Pavel | Robuxio

@PKycek

Followers

11K

Following

6K

Media

2K

Statuses

7K

Providing institutions and individuals access to fully automated algorithmic crypto portfolios with institutional-grade infrastructure | CEO @robuxio_com

Get our trading playbook ➜

Joined September 2021

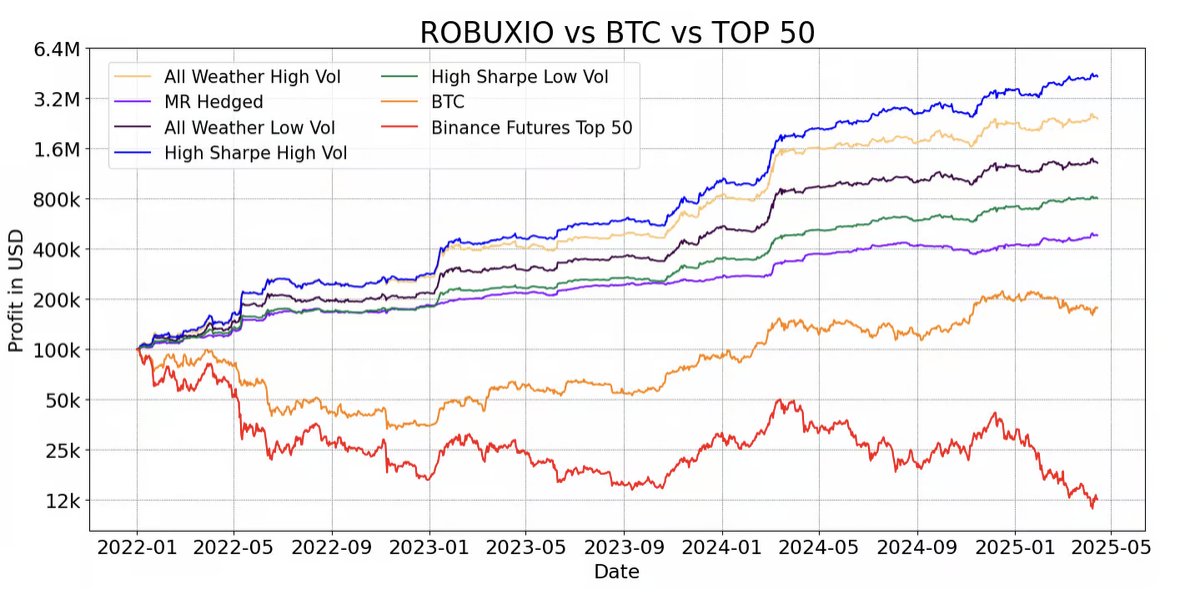

Crypto is the most profitable asset class for traders. But it's maturing fast and the edge won't last forever. Here’s how you can build, test, and deploy systematic portfolios that survive every regime:

158

238

2K

Don't ignore how strategies correlate in drawdowns. A strong correlation can amplify drawdowns. If they are correlated, assign them smaller weights in the portfolio. Always prioritize risk management over absolute profit.

0

3

14

Bottom line:. Like casinos, traders win by controlling exposure. Ignore risk of ruin, and it’s only a matter of time before the market takes you out.

0

0

2

Trading works the same way. • One oversized bet = casino scenario 1. • Spreading risk across many trades/strategies = casino scenario 2. Capital allocation, not just entry signals, decides survival.

1

0

2

Risk of Ruin = the probability of losing all your capital and being forced to stop trading. To illustrate, imagine you own a small-town casino with $1M in cash. You’re running roulette, where the chance of red/black is ~47%.

1

0

0

Most traders obsess over returns. Few think about the one metric that decides if they’ll even survive:. Risk of Ruin. Here’s why it matters, and how casinos use the same logic to stay in business:

4

1

13

One breakout coin can lift an entire portfolio by tens of percent. That’s the power of diversification in crypto.

0

2

1

2/ Catching positive outliers. No one knows which absurd token will breakout next. Here's an example where we caught JUPUSDT for triple digit gains.

1

0

3

1/ Risk reduction. Holding >10% in a single project is too much exposure. Any coin can drop 50–70% overnight, especially low-liquidity names.

1

0

0

We have a full article on all of these biases here:.

robuxio.com

Navigate Survivorship, Hindsight, Sample, Selection, Look-Ahead, Recency biases, and Curve Fitting in crypto trading for sound strategies.

0

0

4

Most common trading biases:. • Survivorship Bias.• Hindsight Bias.• Sample Bias.• Selection Bias.• Look-Ahead Bias.• Recency Bias / Market Condition Bias. If you don’t understand these, you probably shouldn’t be trading.

4

0

23

I post daily insights on trading and getting robust crypto exposure. If you want to learn more, make sure to give ma follow. If you want to help others, consider retweeting the first tweet below.

Your worst drawdown is probably still ahead of you. Here’s how to prepare for it and why your backtest could be lying to you:

0

0

5

That's why I always recommend running a diversified portfolio of uncorrelated strategies. It will significantly dampen the drawdowns and make your trading easier emotionally.

1

1

5

Here’s a simple rule of thumb based on years of observation:. For a single strategy → expect future drawdowns up to 1.5x – 2x the backtest. For a diversified portfolio → allow 1.25x – 1.5x more.

1

0

3

Run 1,000 Monte Carlo simulations, and you’ll get a better idea of your maximum future drawdown. Still not 100% accurate, but much closer to reality than a single backtest. Don’t want to run Monte Carlo?.

1

0

2

Use Monte Carlo simulation to estimate future drawdown risk. It randomly reshuffles your trade results across thousands of iterations to simulate possible future outcomes. But how many simulations?.

1

0

4

Backtested drawdowns often look too good to be true. That’s because they usually are. The shorter your data set, the more optimistic your drawdown stats. That's why I recommend the following:.

1

0

2