquidation mode, probably driven by unwinds of leveraged strategies.

When these are over, there will be great opportunities for long-term investors.

11

38

89

18

80

88

US/UK crisis shows extreme neoliberal economics have failed.

The world needs a more balanced model.

10

63

87

GRIN: Greece stays in €

GREXIT: Greece exits €

GRINCH: Greece in €, Schaeuble steals Christmas

(RT

@charlesforelle

)

11

99

86

10-year inflation expectations are higher following today's weak jobs report:

Covid/delta hits specific economic sectors (leisure and hospitality), the Fed reacts with a delay on tapering and lower for longer, and the result is more inflation down the line.

#QEinfinity

5

22

81

Since

#Brexit

£ at 31yr low

AAA rtg lost

Property buyers ask ~10% discnt

0.5% bank capital spent

FTSE250 -9.4%

Still tired of experts?

20

93

84

#Greece

reminds us again of democracy & human rights while countries in far better situation (US/UK) go adrift.

5

66

83

The 5-year German

#Grexit

"solution" requesting €50bn of Greek "valuable assets"

one word: enough

#Schaeublexit

http://t.co/pXYQCTG6zD

10

153

80

10:03 *ERDOGAN: CENTRAL BANK INDEPENDENT, TAKES ITS OWN DECISIONS

10:09 *ERDOGAN: WE SHOULD CUT THIS HIGH INTEREST RATE

That was quick

5

62

82

You now need €10 million to make an annual pension income of €60,000 pre tax and pre inflation, if you hold 30-year bunds

#QEinfinity

#FinancialRepression

13

31

81

Fed terminal rates are now above 5%.

Rates can still go wider - but risk premia should take the lead now - as we enter the next stage of the anti-goldilocks era.

1

16

79

For many years,

#Turkey

's government forced public & private banks to push credit to the economy, and sell Dollars to support the Lira.

Result: negative net FX reserves and a double-digit % GDP contingent liability on the sovereign.

Today, the first cracks are starting to show.

6

27

81

#Turkey

: Lira weakness comes back as policymaker continue to play with overnight markets without addressing fundamental problems: excess private leverage, fiscal deficit, unsustainable infrastructure investment, rising inflation vis a vis too low interest rates.

6

58

80

JFK customs officer: what do you do?

Me: I'm an economist

O: so is the Fed gonna do QE4?

Me: maybe next year

O: should I buy stocks?

A: No.

6

62

76

Surprise: even after 500bp hikes, interest rates are not restrictive yet, recent

@kansasCityFed

research says.

Why?

Inverted yield curves and insufficient quantitative tightening are part of the problem, as discussed in our latest

#SilverBullet

.

4

21

79

The

@economist

is usually top quality.

On Italy's reform, their analysis is superficial, as its readers point out.

23

41

71

After ten long years of stagnation,

#Italy

is growing.

Now, the country needs five key reforms to make it count.

- Justice system

- Education

- Bank consolidation

- SME financing

- Welfare and social mobility

On today's

@Corriere

@L_Economia

7

40

77

The Magic Money Tree: how over $2 trillion investment strategies rely on short volatility and QE, and why some may be at risk of losing most of their value:

1

47

75

Things no longer exist:

Dinosaurs

Audio cassettes

Positive risk-free returns

Discussing today

@BloombergTV

with

@flacqua

5

15

75

#Brexit

reality check:

the rich who funded

@vote_leave

get corp tax cuts

the poor who voted leave get inflation, no EU funds and 'freedom'

12

96

73

The “thing that’s not priced in” is that both inflation and interest rates will be much higher, for much longer, than the markets are willing to price.

via

@totemmacro

@FT

6

23

76

Why are Fed hikes not working?

First, both corporates and households termed out their debt over a decade of NIRP. The average maturity of $ investnent grade credit is now 13 years, and >98% of mortgages are fixed. This means short end rates aren't effective.

6

18

74

What should investors do in a market where there's nothing left to buy?

Central bankers have skewed the odds against investors. Our job is to rebalance them in their favour: in our latest

#SilverBullet

we explain how we can find value in a

#QEinfinity

market.

7

16

73

How many civilians killed, hospitals attacked, neutral ships sank, before Europe gets serious?

Time to take off the white gloves.

5

19

72

Britain saved 10,000 children in WWII.

Today, it has admitted a handful, with widespread complaints that they aren't all girls.

6

60

68