Ziang Li

@ZiangLi_

Followers

701

Following

879

Media

7

Statuses

46

🔜 Finance Assistant Professor @ImperialBiz | PhD @PrincetonEcon | Financial Intermediation, Asset Pricing, Macro-Finance, Behavioral Economics & Finance | 李子昂

Princeton, NJ

Joined August 2019

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

ALL EYES ON RAFAH

• 796778 Tweets

De Niro

• 387631 Tweets

Palestino

• 103996 Tweets

Fernando

• 92116 Tweets

#WWENXT

• 56714 Tweets

Thomsen

• 54044 Tweets

#خادم_الحرمين_الشريفين

• 50758 Tweets

Millonarios

• 38365 Tweets

Lali

• 37777 Tweets

Lali

• 37777 Tweets

Coronado

• 36152 Tweets

Lala

• 35490 Tweets

Renê

• 34261 Tweets

DAME MIL FURIAS

• 34159 Tweets

Paulinho

• 33737 Tweets

Peñarol

• 30256 Tweets

$BOOST

• 26582 Tweets

Wesley

• 18251 Tweets

Sudamericana

• 16133 Tweets

Josh Gibson

• 14829 Tweets

Jordynne Grace

• 13047 Tweets

#PumpRules

• 11494 Tweets

Pinned Tweet

Finally a PhD! Huge thanks to my advisors

@MarkusEconomist

,

@MoritzLenel

, Jonathan Payne, Wei Xiong, and

@motoyogo

for the past 6 years.

Looking forward to the next chapter at

@ImperialBiz

. See you in London!

8

2

140

Thank you

@PrincetonBCF

for the Ben Bernanke Prize! Check out the paper here

Congratulations to Ph.D. candidate

@ZiangLi_

on his outstanding job market paper and subsequent award of the 2023 Ben Bernanke Prize in Financial and Monetary Economics!

Learn more about this award and Li's research:

@MarkusEconomist

1

0

58

2

5

93

I’m on the job market! Here is a thread on my job market paper, which looks at how long-term interest rates (e.g., 10-year Treasury yields) affect the corporate bond market.

Ziang Li’s (

@ZiangLi_

) job market paper examines how long-term interest rates affect corporate bond credit spreads. He finds that increases in long rates have led to declines in credit spreads after the 2007-2008 Financial Crisis.

1

7

36

1

10

95

Happy to chat! Also please check out my other papers on my website!

3

1

8

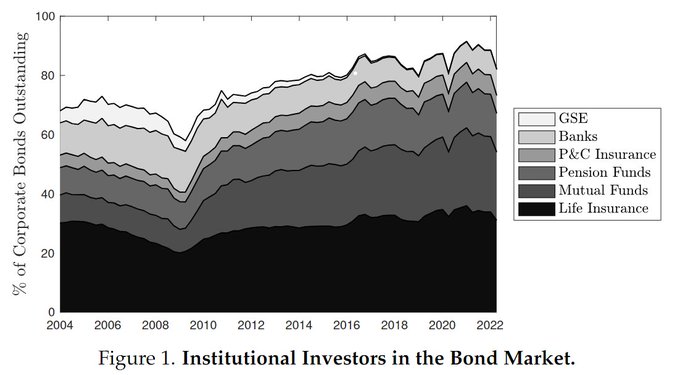

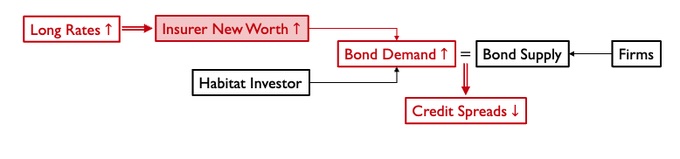

I find that life insurers (largest bond investors, >30% market cap) are key contributors to this result. Post-2008, insurers start to face severe duration mismatch —> their market equity rises by over 7% when the 10y Treasury yield rises by 1%.

1

1

6

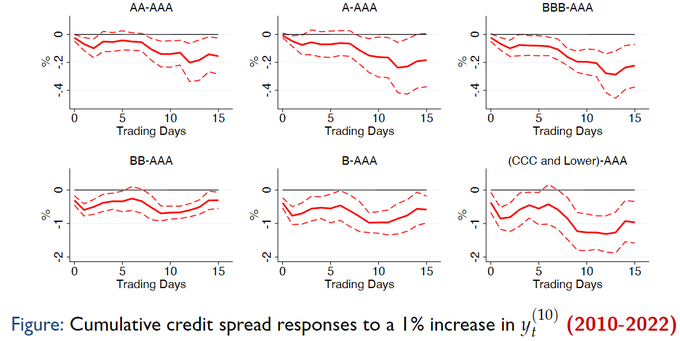

I document that rises (declines) in long rates depress (heightens) credit spreads after the 2008 Financial Crisis

1

2

5

I build a quantitative model based on this mechanism that explains the observations. The model shows that unconventional monetary policy, such as QT, which raises long rates, has large unintended consequences in the bond market.

1

0

2

When long rates increase, insurers receive equity gains and become less constrained. They increase their bond demand, which lowers credit spreads.

2

0

2

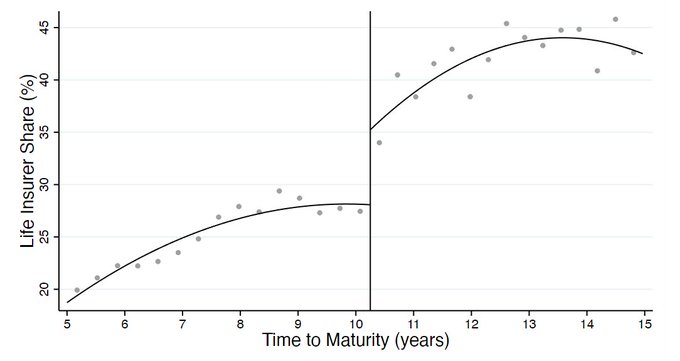

I provide causal identification using an exogenous discontinuity in bonds’ investor composition due to mutual fund investment mandates and confirm that spreads of bonds held more by insurers exhibit stronger responses to long rates.

1

0

2

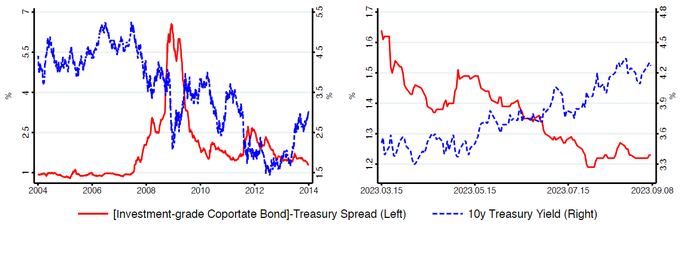

It helps explain two striking market observations: (1) heightened credit spreads in the low-rate environment post-GFC and (2) tightening of credit spreads this year following the recent hiking cycle. (also in )

1

1

1

The channel has large real effects on bond issuance and firm investment -- new bond issuance is tilted towards speculative-grade bonds when rates are higher

1

0

2