Rihard Jarc

@RihardJarc

Followers

39,473

Following

2,682

Media

435

Statuses

6,895

Investor & writer @uncoveralpha . Tweets are only opinions. Researching and sharing the findings of the technology sector in detail (+12k subscribers).

Joined January 2016

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

ariana

• 243330 Tweets

$GME

• 203499 Tweets

Dr. Phil

• 150570 Tweets

Corinthians

• 139511 Tweets

the boy is mine

• 135333 Tweets

South Africa

• 90153 Tweets

Roaring Kitty

• 78453 Tweets

Alcaraz

• 73393 Tweets

Sinner

• 71451 Tweets

Saka

• 44380 Tweets

READ THE ROOM SOON

• 42265 Tweets

Dolly

• 39826 Tweets

Kaytranada

• 32810 Tweets

$PEIPEI

• 29504 Tweets

Gordon

• 25830 Tweets

#BBCDebate

• 23150 Tweets

Iceland

• 16900 Tweets

Justine

• 13750 Tweets

Zverev

• 13040 Tweets

القايمه السوداء

• 12717 Tweets

Penny Mordaunt

• 12684 Tweets

Rayner

• 11313 Tweets

Carlitos

• 11162 Tweets

Ruud

• 10140 Tweets

ジムシャニ

• 10011 Tweets

Pinned Tweet

My article on Generative AI is out.

Breaking down what industries and companies stand to benefit most and what the future of generative AI might look like.

From cloud players: $MSFT, $GOOGL, $AMZN to data companies and semiconductors.

27

118

555

I have nothing against shorting a stock. Although I would not be short $TSLA because of Elon. But how can you ask the CEO of a company you are shorting to come and join you (aka put money) in your friendly charity endeavors. That is crazy, seriously.

107

93

2K

I sold my $GOOGL position today.

I will be publishing an article explaining the reasons in the coming days, but in a short summary:

$GOOGL was one of my biggest positions and has done well for me over the years, but I want to go on the sidelines right now.

1. Search is over

136

114

1K

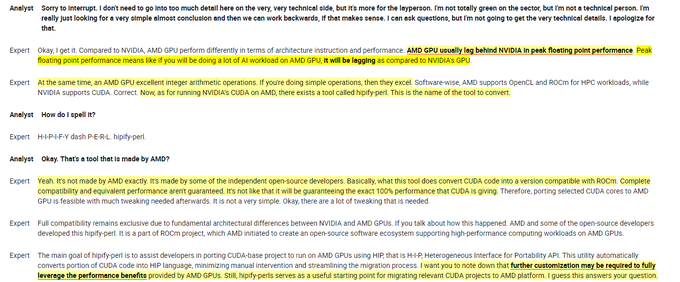

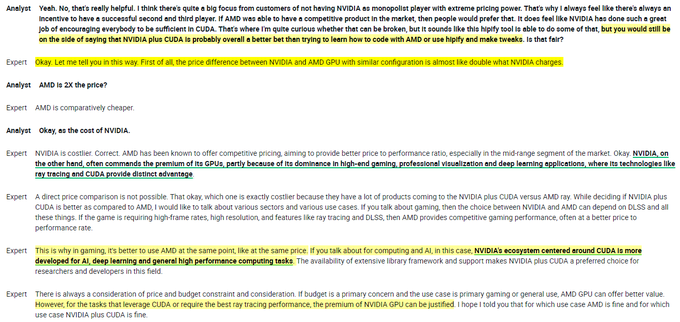

Interview with former $NVDA Researcher. One of the best explanations of the difference between $NVDA and $AMD and CUDA's »edge«. Worth the read:

1. $AMD's GPUs usually lag behind $NVDA in peak floating point performance. The use-case for that is if you will be doing a lot of AI

39

141

831

Added to $GOOGL today...Weird times we live in, where the leader in AI trading at a 12x EV/EBITDA with $80B of net cash and +100k best engineers is being questioned if he will be able to compete with startup AI products.

The biggest risk was cost discipline which changed today.

40

49

788

$META reported on their earnings call:

- Reels taking time from TikTok and grew +50% vs 6 months ago

- WhatsApp fastest growing region is the US right now

- WhatsApp click-to-message ads crossed $1.5B growing 80% YoY

- Users & time spent is record high

Core is more than solid!

38

83

773

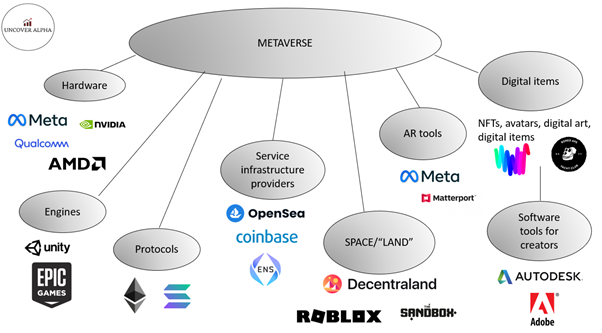

Every decade something special emerges that is about to change the world. And this is it for me - The Metaverse.

The assets that interest me in the space as an investor.

👇👇👇

$FB, $NVDA, $AMD, $U, $SAND, $MANA, $ENS, $ETH, $COIN,

#BAYC

& more.

34

185

763

A portfolio of $AMZN, $MSFT, $GOOGL and $META will probably outperform most other portfolios in a 5 year time frame including all the indices.

Setting a reminder to circle back on this call in 5 years.

96

38

742

$DIS stock is lower than what it was before Disney announced Disney+.

41

40

701

A must-read interview for investors investing in the AI space from a Former high-level employee at $MSFT who also worked with OpenAI from the $MSFT side. Key insights from the interview:

1. When they tested Copilot, productivity gains were average in the 60-70% range. Copilot's

18

108

703

What would you rather own for the next 5 years?

$GOOG at 20x P/E or $KO at 29x P/E

It's a no-brainer for me. The market is not always rational. Ignore the short term and focus on the long term...

78

44

658

Imagine. You pour $10B into a startup, which you then own 49%.

- The board replaces your star CEO, and you get 5-10 min in advance notice.

- The board used your biggest competitors' video call service instead of your market-leading one.

You are a $2.7T company Microsoft/ $MSFT.

37

69

651

Tomorrow my article on the Metaverse is dropping!

The picture is a small teaser.

Talking about interesting assets from an investor standpoint: $FB, $U, $NVDA, $AMD, $COIN, $ETH, $ENS, $SAND,

@BoredApeYC

& many more.

If you haven't subscribed yet 👉

26

137

642

Yesterday one of the MOST important partnerships in tech this year was announced, and it didn't get as enough attention as it should.

$META and $AMZN have partnered, and it's a HUGE deal for both companies. Here is why:

For the first time, customers will be able to shop

34

102

642

I have been researching NFT's the last few days. There is a lot of hype but some projects are here to stay.

The most important thing is that you like what you own.

And with that, I got myself a

@KoalaAgencyNFT

. I really like the community, the social cause and I love Wallas🐨

208

237

613

$META earnings are out:

- Revenue $40.1B (estimates $39.17B)

- EPS $5.33 (estimates $4.96)

- Net income $14B

-Guidance $34.5B-$37B vs estimates $33.8B

First ever dividend of $0.5 per share!

Blowout!!!

26

61

629

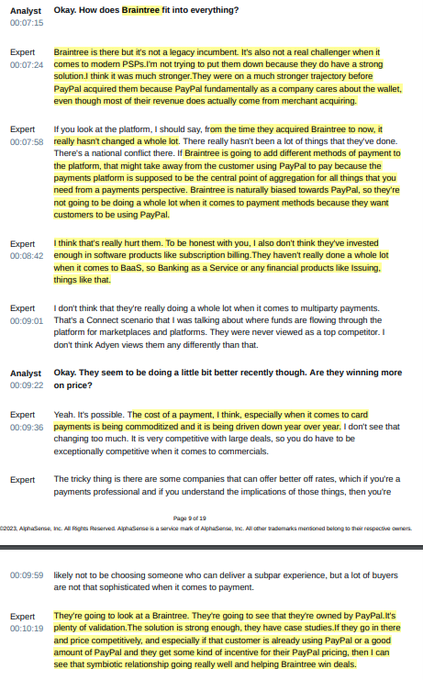

A really great interview from a current Account Executive at Stripe. Talking about $ADYEY and $PYPL. Must read for Fintech investors:

- In his opinion, $ADYEY is very efficient and good at high touch sales cycle, especially with enterprises and, more specifically, with

22

94

621

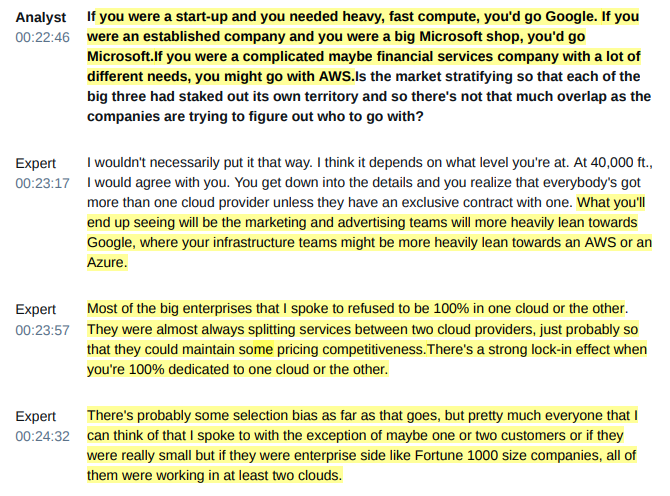

One of the most insightful interviews on the cloud industry from an industry expert director/cloud consultant:

- Clients pick AWS because they have the biggest “menu” and you can basically solve any problem you have on AWS.

- In his view, Azure is not necessarily the fastest

14

101

607

Everybody on Twitter seems to be an expert in social media & the future now. And Zuckerberg, the guy who founded social media as we know it and built a $650B company & whose products are used every month by 55% of the people in the world (ex-China), doesn't have a clue.

54

38

588

$FB EARNINGS:

Total Revenue $29B up 35%

Other revenue up 195% (Oculus)

Net Income $9.2B up 17%

DAU up 6%

MAU up 6%

Say what you want hate it all you want but they are growing 35% on the top line at $29B. Growth monster.

Super long $FB!

19

53

568

Great damage control done by $MSFT, especially Satya, who no doubt is brilliant, getting Altman and Brockman now on $MSFT, BUT...

There is no doubt that the whole situation is less optimal for $MSFT than it was before Friday. Here is why:

- OpenAI's tech is great, but one of

55

78

572

$SQ is valued at 12x EV/Gross Profit.

In 2019 the same multiple was 19x and in 2018 it was 24. But in the period the company has grown into a dominant market leader with Cash App and has increased gross profit by 3x.

$SQ reports earnings tomorrow.

Long $SQ

44

24

558

This is a list of the most interesting companies for the next 5-10 years for me. Valuation matters & these companies are definitely on my watchlist when the prices are right:

$NVDA

$SHOP

$FB

$PINS

$SQ

$COIN

$ABNB

$AMZN

$DOCN

$SOFI

$PLTR

$U

$SE

$PATH

$MTTR

$MTCH

$NET

$INTU

$AMD

44

82

558

Almost 1 year since the post:

$AMZN +60%

$GOOGL +59.7%

$META +242%

The smile is definitely there for us $AMZN, $GOOGL & $META long term holders…

23

22

554

My article on $META and its challenges is out.

- The rise of TikTok and what it means for $META,

- The Apple privacy change problems and monetization

- The Metaverse and its cash burn.

I also talk about the valuation and what is reflected in it.

44

103

534

Right now you are getting $AMZN at:

- AWS at $DOCN multiple

- Amazon Ad business at $GOOG multiple

- and Amazon e-commerce multiple at $WMT levels.

Not many times this juggernaut offered these price levels to investors.

Long.

43

37

504

The $PINS analysis is out!

- Unique user base (83% of young US women)

- E-commerce centric platform

- Growing user and revenue base (over 60%)

- Valuation and Price target (32%-110% upside)

$PINS bulls, feel free to retweet!

👇👇

37

133

521

$META is now trading at 11x EV/FCF (TTM).

Can't wait to look back at this in 2 years.

49

36

516

Investors don't fully comprehend how big of a physical infrastructure moat $AMZN has built over the years of intense CapEx spend in a low-interest rates environment.

Data centers, logistics, fulfillment...

Add their online moats & networks, and you have a 21st-century empire.

18

56

513

Very insightful interview from a former Global Lead at $AMZN - AWS and current $GOOGL employee:

1. $NVDA's biggest advantage is not hardware but software; it’s CUDA library.

2. The expert thinks $AMZN's AWS is playing it very smart with AI and its Bedrock offering. He also sees

14

89

507

$AMZN's ability to develop new huge business segments is really impressive.

- AWS: +$100B growing +13%

- Ad services: +$46B growing 26%

- Subscription services: +$42B growing 14%

Less than 20 years ago, this was just a ecomm website.

No reason to think they are done here.

29

50

485

Sundar Pichai of $GOOGL had a weird pause when asked about $PINS. And then later said “..I can’t comment on any M&A deal.”

Very interesting.

21

31

478

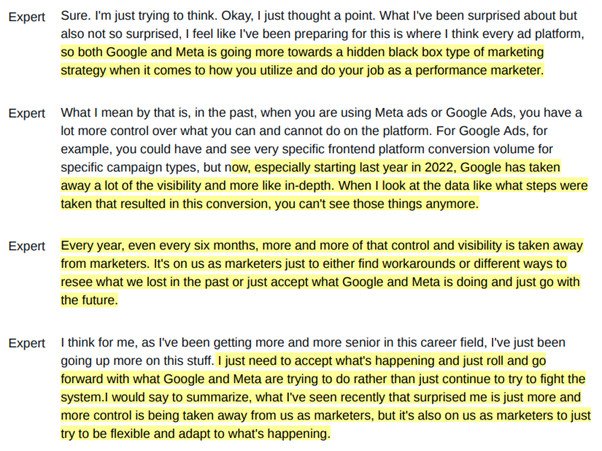

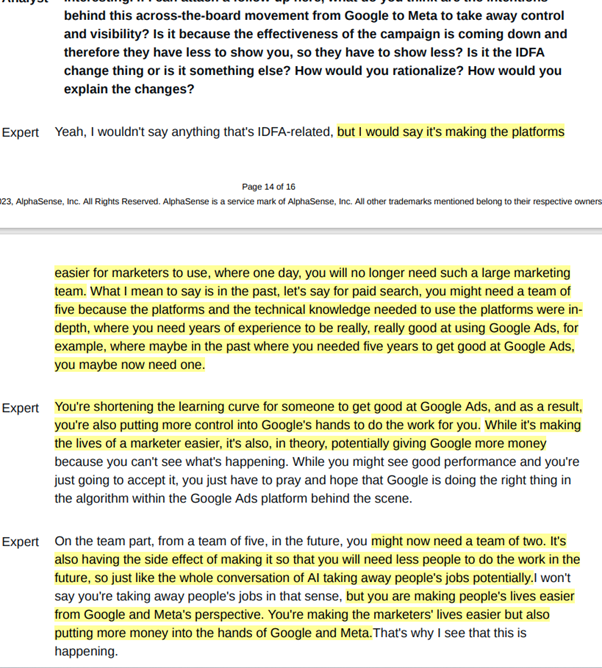

Really insightful interview with a former $GOOGL employee and ad industry expert explains what he is seeing from clients right now when it comes to ad spend - $META, $GOOGL & others:

- The expert gathers data from 190 advertisers who together spend $600M a year in US, Canada and

12

78

480

In the next few years, when CashApp will be used by almost everyone in the US and Europe, we will look back and say wow $SQ really traded for $85 in 2022...

47

21

474

$GOOGL is trading at 17x EV/Net Income if you reduce its net income from 2021 by -20%.

All that with the world's third biggest Cloud computing unit growing over 35% and not yet contributing any profit (even lowering core profit).

Truly remarkable times.

Long $GOOGL

27

30

469

A must-read interview for $PYPL and other fintech investors from a Former Director at $PYPL (worked there for 6 years until end of 2022). Because of so many insights, I will be posting it in 2 parts. Part 1:

- The expert shared that the internal indications & research say that

10

66

451

People that are selling $AMZN now down more than 20% from it’s highs will probably buy it back at higher levels.

Learned my lesson years ago.

36

15

455

For those people who still say "nobody" is using $META apps anymore.

MAU up 6% to 3.98B

DAU up 8% to 3.19B

Please let that sink in....

22

27

461

Zuckerberg’s internal comments on the $AAPL Vision Pro headset by the Verge.

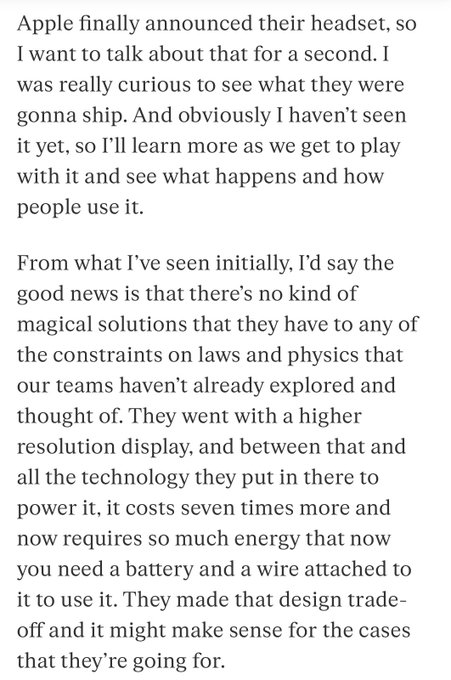

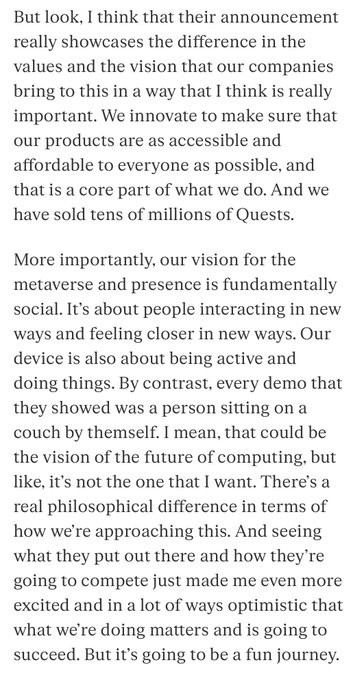

Key points:

- no new tech that $META doesn’t have

- fundamentally different approach. $META wants people to be connect and active & $AAPL demo showing only people doing stuff alone on their couch.

55

70

455

I love $NVDA's business and its current position, but I think the fundamental realistic upside given its valuation is limited at this point.

This is an oversimplification, but just so people understand it easier, this is a short back-of-the-napkin math:

Jensen himself thinks

102

74

454

I am sorry but $SOFI earnings numbers are very good. The financial service segment with user growth impressed me the most. I get that the market might not appreciate it given where the sentiment is right now, but the company delivered!

Long.

27

33

441

My $SQ analysis is out!

Interesting points from it:

- less than 3% of $SQ Seller ecosystem revenue comes from hardware

- Search data shows Cash App running away from Venmo

- Cash App as a stand-alone business could be worth more than $85B

Long $SQ

32

50

437

One of the best interviews I read.

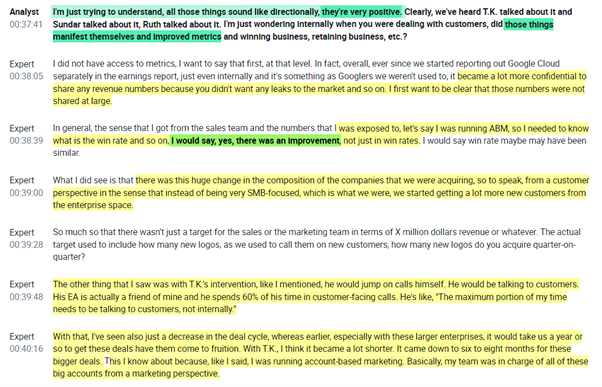

Former Global Head at $GOOGL /GCP who worked there for 7 years:

- $GOOGL's edge on AI

- Talks about CEO of GCP: T.K - 60% of the time on customer-facing calls

- Transition from SMB clients to enterprises

- Thinks $MSFT Azure will be num. 1

6

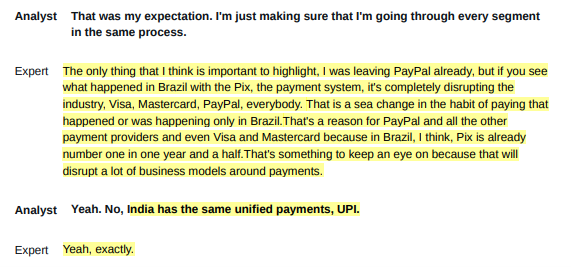

63

442

$AMZN will turn out to be a similar setup like $META was a few months ago IMO. Investors are over focused on the short term. The long term thesis just continues to grow with multiple oligopoly businesses (3P, cloud, ad, logistics)

$AMZN now overtook $META as my biggest position.

47

38

438

$GOOGL results are out:

Revenue $68B up 23% YoY

Operating income $20B up 30% YoY

Net income $16.4B down from $17.9B last year

Google Cloud $5.82B up 44% YoY.

Google Search revenue up 24% YoY

YouTube ads up 14.4% YoY

17

42

432

$FB is trading at 11x Operating Cash flow excluding Stock-Based comp.

As a long-term shareholder, I want the price to stay at these low levels and authorize the board with a new buyback program. With the cash flow, they can reduce the number of shares by almost 10% each year.

28

26

433

Let's clear one thing about $META.

Today's selloff has nothing to do with TikTok, because the core was better than expected (revenue, engagement, Reels traction, user growth). So the concept that nobody is using $META is wrong.

It's all about $META not willing to control costs.

46

26

436

$PINS monster quarter!

Q4 revenue up 76 YoY!

MAU grew 37%!

Look at the baby fly! Stock pops 10%

Long!

27

25

418

Added to my $AMZN position here, down more than 50% from the highs.

The stock market right now only focuses on the short term but that's ok, I don't.

39

14

424

HUGE news: $AMZN announces deal with Anthropic.

Chess moves are being played by the big guys.

$AMZN will invest up to $4B in Anthropic. At first, a $1.25B for a minority stake.

- AWS will be Anthropic's "primary" cloud provider

- Anthropic will have access to significant

20

51

419

Can’t really believe how much alfa long term investors will be able to generate from owning a big tech company like $FB in the next 3-5 years.

Remember today’s sentiment it will go down in the history books.

Long $FB

42

21

412

2 months of non-stop on Twitter: “Bing is killing $GOOGL in search everyone is switch search to ChatGPT-Bing…”

Meanwhile in the real world: “Google INCREASES Search Engine Market Share in February…”

Data > hype

24

29

419

9 months in - "There is no alpha in Big Tech" folks.

A portfolio of $AMZN, $MSFT, $GOOGL and $META will probably outperform most other portfolios in a 5 year time frame including all the indices.

Setting a reminder to circle back on this call in 5 years.

96

38

742

27

34

420

A very informative interview with a Former $META director; a MUST read for $META investors as I highly agree with the views of this expert:

1. He thinks that now you are seeing a ton of parity around Reel consumption vs. TT for many key demographics. In $META, there is a large

11

60

418

Selling $GOOG -6%, $META -8% and $PINS -14% based on the fact that $SNAP ‘s management doesn’t know how to guide and doesn’t have any foresight in the industry is a stupid reason.

$SNAP never was and never will be a bellwether for the ad industry.

34

39

412

Got to be honest. $SQ earnings call got me excited. Especially the part where CashApp can now with Afterpay even tap into social commerce with leads and potentially even adtech.

Not to mention the CFO Amrita Ahuja is a gem! Clear, precise & on point! Should be CEO...

Long $SQ

22

22

390

Here is my view of $META's great Q4 earnings results and what the most important things are going forward for the company:

1/7 Headline numbers

- Revenue up 25% YoY to $40.1B

- Net income up 201% YoY to $14B

- Family daily active people 3.19B up 8% YoY

- Family monthly active

27

58

402

1) Went through $FB/ $META earnings and the call. The quarter and the guidance were not good, but the 23% selloff in the stock is a big exaggeration IMO.

$FB went from 20x to now 17x P/E, which is ridiculous.

31

35

388

This week I became a father. Truly a one of a kind feeling! I am full of gratitude and joy. Life goes fast so don’t forget to live it. ❤️

53

1

398

Anthony Noto, the CEO of $SOFI, buying almost $1M of $SOFI stock today certainly sends a strong message.

24

30

396

IMPORTANT LESSON from the 1st lockdown:

The waves of buying “Stay At Home Stocks.”

1. wave: Buying "pure" stay at home stocks - $NFLX, $AMZN, $ZM, $WMT, $SHOP

2. wave: Buying stocks that help online business thrive - $TWLO, $FSTLY, $DOCU, $OKTA, $TEAM, $CRWD, $ZS , $NET $NOW

20

75

389

Looking forward to the day when $AMZN surprises investors with its earnings with an 8%-10% profit margin on e-commerce and investors suddenly realize $AMZN is valued at 24x P/E with a growth of 15-20% in one of the most attractive industries out there (cloud, e-commerce, ads).

32

26

392

The $META letter from Zuck is the key turning point for the stock IMO.

- 13% workforce layoffs (ALSO in Reality Labs unit)

- Commitment to reduce costs

- and this: "a path to achieve a more efficient cost structure than we outlined to investors recently"

Long $META

17

28

393

What great times for long-term investors those were.

Returns since the post (1 year and 3 month):

$META +336%

$AMZN +76%

$GOOGL +76%

Having a long-term mindset is an advantage.

19

13

390

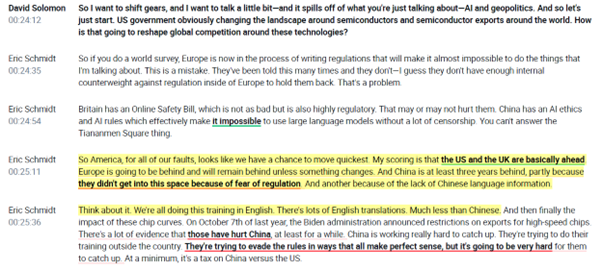

This one is a real treat. An exclusive interview with former decade long $GOOGL CEO Eric Schmidt on Generative AI:

- Explains that the next scale goal is LLMs that will cost $1B to train (from $100M ones that we use today) and that we could be looking at $100B ones in the

7

75

391

I hope $META is ramping up the buybacks at these levels.

Investors are extremely short-sighted…

$META is a profit and FCF machine and will continue to be…

Long.

29

23

377

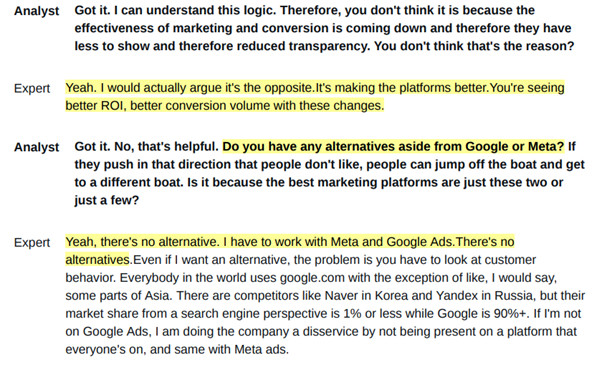

Another display of the power that $GOOGL and $META have in the ad industry and the change that is going on.

Senior Performance Marketing Manager at Udemy explains how he views using the ad platforms:

- There is really no real alternative to $GOOGL & $META on the ads front.

10

42

385

Remember these prices when it comes to $AMZN, $GOOGL, and $META.

If you can zoom out and have a horizon longer than 3-6 months then you will smile in the future IMO.

39

15

382

$AMZN just brought a Trojan Horse inside $SHOP with "Buy With Prime" now in Shopify.

The end goal of all this is simple: Everyone to become Prime members & even more scale on logistics for $AMZN. Economies of scale 101.

As a $AMZN shareholder, I absolutely love it!

17

26

378

Big news. $SQ and $AAPL partner to bring Tap To Pay on iPhone within the Square Point of Sale app.

Seems the fear of $AAPL eating $SQ lunch was overblown.

Long $SQ

15

46

374

$META earnings are out:

- Revenue $32B up 11% YoY

- EPS $2.98 up 21% YoY

- DAUs 3.07B up 7% YoY

- Guidance 3Q rev $32B-$34.5B estimates $31.18B

Growth is back! Great quarter! looking forward to the conference.

Long!

14

36

378

1) My investment strategy:

My portfolio is mainly focused on growth (primarily Tech) stocks. I invest in businesses that are disrupting an industry, are in a leadership position, and have low competition. Because of my background, I prefer to invest in software tech.

(THREAD)

45

66

367

$NVDA is not just a GPU provider. In the last few years, it has developed into an AWS-like computing platform.

Never thought that the Big Tech players like $AMZN, $GOOG, $MSFT could be intimidated by any company.

But I really think they should fear $NVDA.

16

25

371

The Phases of $FB:

Phase 1: Ad platform

Phase 2: +Shopping and payment platform

Phase 3: +AR/VR hardware platform

Phase 4: +Metaverse App store

So basically $FB becomes ( $FB + $AMZN + $AAPL ) in one company.

17

46

366

$FB $GOOG and $PINS now have almost the same forward P/E in the low 20s. At the same time, their revenue growth for the fiscal year is in the 40% range.

But yeah, owning a $PG with 27.5x P/E and 7% top-line growth (record high in last 4 years) makes more sense.

41

40

365

Pausing just for a minute to appreciate that $AMZN has build and pioneered two different +$100B businesses under one company in less than 20 year.

Truly amazing!

6

20

367

Former VP at $MSFT, who worked there for over 20 years, shares his views on the cloud industry:

1. Explained that Satya believes we are still in the early stages of cloud computing and that TAM will grow significantly.

2. $AMZN - AWS is strong with born-in-cloud companies

6

58

369

$GOOGL is hiking YouTube Premium plans for new users in the US by $2 to $13.99.

Even if they hiked prices by 100% for new and existing users, the churn rate would probably be close to zero. One of the best value-for-money services out there.

$GOOGL just showing pricing power.

20

32

371

$FB under $190 really was a gift for long-term investors. Even at this levels still is IMO. Investors pricing only negative outlooks for the company. Not to mention giving zero credit to Mark Zuckerberg, when he has proven time after time he knows where to invest & grow.

Long.

25

17

358

My article on why I sold $GOOGL is out. The Innovator's Dilemma is real.

- Definition of LLM's as disruptive tech to Search

- The "moat" is not the same anymore

- Alternatives to Search on the rise

- What $GOOGL needs to do and what that means for investors.

Link in next post.

56

49

359

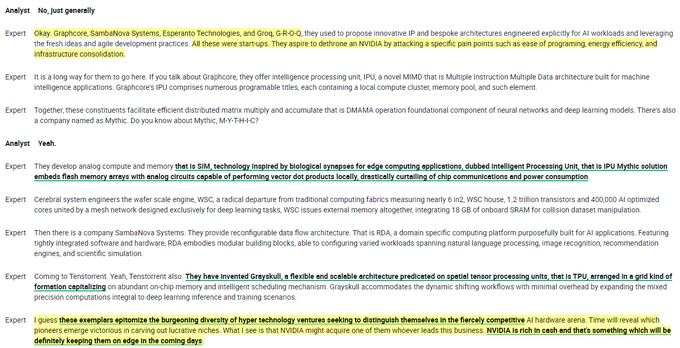

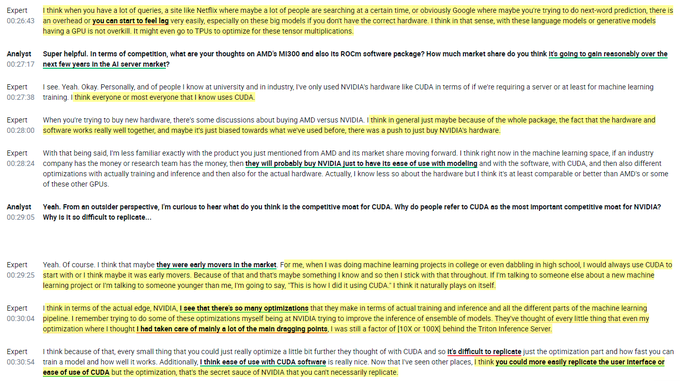

Interesting viewpoints from a Former $NVDA employee on AI infrastructure:

1. He sees bottlenecks in the supply chain, with $TSM and other companies essentially having a monopoly.

2. You have a few big companies training their own LLM models, and then you have smaller companies

16

69

363

Today feels like a great day to remind myself of the great times little over a year ago. Since then:

$META +262%

$GOOGL +63%

$AMZN +61%

You can’t make alpha in big cap…sure.

I am not the only one with a smile.

27

7

359

My hairdresser told me the economy is headed towards a recession.

60

12

343

Interview with a Former Unit Head at $META. I strongly agree with what he said, as most of the viewpoints are something that I already shared in my posts and articles:

1. $META's value proposition is that you can reach most user segments at scale. In his view, $AMZN has the best

8

52

358

$GOOGL earnings are out:

- Revenue $76.69B up 11% YoY

- Net income $19.69B up 42% YoY

- Google Search $44B up 11.4%

- Youtube ad revenue $7.95B up 12.5% YoY

- Google Cloud $8.41 up 22% YoY

17

33

352

$COIN is probably going to earn more than $6B on an annual basis this year. It's trading at 13.5x P/E.

And this includes no revenues from the NFT marketplace or the $FB custody deal or anything else.

Yeah, it missed earnings but this is really not a short-term play.

Long.

14

16

348

I hope $FB is ramping up these purchases of the buyback program at these levels. The stock is trading at a 12x ex-cash P/E...ridiculous.

26

15

347

$SHOP to sell its logistics business to Flexport.

As I said many times, nobody has the resources to build out the logistics network that $AMZN has built in the last 3 years.

It's such an important physical moat for $AMZN, which will yield results in the future.

22

20

351

$META went from defense to pure offense.

Last year it was “TikTok will end $META” sentiment.

This year $META:

- Reels growing faster than TikTok taking market share

- Big LLM possible winner

- now ready to launch a Twitter like text app.

Zuck is a beast.

25

23

348

On a recent podcast, Zuck said that $META is spending at least $15B on AI and $15B on the metaverse.

What most investors still don't understand is that despite the big run in the stock price, $META is still attractively valued.

$META is going to do at least $52B in net income

24

39

352

@saxena_puru

Puru with all respect I do miss more of your stock tweets. Not taking any sides on this crypto theme just hoping for some more of your stock tweets because a lot of them have been great!

8

1

342

$AMZN logistics network will turn out to be one of the biggest moats in history.

They spent $61B in Capex in 2021. Out of that, $18B to expand their fulfillment capacity. In 2022 $AMZN Capex even increased to $63.6B.

There is not a single company out there that is willing to

19

37

339

$AMZN launching same-day delivery of prescription medications in NY and LA.

Another industry getting disrupted by $AMZN.

Love this company.

7

23

344

$PYPL expanding and adding a lead/ad platform to their products and leveraging all of their e-commerce purchase data.

No idea why the market doesn't like what $PYPL just introduced I for one like it.

Also, bear in mind

@acce

, the new CEO, just shipped more in the last 6 months

46

32

342

$GOOGL earnings are out:

Revenue $74.6B (+7% YoY) estimate $72.82B

Net income $18.39 (+15% YoY)

Google Cloud $8.03B (+28% YoY)

YT ad revenue $7.67 (+4.4% YoY)

Really nice quarter ad growth is back, cloud remains strong.

Long.

9

41

343

$META producing $13.6B in FCF this quarter tells you everything you need to know long-term about this business.

14

23

340

My analysis of SoFi and $IPOE is out:

- detailed explanation of the company

- valuation of each segment (Lending, Financial Service, and Galileo)

- why I started a position

👇

28

42

341

Added to $SQ. Love the valuation 16.5x EV/GP. It's trading at a similar valuation as it was 2-3 years ago, when CashApp was an "unproven" app, now basically the market leader.

Dominant market leader in a big TAM industry at a reasonable valuation, I'll take it any day.

Long.

22

16

332

$ABNB just a great company dominating its industry with no Big Tech as a competitor and a great CEO.

Rare breed.

Long.

23

10

335